Big Deals, Big Consequences: How some deals went very wrong

June 18, 2026In November 2018, a conglomerate of car dealerships went out of business in California. Within three weeks, a merchant cash advance company, 1 Global Capital, was discovered to have filed bankruptcy as a result. They had lost more than $40 million in that dealership deal alone. Over the ensuing weeks, additional funding companies revealed that they had also been in it and gotten burned, some so badly that they also closed their doors. It was a moment of reckoning for the industry as deals got bigger and the stakes got higher. At the time, it was considered the largest deal (and then the largest default) in history.

Less than two years later, an even bigger deal was revealed, a $91M MCA made by Par Funding. Par also became a rather infamous failed business.

And some time in between the two, a $1B hedge fund that provided credit facilities to small business lenders, also failed and took some lenders down with it.

In each case there was a lesson learned.

1 Global Capital

In 1 Global Capital, internal emails revealed that the company knew the dealerships were on the brink of collapse, but were compelled to keep funding them to avoid taking the loss.

“…if they were to become insolvent, everyone loses,” said 1 Global’s Director of Accounting. The result was they dug a deeper and deeper hole until they were on the hook for tens of millions and their exposure became existential.

1 Global was not forthcoming about the performance of its portfolio to its investors and by the time the dealerships went bust, regulators and prosecutors moved in to deal with the fallout.

Par Funding

In the Par Funding case, foul play appears to have been the defining issue. The large funding amounts and low defaults looked good to the investing public because the books were not being accurately reported. Par was adamant that the power of “compounding” could make up for any losses they incurred, but regulators said they had not even properly disclosed their losses to begin with and investors were not aware of them. The $91M deal was just the tip of the iceberg. Another customer purportedly owed $35M, for example. And then those combined with the next eight largest deals on their books added up to $228M, which made up 54% of their entire portfolio. Par had very severe concentration risk and compounding probably could not save it on other deals if these went bust.

Direct Lending Investments

In the Direct Lending Investments hedge fund case, the CEO had famously proclaimed that small businesses were overpaying for credit and that was how their investors stood to profit. But over time, it became evident that some of the small business lenders they backed actually had customers underpaying for credit and the losses overwhelmed the hedge fund. Unfortunately, the CEO was unwilling to concede the losses and told investors they were actually profitable instead. To try and cover it up and make it back, the hedge fund loaned nearly $200M to telecom companies at high interest rates. And because they made these loans during a state of distress and probably were not underwriting them carefully, the borrowers scammed them and disappeared with the funds. There was no longer a way out and the CEO resigned. The receiver in the case initially estimated that portfolio was then worth $500M less than what they had last reported to investors.

Ironically, the CEOs of all three companies were convicted of crimes for their roles in the lies and the losses.

Concentration risk, misleading investors, and falling victim to the sunk cost fallacy ultimately were their undoing. For some, the deals got larger to try and keep a dead deal from failing. For others, it was a Hail Mary play to try and generate a return to make up for losses elsewhere.

The Fatal Flaw in Upstart CEO’s Vision for AI Underwriting in MCA: A response to Upstart’s view of AI in underwriting

June 12, 2026David Roitblat is the founder and CEO of AI My Advance and Better Accounting Solutions, a leading authority in specialized accounting for merchant cash advance companies alongside our new innovative CRM designed to solve the critical gaps holding the industry back. To connect or schedule a call about working with AI My Advance or Better Accounting Solutions, email David@betteraccountingsolutions.com

As deBanked reported (March 23, 2026), Paul Gu, CEO of Upstart, said something on his company’s Q4 earnings call that has been quoted approvingly in a few corners of the credit world. It deserves a careful read because some important points are incorrect when it comes to the MCA industry.

Gu’s argument, as reported, runs roughly like this. Humans have never been very good at precisely underwriting loans and projecting cash flows. That problem has always been a math problem, not a language problem. The recent wave of AI, the LLMs from Anthropic, OpenAI, and Google, is good at the things humans are naturally good at: reading documents, navigating messy paperwork, perfecting liens, and checking property records. Therefore, in Gu’s framing, LLMs are well-suited to the operational layer around lending but not to the underwriting decision itself. He puts it bluntly: “No matter how many humans you have, you don’t want that army of humans underwriting loans for you.”

The deBanked piece does a real service by reporting it. But the framing carries a serious blind spot. It implies that AI underwriting is essentially a solved problem, owned by structured-data shops like Upstart, and that the broader conversation about AI in lending is mostly noise. For consumer credit, that may be true. For the MCA industry, it is not, and treating it as if it were misses the actual point.

Begin with the parts of his argument that hold up. Underwriting, at its core, is a probability problem. Given a set of inputs, what is the likelihood of repayment, and what is the distribution of outcomes if it fails? That has always been the question, and Gu’s phrasing is exactly right: “That’s something that has always been solved as a big math problem.”

He is also correct in saying that LLMs, in their current form, are not the natural tool for that math problem. They are extraordinary at reading, summarizing, classifying, extracting, and reasoning over language. They are not, on their own, the right architecture for portfolio-level probability estimation. The deBanked piece links to Upstart’s own track record, 91% of their loans now fully automated, and that result was not built on top of GPT-class models. It was built on years of structured-data modeling. Gu is entitled to point that out.

He is also right that the most obvious near-term wins from LLMs in lending are operational: HELOC processing, lien perfection, document review, title work. Anywhere a human currently spends hours reading and routing paper, an LLM can do meaningful work. His framing of those as “the perfect problem to throw sort of LLM-style AI against” is well put.

The problem is the conclusion the framing pushes the reader toward: that because the underwriting decision is a math problem, and because the new wave of AI is mostly a language problem, the conversation about AI in underwriting is largely settled. That conclusion translates poorly from Upstart’s world to ours, and it does so in a way that matters.

Upstart underwrites consumer installment loans. The data is clean, the durations are predictable, the borrowers are individuals with credit files, and the question being asked is essentially: will this person make 36 or 60 fixed monthly payments on time. That is, as Gu says, a big math problem with a long history of structured inputs.

MCA underwriting is not that problem. It is a different problem with a different shape, and the difference is not cosmetic.

An MCA underwriter is not pricing a fixed-term installment loan to an individual with a credit file. They are pricing a daily or weekly remittance against a small business’s future receivables, over a horizon measured in months, where the inputs are messy by nature: bank statements with idiosyncratic categorization, industry-specific seasonality, owner behavior that does not show up in a FICO score, stacking risk, processor changes, lease events, partner disputes, and dozens of other signals that live in unstructured form. The decision is not made once and then monitored passively. It is revisited continuously as the merchant’s behavior evolves over the life of the advance.

That is a different beast, and the math that solves consumer credit does not, on its own, solve it. The part of AI that Gu sets aside, the language part, the unstructured-data part, the continuously-observing part, is precisely the part that matters for the underwriting decision itself in MCA, not just the paperwork around it. Setting it aside is not a clean theoretical move. It is a category error when applied to this industry.

In modern MCA operations, the most important thing AI is doing is not the initial decision. It is what happens after the capital goes out.

Underwriting does not end at approval. Our new and up-and-coming platform continues to ingest merchant behavior after funding. It links directly to merchant bank accounts, monitors post-funding activity, tracks changes in deposit patterns and remittance behavior, and detects patterns across defaulted deals. It does not simply record that a deal failed. It identifies what those failed deals had in common. That information does not sit in a static report. It feeds directly back into how new deals are evaluated.

That is underwriting, too. It is just underwriting, not the single-moment, single-file decision the term usually evokes. It is a feedback system: the decision at funding is the first input, the merchant’s subsequent behavior is the second, and the model that prices the next deal is the third.

Gu’s framing treats underwriting as the moment of decision. In MCA, the moment of decision is a single frame in a longer film. The frames that matter most are often the ones after funding, where a human underwriter cannot realistically hold the pattern in mind across hundreds or thousands of merchants, while a system can. Any framework that ignores those frames does not describe MCA underwriting. It describes something else and calls it by the same name.

This is also where the LLM-versus-structured-model dichotomy starts to fall apart. Reading a bank statement well is partly a math problem and partly a language problem. Categorizing a $4,200 ACH out as a vendor payment versus a stacked advance from another funder is not pure math. It requires reading the counterparty name, recognizing the funder, knowing the industry conventions. That work sits exactly at the seam between what Gu calls “solved as a big math problem” and what he calls “the perfect problem to throw sort of LLM-style AI against.” In MCA, those two are not separable layers. They are the same workflow, and pretending otherwise produces a model of the industry that does not match how the industry actually runs.

The deeper point is that the AI conversation in lending is not one conversation. Upstart’s answer is the right answer for Upstart’s problem. It does not automatically transfer, and the confidence with which it has been quoted in the credit world suggests the transfer is being assumed rather than examined.

Consumer credit, where Upstart operates, has had decades of structured-data infrastructure built around it: bureaus, scores, standardized loan documents, regulated disclosures, and well-defined repayment behavior. A math-heavy, low-LLM approach makes sense there because the inputs were already structured by the time the modeling started.

MCA grew up differently. The data is unstructured by default. The borrowers do not have meaningful credit files in the consumer sense. The product is non-recourse against a fluctuating revenue stream. The lifecycle is short and active. The signal that matters often lives in places, bank statement memos, merchant behavior, processor data, partner disputes, that look like language problems and behavior problems before they look like math problems.

That is why the LLM-style AI Gu is comfortable assigning “around the edges” work, which, in MCA, frequently involves core underwriting. Parsing the statement is part of underwriting. Reading the memo line is part of underwriting. Recognizing the third stacked funder is part of underwriting. Watching how a merchant’s deposit pattern shifts in week three of an advance is part of underwriting. Those are not auxiliary tasks bolted onto a clean math problem. They are the problem.

The disagreement with Gu, then, is not that AI cannot underwrite. He is not really arguing that. His actual position is closer to this: LLMs are not the right tool for the underwriting math, and you should not let the hype around LLMs convince you otherwise. On that, we agree.

The disagreement is this. In MCA, the underwriting problem is a math problem wrapped in a language problem wrapped in a continuous-monitoring problem. The math is necessary but not sufficient. The language and behavioral layers are where modern AI, LLM-style and otherwise, is genuinely changing how deals are priced, monitored, and learned from. With our new and up-and-coming platform, AI My Advance, this is exactly what we do: we parse the unstructured inputs, track merchant behavior after funding, and feed what we learn from defaulted deals back into how the next deal gets priced. Treating that work as merely “operational” is not a small mistake. It is the kind of mistake that produces a confident answer to the wrong question.

Upstart has earned the right to its view. The 91% automation figure is real, and the underlying modeling is serious. But that view was built on a problem whose inputs were already structured. The MCA industry is solving a different problem in real time, and the tools that work for it are not the same tools, in the same proportions, as those that work in consumer credit. The sooner that distinction is named clearly, the better the conversation about AI in lending becomes.

Serial Litigants May Target Websites and “Trackers” As Alternative to TCPA

June 12, 2026![]() The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The merchant alleged that they had only been served ads on social media by that company because they had been tracked from a prior website visit. They hadn’t wanted to be tracked and there was no option to opt out of tracking. As a result, they demanded to be compensated, heftily.

By now, most internet users have at least heard the term GDPR, the General Data Protection Regulation that became a never-ending source of controversy throughout Europe, but not all are aware that states and litigants in the US have tried to create a similar framework for privacy. For some in the small business finance industry, the vast complexity of compliance was not fully understood until the lawyers came calling.

“Pretty much every MCA company is potentially a victim because they’re all doing advertising,” said Richart Ruddie, CEO of Captain Compliance, a firm that specializes in safeguarding companies against these sorts of threats. “What we do is we protect against the rise and surge in privacy lawsuits and privacy litigation. So, anybody running TikTok ads, Facebook ads, Instagram ads, any sort of technology that does session-replay where it watches you move the cursor on the screen, if they’re running Google Analytics, all of these are cases that have been tried and are being litigated over.”

Ruddie said that companies within the small business finance industry, including a few within the segment of MCA, have been hit with claims, and they’re now actively working with them to make sure it doesn’t happen again.

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

The larger issue is that for companies that might already be aware of the risks, the solutions they’re using may not actually be compliant with the laws.

“What’s happening now is there’s a handful of these cookie banner softwares but they don’t work and they’re creating bigger issues because they’re like ‘Hey, you told me I could opt out, and then I turned off the selling and sharing of my personal information and you still track me,'” Ruddie explained.

This is made all the more complex by the fact that there are nearly two dozen states with their own twists on compliance. And a growing cottage industry of serial litigants that know this complexity could make website operators easy targets to profit off of. For instance, some of them are going around and running automated website scans just to see who to target. Ruddie said that he’s seen claims reach into the tens of thousands or hundreds of thousands of dollars for alleged privacy violations.

Preventative measures are within reach, however. Ruddie says that for a brand new customer they can get a company compliant in one to three business days. It’s hard for companies to hide in the shadows if they’re online because it doesn’t take much to see what’s there and what isn’t.

“You can right-click and look at the code and then you can see all the different tech and what’s running on the website,” Ruddie said.

Fed Surveys Show Minimal Change in Regular Financing Product Usage

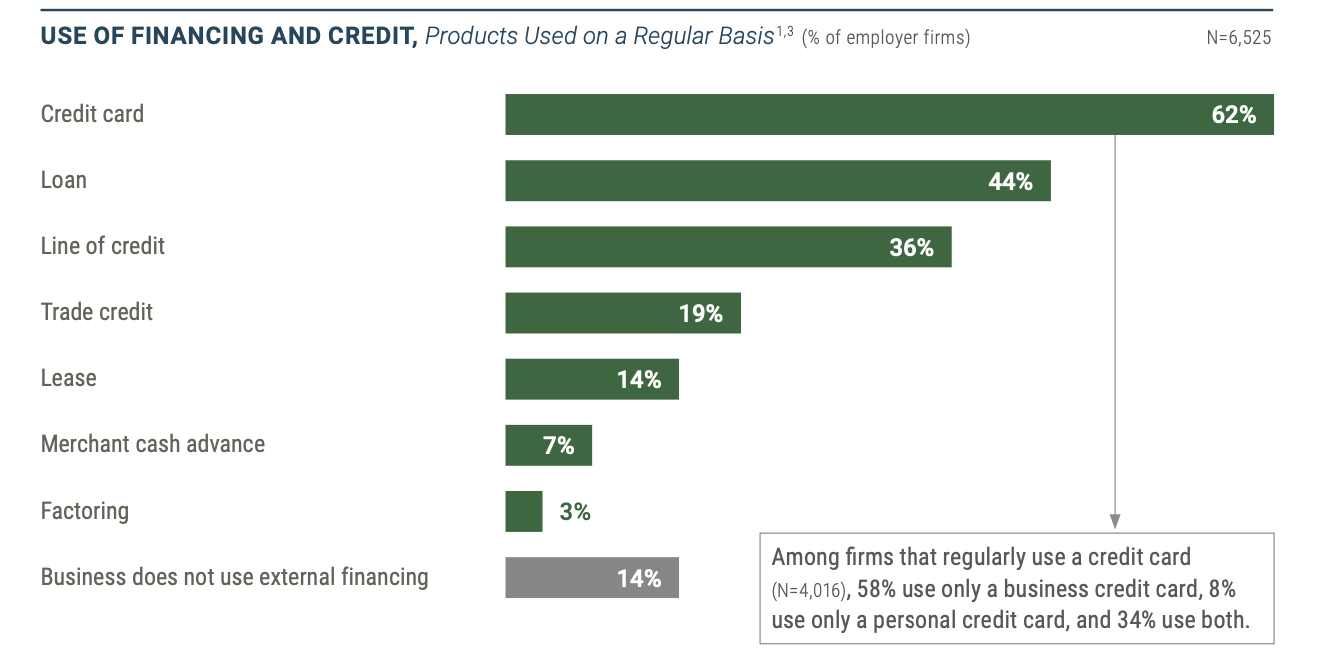

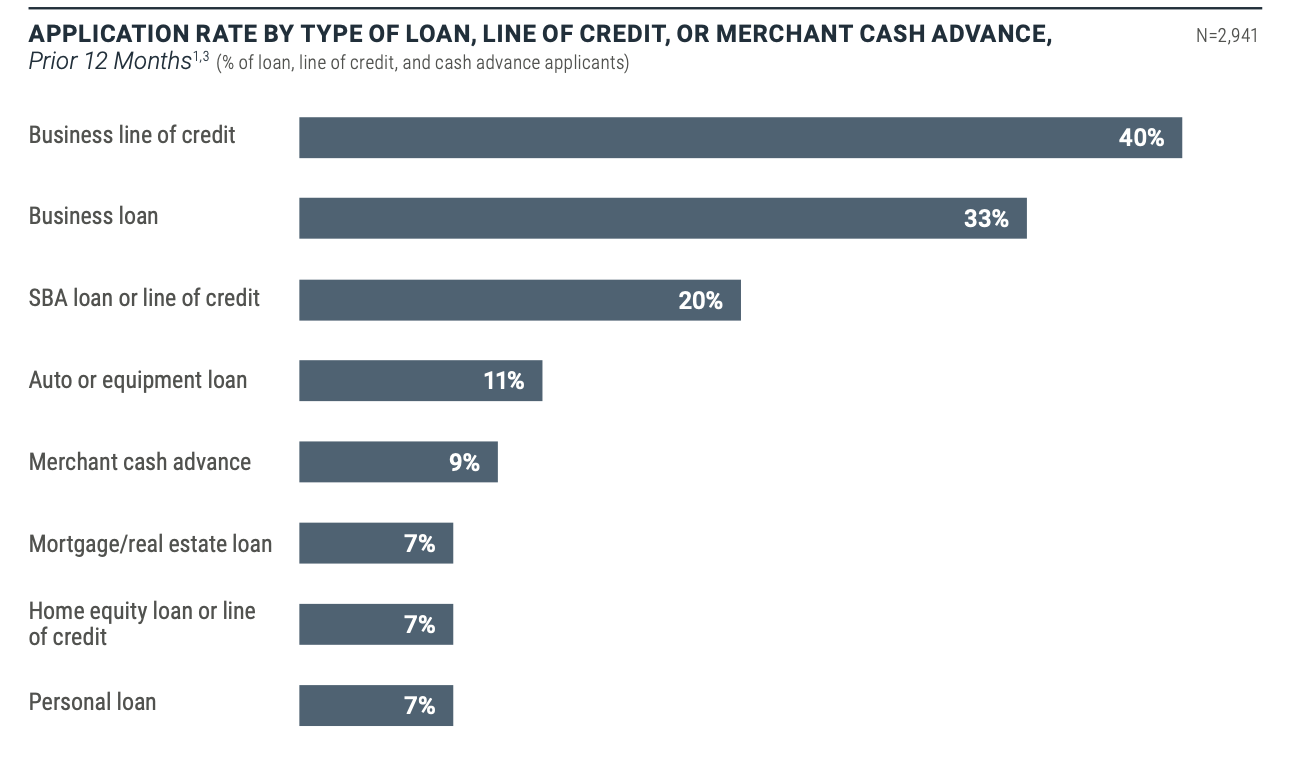

June 9, 2026The Federal Reserve’s 2025 survey of small businesses with less than 500 employees revealed that 7% of them regularly used merchant cash advances. That’s the exact same level reported by business owners in 2017 during the same survey, 7%. While news reports have suggested that the product has grown substantially over an eight-year period, respondents indicate that not much has changed.

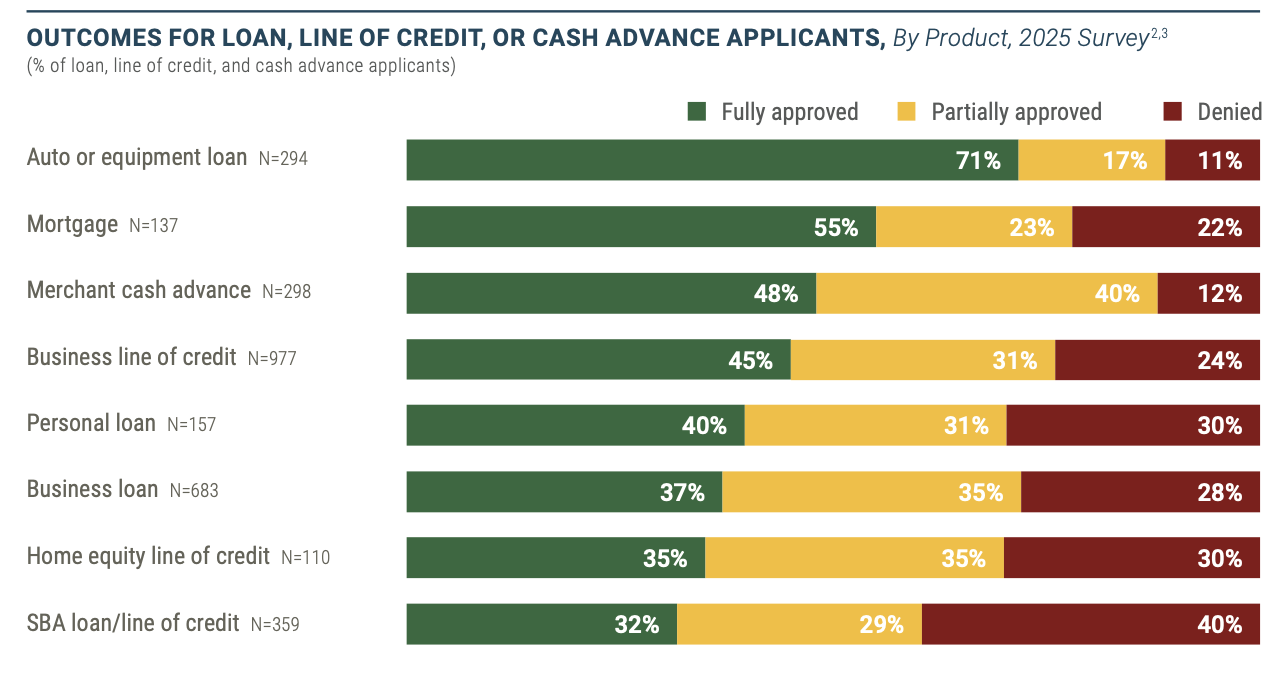

The approval rate for MCAs is also low compared to alternatives in the market. Respondents, for example, reported that in 2025 they were more likely to get approved for an auto or equipment loan (71% got fully approved) and a mortgage (55% got fully approved) than an MCA (only 48% got fully approved). Business lines of credit were right below that with 45% saying they got fully approved for one.

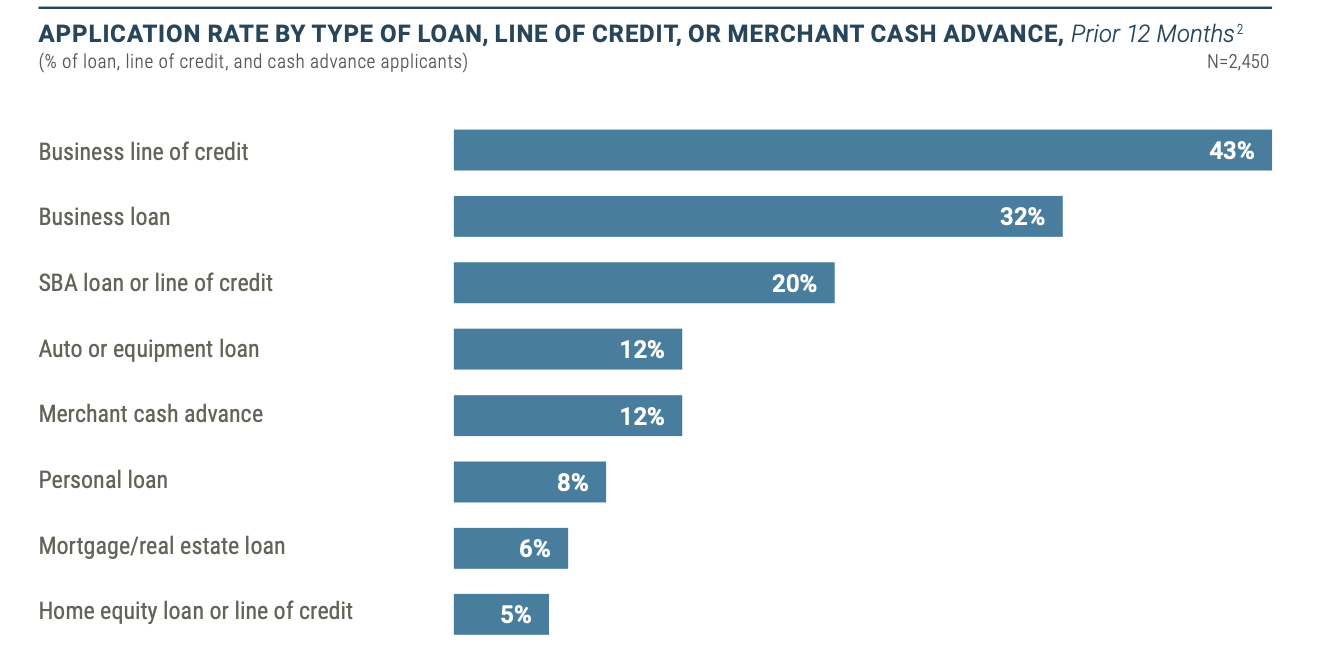

Respondents were also more likely to have applied for a business line of credit (43% applied), business loan (32% applied), or an SBA loan (20% applied) than they were an MCA (12% applied) in 2025.

“Large and small bank applicants chose their lender based on their existing relationships, while online lender applicants prioritized speed and their expected chance of being funded,” the Federal Reserve report stated.

The 2025 survey was published in the 2026 report and the 2017 survey was published in the 2017 report.

Lightspeed Capital’s MCA Revenue Grew by 73%

June 5, 2026Capital revenue grew 73% year-over-year, while merchant cash advances outstanding grew a more modest 12% year-over-year, thanks to a payback period that declined to 7 months, a 13% improvement over last year,” said Lightspeed CFO Asha Bakshani during the company’s recently quarterly earnings call.

When Daniel Perlin of RBC Capital Markets asked if that growth might continue to accelerate, Bakshani said they were still being careful and to expect 35%+ growth going forward.

“What we have to keep in mind at the end of the day, Dan, is we want to make sure that our default rates remain in the low single digits,” Bakshani said. “We’ve done a really good job at accelerating ROI on Lightspeed Capital, reducing the months payback with which we get repaid (down to 7), and that’s resulted in very low default rates, the lowest we’ve seen in the industry, to be honest. So what’s important to us is to grow this business prudently and we expect to continue to do that with some nice 35-plus percent growth in fiscal ’27.”

Lightspeed funded about $350M in MCAs from March 31, 2025 – March 31, 2026.

Deep Search, Merchant Lawsuits, and More

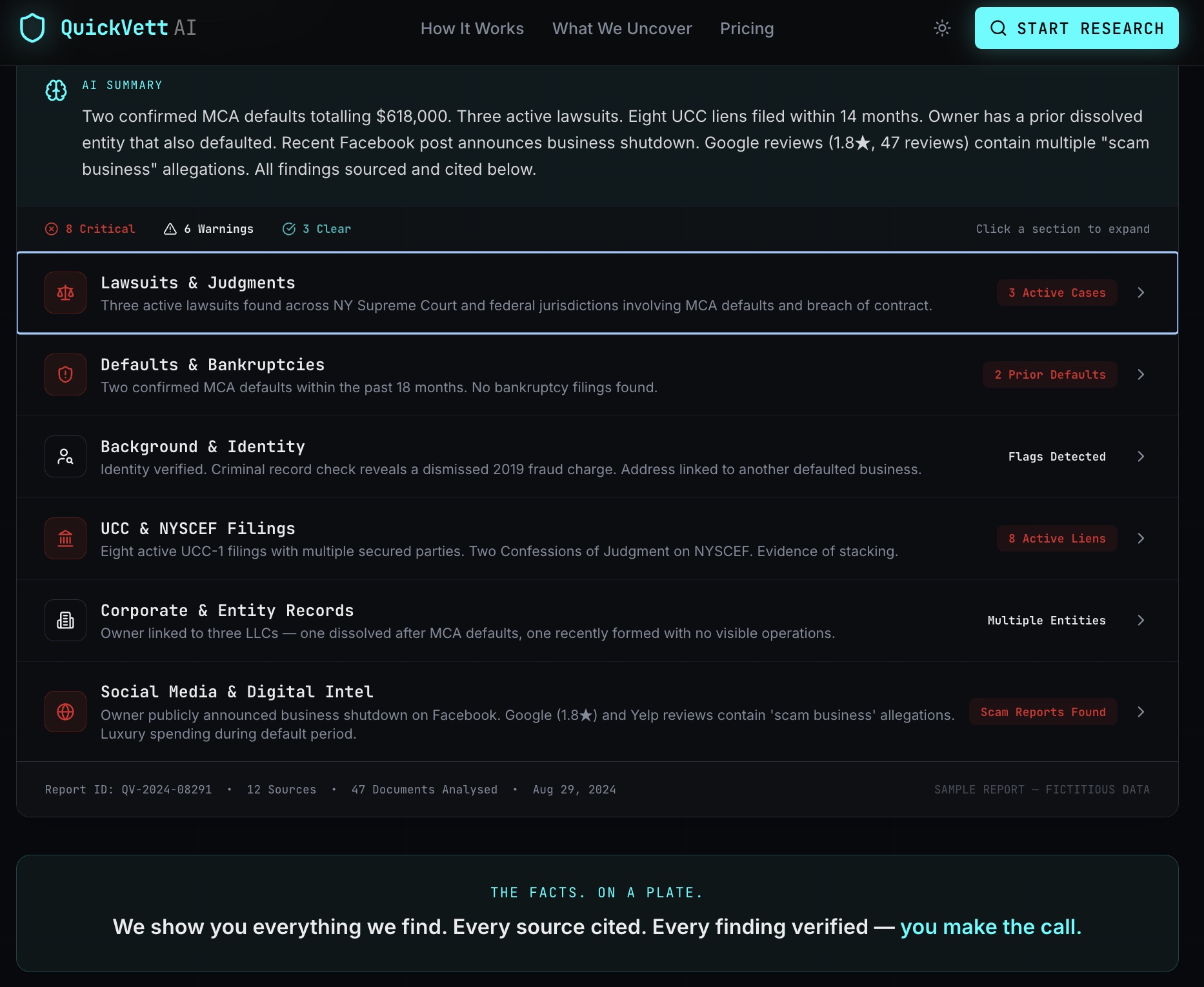

May 19, 2026 The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

QuickVett will spare you the trouble and cut right to the chase. That lawsuit? A dispute over $3k that happened at the tail-end of a large $100k deal. The outcome? A satisfied settlement. It’ll all be right there in its report. No manual lookup on the case required. QuickVett, which describes itself as a merchant intelligence platform, scans state and federal court records across the US. If there’s a hit involving an MCA it will use an MCA-specific AI analysis to present relevant details to an MCA underwriter. An immediate default is distinguishable from one that happened after a long lengthy relationship, for example. Maybe a conflict arising after the 7th renewal provides clarity that otherwise wouldn’t be readily obvious. Most underwriters are already familiar with NYSCEF but if the deal is not in the New York State court system, it’s not going to be found. QuickVett says they’ll find it wherever it is.

QuickVett also does creative searches on its own, such that it will discover if the merchant’s DoorDash account or e-commerce site has gone offline, for example, or if employees of the business recently updated their LinkedIn accounts to say that they no longer work there. QuickVett also pays special attention to the corporate structure and job title of the officers. For example, in an impromptu trial afforded to deBanked for test purposes, QuickVett’s deep search system discovered a sworn affidavit filed by a business owner in an old court case and compared what he said to public records and his LinkedIn profile about his role in the business. The result was that everything matched. But if it hadn’t, an underwriter might have to contend with why a business owner swore he had partners in an obscure court case but listed himself as the 100% owner on a funding application and proceed accordingly.

Overall, “QuickVett scans court records, background databases, corporate filings, social media, and the web — delivering a complete merchant intelligence dossier in under 5 minutes,” the company states. Its AI systems custom tailor the findings to an MCA-style underwriting process.

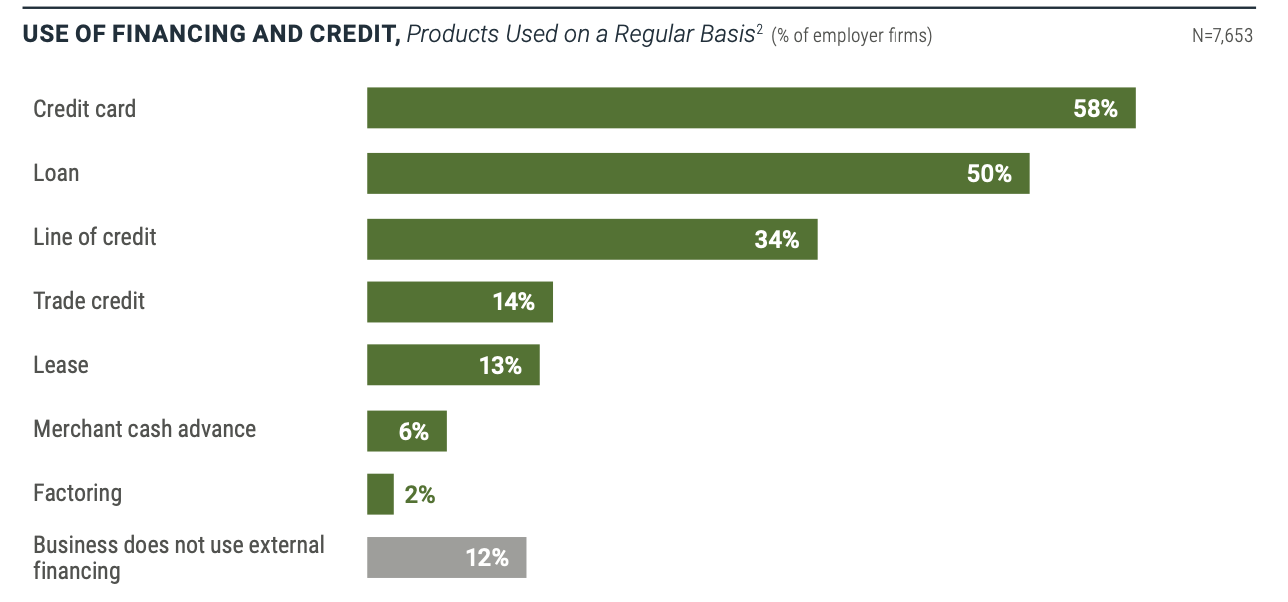

Seven Percent of Small Businesses Use MCAs on a Regular Basis

May 15, 2026According to the latest Small Business Credit Survey taken by the Federal Reserve, 7% of businesses with less than 500 employees use merchant cash advances on a regular basis. This was up from 6% the previous year.

For businesses that applied for financing, 12% applied for an MCA, up from 9% the previous year. Forty-eight percent of those applicants said that they got fully approved for one and 12% said they were declined. This contrasts with last year’s figures of 33% and 9% respectively. These charts are compared below while the full 2026 survey report can be viewed here.

It should be noted that the 2026 data reflects a survey conducted from September 2025 – November 2025 for that trailing 12 month period and the 2025 data reflects a survey conducted September 2024 – November 2024.

New York State Bill Seeks to Criminalize Invoice Factoring, Merchant Cash Advances, and More

May 6, 2026A Senate Bill in New York hopes to rewrite the state’s criminal usury laws to include invoice financing, revenue-based financing, merchant cash advances, retail installment contracts, “or any transaction that in substance functions as the advance of funds in exchange for a future payment or obligation, regardless of the label assigned to such transaction.” S10127, introduced by Senator Rachel May (D), says that the purpose is to ensure “that businesses cannot evade New York’s longstanding usury laws by re-labeling high-cost financing products as services or other non-loan transactions, and to apply existing civil and criminal interest rate protections to covered financing arrangements.”

Any product that falls under these definitions would be deemed criminal if its all-in cost exceeds 25% per annum or the equivalent rate for a longer or shorter period. Depending on the circumstances it would either be considered a Class E felony punishable up to 4 years in prison or a Class C felony punishable up to 15 years in prison.

The bill has merely been introduced and has not yet made its rounds through the legislature. It can be viewed here.