The ‘Loan’ Star State – Texas is an alternative finance nexus

June 15, 2017

We’re at Able Lending in Austin, Texas, a financial technology company occupying three floors deep in the heart of the Seaholm power plant overlooking Lady Bird Lake. The fortress-like building anchors an inner-city complex of offices and residences, chic restaurants, boutique shops, and a Trader Joe’s.

Once the main source of electricity for Texas’s capital city, the natural gas-fired boilers have given way to a warren of glassed-in offices and meeting rooms connected by angular metallic stairways and a carpeted mezzanine.

It is here, in a tiny conference room, that Will Davis, a slim man of 35 and an alumnus of Harvard Business School, is drawing a bell curve on a whiteboard. Dressed for the balmy Texas weather in tan Bermuda shorts, a black tee-shirt and Nike running shoes, the company’s chief executive and co-founder is explaining how Able’s friends-and-family lending formula “widens” the risk curve.

“We all compete here in this box on price,” Davis says, drawing a square at the topmost point of the bell curve, indicating where the near-prime borrowers abide and where lenders are crowded in pursuit. But when loans from friends and family form 10%-15% of the total loan, he says, drawing squiggly lines just to the left of the box, a cohort with less-than-stellar credits now becomes credit-worthy.

Because of the “peer pressure” and “behavioral change” exerted by the involvement of family and friends, the formula produces a “positive-selection effect on the loan portfolio” Davis says, declaring: “We can serve more of the market.”

It all sounds very business-schoolish. But here’s the bottom line: Able’s lending model sharply reduces both risk and borrowing costs, allowing it to go head-to-head with national rivals like Funding Circle, Bond Street, OnDeck and StreetShares. Thanks in large part to its reduced risk, asserts Able’s director of development, 30-year-old Matt Irving, the Austin fintech can lend twice as much money as its competitors at half the interest rate.

Since opening its doors and firing up its computers in the fourth quarter of 2014, Able’s average loan size has climbed to $231,200 from $100,000. Of that, an average of 3.2 “backers” have accounted for $40,691, or 17.6% of the average total loan amount. The average “blended” annual percentage rate is 16.41%.

Meanwhile, Able, which has made some $48 million in loans to entrepreneurs through the end of April, 2017, reports CEO Davis, is itself on sound financial footing. According to the data-services firm Crunchbase, Able has raised $12.5 million in three rounds of venture capital financing from 21 investors. Principal equity financiers are Peter Thiel’s Founders Fund, Peterson Ventures, RPM Ventures, and Blumberg Capital. On Sept. 27, 2016, moreover, Able added another $100 million to its arsenal in debt financing from Community Investment Management, a San Francisco investment firm. Borrowers include owners of food trucks and apparel shops; professionals including doctors, dentists, veterinarians, and accountants; “creatives” like public relations and advertising firms; and construction companies. Since its inception, Davis says, just one borrower has defaulted, resulting in an $85,000 charge-off.

So far in 2017, the company has lent out nearly $15 million in the first quarter, but it’s on track to make $80 million this year. “We’re ramping up,” Davis declares.

Welcome to fintech in the Lone Star State. While everything may be bigger in Texas, as the saying goes, that’s not quite true of financial technology. The geographic contours of fintech operations are roughly 60% in California (especially Silicon Valley/San Francisco), 30% New York, and 10% scattered about the rest of the country, says 40-year-old Mihir Korke, the San Francisco-based chief marketing officer at Able.

Nonetheless, Texas offers fertile ground for the burgeoning fintech industry. The vaunted Texas business climate promises a relaxed regulatory regime, the absence of either a personal or corporate income tax, and a lower cost of living. All of which were cited by Able Lending, as well as an additional pair of fintech companies that specialize in factoring and merchant cash advances: Jet Capital, located in North Richland Hills in the Dallas-Fort Worth “metroplex”; and Ironwood Finance in Corpus Christi, a port city on the Gulf of Mexico.

“What’s interesting about fintech companies is that they can choose to locate where they want to do business,” says Erin Fonte, an attorney at Dykema Cox Smith in Austin whose legal practice includes mobile payments, mobile wallets and financial technology. “They don’t necessarily get a regulatory advantage because much of what they do is based on their customers’ location,” says Fonte, who is currently serving as a member of the Federal Reserve’s Faster Payments Taskforce. “That said,” she adds, “some companies have chosen to locate in Texas because of the labor and talent pool, because it’s a good source of venture capital, and it’s more affordable.”

Jet Capital’s 42-year-old chief executive, Kenneth Wardle, confirms many of Fonte’s observations. “So far, Texas has been friendly to MCA companies,” he says, using the initials for “merchant cash advance.” Especially favorable to his industry is the fact that “Texas regulators do not define an MCA as a loan,” he adds.

Prior to co-founding Jet Capital with chief operating officer Allan Thompson, 49, Wardle served as a portfolio manager at Exeter Finance Corp, a $3 billion company in nearby Irving which specializes in subprime auto financing. Wardle has also held leadership positions at AmeriCredit Corp., now GM Financial, and Drive Financial, now Santander Consumer USA.

His 20-year background has included the gritty work of repossessing cars when owners fell into arrears on their auto loans. “Most of my career in auto finance was in risk management and I’ve driven a repo truck,” he says. “You take off with the car right away and then chain it down after you’ve gone a couple of blocks so you don’t lose it out on the highway.”

Backed by more than $5 million in equity financing from a family office in Puerto Rico, Jet Capital makes cash advances of $25,000-$30,000, on average, for working capital.

The sweet spot for Jet’s financings are retail establishments, trucking companies, hair-and-nail spas, and medical doctors. Doctors in particular are prime candidates for a Jet cash advance. “They have a pretty good gap between when they perform services and when they get paid by insurance companies” during which they have to cover payroll expenses and overhead, Wardle notes. Prospecting for customers is done largely through independent sales offices, direct mail, and pay-per-click services offered by Google, among additional online channels.

“Our defaults are relatively in line with expectations” and were largely confined to the first year of business, Wardle says. “We made some underwriting and verification changes last September and October,” he adds, “and we changed our minimum credit scores. Since then we’ve seen defaults migrate in the right direction.”

Since Wardle and Thompson took occupancy of an empty office outside Fort Worth in October, 2015, Jet has grown to 12 employees who today have “a variety of roles” says Thompson, citing sales, underwriting, customer service, collections, analytics, and information technology. “They wear a lot of hats and there’s a lot of cross pollination,” he says.

Since Wardle and Thompson took occupancy of an empty office outside Fort Worth in October, 2015, Jet has grown to 12 employees who today have “a variety of roles” says Thompson, citing sales, underwriting, customer service, collections, analytics, and information technology. “They wear a lot of hats and there’s a lot of cross pollination,” he says.

Looking ahead, Wardle foresees Jet expanding its product line beyond merchant cash advances to offer lines of credit and installment loans. “Our goal is to be a one-stop, nonbank financing solution,” Wardle says.

Kevin Donahue, 37, owner of Ironwood bootstrapped the South Texas company, which opened in 2013 using personal savings of $1.5 million remaining from the sale of mobile home parks in South Dakota and Texas. He also plowed earnings into Ironwood from a subsequent job as a commercial loan broker.

Donahue, who grew up in a family of fishermen on the Oregon and California coasts and is a 2006 graduate of California Polytechnic State University at San Luis Obispo, says that he turn up in Corpus Christi somewhat by accident. While operating the mobile home park in nearby Kingsville, he got married, started a family, and put down roots.

With 20 employees, Ironwood focuses on providing merchants cash advances in the $5,000 – $50,000 range, Donahue says, “but we can go up to $1 million.” The average cash advance – usually $10,000-$15,000 – is put to use as working capital by what he dubs “Main Street” businesses: restaurants, boutiques, trucking and transportation companies, professionals, and contractors. Ironwood charges clients factoring fees that are collected via ACH.

“Many times (these businesses) don’t qualify for bank loans,” Donahue says. And even when they do qualify, he notes, “banks take forever – up to three months – while we’re using our own money and can do it in three days. We’re very low on requiring a lot of documents.”

For his part, Donahue wants to see a customer’s bank statements, a photo I.D., voided checks, and a financial report. But, he says: “Cash flow is much more important than financials.”

Clients typically find their way to Ironwood through the website, although they often arrive through referrals from brokers and real estate agents, attorneys, accountants and “anyone doing commercial lending,” he says. Donahue says he closed down a call center. “The way to get leads is more through relationships than marketing,” he says.

Trucking companies are important customers. “They work on thinner margins, the barriers to entry are lower, sometimes their customers don’t pay their bills,” Donahue says of the industry’s economics. “They have huge expenses for fuel, payroll, insurance – and they might not get paid (by their customers) for 30 days or more.”

Ironwood’s advance for a million dollars, cited earlier, was made to a trucking company in Midland, Texas, which hauled both general freight and oilfield equipment. The money was put to use both to smooth out cash flow and as growth capital. The trucking concern “used part of that for expansion, making down-payments with Volvo or Peterbilt,” Donahue recalls.

Backstopped by the titles for 18 trucks valued at roughly $1.5 million, the deal was structured as a three-year, sale-leaseback agreement with “no interest” but rather a fee, Donahue says. Payments were $32,000 monthly, he says, amounting to $152,000 above the advance.

Donahue has no trouble justifying the steep fee schedules. Not only does he release money quickly but in many instances Ironwood has stepped in to bail out businesses that could have gone belly-up. He cites a trucker in the Midwest who had a “very lucrative” business hauling Boeing jet engines worth $30 million to Seattle where they could be worked on and returned to the planes for installment. In order to fulfill the contracts – which earned the hauler $25,000 monthly — the trucking company’s owner needed to purchase pricey insurance.

The owner, however, “had horrible credit,” Donahue says, largely the result of cash flow problems after investing in a special trailer for the jet engines, compounded by a messy divorce. To secure the $10,000 for the special insurance, the trucker sold Ironwood $14,000 of their future receivables. “For his investment of $4,000 he’s making $25,000-a-month forever,” Donahue explains.

Back in Austin, Able is gearing up for another round of capital-raising to bulk up staff and, according to Korke, win licensing to do business in California. At the same time, its friends-and-family credit structure is winning kudos for reaching what researcher David O’Connell calls “the unloaned.”

A senior analyst at Aite Group, a Boston-based consulting firm, O’Connell recently completed a study disclosing that 35% of small and medium-sized businesses in the U.S were unable to obtain credit over a recent two-year period. Able’s lending model is “a good example of using covenants to structure a deal that brings down borrowing risk,” the Bostonian says. “It’s terrific.”

A senior analyst at Aite Group, a Boston-based consulting firm, O’Connell recently completed a study disclosing that 35% of small and medium-sized businesses in the U.S were unable to obtain credit over a recent two-year period. Able’s lending model is “a good example of using covenants to structure a deal that brings down borrowing risk,” the Bostonian says. “It’s terrific.”

Able’s staff doesn’t have to travel far to witness the fruits of their efforts. On Congress Avenue, in the heart of downtown Austin, is Jae Kim’s food truck offering Korean barbecue thanks to a $100,000-plus loan from the fintech lender. Kim, the founder and chief executive at food vendor Chi’lantro, enlisted his mother to pitch in $10,000. All told, family and friends ponied up 30% of the total loan.

In the three years since he hooked up with Able, Kim has gone on to bigger things, including a television appearance last November on Shark Tank that netted him $600,000 from celebrity investor Barbara Corcoran.

Chi’lantro is now operating five restaurants and four food trucks and as Kim disclosed on Shark Tank, annual sales topped $4.7 million last year.

Able Funds Chi'Lantro from Able Lending on Vimeo.

In an interview, he told deBanked that he counts himself fortunate to have gotten the Able “micro-loan.” It played a key role in generating the cash flow that qualified his company for a $200,000 bank loan backed by the Small Business Administration. “It was one of many opportunities, and now we have good relationships with banks,” he says.

And then, a little farther south, there’s Stephanie Beard’s “esby apparel,” a women’s clothing boutique named for her initials. Beard, 35, came to Austin in 2013 after a decade in New York designing men’s clothing at Tommy Hilfiger and Converse. Originally from North Carolina and a graduate of Appalachian State University, she had zero connections in Texas and only a little money.

But she had a big vision: She would open a store and design and sell top-quality, flattering clothes for women that had “a menswear mentality.” Men, she had discovered, buy fewer clothes than women. But men tend to buy clothes that are durable, clothes that they can wear again-and-again over many years. After she sold $65,000 worth of her casual clothing line on the website Kickstarter, Beard developed a fan base and was put in touch with Able. “Actually, they contacted me,” she says.

To qualify as an Able borrower, Beard assembled $20,000 from friends and family, she reports, including $2,500 from her future mother-in-law, another $2,500 from the proprietor of a dress shop that “wholesaled” her collection, and the rest from aficionados of her wares. Once that money was gathered, Able lent her $100,000 at a 10% APR in October, 2014, which enabled her to open her shop. The combined interest rate was 9.8%. Monthly payments have automatically been withdrawn from her business’s checking account.

She’s scheduled to repay both Able and her backers in full by this October. Total sales for the shop have cleared $1 million and Beard expects annual revenues for 2017 to hit $900,000. “A lawyer friend who helped me out with the paperwork pro bono told me that Able was practically giving money away,” she says. “I definitely was lucky.”

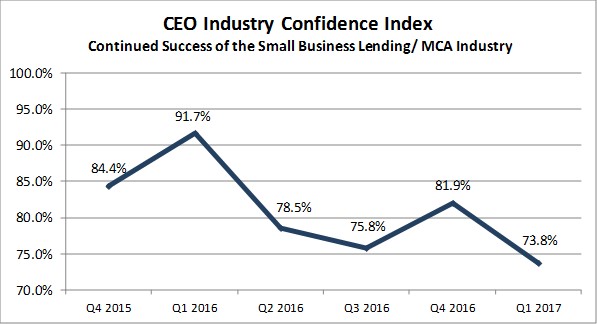

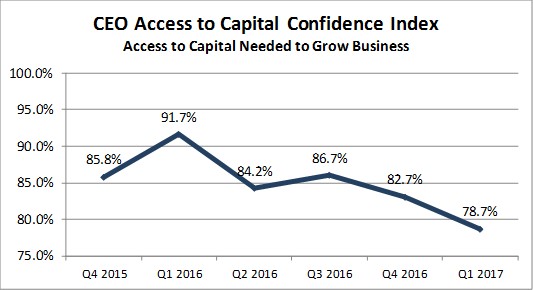

Industry CEOs Were Less Confident in Q1

June 6, 2017According to the latest quarterly Bryant Park Capital/deBanked survey of industry CEOs, confidence dropped to the lowest levels since the survey first began in Q4 2015. Specifically, confidence in being able to access capital needed to grow dipped down to 78.7% from 82.7% in the prior quarter. Confidence in the continued success of the Small Business Lending & MCA Industry shrank from 81.9% in Q4 to 73.8% in Q1.

See the trends below:

The survey does not ask participants to offer a reason for their confidence but the drop could probably be partially attributed to the events that occurred at CAN Capital, OnDeck’s struggles, and a general correction that took place at several other competing firms.

Commercial Finance Coalition Continues to Engage

June 1, 2017

A sign of a mature industry? The Commercial Finance Coalition is becoming a major liaison between the merchant cash advance industry and Washington. Just as peer-to-peer lenders and electronic payment companies have their own trade associations, the CFC is regularly engaging with legislators to offer their input where needed. And that requires a concerted effort, as evidenced by the group’s most recent trip that included meetings with 26 Members of Congress and senior staff. Those are typically separate individual meetings so you can imagine the amount of time and preparation involved.

“The Commercial Finance Coalition (CFC) conducted our third Washington, DC legislative fly-in last week,” Dan Gans, the CFC’s executive director, said to deBanked. “Fifteen members of the organization attended as well as a few prospective members. The CFC continues to establish itself as the premier trade group in the MCA and alternative small business finance space.”

The CFC also gets involved at the state level and played a role in preventing harmful legislation in New York a few months back. Most importantly, their mission is to simply tell their story.

“Studies show that traditional banks cannot meet the overwhelming demand for small business capital in the United States and we be believe that CFC members help thousands of entrepreneurs grow and sustain their businesses,” Gans explained. “We believe it is critical to educate policy makers in Washington and in state capitals like Albany and Sacramento about the vital role our industry plays in helping small businesses achieve success.”

The CFC is not the only trade association in the industry, but they have made political engagement a focal point of their mission since they were founded 18 months ago.

Gans elaborated on this. “Since its establishment in January of 2016, the CFC has been educating Members of Congress and state legislators about MCA and non-bank small business finance. We give our members a needed voice with elected officials and regulators. I would encourage anyone in the MCA space that is not a CFC member to inquire about membership. The industry is facing many threats and it is important that groups like the CFC stand in the gap to educate government leaders about the thousands of jobs advances from our members create across the country.”

To inquire about CFC membership, they advise to please contact Mary Donohue at mdonohue@polariswdc.com or call (202) 368-9758.

Full disclosure: I have accompanied the CFC on their DC fly-ins and the engagement is every bit as real and consequential as it sounds.

Federal Court Agrees, Merchant Cash Advances Not Loans or Usurious

May 13, 2017 By now, numerous judges in the New York Supreme Court have concurred that purchases of future receivables are not loans nor usurious, yet challenges to these contracts continue. In the latest landmark ruling, defendants/counterclaim plaintiffs Epazz, Inc., Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley, moved to have the original action involving their merchant cash advance dispute transferred from state court to federal court, perhaps hoping for a different opinion on whether such agreements are usurious.

By now, numerous judges in the New York Supreme Court have concurred that purchases of future receivables are not loans nor usurious, yet challenges to these contracts continue. In the latest landmark ruling, defendants/counterclaim plaintiffs Epazz, Inc., Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley, moved to have the original action involving their merchant cash advance dispute transferred from state court to federal court, perhaps hoping for a different opinion on whether such agreements are usurious.

The law was not on their side. In the Southern District of New York, a federal court, the Honorable Louis L. Stanton echoed on May 9th, 2017, what state judges have been saying all along, that a purchase is not a loan because the purchased receipts are not payable absolutely.

In this case, the “receipts purchased amounts” are not payable absolutely. Payment depends upon a crucial contingency: the continued collection of receipts by Epazz from its customers. TVT [TVT Capital] is only entitled to recover 15% of Epazz’s daily receipts, and if Epazz’s sales decline or cease the receipts purchased amounts might never be paid in full. See counterclaims, Exhs. A-C at 1. The agreements specifically provide that “Payments made to FUNDER in respect to the full amount of the Receipts shall be conditioned upon Merchant’s sale of products and services and the payment therefore by Merchant’s customers in the manner provided in Section 1.1.” Id. at 3 § 1.9.

Defendants’ argument that the actual daily payments ensure that TVT will be paid the full receipts purchased amounts within approximately 61 to 180 business days, id. ¶¶ 33-47, is contradicted by the reconciliation provisions which provide if the daily payments are greater than 15% of Epazz’s daily receipts, TVT must credit the difference to Epazz, thus limiting Epazz’s obligation to 15% of daily receipts. No allegation is made that TVT ever denied Epazz’s request to reconcile the daily payments. TVT’s right to collect the receipts purchased amounts from Epazz is in fact contingent on Epazz’s continued collection of receipts. See Kardovich v. Pfizer, Inc., 97 F. Supp. 3d 131, 140 (E.D.N.Y. 2015), quoting Amidax Trading Grp. v. S.W.I.F.T. SCRL, 671 F.3d 140, 147 (2d Cir. 2011) (“Where a conclusory allegation in the complaint is contradicted by a document attached to the complaint, the document controls and the allegation is not accepted as true”).

None of the defendants’ arguments, Counterclaims ¶¶ 51-109, change the fact that whether the receipts purchased amounts will be paid in full, or when they will be paid, cannot be known because payment is contingent on Epazz generating sufficient receipts from its customers; and Epazz, rather than TVT, controls whether daily payments will be reconciled.

The decision relies heavily on the reconciliation clause common to merchant cash advance agreements, whereby merchants can adjust their daily ACH amounts to correlate with their actual sales activity. This concept is explained at length in the Merchant Cash Advance Basics training course.

Furthermore, the court was incredulous over the defendants’ claim that they actually wanted loans but were instead fraudulently induced into purchase agreements.

Defendants do not claim that they were misled with regard to the amount of their payment obligation, only that they were misled into believing that their repayment obligation would be absolute when it actually is contingent. Their injury from that is unclear.

In short, the judge suggests that entering into a loan would’ve been worse because it was absolutely repayable, whereas the purchase agreement was not. So how could they have been damaged?

The entire decision surrounding all the claims can be downloaded here.

The case is Colonial Funding Network, Inc. as servicing provider for TVT Capital, LLC v. Epazz, Inc. Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley in the United States District Court’s Southern District of New York. Case: 1:16-cv-05948-LLS.

Defendants Shaun Passley and Epazz also lost challenges in another merchant cash advance case in the New York Supreme Court.

Exercise of Ordinary Intelligence Would’ve Revealed Merchant Cash Advance Contract Was Not a Loan, Court Says

May 9, 2017 In the New York Supreme Court, the Honorable Linda S. Jamieson was tasked with ruling on twelve causes of action in a merchant cash advance contract case. While the 18-page decision covers a lot of ground, one notable section was the plaintiffs’ request for rescission based on “misrepresentations or unilateral mistake” and “damages for fraudulent inducement.” According to the order, the plaintiffs, K9 Bytes, Inc., Epazz, Inc., Strantin, Inc., MS Health Inc., and Shaun Passley, “claim that the defendants misled them by representing that they were entering into “loans governed by usury laws,” but instead caused them “to enter into ‘merchant agreements.'” Exhibits on the docket attached by the plaintiffs purport to demonstrate the word loan being used in communications, though the judge noted that the plaintiffs failed to identify how the individuals in those communications specifically attributed to the defendants. Nevertheless, the judge was unmoved by plaintiffs given the overt language spelled out in the contract itself.

In the New York Supreme Court, the Honorable Linda S. Jamieson was tasked with ruling on twelve causes of action in a merchant cash advance contract case. While the 18-page decision covers a lot of ground, one notable section was the plaintiffs’ request for rescission based on “misrepresentations or unilateral mistake” and “damages for fraudulent inducement.” According to the order, the plaintiffs, K9 Bytes, Inc., Epazz, Inc., Strantin, Inc., MS Health Inc., and Shaun Passley, “claim that the defendants misled them by representing that they were entering into “loans governed by usury laws,” but instead caused them “to enter into ‘merchant agreements.'” Exhibits on the docket attached by the plaintiffs purport to demonstrate the word loan being used in communications, though the judge noted that the plaintiffs failed to identify how the individuals in those communications specifically attributed to the defendants. Nevertheless, the judge was unmoved by plaintiffs given the overt language spelled out in the contract itself.

[The plaintiffs] state that they would not have knowingly entered into merchant agreements, because what they really wanted were loans. Indeed, plaintiffs allege that “the word ‘purchase’ or ‘sale’ would have caused Passley to decline a transaction with [defendants] because a loan – the product Passley wanted to obtain – is not a purchase or sale.”

A review of the contracts in this action shows that not only do they all clearly state that they involve purchases or sales, but they all expressly state they are not loans. Even if someone were confused by the contracts, or did not understand the obligation or the process, by reading the documents, one would grasp immediately that they certainly were not straightforward loans. The very first heading on the page was “Merchant Agreement,” and the second heading says “Purchase and Sale of Future Receivables.”

[…] For plaintiffs to state that they would not have entered into a purchase or sale if they had known that that is what they were doing is utterly undermined by the documents themselves. As the Second Department has held, in Karsanow v. Kuehlewein, 232 A.D.2d 458, 459, 648 NY.S.2d 465, 466 (2d Dept. 1996), “the subject provision was clearly set out in the … agreements, and where a party has the means available to him of knowing by the exercise of ordinary intelligence the truth or real quality of the subject of the representation, he must make use of those means or he will not be heard to complain that he was induced to enter into the transaction by misrepresentations.” So too here, plaintiffs had the means to understand that the agreements set forth that they were not loans. As it has long been settled that a party is bound by that which it signs, the Court finds that the ninth cause of action, for recission based on misrepresentation or mistake, and the tenth cause of action, for fraudulent inducement based on misrepresentation, must be dismissed as a matter of law. Pimpinello v. Swift & Co., 253 N.Y. 159, 162-63 (1930) (“the signer of a deed or other instrument, expressive of a jural act, is conclusively bound thereby. That his mind never gave asset to the terms expressed is not material. If the signer could read the instrument, not to have read it was gross negligence; if he could not have read it, not to procure it to be read was equally negligent; in either case the writing binds him.”).

The plaintiffs are likely to be disappointed with the rest of the ruling as well. The decision can be found in the New York Supreme Court in the County of Westchester under Index Number 54755/2016 or can be downloaded in full here.

Words Matter in Contracts (And everywhere else)

April 25, 2017 The Counselor Library conference powered by law firm Hudson Cook LLP was a big hit in Baltimore this week. While focused on consumer lending, they held a special one-day program on merchant cash advance and small business lending. The topics and discussions were off-limits to press reporting but what was largely visible on the exhibition floor was the Merchant Cash Advance Basics training course.

The Counselor Library conference powered by law firm Hudson Cook LLP was a big hit in Baltimore this week. While focused on consumer lending, they held a special one-day program on merchant cash advance and small business lending. The topics and discussions were off-limits to press reporting but what was largely visible on the exhibition floor was the Merchant Cash Advance Basics training course.

Recent merchant cash advance case law suggests that it is of critical importance for sales reps and underwriters to be knowledgeable of their own products. To be specific, the words you use to communicate with merchants over emails, on the phone and in your contracts should always be consistent and in compliance with applicable laws. What you write on forums and the promises you make in your ads should also pass legal muster.

Even if you consider yourself to be an industry veteran, the Merchant Cash Advance Basics course should refresh your memory on fundamental industry practices. If you are a newcomer, consider Merchant Cash Advance Basics an absolute necessity.

Hudson Cook, LLP has established itself as a leader in the MCA legal arena and we were proud to participate in their event.

Text The Merchant, Close The Deal

April 15, 2017

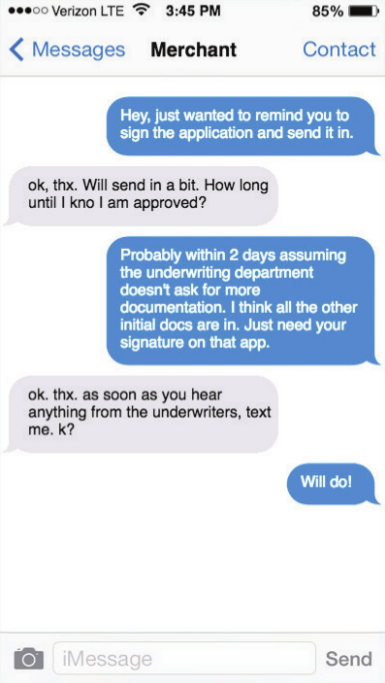

About a year ago, Cheryl Tibbs, general manager of Douglasville, Ga.-based One Stop Funding, was having trouble getting in touch with one of her clients. The merchant in question runs a lawn care service and is usually out on the job, so he isn’t quick to return phone calls or respond to email messages.

“I just got the idea to send a text,” Tibbs recalls. She typed a message expressing her regret for intruding but letting her client know that he needed to take certain steps to advance the funding process for his loan application. He texted right back.

After that initial success, the texting continued between Tibbs and the lawn care provider. He’s been a customer for us for a while, and that’s just how we communicate,” she says. “It’s easy for him to stop and shoot me a text as opposed to having a full conversation with me.”

Tibbs isn’t alone in her appreciation for text messaging as a part of the sales process. Quick responses to texts are making the medium increasingly important in the alternative small-business funding business, maintains Gil Zapata, CEO of Miami-based Lendinero. “Text messaging is more powerful than emailing nowadays,” he declares.

One reason for that shift is that texts are easy to use, according to Tibbs. “It’s a matter of convenience for the merchant,” she contends. “In this business, any way you can make it easier for the merchant to facilitate the transaction with you is the method you have to use.”

Besides the convenience, there’s the sense of urgency people feel when they receive a text, asserts Jeb Blount, a sales trainer who’s written eight sales-oriented books, including the bestselling Fanatical Prospecting. “When you send a text message you move to the top of a person’s priority list,” he says. In fact, people who are talking face-to-face often disengage from the conversation to respond to a text message, he notes. “It’s treated as something that’s urgent.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

Texting has become almost standard procedure at Florida-based Financial Advantage Group LLC, according to Scott Williams, the firm’s managing member. He prefers that sales associates make the initial contact by phone to get a sense of what the merchant is looking for in a funding deal. After gathering information and getting approval, it’s best to send the offer by email so the merchant has “all the numbers in black and white” and more details than a text message can hold, he notes. After that, text messages can deliver requests for additional documentation and provide updates on the progress of the funding process. “We can tell them, ‘Hey, everything got cleared this morning – we should be able to do the funding this afternoon,’” he says.

Texting expedites communication regarding renewals, too, Williams observes. “If a merchant is 50 percent paid back, you can check in and see if they need some additional capital right now,” he says. “It’s really good for that.”

Clients can use messaging to convey images of documents needed in the funding process, Tibbs says. “I had a merchant yesterday who sent me over her IRS tax agreement through picture message,” Tibbs says by way of example. Often, funders request color images of both sides of an applicant’s driver’s license, she notes. To fulfill such requirements, it’s generally easier to snap a photo with a phone and send it as a picture message than to scan pages of paper into a computer to create an electronic document and then send the resulting file by email. “We do a lot with picture messaging,” she observes.

But as useful as text messaging can become for contacting phone-shy clients or helping clients share an image to document a key cancelled check, companies should exercise care when using the medium for prospecting, warns Zapata. He and just about everyone else deBanked consulted emphasizes that sending unsolicited text messages can violate Federal Trade Commission regulations. “Just because our industry isn’t regulated doesn’t mean there aren’t regulations out there on the side,” he says.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

The feds heavily regulate five-digit short-code texts but tread lightly with long-code texts – the ones sent from 10-digit phone numbers, Guggenheim says. The latter would apply in alternative finance, and if a text recipient calls back on the phone number associated with a long-code text, someone will answer, he notes.

Citing guidelines from the Cellular Telecommunications Industry Association (CTIA), Guggenheim stipulates that consumers should have the ability to opt out of additional messages after receiving the first one. Members of the industry who want to send groups of text messages can post conditions on their websites that compel users to grant permission to contact them by text if they submit their contact information, he suggests.

After ensuring everything’s legal, Tucker reports 1st Capital Loans nets a good response when he uses a vendor to blast multiple identical text messages to lists of prospective clients who have already granted permission for his company to contact them by text message. The strategy has helped bring in a reasonable number of deals because the prospects were “already in the pipeline,” he notes.

Remember, though, that cell phone numbers change more often than land line numbers, Tucker cautions. That means a call to a number that’s been reassigned could inadvertently fall into the unsolicited text message category that violates federal rules, he says. “You could be texting a 14-year-old,” instead of a small business, he warns.

When mounting a mass text campaign, marketers are wise to avoid lengthy missives, according to Tibbs. “Keep it simple,” she says. A typical message from her might read: “Looking for funding? Looking for capital? Give us a call,” she notes.

In business texts, avoid acronyms like “LOL” and write in complete sentences with proper punctuation and capitalization, Blount suggests. “Begin by typing out the message somewhere other than in the text box, read it, make sure it makes sense and then send it,” he says. Put your name with the word “from” at the top of the message so the recipient knows who sent it, he emphasizes.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Users can also rely on Guggenheim’s TextUs system to schedule messages for delivery in the future to remind clients of meetings. The system detects land-line numbers and informs the user that the phone will not receive text messages, and it integrates with customer-relationship management systems to exchange information, he says.

So used properly, texting can offer benefits for everyone involved. But some unscrupulous players still insist upon using the medium to mislead prospective clients, says Zapata. His customers have shown him texts from competitors who make initial contact or early contact by sending text messages that might look like offers but are really just marketing letters, says Zapata. That approach, which might tout the availability of $50,000, can cause problems when it turns out that the merchant qualifies for only $25,000, he explains. “Trust me, you’re not going to look like the good guy,” he says of the firms that send what he considers objectionable text messages.

Sensitivity comes into play with text messaging, according to Blount. He and other sources say a great number of people regard email as business-oriented and texts as personal. That leads them to nonchalantly delete unwanted email messages but to become angry when they receive a text they didn’t want, he says. “You can’t send text messages to customers if they don’t know you,” he counsels.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Blount’s example seems to suggest the line between business and personal may be blurring when it comes to texting. People often check their email messages on phones these days – instead of on a laptop or desktop computer – which also minimizes the difference between texting and emailing, says Tibbs. “Everybody does everything with their phone these days,” she notes.

Communicating through a more personal channel such as texting has advantages, too, Williams contends. That’s because some merchants consider their financing to be personal and don’t want to broadcast the details to employees, he says. To protect their privacy, merchants often provide financial institutions with their cell phone number instead of their office number or toll-free line, he notes.

Meanwhile, the world continues to become more comfortable with texting. When Williams and his sales associates began messaging clients about four years ago, they found younger customers receptive and older ones reluctant, he remembers. In the intervening years, however, the 50 plus crowd has warmed to the medium, he observes.

An advantage that accrues with text messaging – compared with email – arises from the fact that spam filters and spam folders don’t seem to have a place in the world of texting. Several sources cite that as a big advantage with using texts. “If you send someone a text message, they’re going to see it,” notes Zapata.

Asked about a downside to the proper use of text messaging in business, most sources could not name one. However, Williams has discovered one area where the mode of communication comes up short. “I would not deliver bad news over text-messaging,” he advises. “If the merchant is upset or frustrated by the news, it would be better-handled in a phone call so you could explain the reason for the negative news. A text message leaves too many things unsaid.”

Nulook Capital Has Filed Chapter 11

April 13, 2017NY-based merchant cash advance funding company Nulook Capital filed for Chapter 11 on April 4th, according to court records. They listed more than $2.6 million in creditor claims. The largest among them was a secured claim for $2 million by a specialty finance company.

Two other creditors in the bankruptcy proceeding are also involved in the merchant cash advance industry.

The voluntary petition was filed in the Eastern District of New York in the United States Bankruptcy Court.