Announcements

Yellowstone Capital Has Record Month

September 1, 2017Yellowstone Capital had a “record smashing August,” according to a post on Instagram. They originated 1729 deals for a total of $55.5 million. The top rep recorded 161 deals for $4.62 million. Juan Monegro, who was previously interviewed by deBanked, originated 202 deals for $3.7 million.

The Alternative Finance Bar Association Announces September 13th Event

August 31, 2017An announcement from the AFBA:

Download Save The Date PDF

SAVE THE DATE

Location: NYC Bar Association Offices

42 West 44th Street

New York, NY 10336

When: September 13th

Date: September 13, 2017

LOCATION: NYC BAR ASSOCIATION OFFICES

Clark Hill’s Consumer Financial Services Regulatory & Compliance Practice Group is a national leader in the field of consumer financial services law, providing strategic legal counsel to clients in all areas of consumer and small business finance. We provide advice, consultation and litigation services to a wide variety of financial institutions throughout the country. Our exceptional team of lawyers as well as government and regulatory advisors has extensive experience in – and an in-depth understanding of – the laws and regulations governing consumer financial products and services including engagement with the Consumer Financial Protection Bureau and prudential regulators.

Credibly Selected to Service Bizfi’s $250M Portfolio

August 30, 2017

Credibly also announced that it has crossed the $500 million milestone in capital deployed to tens of thousands of SMBs across the U.S. This is separate from the $250M portfolio the company is now servicing from BizFi.

“Acquiring the servicing rights of BizFi’s portfolio is a testament to our data-driven approach and laser focus on the working capital needs of small businesses,” said Ryan Rosett, Credibly’s Founder and Co-Chief Executive Officer. “We welcome our new customers and are committed to ensuring that their growth capital needs are met.”

In addition to servicing the BizFi portfolio, Credibly is working with both sales partners and merchants to provide additional working capital to the businesses in BizFi’s portfolio. Credibly’s data science team has the ability to analyze BizFi’s twelve years of data and remittance history, which will allow Credibly to better service both the BizFi and Credibly portfolios. Further, BizFi’s data enhances Credibly’s risk management, scoring models, and portfolio management tools.

The Small Business Association (SBA) estimates that traditional banks still reject approximately 90 percent of SMB loan applications. Since 2010, Credibly has emerged as a proven platform that leverages data science and analytics to provide SMBs with a simple and intuitive way to access critical working capital. The company addresses the fundamental capital needs of SMB owners across a broad credit spectrum and through every stage of a business’s life cycle.

Main Street SMBs across a wide variety of industries that include restaurants, retail stores, salons, spas, dry cleaners, auto body shops, and doctors’ offices, all rely on Credibly to secure the necessary capital they need to grow.

Credibly has achieved widespread industry recognition for its risk management, data technology, and data driven approach. For more information on Credibly, please visit www.credibly.com.

About Credibly

Founded in 2010 and with offices in Michigan, Arizona, Massachusetts, and New York, Credibly is a best-in-class Fintech platform that leverages data science and analytics to improve the speed, cost, and choice of capital available to small businesses in the United States. Credibly is dedicated to creating a superior customer experience that meets the needs of all small businesses, regardless of product need or credit profile.

Learn more at www.credibly.com. Follow Credibly @credibly360.

Media Contact:

Tracy Rubin / Olivia Levis

JCUTLER media group

323-969-9904

tracy@jcmg.com / olivia@jcmg.com

IOU Financial Posts $2.1 Million Loss in Q2

August 30, 2017IOU Financial’s Q2 loss was double that of Q1, according to their recently filed financial statements. The company lost $2.08 million (CAD) on $4.36 million in revenue. IOU had lost only $1 million in Q1 on nearly the same revenue. $393,814 of Q2’s expenses was a one-time cost related to contract cancellations, however.

The company lent $26.2 million (US) in Q2, down from $31.8 million for the same period last year.

Notably, the company said they are focusing on an aggressive litigation strategy against businesses who intentionally default on their loan obligations. “Provision for loan losses (net of recoveries) increased to $2.4 million for the three-month period ended June 30, 2017, up from $1.2 million for the previous year,” they stated. “The increase is primarily attributable to an increase in defaults by borrowers and partially due to an increase in the size of the loan portfolio.”

Former CFO of Credibly Moves On to Western Funding

August 19, 2017Credibly’s former chief financial officer and product officer, Jim Murray, has moved on to become President of Western Funding, according to LinkedIn. Murray was with Credibly for 5 years, originally starting as the company’s chief operating officer.

BFS Capital Appoints Michael Marrache as CEO

August 17, 2017Coral Springs, Fla.—August 17, 2017—BFS Capital Inc., a leading small business financing company, announced that it has appointed Michael Marrache as Chief Executive Officer to succeed outgoing CEO and co-founder Marc Glazer. Named President in September 2016, Marrache previously served for more than three years as the company’s Chief Operating Officer. He also will join the company’s Board of Directors. Marc Glazer will continue to serve as Chairman of the BFS Capital Board.

“Michael has been invaluable in enhancing operations and driving sales. As CEO, he will lead our strategic direction both domestically and internationally, and spearhead initiatives that will continue to improve our loan portfolio metrics and strengthen our reputation among customers and partners as a premier small business lending organization,” said Glazer.

Over recent months, Marrache has built a management team that will execute on a long-term strategic plan to guide the company’s future and reach new milestones in the areas of origination, ISO partnerships and customer experience.

“I began work with BFS Capital nearly four years ago because I thought the company had enormous potential, and I’m even more certain of this today. I’m honored to have been asked by Marc and the Board to lead the company’s next phase of growth,” said Marrache.

“Our business has experienced great momentum over the last year and we’re setting a course for continued growth and leadership. We have a strong, committed management team and together, along with our employees, we’re primed to execute on our priorities, including upgrading the customer experience, investing in our product offerings and leveraging our data science to drive insights for our customers and partners,” Marrache added.

In April, BFS Capital reached a milestone of $1.5 billion in financing—a 50% increase over the $1 billion the company generated from inception through July 2015, led by loan portfolio growth in both new and repeat customers.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS Capital’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund businesses in all 50 states and Canada, and through its affiliate, Boost Capital, in the United Kingdom. Since 2002, BFS Capital has provided more than $1.5 billion in total financing to more than 18,000 small businesses across more than 400 industries. Headquartered in South Florida with offices in New York, California and the United Kingdom, BFS Capital is an accredited BBB company with an A+ rating. To learn more, please visit: www.bfscapital.com.

Has OnDeck Turned The Corner?

August 7, 2017

OnDeck’s loan origination volume declined by approximately 20% in the second quarter to $464.4 million but more importantly the company only recorded a GAAP net loss of $1.5 million. That’s down from the $11.1 million loss recorded in Q1 and in line with the company’s plan to achieve profitability in the second half of the year. OnDeck predicts that sequential originations growth will resume in Q3.

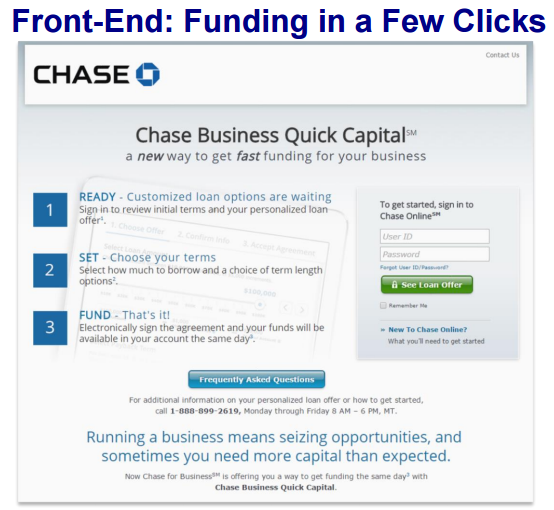

OnDeck also announced that it has expanded its collaboration with JPMorgan Chase for up to four years to provide the underlying technology supporting Chase’s online lending solution to its small business customers, according to the release. “Chase plans to continue to refine the offering, including expanding access and enhancing features throughout next year.” The image at right is from their Q2 earnings presentation demonstrating the front-end collaboration.

The company has also implemented stricter underwriting standards which includes lower loan amounts, shorter loan terms and stronger credit metrics.

Sales and marketing expenses actually increased from $14.8 million in Q1 to $15.3 million in Q2 but that was inclusive of $1.4 million in severance charges. The high cost of marketing is consistent with anecdotal reports obtained by deBanked regarding market saturation. Just recently, a small business owner told us in an interview that she has received so many mailed advertisements for working capital that she has a pile of them that’s now four inches thick.

OnDeck recorded a significantly higher charge-off percentage in Q2 at 18.5% up from 14.9%, which the company partially attributed to a contracting portfolio. However, the raw dollar amount grew substantially as well. The 15+ day delinquency ration dropped from 7.8% in Q1 to 7.2% in Q2

During the Q&A session of the earnings call, CEO Noah Breslow said he believed the company was positioned well to gain some market share due to the shakeout occurring in the industry.

Breakout Capital Expands Senior Leadership Team

August 6, 2017Breakout Capital – a leading small business lender – announces the hires of Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. These key additions position the small business lender for continued growth.

McLean, VA, August 7, 2017 – Breakout Capital announced today the appointments of Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. Both Mr. Fleischmann and Mr. McCammon bring a wealth of knowledge and small business lending experience that can accelerate Breakout Capital’s rapid growth.

“Breakout Capital’s growing employee base shares the same passion and commitment to advancing the Company’s mission to provide transparent working capital solutions, educate small businesses, and promote industry-wide best practices. We are thrilled with the additions of Robert and Tom to the leadership team,” said Founder & CEO, Carl Fairbank.

“Breakout Capital impressed me with its outstanding commitment to educating and advocating on behalf of small businesses,” said Fleischmann. “The innovative loan products combined with the impressive team of professionals make me extremely excited about the opportunity.”

Mr. Fleischmann will lead Breakout Capital’s efforts to expand and diversify its channels through strategic partnerships. Prior to joining Breakout Capital, Mr. Fleischmann was Director of Strategic Partnerships at RapidAdvance where he worked with a diverse group of partners, including banks and commercial finance companies, to help meet the financing needs of their business clients.

Mr. McCammon joins Breakout Capital with direct industry experience as he was formerly Director of Portfolio Management and Credit Operations at OnDeck. Prior to OnDeck and his recent move to the Breakout team, Mr. McCammon was involved in two de novo banks and was a consultant to the FDIC during the financial crisis. He will be a central figure in continuing to build Breakout Capital’s stature as both a credit-and customer-centric enterprise.

“Having worked in both retail banking and fintech, I was drawn to Breakout Capital as they have successfully combined strong credit and ethics fundamentals from traditional banking while still efficiently delivering capital to small businesses,” said Mr. McCammon.

Breakout Capital has quickly established a reputation as one of the most trusted and respected lenders in the market with a focus on product innovation, transparency, responsible lending and a partnership-based approach that extends beyond providing capital. Additionally, Breakout Capital is a Principal Member of the Innovative Lending Platform Association (ILPA), the leading trade organization representing a diverse group of online lending and service companies serving small businesses.

About Breakout Capital

Breakout Capital, headquartered in McLean, VA., is a technology-enabled direct lender which has provided a wide range of working capital solutions to small businesses across the country. In addition to becoming one of the fastest growing companies in the market, Breakout Capital is a leading advocate for small business. Its CEO, Carl Fairbank, is a Board Member of the Innovative Lending Platform Association. Breakout Capital has produced a highly regarded “educational series” through its blog, Breakout Bites, that helps small businesses better understand the technology-enabled lending market and how to avoid the hidden fees and debt traps that are prevalent in the industry. With a laser focus on educating small businesses, advocating for industry-wide best practices, and providing diverse, transparent working capital solutions, Breakout Capital is changing the financial landscape for millions of small businesses in need of funding. For more information, visit http://www.breakoutfinance.com.