Should I Start an ISO With Only $2,000?

January 12, 2015A long time ago in a galaxy far, far away…

It is a period of civil war. Rebel sales reps, striking from a hidden ISO, have won their first victory against the evil Galactic Funder.

During the battle, Rebel spies managed to steal secret formulas to the Funder’s ultimate weapon, the UNDERWRITING ALGORITHM, an advanced code with enough power to destroy an entire industry.

Pursued by the Funder’s sinister sales agents, our hero races home with her flash drive, custodian of the stolen formulas that can save her merchants and restore freedom to the industry…

Breaking away to start your own ISO or brokerage in this industry used to be a rite of passage. You started somewhere, learned the ropes, then went off on your own like a Jedi Master.

The stories of reps and underwriters of years past who left their jobs to start their own ISOs are a bit nostalgic. Young twenty-somethings defying authority to plant their own flags in an industry they felt offered unlimited potential. For some, going solo was a rude awakening, a healthy taste of the real world, where you needed to be able to do more than just close the leads you’re given. But for others? Well, today they are the owners or managers of companies worth millions, tens of millions, or hundreds of millions of dollars.

Empires were built not that long ago and they certainly were not in a galaxy far, far away. But today the prospects are much bleaker. The industry has matured and certain channels are saturated. Merchant cash advance and non-bank business lending are no longer part of a young unexplored universe.

So to those that have asked me whether or not it makes sense to start an ISO in 2015, I’d have to say in many cases it does not. It’s a little late in the game. Below is one of the most popular questions posed to me over the last six months:

Q: I’m thinking about starting my own ISO. I have about $2,000 to $5,000 to spend on leads. Do you think I can do it and where should I buy the best leads from?

Q: I’m thinking about starting my own ISO. I have about $2,000 to $5,000 to spend on leads. Do you think I can do it and where should I buy the best leads from?

A: There’s a few things to address here. If you are working out of your house and your rent/mortgage is already taken care of without you having to pay yourself from your new ISO, you may be able to turn a profit starting with something this small. The first problem though is that if you’re not absolutely positive where to get excellent leads, you’re going to spend a lot of money on experimenting with multiple sources. $2,000 might be the cost of an experiment with one lead provider. In other cases, it might be $5,000. Your entire budget could get wiped out in an experiment with just one source.

There may be no barriers to entry in this business, but $2,000 to $5,000 is entirely too little to give yourself a real chance to get off the ground. Direct mail takes a lot of trial and error and thousands of dollars. Google/Bing advertising takes even more trial and error and tens of thousands of dollars before you can get really meaningful results.

And if you’re going to put all your eggs in the UCC marketing basket because of budget, it’s going to be a tough climb uphill.

The companies that do actually have the best leads don’t need a $2,000 startup ISO to sell them to. A big ISO or funder is probably already paying double the price they’re worth.

So how do you stand a chance? You should realize that the odds are you won’t.

And if you need to allocate part of that 2-5k to pay for an office and get set up like a business, you might not have anything left for marketing at all. That’s a horrible place to be!

Lastly, I have seen many ISOs try to become a broker’s broker in order to acquire deals. That means trying to close ISOs to send you deals for you to forward on to a funder as a middleman where you will get a cut if the deal closes. It’s a hustle, and if you can swing this, great, but it’s not exactly a sustainable model especially if the ISO realizes they can go direct to the funder themselves. If you can’t acquire merchants on your own (and deals you stole from the last place you worked at don’t count as acquiring on your own), then you probably shouldn’t be in the ISO business at all.

If you’re going to start an ISO in 2015, I suggest having a minimum $25,000 (50k to be safe) in marketing to start off. And if you don’t know what you’re doing, well then may the force be with you.

Heather Francis Launching New Funding Company

January 5, 2015 One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

When the news broke, deBanked asked Francis about the change. This was her response:

“So the start of the new year begins with something exciting for me as I will be leaving Merchant Cash Group to pursue heading up my own funding company. Elevate funding is still in the set up stages and will not be operational and funding until Mid February but I can assure you that with each unveiling of what we will be funding and what we will offer to the Alternative Industry as well as the business owners will help shape a new future. I enjoyed my time at Merchant Cash Group and I wish them all the best but I am excited for this new adventure and to take a lot of the ideas that have been kicking in my head for a while and see them come to fruition. I know it will be difficult and I am greatly looking forward to the challenge. In the words of a Fort Minor song : This is 10% luck, 20% skill, 15% concentrated power of will, 5% pleasure , 50% pain, and a 100% reason to remember the name… Best of luck to all in 2015!”

Elevate will be based in Gainesville, FL.

Despite FinTech Disruptions, Many Thing Stay The Same

January 5, 2015 2014 was an unbelievable year!

2014 was an unbelievable year!

I kicked off last year by opening an account with Lending Club so that I could understand their product. Today I have tens of thousands of dollars invested on their platform and picking up new loans has become part of my daily routine. You could say I’m not surprised they went public a few weeks ago.

I also launched the industry’s first trade publication and ran it as both publisher and chief editor. We produced 6 issues and distributed more than 20,000 print copies combined. Unfortunately the publication will not be continuing further. It is wild to think that it both started and concluded in 2014 as the magazine had a cult-like following.

7 conferences in 4 cities. Las Vegas (twice), San Francisco, New Orleans, and here in New York. I spoke at two of them. Hoping for at least 1 Miami conference this year. Please??? It’s so cold here right now.

OnDeck Capital took a lot of flak in 2014 from both industry insiders and the media. They shrugged it all off and went public on December 17th. Considering they’ve operated on the fringe of the merchant cash advance industry for so long, it was one of those things you had to see to believe. I didn’t get inside the building but I saw the IPO was real from the outside.

I started off 2014 not knowing what a Bitcoin was. Now I have a copy of the entire blockchain, operate a full node (don’t worry I have port 8333 open), have 10 dedicated mining devices running 24/7, have made purchases with bitcoin, conducted countless transfers, and just finished coding a working prototype application using Coinbase’s API. And when I realized that bitcointalk.org and my cryptography books weren’t enough to satisfy my appetite, I found myself talking about bitcoin on IRC; #bitcoin and #bitcoin-pricetalk on irc.freenode.net. I also know who Satoshi Nakamoto really is now too but he made me promise not to tell anyone.

I rebranded Merchant Processing Resource to deBanked, retiring a name I’ve used for 4 years.

I interviewed former Congressman Barney Frank, one of the two architects of the Dodd-Frank Wall Street Reform and Consumer Protection Act (it was only a few questions).

I got asked by a credible movie producer if I would help him on a storyline for a script about Wall Street and the alternative business lending industry. Don’t worry I turned it down!

I jumped on the payment disruption bandwagon and used Square to process credit card transactions all year. You should know that I previously did merchant account sales. I could’ve boarded my own account and set my own fees but I went with Square anyway.

I finally got set up to syndicate on merchant cash advances.

I ran my first 5k in Central Park.

I moved to a different part of Manhattan.

Of course a whole lot more happened. It was a roller coaster year which leads me to believe that 2015 will be impossible to predict. There’s a lot more room to grow in FinTech but it might be time for fresh ideas. Everyone and their mom built an online lending marketplace platform in 2014.

Similarly, it’s also a tough time to become a loan broker or MCA ISO especially if you’re undercapitalized. The easy profit ship has sailed. Press 1s and UCCs aren’t winning business models, at least not ones that will invite outside capital or ensure survival long term.

2014 changed finance but in many ways it stayed the same.

It still takes 2-4 days to confirm an ACH didn’t reject! This is annoying all around. If I add funds to Lending Club on a Monday, it’s not accessible until Friday evening. If you debit a merchant on Monday, you won’t really know if you have it until a few days later. Believe it or not I actually mailed out more checks in 2014 than in any other year of my life. The ACH system appears to be fine until you use something that is far more advanced, something I will probably write about over the next month. Instantaneous payments, low transaction fees, no bank involvement. Yeah, it’s time for ACH to go away…

And with banks, well… I have opened business bank accounts over the last few years with 3 different banks. The one I opened in 2014 required a two hour in-person interview, a process that involved filling out forms by hand and being threatened that the government would shut everything down in a heartbeat if they found out that I so much as breathed wrong on an ATM. It was a repeat of prior account opening experiences. Although I’ve never had an account closed for doing anything wrong (because I’m not actually doing anything wrong), it is easy to see how much regulatory pressure banks are under. Swiping your debit card upside down could cause the entire bank to get an Operation Choke Point subpoena. They want your business but they’re scared to death of anything you might do with a bank account.

All the major peer-to-peer platforms of 2014 became centralized. Lending Club and Prosper don’t even fall in the p2p category anymore. The market trend has been to create a platform designed for the little guys and then hand it over to a bank or institutional money to do all the funding. In some ways it’s easier to deal with a handful of big players instead of thousands or millions of retail investors. But with the regulatory environment uncertain on so many new investment products, it’s probably also safer to deal with institutional investors, lest the regulators claim they violated a consumer protection law they thought up this morning.

Banks continue to be the biggest obstacle to innovation because at the end of the day, all payments flow through them. How can one deBank and truly disrupt?

Hopefully we’ll find out in 2015. Happy belated New Year.

Through OnDeck Capital, An Industry Wins

December 16, 2014 Call it merchant cash advance, non-bank business lending, or financial disintermediation. Whatever floats your boat. On December 17th an entire financial methodology will be validated, the daily repayment method. Daily payments don’t exist anywhere else in lending but ’round these parts it’s the standard. It’s what makes unbankable businesses bankable.

Call it merchant cash advance, non-bank business lending, or financial disintermediation. Whatever floats your boat. On December 17th an entire financial methodology will be validated, the daily repayment method. Daily payments don’t exist anywhere else in lending but ’round these parts it’s the standard. It’s what makes unbankable businesses bankable.

OnDeck is a lender. They target small businesses. The costs are high. Anyone could feasibly do those things and plenty are doing them, but only a certain segment of fintech companies utilize daily payments and most of those are merchant cash advance companies. OnDeck is a lender but like it or not their core repayment mechanism overlaps with an industry well known for being even more expensive.

Daily payments are so unique and so revolutionary that it hasn’t sunk in to the masses yet. Even the press glosses over this fine detail to instead dwell on things like APRs and social media’s role in approvals. Daily payment and daily repayment look like tech jargon, some kind of code for a backend computer process to hotwire an anomalous rate algorithm.

Daily payments mean borrowers have to make payments every single business day. It’s daily, get it? If the sun rises and it’s not Saturday or Sunday, it’s time to make a payment. I’m not saying there’s something wrong with this. I’m a proponent of this mechanism. It works for business owners that struggle to make a single lump sum payment each month and it works for lenders who need to mitigate and monitor their risk as much as possible.

I feel it’s better to know there was a problem that started yesterday than to learn there was a problem that started 29 days ago. That’s how OnDeck thinks too. And business owners can incorporate the daily deduction into their normal business operations instead of fretting to cover the balance for a big debit the day before a monthly payment is due.

I feel it’s better to know there was a problem that started yesterday than to learn there was a problem that started 29 days ago. That’s how OnDeck thinks too. And business owners can incorporate the daily deduction into their normal business operations instead of fretting to cover the balance for a big debit the day before a monthly payment is due.

This isn’t just a theoretical design that can’t function in practice. It’s been working for lenders and factors since AdvanceMe (Now CAN Capital) started doing it in 1998. The daily payment methodology has survived the Dot Com Bust and the Great Recession. It’s grown to a $3 – $5 billion a year industry. By some measures, it’s taken a hell of a long time to go this mainstream.

But it’s here. The press will call OnDeck a lender, a tech company, or a combination of both. They’re a sign of the times but they are unique in that they will show the world that daily payments have a place in the modern economy. With OnDeck leading the way, traditional lenders may consider leveraging their methodology to serve categories of risk they usually shy away from.

I’ve never heard of a business credit card that required payments to be made every day. Some might think that defeats the purpose of credit. OnDeck proves it doesn’t. And 100+ merchant cash advance companies serve as a secondary validation. Perhaps there are lenders that have considered a daily payment system previously and feared the political or legal environment was too risky. But OnDeck is making no apology about what they’re doing or how they’re doing it. They’re putting themselves on the open market, surrendering themselves to total scrutiny.

CAN Capital is gearing up to follow them, the pioneers who first experimented with daily payments 16 years ago. And while OnDeck bemoans their loan program being compared to merchant cash advance, CAN is made up of two departments, one of which is undoubtedly a merchant cash advance service provider.

CAN Capital is gearing up to follow them, the pioneers who first experimented with daily payments 16 years ago. And while OnDeck bemoans their loan program being compared to merchant cash advance, CAN is made up of two departments, one of which is undoubtedly a merchant cash advance service provider.

And there you have it. It’s not all about algorithms or tech or using facebook activity to judge a borrower. Those are old ideas now. OnDeck smashes down the door with something completely different, something that nobody is even talking about, daily payments.

December 17th is Wednesday and just about all of OnDeck’s borrowers will be making a payment. A good many of them won’t even notice. That’s the great part about layering it in as a daily cash flow expense. There’s no worrying about it at the end of the month. If they underwrite the borrower financials well enough, it should be completely painless. That’s not always the case, but it’s the goal.

You can’t possibly understand OnDeck until you understand daily payments. With this IPO, an entire industry wins.

Merchant Cash Advance Underwriting For Humans

December 11, 2014 There is no doubt that the merchant cash advance industry has undergone significant expansionary changes within the past decade. The first-mover advantage is past its prime in this industry and no longer proves to be as profitable as it once was for some of the earlier entrants to the market.

There is no doubt that the merchant cash advance industry has undergone significant expansionary changes within the past decade. The first-mover advantage is past its prime in this industry and no longer proves to be as profitable as it once was for some of the earlier entrants to the market.

Although the alternative lending industry still has not garnered enough attention for change and reform from policymakers, it has attracted attention from Wall Street and wealthy Main Street investors alike. As today’s merchant cash advance providers continue to grow their capital bases, these larger players have the option and arguably an incentive to explore new products that will help them capture a larger market share of small businesses financing needs and ultimately will help them improve their bottom line.

Several of the more established companies have continued to grow either organically through strategic leadership and good timing, while others have been able to grow and cover new markets through mergers and acquisitions. Of all changes that have been affecting this space, one of the more interesting ones is the introduction of proprietary software used by some of these companies that will allow them to pre-qualify a merchant based on an online application, rate their credit risk, briefly scan submitted bank statements, merchant account statements and financial statements.

Several companies in this industry have invested extensively into making this process a reality, believing it will help them excel against their competitors by creating an economies of scope situation.

Not so fast though…

While automation can help make a company more efficient by converting applications into funded accounts, it can also create a gap in a company’s risk management policies if the company does not have steps in the process to reduce two important risks in any financial services business:

a) Information Asymmetry

b) fraud detection.

For those companies that still use human underwriters, I have compiled some pointers on my experiences relating to things I pay tremendous attention to when underwriting new accounts that help me spot fraudulent documents.

The starting point in the fraud detection process begins with the application and a thorough review of the information provided. Google everything. Make sure the business is not reported as being closed, that the merchant is not going through extensive litigation that could result in jail time or in the business being sold off to another individual. Information on the internet is bountiful, and most of it is completely free. Unlike traditional financial services companies, he who pays the piper calls the tune does not apply in the alternative finance industry. Merchants are almost completely unbound with how to spend their advance, and sometimes engage in reckless borrowing to achieve their means, oftentimes altering documents in the process.

The starting point in the fraud detection process begins with the application and a thorough review of the information provided. Google everything. Make sure the business is not reported as being closed, that the merchant is not going through extensive litigation that could result in jail time or in the business being sold off to another individual. Information on the internet is bountiful, and most of it is completely free. Unlike traditional financial services companies, he who pays the piper calls the tune does not apply in the alternative finance industry. Merchants are almost completely unbound with how to spend their advance, and sometimes engage in reckless borrowing to achieve their means, oftentimes altering documents in the process.

Credit Reports

In my experience with underwriting, many of the fraudulent accounts that I view have owners with either bad credit, limited credit history or no credit history. Furthermore, pay close attention to any fraud alerts on the 1st page of the report, and especially the date of the alert if it is fairly recent. Lastly, pay close attention to the number of recent inquiries on the credit inquiries. Today’s small businesses receive dozens of inquiries from cash advance companies and ISOs. While the inquiries themselves do not outright indicate any fraud and may even be encouraged by ISOs looking to get their merchant the best deal, the combination of a fraud alert and say 20 inquiries from competitive cash advance companies could signify that the other competitors found something that may not add up on the file and will warrant a close eye on the other submitted documents.

Bank Statements

Through community websites, fraudulent bank statements, merchant account statements, or any other type of statement are made easily accessible to purchase. The number of submitted fraudulent bank statements that I have seen within the past year has dramatically increased. Some statements can take as little as 5 seconds to determine if they are fraudulent and there are others that are so clever that they can take close to an hour of close scrutiny to find.

I personally use Adobe Acrobat to read and navigate through bank statements. Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents to put as a simple example. Be sure to quickly glance over all the statements, checking to see that you have a complete page sequence and the page count is correct.

One of the more common amateur mistakes is to use a prior year’s bank statement and simply change the year to read current year. Fortunately for underwriters, that process is not as simple as it seems on the surface. Not only do they have to make changes on the header of every page, but many times banks and credit unions make announcements throughout the statement for the current year. Other statements include full dates (month, day, year) on some line items usually in the withdrawals section but sometimes in deposits, subtotals and totals. This is more work for merchants to alter, and leaves them more prone to forgetting to change one of the dates.

Just one inconsistency that happens to somehow conveniently flow with the rest of the statement can be the only evidence that you need. Some of the other common amateur mistakes include poor spelling throughout the statement, whiting out of numerical figures, inconsistent margin changes, font changes, and repetitive use of the same check numbers paid month after month (excluding those with default 0’s or 1’s issued by bank tellers directly).

Just one inconsistency that happens to somehow conveniently flow with the rest of the statement can be the only evidence that you need. Some of the other common amateur mistakes include poor spelling throughout the statement, whiting out of numerical figures, inconsistent margin changes, font changes, and repetitive use of the same check numbers paid month after month (excluding those with default 0’s or 1’s issued by bank tellers directly).

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

Also, be sure to check that the summary data at the beginning of each statement matches the counts for deposits, withdrawals, and checks written each month. I’m also particularly skeptical when I see unusual consistency in the number and value of summary data with very little bank activity. Such an example would be a bank statement that consistently shows only 3-4 deposits each for over $100,000 and miniscule withdrawals such as a few small checks or a handful of fast food POS debits comprising all withdrawals for example. The business could be legitimate and the merchant simply submitted the wrong bank statement, which does not allow you to see the better cash flow picture from first glance, or the merchant could have simply taken the easy way out in creating a basic bank statement. Again, it is helpful to reference the type of business that you are underwriting in order to see if these transactions make sense. I am much more willing to acknowledge and accept this type of statement from a construction company per se than a brick-and-mortar retail shop.

Final Tips

Final Tips

Don’t let analysis paralysis stop you from sticking to your conviction on an account. Underwriting is not directly focused on generating revenue for a firm, but rather minimizing bad debt expenses at the end of the day. If you feel like something is off on the statements that you are looking at but you just cannot find what is wrong, step away from your computer for a few minutes and focus on something else. When you return to your computer, you’ll better be able to scrutinize the statements and more likely to catch something miniscule that you may have missed from closely going over the statements again and again.

You can also ask fellow colleagues to look at the statements. Try experimenting and let at least one know that you have suspicions on a particular account and if they could take a close look at the statements; it also helps if you have someone else simultaneously looking at the same account but do not tell them about your suspicions on the account. If they also have a strange feeling about the statements, chances are that there is something off that warrants even closer examination. Lastly, when in doubt try to confirm the statements with the source of the statement. It may be beneficial to request that your merchants provide you with a bank representative’s contact information so that you can verify the legitimacy with the bank yourself.

Another source of action would be to have a merchant provide your company with a view only access of the account. This would also allow you to directly confirm the legitimacy of the statements eliminating any left over suspicions. The only downsides to these last two approaches is that they make take some time to complete, oftentimes a merchant is not willing to wait a few more days and will willingly go to a competitor who can promise to have them funded within 24 hours. In these cases, your last line of defense comes down to the merchant interview part of the process.

Merchant Cash Advance Now In-Depth

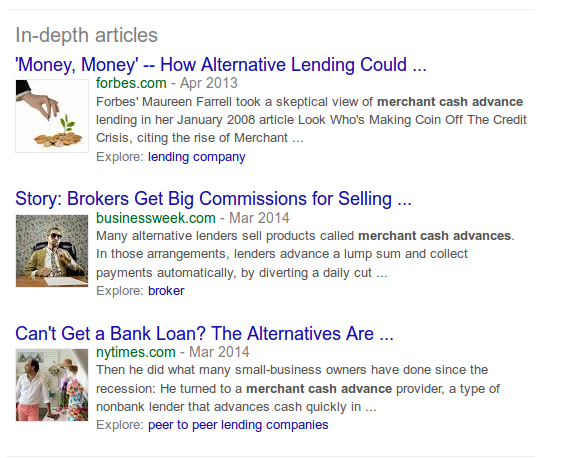

December 1, 2014For quite possibly the first time ever, Google has blessed merchant cash advance with its own array of In-depth articles. What are In-depth articles? Why, they’re featured stories at the bottom of the normal search results. The In-depth feature launched in 2013 and has only worked for certain keywords.

Today it appeared for the very first time for the keyword merchant cash advance

Since Google experiments constantly and shows different results to everyone, it’s possible that you’ve been seeing this for some time already.

I had this to say about the feature 16 months ago:

If you’re wondering how websites can prepare themselves to benefit from such rich snippets, I published Schema.org Markup and Rich Snippets for the Little Guy back in August 2013.

Businessweek, NY Times, and Forbes… I’m not surprised that they’re the chosen publications. Truth be told, there may not have been enough written about merchant cash advance to implement this feature until now. Consider this a milestone.

Merchant Processing Resource is Now deBanked

December 1, 2014 Back in July 2010, I launched www.merchantprocessingresource.com as an independent resource for merchant processing and merchant cash advance. At that time I was celebrating my 4th anniversary of working in the merchant cash advance business and realized there was little to no information about the industry online.

Back in July 2010, I launched www.merchantprocessingresource.com as an independent resource for merchant processing and merchant cash advance. At that time I was celebrating my 4th anniversary of working in the merchant cash advance business and realized there was little to no information about the industry online.

For the last 4 and a half years, this website under that name has been visited by hundreds of thousands of people, many of whom were new to the business or interested in getting into it. I’ve received thousands of emails and responded to an insane amount of questions.

In 2010, 95% of all merchant cash advances relied on merchant processing. For those that remember, funding was in many ways secondary to acquiring merchant accounts. But the industry has evolved and other related financial alternatives have sprouted up around it.

Over time I found myself exploring new avenues and relaying what I’ve learned or what I knew with the rest of the world.

Merchant Cash Advances may have started off as a product for those underserved by banks but it has morphed into an option for bankable businesses that would rather skip the bank. In a sense, today’s capital-seeking merchants are deBanking.

Consumers too are turning to peer-to-peer platforms and crowdfunding campaigns instead of credit cards and bank loans.

And then there’s myself. I started buying into Lending Club loans in January of 2014, almost a year ago. The returns crush what I could earn with a savings account or CDs. The bank is the least attractive option if you want to earn a return on your money.

But it goes beyond lending and earning interest. All the big conferences this year were filled with bitcoin enthusiasts, a payment technology and currency that is not only independent of government, but of banks. Of course I gave it a look and loved it. I shared my feedback in a post titled, My Journey to Bitcoin.

Merchant Processing and Merchant Cash Advance may have kicked off this blog, but four and a half years later, it’s time to acknowledge the other forces, many of which I have already been covering for quite some time.

With 2015 right around the corner, the world is deBanking in more ways than one.

I’m deBanked.

Are you?

The Funding Calls That Won’t Stop

November 23, 2014“Your business has been approved for a loan…”

Last week, Chicago Public Radio (WBEZ 95.1 FM) investigated a trend in the small business community, the use of merchant cash advance financing. The station called me in advance to answer some questions about merchant cash advances and I gave my best explanation of the industry and its products.

Of the discussion that lasted more than 30 minutes, only about five of my sentences made it on the air. While I clarify some of my positions below, it was sobering to learn the context of how they were used, as a defense to real life merchant complaints.

The satisfaction rate with merchant cash advances are pretty high and I say that mainly because it’s so rare to hear complaints from anyone other than journalists that can’t believe anyone would accept rates above 6% APR. And while there are indeed bad actors in the industry (as there are in any industry), the gripe one merchant had about phone solicitations that just won’t stop is a recurring theme.

It’s happening to me too.

As an account representative in 2010 calling real time leads sold to five parties at once, I did what anyone would do, I pretended to be a small business myself and inquired through the website that we bought leads from and entered my cell phone as the point of contact

Ring. Ring. Ring…

Within a half hour, representatives from four companies called me, and I learned exactly who my competition was, how they explained the product, and what they would say to win me over. Two of the four were really good and one even referenced my name personally, saying something to the effect of, “If you get a call from Sean Murray, his rates are worse than mine.” Obviously he had already done what I was doing now, which was pretend to be a small business so he could prove to the prospect he was well informed about the alternatives. He had heard my pitch already and was now throwing me under the bus by planting the seed that I was going to offer something more expensive even if it wasn’t the truth.

In the end none of them won because it was all a farce. One never called me again after the first call. Another kept at it for a week and the remaining two followed up for a month.

And then it got quiet…

I had been marked as a dead lead and forgotten about until three months later when one company sent a follow up email. “Smart,” I thought. But then a call came six months later, and then more emails, some from companies I didn’t originally engage with.

And they continued at regular intervals, every couple of months an email or call. Was it interesting? Yes. Annoying? No.

Until this year.

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The press 9 option doesn’t work for me. Sure, I might be removed from that marketer’s list, but it in no way removes you from anyone else’s list. I knew that already of course because I’ve been on the other end before.

The first time I got one of these calls, I was excited to tell the sales representative who I really was, level with him, and explain that it was a really good idea to take me off the list. But much like other business loan robo call complaints, the representative wouldn’t tell me anything about himself or his company.

I got yelled at.

Every time I tried to ask a question, he’d get louder, insisting I tell him my monthly gross sales volume for the “cash advance I wanted.”

A rogue actor maybe, but I’ve since gotten additional business loan robo calls and have made no progress in getting myself removed. I just hang up now.

Call it sweet irony perhaps. Or maybe a wake up call (pun intended). I applied on a website once four years ago and the rest is history.

My experience with repeat solicitations is marginal compared to somebody that has actually used a merchant cash advance. With the filing of a public UCC-1, anyone in the industry can easily access that data and convert it into a marketing list. And they do.

Brokers that scorn UCC marketing acknowledge that these businesses could be getting called 5-10 times a day. My own clients had reported repetitive calls back when I was an account representative. And while UCC marketing is very cost effective, in today’s market where more than a thousand companies are offering similar financial products, it’s probably safe to say it’s overly saturated.

And if 5-10 calls per day were even remotely accurate, I’d surmise that level of volume is marring the industry’s reputation as a whole.

I could argue though that when customers have a great many options to choose from, they win. With more than a thousand companies offering merchant cash advances and business loans, it’s truly a buyer’s market. Play all the companies against each other and you should end up with the best possible terms. It’s a great time to seek capital.

Except we’ve got to do something about those phone calls, or at least the robo calls.

Every angry robo dial recipient becomes one less person likely to speak positively about the the nonbank financing industry. Aged leads, UCCs and phone calls might be inexpensive, but the cost to undo negative preconceived notions is immeasurable.

Do you want to be known as the company that helped small businesses or the annoying people that won’t stop calling? If merchants are taking to the air waves to complain, it will only be a matter of time before the FTC and FCC become interested.

—

Regarding my comments on the radio about APRs and daily amortization, they were pulled from a conversation that compared daily payment loans to purchases of future sales. I DO believe bad actors exist and every business owner should have an accountant, lawyer, or savvy third party review any contracts they enter into, financial or otherwise.