Marketplace Lending

Upcoming Industry Conference Schedule

September 2, 2016It’s not too late to sign up for this year’s remaining industry conferences. deBanked will be at all three of the following events:

Marketplace Lending and Investing Conference

Who should go?: Investors, lenders, platforms, etc.

When is it?: September 27 – 28

Where is it?: New York City

How do I sign up? Register here

Bonus: Use promo code DB to get $250 off the ticket price

Commercial Loan Broker Conference

Who should go?: Business loan brokers, MCA brokers, equipment finance companies, lenders, MCA funders, investors, etc.

When is it?: October 4 – 6

Where is it?: Las Vegas

How do I sign up?: Register here

Lend360

Who should go?: Consumer Lenders, Business loan brokers, MCA brokers, MCA funders, investors, etc.

When is it?: October 5 – 7

Where is it?: Chicago

How do I sign up?: Register here

Bonus: Use promo code deBanked15 for 15% off the registration price

LendIt Europe

Who should go?: Everyone

When is it?: October 10 – 11

Where is it?: London

How do I sign up?: Register here

Bonus: Use promo code deBankedVIP for 15% off the registration price

Money2020

Who should go?: Everyone

When is it?: October 23 – 26

Where is it?: Las Vegas

How do I sign up?: Register here

The Empty Loan Marketplace – Lending Club Zero?

September 2, 2016Update: 9/2/16 – At 1 PM, Lending Club uploaded a batch of 600+ loans on to the platform.

Update: 9/3/16 – The only notes available on the platform today are C-grade notes. No A,B,D,E,F,G…

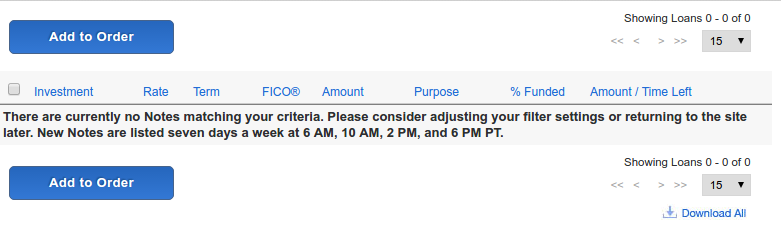

The leader in marketplace lending is showing ZERO available notes in its retail marketplace, according to a screenshot captured of Lending Club this morning. This indicates that Lending Club either hasn’t uploaded its latest batch or that no loans are currently being allocated to retail investors. It doesn’t mean that the company isn’t lending.

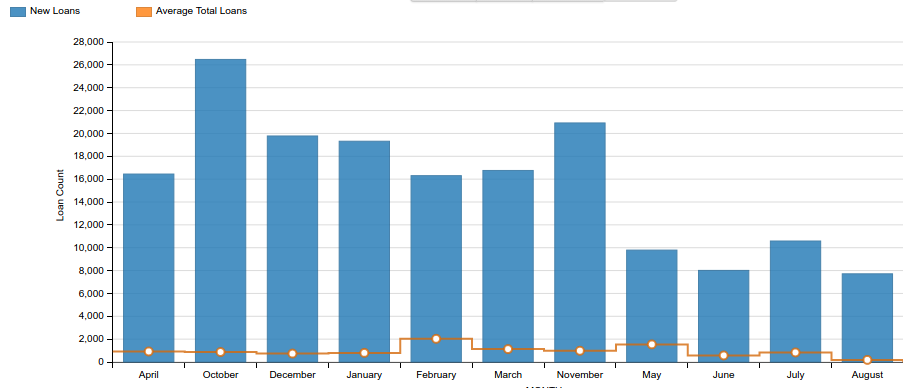

PeerCube, which tracks the amount of new and total loans on the Lending Club platform, also shows zero availability over the span of several hours.

Even if it’s a technical issue, Lending Club’s purported 135,000 self-managed active individual investors will be sure to notice that the marketplace is currently out of stock.

PeerCube also shows that there were 27% fewer loans listed on the retail marketplace in August than in July.

Meanwhile, a thread started on the LendAcademy forum where many Lending Club retail investors hang out, shows users discussing a dearth of new loans going back to July 22nd. Anil Gupta, who runs PeerCube, said in the thread that Lending Club had recently stopped releasing new loans to the retail platform on weekends.

Lending Club has not yet responded to an email sent to them inquiring about the zero note availability, but recently company CEO Scott Sanborn reassured investors that they were committed to the marketplace.

Some of our investors have observed the funding environment and asked: “Are you going to become a balance sheet lender, just like a regular bank? Has Lending Club’s business model changed?”

Let me be very clear: Lending Club is committed to the marketplace model and we do not plan to become a balance sheet or “hybrid” lender. Our mission of connecting borrowers and investors has not changed.

– Scott Sanborn, in an email on 7/28/16

On August 4th, Bloomberg reported that Lending Club was in talks with Western Asset Management Co. to set up a fund that would purchase as much as $1.5 billion of loans over time. Institutions like these may be responsible for the periodic lack of notes made available to the retail market.

Marketplace Lenders Win Over Wall Street Lobbyist

August 25, 2016 The line between marketplace lending and Wall Street just got thinner with the head of a major Wall Street bank trade group switching camps.

The line between marketplace lending and Wall Street just got thinner with the head of a major Wall Street bank trade group switching camps.

Nat Hoopes, VP of public policy and government relations at the Financial Services Forum will head the Marketplace Lending Association.

Formed in April this year, the Marketplace Lending Association was formed by Prosper Loans, Funding Circle and Lending Club to “promote a more transparent, efficient, and customer-friendly financial system by supporting the responsible growth of marketplace lending.”

A requirement to join the association is to be matching 75% of loans, by dollar, with commitments for funding from investors before the loans are issued. The group therefore probably seeks permanent acceptance of the ability for investors to buy loans or securities backed by loans in online marketplaces.

Hoopes has held a couple of stints in Washington as legislative director to Republican senator Scott Brown and as VP of government relations for the ‘Fix The Debt’ campaign. His appointment comes at a time when marketplace lenders have been trying to gain some clout in Washington as regulatory scrutiny tightens.

LendIt’s Peter Renton is Still Earning 8.72%

August 25, 2016

LendIt, speaking to LendIt USA 2016 conference in San Francisco, California, USA on April 11, 2016. (photo by Gabe Palacio)

LendIt Conference founder Peter Renton made more from his marketplace lending investments in the last twelve months than some people earn in a year just from their nine-to-five job. $54,936 to be exact, according to his latest blog post detailing his performance. That’s a result of investments on the Lending Club platform, Prosper, P2Binvestor (which requires you to be an accredited investor), the LendAcademy P2P Fund (which includes Funding Circle, Upstart, Lending Club and Prosper), and the Direct Lending Income Fund managed by Brendan Ross (which invests with lenders such as Quarterspot and IOU Financial).

Unsurprisingly, his business loan performance through the Direct Lending Income Fund has earned the highest yield, a TTM return of 12.77%.

While reporters and critics seem to be planning the funeral for several lending platforms, Renton remains steadfast in his optimism. “Eventually, I plan to have a diversified seven-figure portfolio made up of consumer, small business and real estate loans,” he wrote on his Lend Academy website.

Though Renton is reaping the benefits of being a platform investor, it’s the platforms themselves that may be in trouble, according to a recent op-ed by Todd Baker, a senior fellow at the Mossavar-Rahmani Center for Business and Government at Harvard University’s John F. Kennedy School of Government. On American Banker, Baker wrote, “Almost all [Marketplace Lending] revenue is generated from ‘gain on sale’ fees earned from new loan sales. This dependence on origination volume and gain-on-sale margins makes MPL results exquisitely sensitive to macro and micro trends in investor demand and risk appetite.”

And if a platform isn’t sustainable, the theory is that future investment opportunities may not be as available as they have been historically.

“MPLs need to shift to a more sustainable mode — either as banks or as nonbank balance-sheet lenders — before the end of the current credit cycle brings on a real shakeout and the MPL experiment becomes a financial failure,” Baker wrote.

Renton himself acknowledged a downward trend in his yield, conceding that it may never return to previous levels. “While I would love to be earning more than 10% again I don’t expect to get back there any time soon,” Renton wrote.

He also recently rebutted a Bloomberg article that argued Lending Club was being shady with repeat borrowers.

Hillary Clinton Wants to Harness the Potential of “Online Lending Platforms”

August 24, 2016 Presidential candidate Hillary Clinton acknowledged online lending on Tuesday when she published her plan to help small businesses. “Small businesses owners cite insufficient access to capital as a primary inhibitor to starting, growing, and sustaining a small business,” she asserted in a fact sheet posted to her website.

Presidential candidate Hillary Clinton acknowledged online lending on Tuesday when she published her plan to help small businesses. “Small businesses owners cite insufficient access to capital as a primary inhibitor to starting, growing, and sustaining a small business,” she asserted in a fact sheet posted to her website.

To solve that dilemma, she wants to:

- Harness the potential of online lending platforms and work to safeguard against unfair and deceptive lending practices.

- Streamline regulation and cut red tape for community banks and credit unions while defending the new rules on Wall Street.

- Give the SBA administrator the authority to continue providing 7(a) loan guarantees to small businesses if demand is higher than the yearly cap, helping even more small businesses get affordable bank loans.

- Etc.

The WSJ and other media outlets have claimed Clinton’s reference to online lending means “marketplace lending” but that appears to be an exaggeration. The two are not synonymous. One company for example that just secured a $100 million credit facility from Goldman Sachs to make more loans online is not a marketplace, but rather a balance sheet lender that helps banks make loans to their clients.

Hillary Clinton’s plan for small business growth is focused on community banks, the SBA and tax incentives. Fintech and marketplaces were not mentioned. You can read it here.

Avant Loses 30% of its Staff, Including CEO’s Wife; Here’s Why You Don’t Have to Worry

August 17, 2016Avant lost 30 percent of its staff to the voluntary severance program it offered its employees last month , and CEO Al Goldstein’s wife and chief compliance officer, Anna Fridman is said to retire at the end of the quarter.

The Chicago-based subprime lender has had a spate of troubles recently, jeopardizing investor confidence in the company. The 30 percent staff cut was originally going to be 40 percent and the company had planned to cut two thirds of their loan volume. They also pulled back on their auto refinancing plans.

But things are getting better..or are not as bad as they sound. Avant has been making progress on some fronts — it closed a $255 million asset-backed securitization led by JP Morgan and Credit Suisse as well as renewed a $392 million warehouse facility with the banks and plans to start charging fees on its loans to keep its investors from going astray.

Avant’s model, as The Wall Street Journal noted was built on selling loans at a premium to the investors and not charging fees to the borrower. And as investors retreated, Avant decided to pivot too. The lender said it plans to charge an “administration fee,” competitively priced at 1.75 percent to 3.75 percent of the loan amount. The company hopes to keep its investors roped in by making loans cheaper for them.

Will it work? There’s only one way to find out.

loanDepot Raises $150 million, Plans to Hold More Loans on Balance Sheet

August 17, 2016California-based marketplace lender loandepot secured $150 million in term-debt financing to make investments in technology and product and hold loans on balance sheet.

For Q2, the company funded $10 billion in personal loans, home loans and home equity loans. Total funding for the first half of 2016 was up 16 percent compared to last year, the company claimed.

loanDepot was launched in 2010, by entrepreneur Anthony Hseih who has led companies like LendingTree, Homeloancenter.com and pioneered online consumer lending with Loansdirect, acquired by E*Trade Finance in 2001. Despite strong growth (Originating more than $50 billion worth of loans since 2010), the company postponed its November 2015 IPO because of “adverse market conditions.” For reference: Square went public six days later on November 19.

In March of this year, the company partnered with subprime lender Avant for a mutual borrower program.

Prosper Marketplace Bitten in Q2 With Major Loss

August 17, 2016Prosper Marketplace Inc. reported a Q2 2016 loss of $35.5 million, down from a loss of only $6 million over the same period last year. While not publicly traded, the company is still required to file its results. Originations for the quarter totaled $445 million.

For comparison purposes, rival Lending Club posted an $81 million loss on $1.96 billion in originations.

Prosper incurred $14 million in expenses just from restructuring related to their downsizing and layoffs which includes the closing of their Salt Lake City office and the termination of 167 employees.

The company also used a lot of cash, finishing Q2 with only $29 million in the bank, down from $66 million at the beginning of the year. Lending Club by comparison had $573 million in the bank at the end of Q2.

According to their 10Q, “Prosper Funding saw reduced listings on the marketplace as Prosper slowed down marketing efforts to reduce demand from Borrowers and maintain marketplace equilibrium. As a result, Prosper Funding experienced a decline in administration fee revenue-related party during this period and expects a decrease in administration fee revenue-related party in the third quarter of 2016 from the third quarter of 2015.”

Meanwhile, the performance of their actual loans has remained steady. View their latest performance update HERE.