p2p lending

What’s Lending Got to do With Cryptocurrency?

January 10, 2018 Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

A meetup hosted by partners of Central Diligence Group (CDG) on Tuesday night in NYC, for example, was geared towards cryptocurrency enthusiasts. CDG is a merchant cash advance and business lending consulting firm. Those that attended, talked candidly about Ripple, Bitcoin, Ethereum, and the hot topic of Initial Coin Offerings (ICOs). And it did seem all connected. Companies successfully raised more than $3 billion through ICOs in 2017, for example, some of them online lending companies.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

Whether these valuations are overdone is besides the point. A smart phone is all that’s required to get in on the action and trade thousands of cryptocurrencies online, many of which move up and down by astronomical percentages over the course of a day. Becoming a millionaire overnight by hitting on the right one is a dream sought after by many. And young people, especially millennials, are become unconsciously comfortable transacting in non-government-backed currencies through technology that completely shuts out banks.

And that may be the shift in all of this to pay attention to. It isn’t that a local restaurant is going to collateralize their Bitcoin to get a loan and outcompete an MCA company, but that a portion of the monetary system eventually starts to sidestep banks.

Trying to collect on that judgment? Good luck tracing the money in cryptos.

Need to freeze funds? You can’t freeze someone’s Bitcoins if they’ve got them stored on their own hardware.

Evaluating a business’s bank statements? The transactions can only be verified on a blockchain.

You might not believe me, but it’s incredibly likely that you’ve encountered a client that has defaulted on an MCA or loan whose stash of money has been obscured in cryptos all the while their bank statements appear to show insolvency.

It’s also likely that you’ve encountered a client that has used the proceeds of their MCA or loan to buy a crypto. Maybe not the whole amount, but with some of it. One study, for example, revealed that 18% of people have purchased Bitcoin using credit. Bloomberg reported that the phrase “buy bitcoin with credit card,” just recently spiked to an all-time high.

People are even taking out mortgages to buy Bitcoin, according to CNBC.

If you think cryptocurrency is an industry completely independent of your business, consider that the market cap of cryptocurrencies is currently valued at more than $700 billion. That’s nearly twice the market cap of Goldman Sachs and JPMorgan, COMBINED. The #3 cryptocurrency by market cap, Ripple, is being pitched almost entirely to traditional financial institutions.

Bet all you want on the prediction that this bubble will burst. Maybe it will. But the underlying technology, transacting without banks in non-government backed currencies that may be difficult to trace and recover, is a genie that’s not returning to its bottle anytime soon.

In the meantime, now might be a good time to poll your employees or colleagues about their knowledge or use of cryptocurrency. You may be surprised by what you find, especially among the younger crowd.

——–

Disclaimer: I currently hold a material amount of Ether, the currency of the Ethereum blockchain.

Is Lending Club Misleading New Investors About Past Performance?

December 3, 2017

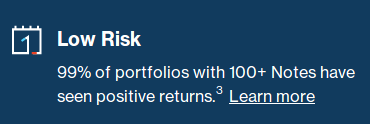

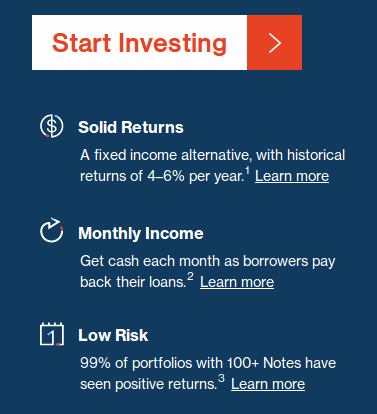

New retail investors interested in the Lending Club platform are greeted with a friendly statistic, that “99% of portfolios with 100+ Notes have seen positive returns.” That’s a slippery statement, which is probably why they footnoted it.

The footnote says that only applies to A through E notes, the only grades of securities that Lending Club is still selling. F and G grades are excluded, presumably because they are no longer for sale as of last month after they noticed “an increase in prepayment and delinquency rate.”

By excluding the notes that significantly underperformed, Lending Club has apparently been able to raise the portfolio performance statistic being marketed to new investors.

On October 28, 2017, for example, Lending Club was reporting that 97% of portfolios with 100+ notes had positive returns. That was representative of all notes. Immediately after announcing that they were discontinuing F and G notes, they raised that number to 99% and added a line about how F and G notes were excluded from past performance.

:::Poof::: And just like that, the bad loans and their drag on returns no longer exist from the history reported to new investors.

The problem with ignoring the letter grades that bamboozled some investors in the past is that Lending Club determines the letter grade of the security, not an independent ratings agency. That means that an F or Grade-grade borrower in October could just be deemed a D or E-grade in December and nobody would be the wiser. Retail investors have no way of knowing because Lending Club’s grading system is proprietary. Go figure.

The problem with ignoring the letter grades that bamboozled some investors in the past is that Lending Club determines the letter grade of the security, not an independent ratings agency. That means that an F or Grade-grade borrower in October could just be deemed a D or E-grade in December and nobody would be the wiser. Retail investors have no way of knowing because Lending Club’s grading system is proprietary. Go figure.

Even if Lending Club did not do that, they’re setting a terrible precedent. If portfolios underperform, again, what’s to prevent them from continuing to make similar inflated claims about returns with a new footnote that excludes D and E notes?

It’s important to bear in mind that Lending Club is in the business of selling securities to unsophisticated retail investors. That 99% of portfolios allegedly yield positive returns is no doubt a major selling point to those worried about the risks of online lending. Why else would Lending Club feel the need to make that a big headline in their marketing?

Online lending is very risky. That’s why in October, the number of portfolios with positive returns wasn’t 99%. Lending Club should not be permitted to sweep past investor losses under the rug.

Bad form Lending Club. Bad form.

Good Riddance F and G Notes on Lending Club

November 9, 2017 When Lending Club announced they were discontinuing F and G grade notes on their platform for investors, I wasn’t surprised. Investors in general have been reporting disappointing returns, even dipping into negative territory some months. My own portfolio there is on track to generate a loss for 2017, which seems even worse when I consider that those funds could’ve returned nearly 15% in an S&P 500 index fund or more than 600% in bitcoin. Granted, only a small portion of my investable assets were tied up in Lending Club so it’s not all bad.

When Lending Club announced they were discontinuing F and G grade notes on their platform for investors, I wasn’t surprised. Investors in general have been reporting disappointing returns, even dipping into negative territory some months. My own portfolio there is on track to generate a loss for 2017, which seems even worse when I consider that those funds could’ve returned nearly 15% in an S&P 500 index fund or more than 600% in bitcoin. Granted, only a small portion of my investable assets were tied up in Lending Club so it’s not all bad.

Out of the 3,262 notes I purchased on Lending Club, only 99 were F-grade and 53 were G-grade. They didn’t do so well in retrospect, echoing Lending Club’s findings.

27 of my G notes have already been charged off. 17 have been paid off, with the rest still outstanding. A charge-off rate over 50% is not so good on its own, but the data is worse because the interest earned on the performing ones was not enough to offset the charge-offs. Even if all of the remaining notes perform, it is no longer possible to earn a positive return on G notes. The amount I loaned exceeds the total dollars returned. The end result of a category that investors heralded as high-risk, high-return is a big fat loss.

31 of my 99 F notes have already been charged off. Only 26 remain outstanding, 4 of which are delinquent. The rest have been paid off. At this time, the amount I loaned exceeds the total dollars returned. It is still mathematically possible to break even if the remaining loans do not default, but we’ll see. Suffice to say, these were a bad investment.

I have been winding down my portfolio since May 2016. RIP F and G notes.

Lending Club Has Become the Domain of Banks as Peer-to-Peer Continues Decline

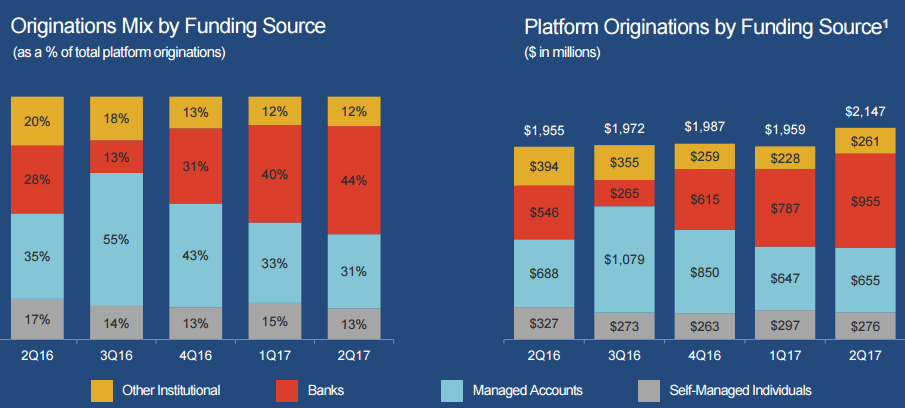

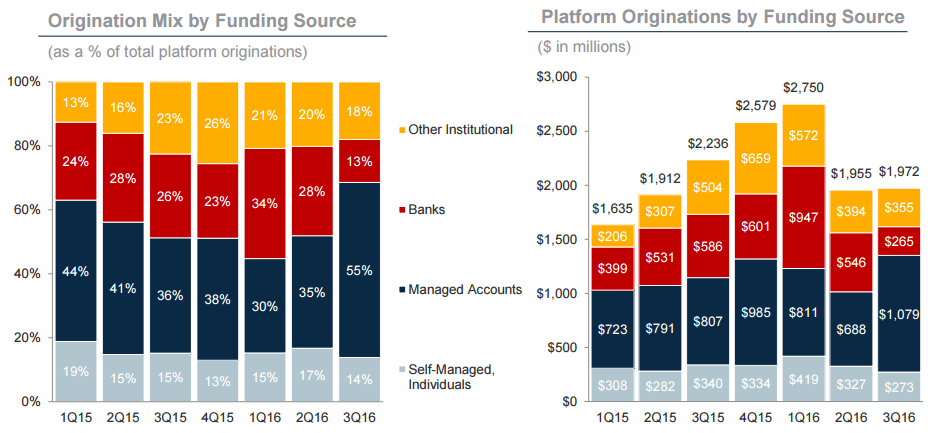

August 8, 2017Lending Club’s latest quarterly report revealed the future of their platform, as a conduit for banks to make personal loans. As illustrated below, banks have gone from funding only 13% of originations three quarters ago to 44% of all originations in the most recent quarter. That’s an increase from $265 million to $955 million.

Meanwhile, self-managed individuals, or the peers in the peer-to-peer aspect of the platform, only funded 13% of originations in Q2, a decrease from the previous quarter.

Lending Club refers to the breakdown as a “diverse” investor mix but it is obvious where the trend is leading.

To be fair, Lending Club had previously depended on banks pretty heavily, as demonstrated by the chart that appeared in their Q3 2016 earnings presentation. Bank funding was at its highest point in Q1 2016 at $947 million, as was self-managed individuals at $419 million. Bank funding has since recovered and surpassed that record, but funding from self-managed individuals is still down by 34% (and shrinking).

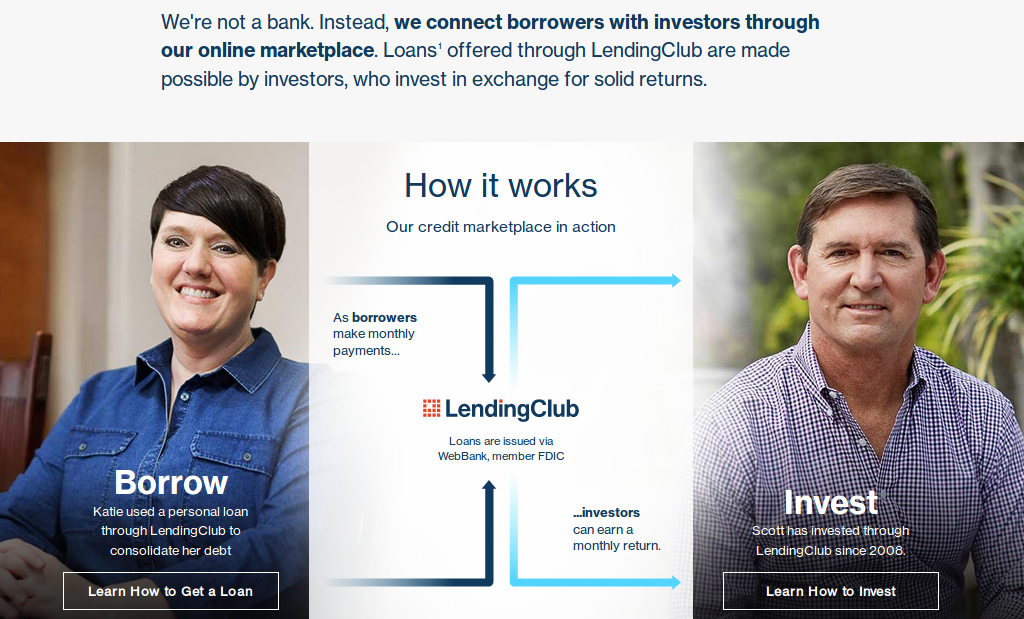

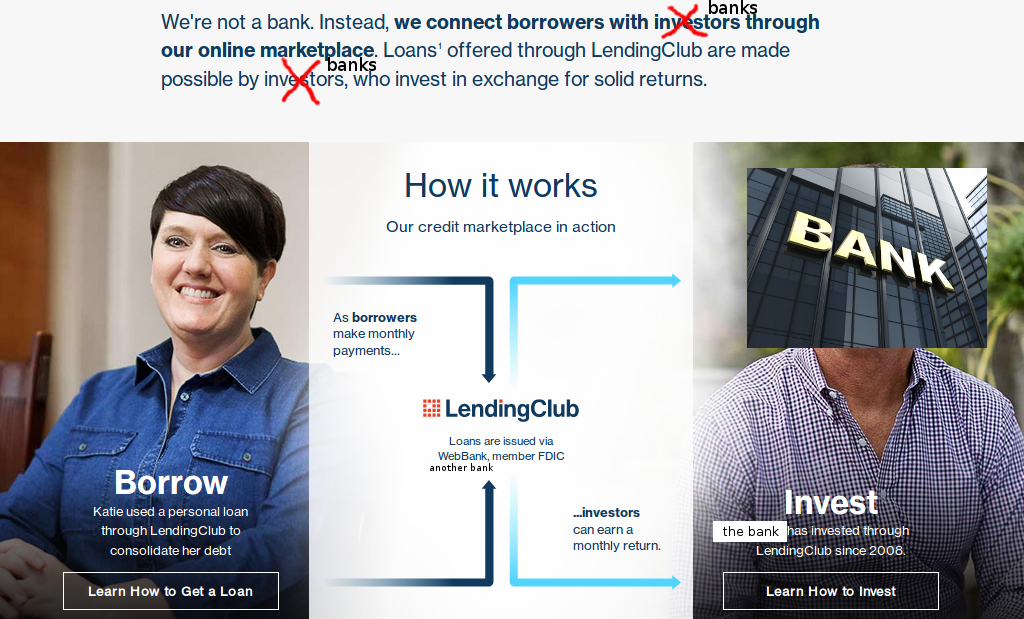

Despite these trends, Lending Club still explains their lending service as peer-to-peer on the homepage. In the example that explains how Lending Club works, “Scott” is investing on the platform to make a loan to “Katie.”

But it’s often more like this:

Lending Club had a $25.4 million loss in Q2. They’re projecting a loss of $61 million to $69 million for the year on revenue of $585 million to $600 million. Expect them to become more dependent on banks in the future.

How P2P Lending’s Evangelist is Faring Now

May 24, 2017Peter Renton, a co-founder of the LendIt Conference and p2p lending investor since 2008, published his latest portfolio performance data on Monday. While he wrote that the downtrend is continuing unabated, he still reports an overall marketplace lending return at 7.73%.

Notably, he reported that one of his Lending Club accounts actually lost money in the first quarter of the year, a first for him, though he is not the only person to experience losses.

Funding Circle is Closing its Forum

May 1, 2017 One notable remaining aspect of Funding Circle’s peer-to-peer roots has been its own online forum. If you haven’t been part of that community, you’re too late, since it’s shutting down on Tuesday.

One notable remaining aspect of Funding Circle’s peer-to-peer roots has been its own online forum. If you haven’t been part of that community, you’re too late, since it’s shutting down on Tuesday.

According to a forum admin, “there has been a developing trend towards a small number of investors asking questions about a narrow range of technical topics – most of which are better dealt with through our Investor Support team. Therefore we have taken the decision to close the forum at 6pm [UK time] on Tuesday 2nd May. We hope you will all continue sharing your views on Funding Circle over on the P2P Independent Forum, which we will continue to monitor.”

One forum user jokingly theorized that the move was really about silencing investors who use the forum to complain about delinquent borrowers, going so far as to create a humorously custom-captioned movie clip.

According to P2P Finance News, a Funding Circle spokesperson said, “The closure has nothing to do with the performance of Funding Circle property development loans over the last three years which continue to outperform expectations. Investors have earned an average of seven per cent since launch and more than £22m in interest on property loans alone.”

Update 5/2: The Funding Circle Forum has officially been taken down. The URL now just redirects to a general FAQ page

For Lending Club Borrowers, Interest Now Accrues During Grace Periods

February 26, 2017On February 24th, Lending Club eliminated a courtesy that had long been afforded to borrowers, interest waivers during grace periods. Specifically, borrowers who missed a monthly payment were given 15 extra days to make the payment with no extra interest assessed or late fees. Going forward, interest will indeed accrue during grace periods.

“we are eliminating the grace period interest waiver in order to better align borrower payment incentives as we seek to deliver solid returns to our investors,” Lending Club said in an email.

Since this will not affect a borrower’s monthly payment, all additional accrued interest will be extended to another month beyond the maturity date.

‘Peers’ Continue Retreat from Lending Club

February 18, 2017 The peer aspect of peer-to-peer lending continued to erode last year, according to Lending Club’s year-end earnings presentation. Self-managed individuals, those still making their own investment decisions, only made up $263 million of their 4th quarter’s origination volume, reaching the lowest level in two years. That’s nearly 38% lower from the peak of $419 million in Q1 of 2016.

The peer aspect of peer-to-peer lending continued to erode last year, according to Lending Club’s year-end earnings presentation. Self-managed individuals, those still making their own investment decisions, only made up $263 million of their 4th quarter’s origination volume, reaching the lowest level in two years. That’s nearly 38% lower from the peak of $419 million in Q1 of 2016.

Overall monthly originations haven’t really moved, hovering at around $2 billion per quarter over the last 3 quarters, down from the peak of 2016’s Q1 when they hit $2.75 billion. There’s money coming from somewhere though, of course. A chart in the presentation revealed that 74% of Lending Club’s Q4 originations came from banks and managed accounts. The managed accounts category is comprised primarily of asset managers who invest mainly in marketplace lending.

A glance at Lending Club’s self-managed individual originations as a percentage of total originations per quarter is below:

| Q4 2013 | Q1 2014 | Q2 2014 | Q3 2014 | Q4 2014 | Q1 2015 | Q2 2015 | Q3 2015 | Q4 2015 | Q1 2016 | Q2 2016 | Q3 2016 | Q4 2016 |

| 27% | 27% | 23% | 25% | 19% | 19% | 15% | 15% | 13% | 15% | 17% | 14% | 13% |

Retail investors were largely skimmed over during the Q4 earnings call, with CEO Scott Sanborn and CFO Tom Casey choosing to focus their attention on bank participation. “As you know, banks returning to the platform has been a priority for us and acts as an endorsement of our strength and compliance and controls,” Casey said.

Using the Seeking Alpha transcript as a guide, the word bank was said on the call 32 times while retail investor was only mentioned once.

To that end, Lending Club’s announcement highlighted its bank funding achievement.

Meanwhile, the word retail doesn’t exist anywhere in the announcement unless you count the necessary Safe Harbor Statement.

RIP the retail investor.