Marketplace Lending

CommonBond Securitizes Refinanced Student Loans Worth $168 Million

October 20, 2016Online lender for student loans, CommonBond closed a $168 million securitization, backed by $178 million in collateral with an ‘A1’ rating from Moody’s and ‘AA’ from DBRS.

This is the company’s second deal this year, after a $150 million transaction, earlier in April.

Founded by Wharton graduates David Klein, Michael Taormina, and Jessup Shean in 2012, CommonBond set out to address the need for affordable graduate student loan options. So far, the company has crossed $500 million in funded loans and provides MBA loans, personal loans and refinances student loans . The New York-based lender uses data and technology to underwrite its loans, holding half on its balance sheet and selling the other half though a marketplace. In July this year, it also raised $30 million in equity, $300 million in debt and acquired a personal finance startup, Gradible.

“CommonBond has built a sterling reputation in the capital markets due to our meticulous, data-driven underwriting,” said Morgan Edwards, Chief Financial Officer of CommonBond. “We continue to be excited to see new investors participate with each transaction we bring to the market and expect to see the diversity of investors increase with subsequent deals,” he said in a statement.

CommonBond competes with the likes of SoFi, which recently securitized bonds worth $427 million, its third deal this year. And like SoFi, which started off with student loans before moving to personal loans and mortgages, CommonBond also wants a larger share of the pie. “Our long term vision is to provide our customers with their evolving needs and we are well positioned to provide other products and services over time,” CEO David Klein told deBanked earlier.

Barclays and Goldman Sachs served as joint-lead managers and bookrunners on the transaction.

Where a Non-Bank Falls, a Bank May Rise

October 19, 2016 Last week, CircleBack Lending disclosed that they were no longer originating loans, making them one of the first major casualties in the alternative lending industry. While even optimists projected that some platforms would eventually fail, the fact that this one coincided with Goldman Sachs’ announced kickoff into consumer lending, made their demise feel all too fatalistic.

Last week, CircleBack Lending disclosed that they were no longer originating loans, making them one of the first major casualties in the alternative lending industry. While even optimists projected that some platforms would eventually fail, the fact that this one coincided with Goldman Sachs’ announced kickoff into consumer lending, made their demise feel all too fatalistic.

Lending Club too, the symbolic leader of the online lending movement, announced some setbacks last week with their riskiest borrowers, which caused their stock price to plummet. In the background, banks such as Discover appear to be patiently waiting to swoop in on them should they stumble.

Even the recent announcement by JPMorgan Chase to double their commitment to Small Business Forward, a program meant to help small businesses access capital, suddenly feels a bit more threatening. Especially so given the bank’s partnership with OnDeck, an alternative business lender.

Goldman Sachs’ lending platform Marcus is offering borrowers no origination fees, no late fees, and no fees of any kind outside of interest charges. Discover is offering no origination fees and even no interest charges if the loan is repaid within 30 days.

On October 18th, the superintendent of New York’s banking regulator encouraged attendees of the New York Bankers Association conference to start their own online lending operations to compete with all the fintech startups.

If banks can match the speed and experience provided by alternative lenders, we just may see more platforms fall and banks rise in 2017.

For Lending Club, Ain’t Nothing But a E,F and G Thang

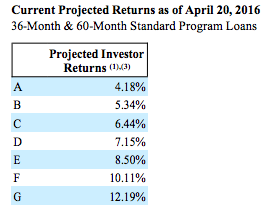

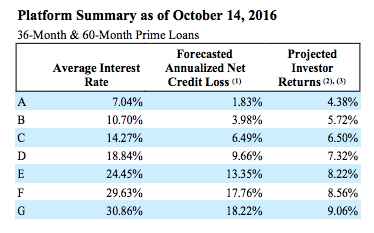

October 15, 2016Investing in a G-grade Lending Club note is projected to earn 313 basis points less than what was projected six months ago. The company published new projected investor returns in their 8-K filed on Friday that showed an expected return of 9.06% on G-grade notes. That’s down from the 12.19% figure they published in an April filing. F-grade note projections decreased by 155 basis points. For Es, it’s down 28 basis points.

“Rate increases are concentrated in Grades F and G with marginal changes in other grades,” the company announced on Friday while reporting a weighted average 26 basis point interest rate increase. But will rate increases save the Fs and Gs from plummeting returns?

As G is the most risky grade, that means the most risky borrowers on Lending Club are projected to earn investors only 9.06%. Is all that risk worth it? Or perhaps more importantly, is that projection even realistic? Six months ago, the riskiest class was projected to earn 12.19%. Nothing has really changed from a macroeconomic standpoint since then, so it’s difficult to even pinpoint why investors should expect a 25% lower return on the riskiest borrowers all of the sudden or why they should be confident that it won’t get worse.

On the plus side, projected returns on As through Ds are up.

CircleBack Lending is No Longer Lending

October 14, 2016CircleBack Lending is no longer originating loans, Bloomberg reports. A Lending Club competitor, the company was an online lending darling, having secured a $500 million deal with Jefferies just two years ago. At that time, company CEO Michael Solomon said in an announcement, “we are taking a rigorous approach to credit underwriting and want to make sure we know our customers before issuing any loans.”

Along the way something must have gone wrong. According to Bloomberg, Solomon recently said that if the lender can’t raise money, it will transfer existing loans to another company to handle collections and payment.

Lending Club Increases Interest Rates

October 14, 2016Delinquencies are up among borrowers with “high indebtedness,” Lending Club said in a document filed with the SEC on Friday. As a result, they’re increasing interest rates by an average of 26 basis points with the bulk concentrated on F and G grade loans.

The announcement comes on the heels of a previous raise made six months ago and another made approximately six months before that. It is not uncommon for the company to make adjustments as trends change.

“Consumers appear to be taking on more debt overall due to low prevailing interest rates,” Lending Club states in their report, citing a Federal Reserve study that observed an increasing amount of indebtedness across student loans, mortgages, credit cards, auto loans, and other forms of credit as of the second quarter 2016.

They’re also tightening up their criteria in such a way that “approximately 1% of borrowers who previously would have been able to obtain a loan under prior underwriting criteria will no longer be approved.”

Who’s Stealing Lending Club’s Borrowers?

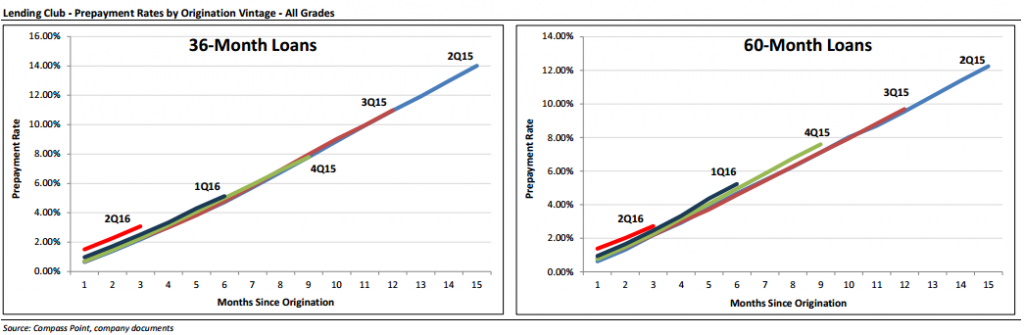

October 11, 2016 A shocking amount of borrowers pay off their Lending Club loans early, the data shows, but the trend has accelerated recently. What’s happening out there?

A shocking amount of borrowers pay off their Lending Club loans early, the data shows, but the trend has accelerated recently. What’s happening out there?

3.07% of people that took a 36-month loan from Lending Club in the 2nd quarter of this year had already paid them off in full just two months later, according to a report published by Compass Point. That’s double the pace that Lending Club experienced three years ago. Meanwhile, 1.51% of Q2 borrowers paid off their 36-month loan in less than 1 month!

And the trend continues as the loans age. Depending on which Lending Club vintage you examine, more than 25% of borrowers are paying off their loans prior to maturity. Several Lending Club users that I’ve connected with suspect that these borrowers are simply paying off these loans using the proceeds of another loan. Discover is a prime suspect, what with their no origination fees and marketing campaigns directed directly at Lending Club. It might also be Prosper or even Lending Club giving the borrower a second loan to pay off their first. There’s no way to know for sure but the trend is notable for two reasons.

Retail Investors Get Sacked

Retail Investors Get Sacked

1. Retail investors on the platform are actually penalized when loans are paid off in full after the 12th month but prior to maturity. Lending Club assesses a 1% fee to the investor purely on the outstanding principal when this happens, so the investor is not only deprived of their future interest but also unfairly hit with a penalty charge over which they have no control. And it’s material because two to three times as many borrowers are paying off their loans early after the first 12 months as they are before it. That’s a lot of penalties for investors to get stuck with especially since their returned cash will no longer generate a return until they’re able to reinvest it into a loan of equal quality. That used to mean a cash drag of a few days, but shifts in the industry have created instances in which there might be no new loans available to replace the previous ones.

FICO Arbitrage?

2. Even the lowest quality borrowers, Grade G, seem to have no trouble paying off their loans early, according to Compass Point’s report. One might wonder how they’re obtaining credit outside of Lending Club so easily. One theory put forth by some retail investors on the Lend Academy forum is FICO arbitrage. Basically, when a borrower consolidates their credit card debt using a Lending Club loan, they are reducing their revolving credit usage and increasing their installment credit. FICO’s algorithm might not correctly interpret this as a 1:1 transfer of debt and instead give the borrower’s score a boost. The new artificially improved score could signal to rival lenders that the borrower is deserving of an even lower interest rate. It’s common knowledge that a creditor could request from a credit bureau the names and addresses of consumers above a certain score and then offer credit to those consumers. And that might be why many borrowers seem to only be using Lending Club as a pit stop on their refinancing journey.

Of course if borrowers are using a second Lending Club loan to pay off their first loan, then the above two scenarios have far more serious implications, but as of now all that is known is that the pace of early payoffs is accelerating. Compass Point’s report states, “while still early, we believe the shift in trend is worth monitoring as it could impact retail and institutional investor returns from Lending Club loans.”

RIP The Retail Investor in Marketplace Lending?

September 30, 2016 Now that credible sources are finally conceding that the pure marketplace lending model is dead, Prosper announced in an email on Thursday that they are shutting down their secondary market for retail investors.

Now that credible sources are finally conceding that the pure marketplace lending model is dead, Prosper announced in an email on Thursday that they are shutting down their secondary market for retail investors.

“We are writing to let you know that as of October 27, 2016, Prosper will no longer offer the Folio Investing Note Trader platform, the secondary market for Prosper Notes. Prosper has found over time that very few investors are using the secondary market and, as such, has made the decision to no longer offer this service. We apologize for any inconvenience that this causes. Prosper remains committed to its retail investor clients and to providing them a great experience.”

An official statement sent by Prosper CEO Aaron Vermut to LendAcademy’s Peter Renton said that the move in no way changes their commitment to the retail investor. But some vocal retail investors did not appear convinced, according to a forum thread on the subject. The few reddit comments posted about this announcement also showed concern.

In July, I joked that marketplace lending would become Goldman Sachs lending, a marketplace for Wall Street by Wall Street. Coincidentally, representatives from Goldman Sachs actually spoke during two presentations at the Marketplace Lending and Investing conference that took place earlier this week in NYC. During one, Goldman Sachs Bank USA CEO Stephen Scherr, laid out the company’s plan to compete against marketplace lenders by relying on their own balance sheet, something they see as an advantage.

In the meantime, Prosper’s elimination of its secondary market means that retail note buyers will need to hold the notes to maturity, making them totally illiquid. While investors may not have been using the market very much historically, permanently dismantling the escape hatch isn’t likely to inspire confidence.

Coincidentally, Lending Club sent out their own email hours after Prosper’s, assuring retail investors that they were committed to providing them with a great investment experience. “We’re proud that we have the largest retail investor base of any company in the marketplace lending industry and are committed to expanding our offering so more retail investors can access Lending Club products,” wrote Patrick Dunne, Lending Club’s Chief Capital Officer. “We have ambitious long term goals. We aspire to allow every type of investor – individual retail and institutional investors – to participate in what we believe is a compelling product that can offer solid risk-adjusted returns.”

it remains to be seen what exactly will happen next for these companies and the industry.

Marketplace Lending: Where No One Makes Any Money?

September 28, 2016 At the Marketplace Lending and Investing conference in NYC, LendAcademy founder and p2p lending expert Peter Renton asked a group of panelists a stunning question, “Why is no one making any money?”

At the Marketplace Lending and Investing conference in NYC, LendAcademy founder and p2p lending expert Peter Renton asked a group of panelists a stunning question, “Why is no one making any money?”

For the sake of context, Renton explained that if banks were basically the most profitable business type on Earth, then how could it be that those companies infringing on their space or partnering up with them weren’t partaking in that.

The question was posed to Noah Breslow of OnDeck and Sam Hodges of Funding Circle, two of the most high profile players in the alternative small business lending industry. Both companies have been operating at a loss despite being in business for quite some time, in the case of OnDeck, almost ten years now.

Breslow took the question in stride, saying that “first you have to look at the unit economics of a loan. If you’re not profitable there, you’re in trouble. You can’t scale your way out of that.” He added that there are indeed competitors that fail on this test alone who won’t likely be around for much longer.

But as to why they personally were still not profitable? He put a lot of emphasis on their continued strategy to expand.

Funding Circle’s Hodges offered a similar explanation, saying that they have spent a lot of resources on expanding into five countries. He also said that “their plan takes them to profitability next year.”

Of course, neither OnDeck nor Funding Circle are as diversified in their product offerings as banks, explaining perhaps why the analogy between bank profitability and their profitability isn’t apples to apples. LoanDepot CEO Anthony Hsieh touched upon this in his presentation earlier in the day when he said that his company acquires an astounding 600,000 leads per month, a record high, but with very low conversions. So many [lenders] are monoline, he said.

Surely that affects the bottom line.