MPR Authored

CNN Distorts Facts with Merchant Processing Statements

August 23, 2011

CNN ran an article today (Business Owners Baffled By Financial Statements) that supposedly exposes the crafty credit card industry. While there can always be improvements in transparency, Catherine Clifford not only misses the mark, she speaks authoritatively on a topic that she does not understand. This is upsetting considering she consulted with experts in her research. (Tim Chen, CEO of Nerd Wallet and Phil Hinke, President of MerchantFeeSavers)

Here’s a few errors we’d like to point out:

“Mom and pop stores do not deal directly with credit card giants, such as Visa (V, Fortune 500) and Mastercard (MA, Fortune 500). Instead, they have to work with third-party processors — known as merchant account providers or acquirers.” – Those poor victim Mom and Pop stores! But it’s not just Mom and pop stores that don’t get to work directly with Visa or MasterCard, NO retailer deals with them. Visa and MasterCard operate payment networks, not card processors. It is the role of credit card processors and acquiring banks to deal with retailers, regardless of their size. Catherine, here’s a simple diagram that can better explain it.

“And to make matters worse, every credit card has a different fee structure. Every credit card brand — such as Standard MasterCard, Gold MasterCard, Premium MasterCard, World Elite MasterCard — has its own fee structure. That means there are at least 400 different combinations of charges.” – Only businesses using an Interchange Plus pricing model are billed according to the 400+ cost categories. For those using tiered systems, which is the VAST MAJORITY of mom and pop stores, there are only 3 or 4 rate categories. These categories are extremely easy to understand and compare against competitors using similar pricing. See more on this in our simple guide: Intechange Vs. 3 Tier.

“For example, the bottom of the statement shown above, says: “Effective June 2011, MasterCard is introducing a new fee.” What it doesn’t say is what the fee is for or how much it is.” – MasterCard is a payment network and the fee they charge is roughly 11 basis points. On $100 in sales, that translates to 11 cents, a near immaterial amount. The payment network fee is normally only applied to businesses using the Interchange Plus pricing model. While we believe the omission of the increase is either a mistake or a deliberate alteration to make news, considering how small the fee already is, any increase is likely to go unnoticed.

“We are business owners. We are working. We are taking care of the customers,” said Mike Craighill, who owns two restaurants called Soup and Such in Billings, Mont., with his wife, Antonia. “I don’t have time to spend looking over every single line of the credit card statement.” – We don’t want to slam Soup and Such but their response is particularly ignorant. Just because you can make soup, doesn’t mean you can run a restaurant. Running a business means taking time to go through the financial statements and paperwork. Whether you do it yourself or hire a bookkeeper is your choice, but to complain that you can’t be bothered by looking at a statement once a month is bad business sense. You can’t make the case for transparency while admitting you are too busy serving soup to care anyway.

“That’s why for some business owners, cash only may be the best way to go.” – The worst conclusion ever. To point out that some business owners have trouble understanding their monthly statements and therefore should only use cash speaks volumes about Ms. Clifford, who clearly didn’t care about making a cohesive argument. It’s a shame that millions of people will read the article loaded with errors with the clear endorsement of CNN.

I guess it’s all about spitting out content in the name of web traffic and advertising. It’s articles like this that spring anti-bank lobbying groups into action to fight against something they don’t understand. That’s how we ended up with debit card reform. The whole 21 cent debit cap fee that just went into effect? Hailed as a victory for retailers, it does nothing to change the price of a debit card transaction at the point of sale. Instead it limits how much of the revenue the acquiring bank can split with the issuing bank. Wait, huh?. Yeah… good work.

Next time Catherine, have the expert write the whole article for you or just don’t bother writing it at all.

– deBanked

Merchant Cash Advance 2nd Quarter 2011 Stats

August 23, 2011

Like following the Merchant Cash Advance industry statistics? Whether you agree or disagree with our findings, we’re planning on releasing the 2nd Quarter MCA statistics in the next month or so. Our research method is constantly being improved in order to quantify the industry as accurately as possible.

The industry hit a big lull in the first quarter, mainly due to the stalling of funding in California. Preliminary reports and experience reveal that funding in California is back on the rise. Bank lending is still non-existent and new players are joining the space every month so it will be interesting to see how things are shaping up.

While you’re waiting, look back at the all the previous data: Merchant Cash Advance Industry Statistics

– The Merchant Cash Advance Resource

And the Misinformation Continues

August 23, 2011Originally published on July 12, 2011.

According to an article in BusinessWeek, Jennifer Cavallaro of Bristol, Rhode Island spent the last year lobbying for debit card interchange fee reform. As a restaurant owner, the cost of accepting a debit card was too high so she rallied to lower the cost the banks were allowed to charge her, or so she thought.

Or so BusinessWeek thinks…

Or so almost everyone thinks…

The Federal Reserve did in fact sign a debit interchange fee cap of 21 cents and 5 basis points into law. But this law has NO EFFECT or IMPENDING IMPACT on the cost a business is charged for accepting a debit card.

HUH?!

There are the three key parties involved in a debit card transaction:

1. The Customer’s Bank (The bank such as Bank of America, Wells Fargo, or whatever bank issued the debit card to the customer)

2. The Acquiring Bank (The bank the business is signed up with to accept debit cards through. It may be a large bank or independent merchant processor)

3. The Payment Network (Visa, MasterCard, PULSE, STAR, NYCE etc.)

An “interchange fee” is the money the Acquiring Bank pays to the Customer’s bank to help cover their costs. Essentially if a business is being charged 44 cents for accepting a $5 debit card sale. That 44 cents is collected by the Acquiring Bank and then shared with the Payment Network and Customer’s Bank.

Today that same merchant could be charged 44 cents or more for that $5 sale. The only difference is that the Acquiring Bank is only allowed to share a maximum of 21 cents and 5 basis points with the Customer’s Bank. Banks that issue debit cards will see a large decline in revenue, but everything may stay the same for all the other parties involved, including the businesses themselves.

Not only did retailers fail to win this fight, but they weren’t even a part of this legislation in any way. The law just caps what one bank is allowed to pay another bank. Nothing about businesses or cost at the point of sale. The world will go forward, but not with lower debit card fees for anyone.

Someone should tell BusinessWeeek that almost all of their facts and reporting are wrong.

- “Both merchants and banks balk at a Federal Reserve compromise on fees that businesses pay financial institutions” WRONG

- the Fed issued its final ruling: a cap of 21¢ per transaction. WRONG

- “Although she says the new rule will roughly halve her debit-card expenses, she feels they’ll still be too high.” JUST PLAIN SAD SINCE HER FEES HAVE NOT HALVED OR CHANGED AT ALL.

– deBanked

15,000 exempt from the debit card interchange fee standards

August 23, 2011Originally Published on July 14, 2011.

Why is the number ‘15,000’ significant? That’s approximately the number of banks that are EXEMPT from the debit fee interchange cap. Download List

From the Federal Reserve:

The Federal Reserve Board on Tuesday published lists of institutions that are subject to, and exempt from, the debit card interchange fee standards in Regulation II, which implements provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act. These lists, available at http://www.federalreserve.gov/paymentsystems/debitfees.htm, are intended to help payment card networks and others determine which issuers qualify for the statutory exemption from interchange fee standards. The statute exempts any debit card issuer that, together with its affiliates, has assets of less than $10 billion.

To facilitate compliance with the debit card interchange fee standards in the Board’s Regulation II, 12 CFR part 235 (which implements section 920 of the Electronic Fund Transfer Act), the Board is publishing two lists of institutions using data available to the Board. These lists are intended to help payment card networks and others determine which issuers qualify for the statutory exemption from interchange fee standards.1 The statute exempts any debit card issuer that, together with its affiliates, has assets of less than $10 billion. The lists have been generated from the set of institutions in existence on December 31, 2010, according to the available data.2 Institutions have been grouped into two categories: Exempt and Not Exempt. Institutions in the Exempt category have been determined to have, together with their affiliates, reported assets of less than $10 billion, and therefore are exempt from the interchange fee standards under the statute. Institutions in the Not Exempt category have been determined to have, either individually or together with their affiliates, reported assets of $10 billion or more, and therefore are not exempt from the interchange fee standards under the statute.

In addition, a small number of debit card issuers may not appear on either of these lists, such as institutions for which the Board has incomplete affiliate data, de novo institutions for which the Board did not have financial data as of December 31, 2010, and issuers without federal deposit insurance. If an issuer does not appear on either of these lists and is exempt from the interchange fee standards, it should so certify to its participating payment card networks.

The interchange fee standards become effective on October 1, 2011. The Board plans to update the lists annually.

For media inquiries, call 202-452-2955.

Read the report and find the list here:

http://www.federalreserve.gov/newsevents/press/bcreg/20110712a.htm

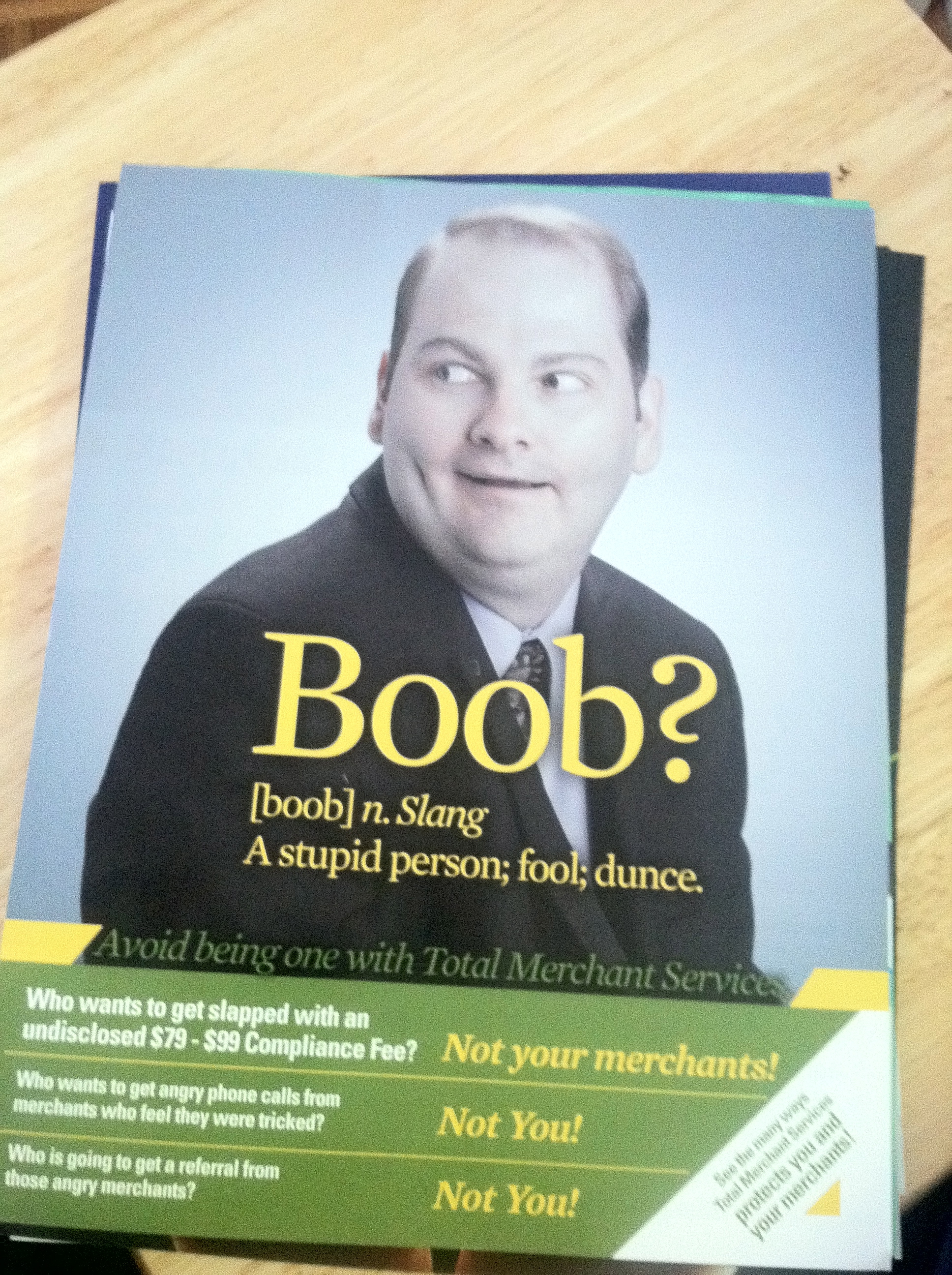

Sales Agents Are You A Doofus?

August 23, 2011

Update 1/16/2012: are you a boob?

The attached advertisement came tucked inside our latest issue of the Green Sheet. By now, this must mean that these ads are working for them. LOL.

————————–

Are you a doofus? A few folks in Basalt, CO are challenging resellers of merchant processing services to find out. Total Merchant Services recently launched an ad campaign touting their ability to maximize both customer and reseller satisfaction. But their target market is having mixed reactions, leading some to claim they have completely missed the mark.

And unlike many controversial ads, this one leaves no wiggle room for interpretation:

Avoid being inept in your career and work with Total Merchant Services!

Of course this may appeal to the younger resellers who are drawn in by flashy, satirical marketing. But for seasoned agents who’ve been in the business 5, 10, 20, and 30 years, they’re unlikely to be anything less than highly proficient. There’s a learning curve in the industry and the ones that turn it into a steady career have already figured out how to balance a good processing deal for both themselves and their customers.

If you click through to the actual full advertisement, it boasts that agents need not worry any longer about tricking their customers. “Who wants to get angry calls from merchants that feel they were tricked? Not you!” It says a lot about who they’re targeting.

Of course on the other hand, it may all just be a ploy to get their company some press. “Did you hear what Total Merchant Services did?!” Maybe you wouldn’t have if they ran the same plain vanilla ads that everyone else does.

Avoid being a dumb bastard and learn a few things at the Merchant Processing Resource!

What do you think?

– deBanked