Regulation

Cleveland Fed Retracts Their Report on P2P Lending

November 18, 2017Here’s something you don’t see every day. A paper published by the Federal Reserve Bank of Cleveland about peer-to-peer lending was so dubious, that it has been taken down.

Since working paper no. 17-18 and related commentary on peer-to-peer lending were posted on our website on November 9, the authors have received several questions about the composition of the underlying data set they used in their analysis. In light of the comments received, the authors are currently revising their paper to further clarify the data sample they used in the study. Their revised paper will be posted as soon as it is completed.

– Federal Reserve Bank of Cleveland after analysts poked major holes in their findings

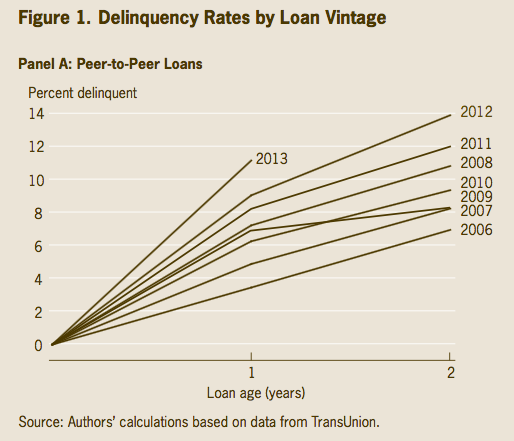

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

“This chart shows that the lowest delinquencies from P2P loans occurred in 2006. Really?” Renton wrote on his blog. “I am sorry but this is just plain wrong and I challenge the authors to show me the actual data this is based upon. In 2006, the only consumer P2P lending (or any significant online lending) platform in existence in this country was Prosper and their 2006 vintage was terrible.”

Nat Hoopes, executive director of the Marketplace Lending Association (MLA), was even more vocal. In an op-ed he wrote for American Banker, Hoopes says, “In our view, this paper — ‘The Taste of Peer-to-Peer Loans’ — and its accompanying materials show that a lack of precision and understanding of subject matter can result in significant inaccuracies. The report’s authors presented findings that seemed to reflect issues with the P-to-P industry, but they actually relied on data from a much broader category of loans. The result was a misleading and brutally critical report about the P-to-P industry that was actually based in part on data from more traditional loans.”

Online lenders had reason to fret over the report as the Cleveland Fed did more than just publish charts. “P2P loans resemble predatory loans in terms of the segment of the consumer market they serve and their impact on consumers’ finances,” the Fed concluded. “Given that P2P lenders are not regulated or supervised for antipredatory laws, lawmakers and regulators may need to revisit their position on online-lending marketplaces.”

The worst offense, according to MLA’s Hoopes, was that the data the Cleveland Fed relied on was not even p2p lending data. A senior VP at Transunion had reportedly admitted that the data used comprised of both traditional loans and online loans that had been requested by the Fed a long time ago to use for a different study.

Oops.

CFC on the Front Lines of the MCA Regulation Battle

November 6, 2017

As the US Senate attempts to reach a bipartisan agreement on relaxing some of the rules in the Dodd Frank legislation of 2010 that would treat banks more favorably, the MCA industry is having to fend off legislation and regulation of its own at the state and federal levels that could position funders in a similarly crippling position.

MCA regulation has been thrust into the spotlight for a number of reasons, not the least of which has been the Consumer Financial Production Bureau (CFPB). The CFPB is moving forward with the Dodd-Frank Section 1071 rulemaking process for data collection regarding small business lending, a sector of the market for which they do not have jurisdiction, sources say.

Front and center in the policy discussions has been the Commercial Finance Coalition (CFC), a merchant cash advance trade association that is coming up on its two-year anniversary in December. While federal policymakers appear to be listening, state legislatures have been a more difficult nut to crack.

The CFC’s Influence

In its short two-year history, the CFC has been one of the most vocal if not the most influential trade organization lobbying on behalf of the MCA industry, having attended 70 congressional meetings and having led advocacy efforts for the industry in the halls of Albany, Sacramento, Illinois and Washington, D.C.

Dan Gans, executive director of the CFC, has been the voice of the MCA industry on Capitol Hill and has been invited to testify in key congressional hearings. “For whatever reason, the CFC has really become the voice and has taken an active part in the so far successful advocacy efforts to educate and mitigate potential harm to our members’ ability to deploy capital to small businesses that need access,” Gans told deBanked.

Most recently the CFC participated in a fly-in, one of two such events this year, to Washington, D.C. in which the association’s counsel Katherine Fisher of Hudson Cook, LLP testified.

In her testimony Fisher said: “The MCA and commercial lending spaces are sufficiently regulated by existing federal and state laws and regulations. Both MCA companies and commercial lenders must comply with laws and regulations affecting nearly every aspect of their transactions, from marketing and underwriting through servicing and collection.”

She went on to explain: “Even if they comply with every applicable law and regulation, small business financers must also be wary of the Federal Trade Commission’s powerful authority to prevent unfair or deceptive acts or practices.”

Fisher told deBanked she received a “positive” response to her testimony from funders but has not heard anything from lawmakers.

Gans said Fisher did a fantastic job in articulating the needs and status of the industry.

“She presented a very good case as to why the industry is currently adequately regulated. We don’t feel there is a need for federal regulation. In some cases, less regulation would allow our members to deploy more capital and help more small businesses,” Gans said.

The sweet spot for MCAs, Gans explained, are transactions under $100,000 and probably in the $24,000 – $40,000 range. He said the industry does a fantastic job of being able to deploy financial resources to small businesses in a timely manner that neither banks nor SBA lenders can match. He’s not suggesting MCA is for everybody but for some businesses it’s an essential product that can help. There have been many success stories.

“Competition is all over the place. But that’s great for the merchant. The more options that merchants have, the more we can enforce best practices and more competitive rates. And the more we can keep the government from impeding people from getting into this space, the better off small businesses are going to be,” said Gans.

Setting the Record Straight

The CFC was formed with the mindset that the organization, which is currently comprised of CEOs of small- and medium-sized funders, would take a proactive rather than a reactive approach to industry regulation. In its two-year history the CFC has tasked itself not only with educating policymakers on the role of MCA funders for small businesses but also with undoing the misinformation and misconception surrounding the anatomy of an MCA.

“Unfortunately, because MCA uses the term cash advance in its product name, uninformed people will often confuse MCA as some form of payday lending. And so that has been one of our biggest challenges, educating members of congress and committees that there is absolutely no correlation between MCA products and what their views of consumer payday loans is,” said Gans, adding that the CFC has had to communicate that MCA is a version of factoring has been around for more than 1,000 years.

A common thread that the CFC has been able to weave with lawmakers has been the diverse geographical representation of both the trade group and the House and Senate.

“Most venture capital is deployed in a few spots – New York, California and Texas – and it’s a cliff to get to those three states. So, one nice thing that I take pride in is my members are looking all around the country regardless of the geographic location. That helps us with policymakers, most of whom are not from the New York City metropolitan area or Silicon Valley. It’s nice being able to look at them in the eye and tell them we care just as much about your district as you do,” he said.

The Road Ahead

The CFC has an ambitious long-term agenda, one that includes raising their profile in the industry and participating in events.

“I think one of the ambitions we have is to have an organization where funders and brokers can be at the same table and work though some of the issues impacting the industry and try to make sure people are doing things in the right and best way.”

The trade group is planning to partner up with deBanked for Broker Fair 2018 and they’re looking to bolster membership.

“The industry has had a lot of free riders that are benefiting from our advocacy efforts but not supporting it. So, from my perspective, if you’re in this industry, particularly in the MCA space, we’d like to expand membership. If we grow our membership, we can do more things, engage more states and expand our lobbying team,” said Gans. “The more members we have, the more we can do to advance the ball and protect the interests of the industry.”

The CFC will need all the help it can muster given the fight ahead to fend off regulation particularly in Washington, Albany and Sacramento. “I think we could see some harmful regulations and potentially legislation over time. Some of those bad ideas that emanate in states have a tendency to percolate into Washington. If at some point there is a less business-friendly administration in the future, we could see all those ideas get some traction at the federal level,” Gans warned.

House Small Business Committee to Hold Hearing on Online Lending

October 22, 2017On Thursday, October 26th, a House subcommittee on Economic Growth, Tax and Capital Access will be holding a hearing about online lending’s role in improving small business capital access.

The two witnesses scheduled to testify are Kate Fisher, a partner at Hudson Cook, and William Phelan, the president and co-founder of PayNet.

deBanked will attempt to stream the hearing LIVE on our home page. It begins at 10 AM EST in the Rayburn House Office Building.

CFPB’s Small Business Lending RFI is Now Closed

September 18, 2017The window to share your two cents on the CFPB’s quest to collect data on small business lending has closed. The extended deadline to respond to the RFI was September 14th.

The agency received 2,668 comments, 650 of which you can read online. Most responses that deBanked reviewed asked the CFPB to exempt certain businesses such as community banks from the law. Others denounced the CFPB’s objective as misguided or poorly thought-out from the get-go.

Nevertheless, Section 1071 of the 2009 Wall Street Reform and Consumer Protection Act directed the CFPB to collect data on small business lending presumably to determine if women and minorities are treated differently.

Some observers expected this initiative to be derailed when Richard Cordray, the Director of the CFPB, resigned to campaign for Governor of Ohio. However, the governor’s race is now in full swing and he has yet to resign, and could now possibly remain in his position until it expires next year.

The implementation of any resulting rule from the RFI would likely not take place until some time in the 2020s, sources contend.

Senate Banking Committee to Hold Hearing on Fintech

September 12, 2017The US Senate Committee on Banking, Housing, & Urban Affairs held a hearing entitled “Examining the Fintech Landscape” on Tuesday morning at 10 AM.

You can watch it below

The witnesses include:

Mr. Lawrance Evans

Director, Financial Markets

U.S. Government Accountability Office

Mr. Eric Turner

Research Analysis

S&P Global Market Intelligence

Mr. Frank Pasquale

Professor of Law

University of Maryland Francis King Carey School of Law

Was Section 1071 of Dodd-Frank a Massive Mistake?

August 23, 2017Did Congress make a huge mistake by thinking small business loans were easily commoditized?

Pursuant to Section 1071 of Dodd-Frank, the CFPB is planning to collect data from companies engaged in small business finance in order to potentially screen for discrimination against women and minorities. Before deciding how exactly they’re going to do that, they’ve asked the public for comment, and the public… isn’t showing the law much love. Below are some excerpts of the nearly 300 responses already submitted.

We can tell all the stories we want, and hold all the hearings imaginable, and there is still no way to disguise the fact that implementing a HMDA-like reporting requirement will add cost, complexity, and rigidity to our amazingly customized lending

– Alan Gay

A loan priced properly for the risk may be acceptable for one institution and not acceptable to another. For example a client requests funds to open their second doughnut shop in town. One bank declines the loan because they do not specialize in food service business per lending policy and the banks appetite for risk. Another bank would consider the loan, however after reviewing the current competition decides that the market is saturated and the loan is too risky based on the three competitors within five miles. The third bank is willing to loan the money based on the cash flow of the owner and her husband, but will not take into account the expected cash flow from the business, and will require the collateral to include the primary residence of the client. The fourth bank is an SBA lender and proposes the client use the SBA program to mitigate the risk for the bank. The fifth bank declines the loan due to cash flows. They will not consider the revenues from the new location, because it is considered a start-up business. As I understand it the CFPB will collect the data from all five banks to determine “Fair Lending” similar to the consumer lending program. I find this problematic on many levels: I believe in the scenario presented all the lenders were fair. The data is redundant and will not show the result of credit search on the commercial loan request or accurate results.

– Doug Mitchell

Creating additional documentation and regulation only makes those in Congress and the CFPB feel better without truly adding benefit to our community and it’s businesses.

– Joseph Williams

COLLECTING AND AGGREGATING THIS INFORMATION WOULD BE A BURDEN THAT WOULD REQUIRE ADDITIONAL STAFF AND NOT CHANGE OUR HISTORY AND BUSINESS MANDATE OF SERVING OUR SMALL TOWN BUSINESSES.

– Dee Baertsch

As a community banker in rural Ohio I strongly urge the repeal of Section 1071 of the Dodd-Frank Act. The addition of another report will be counterproductive to lending to small businesses.

– Chuck Dixon

Commercial lending is a completely different animal from consumer lending, and has so many different aspects to consider. While a consumer loan is typically viewed from and ability and intent to pay by reviewing a consumer credit score and debt to income calculation, a commercial loan is viewed from not only current earnings but also projected earnings, the economic conditions surrounding the specific business/industry, competitiveness in the market, and the speed of obsolescence of the business’ products and services. It is so much more than pulling a credit report and getting the last two pay stubs.

– Brian Smith

The Race and Sex questions should be eliminated from all loans.

– David Ludwig

Our bank in particular will be unduly burdened by small business lending data collection.

– Casey D. Lewis, CRCM, First Bank & Trust

This new requirement will place a large burden on our small bank and staff as more time will be spent on data collection and reporting rather than giving the value added service to our actual customers. It also may increase the cost of credit to our borrowers in order to offset the increased compliance cost to comply.

– Anita Drentlaw

These regulation proposed by the CFPB will only act to hamper and restrict our ability to continue meet the credit need of our communities and will not provide any meaningful benefit to anyone.

– Jim Goetz

Adding new requirements to collect and report data related to these loans much like HMDA diverts time of our limited staff away from serving our customer needs and expends resources that do not help our community.

– James Milroy

The last thing I need is to spend even more of my time collecting data similar to the HMDA data we collect on other loans. It is a timely, costly and inefficient use of our resources which could be better utilized for spending more time with potential and current customers and lowering their interest rates. Very few businesses are the same which would lead to misrepresentation and baseless fair lending complaints.

– Daniel Mueller

By making our jobs harder, you are making it harder for small businesses to thrive.

– Joy Blum

I have seen first hand the negative effects of the HMDA collection and reporting to our bank. The increased work for our small bank has driven up our costs and is making it harder for us to compete. In addition to the negative impact on our bank mortgage customers pay a cost and as more and more community banks decide they can no longer provide these services the community will be left with fewer options.

– Jeff Southcott

Stop all the paper work to get a commercial loan. Enough is Enough!

– Jeff Spitzack

We are a small $65 Million dollar bank with limited personnel now being asked to police another segment of our customer base. We do not have the resources to carry out more regulatory burden.

– Girard J. Hoel, Chairman, The Miners National Bank of Eveleth

Commercial lending cannot be “commoditized” in the way that consumer lending can, nor can it be subject to simplified, rigid analysis which may generate baseless fair lending complaints.

– Steve Worrell

We are so heavily burdened with keeping up with all the changing regulations and requirements, it would be very burdensome for not only our bank, but many other community banks. There has to be a way to ensure the end results that you are looking to achieve without making it so hard on Community Banks. We feel that we have to really analyze if it is cost prohibitive to actually make the loan – and how does that help the small businesses?

– Margi Fleming

We would never decline a profit making loan because of the race or sex of the applicant. You would be appalled to know how little attention borrowers pay to the dozens of pages of disclosures required by regulation. Over disclosure is no disclosure.

– Douglas Krogh

Community banks simply do not have numbers on our side, either in manpower or funding, to seamlessly and efficiently absorb the vast and sweeping regulatory changes.

– Cheryl Hiller, 1st National Bank of Scotia

The new data collection will add additional staff at our institution. This salary will be passed on in the form of origination fees or increased rates to our small business customers. This is not fair to them, but with the increased regulatory demands by the CFPB on small business lending if this is adopted will increase their borrowing cost.

– Russell Laffitte

The burden of data collection and reporting would in effect end up costing our customers more to get a loan.

– Shannon Fuller

This tracking will be onerous on a small bank that stays competitive by maintaining a small staff like ours

– Jim Legare

Section 1071 will have a chilling effect on lenders’ ability to price for risk. This, in addition to the expense of data collection and reporting, may impact community banks’ ability to provide affordable commercial lending products and curb access to small business credit, an engine of local economic growth and job creation.

– Freeman Park

Please make every effort to prevent the added burden to small business lending and community bank processes by repealing Section 1071 of the Dodd Frank Act.

– Julie Goll

The Employee Suing SoFi Only Worked There for Three Months

August 15, 2017On Monday, several news outlets reported that a former employee of SoFi was suing for wrongful termination after he not only reported sexual harassment in the workplace, but also exposed an internal loan cancellation scheme designed to pad the bonuses of certain employees.

According to the complaint, which you can read for yourself here, plaintiff Brandon Charles learned of the loan scheme within 2 weeks of being hired and was fired only 3 months later in June of this year.

According to The New York Times, Charles’ attorney said he expects to bring another lawsuit, a class action, against SoFi next week for broad mistreatment of employees.

These events come just as SoFi had started teasing about a possible IPO in the near future.

You can read Brandon Charles’ complaint here and reach your own conclusions.

The CFPB is Asking The Wrong Questions, Bank President Says

July 13, 2017David Ludwig, the Bismarck branch president of Security First Bank of North Dakota, responded to the CFPB’s small business lending RFI earlier this week. In his written comment, he points out the futility of examining race, gender and ethnicity to judge how a lender is approving business loans. These data points are what the CFPB is hoping to gather pursuant to Section 1071 of Dodd-Frank to examine potential discrimination.

“The bureau appears to only want to know the applicants’ income, sex, race, amount of request and if the loan was approved or not,” he wrote. “Some people have less education, less ability, less equity and not so good credit history. These are not sex or race issues.”

Ludwig says there is no place for discrimination in lending and that if the CFPB was really interested in attributes about business owners that may be impacting their approvals, they should be asking about the owners’ work history, education, equity in the business, loan purpose and other related questions.