Loans

NYC Taxi Workers Block Brooklyn Bridge, Demand Debt Forgiveness

February 11, 2021 Taxi drivers demanding Medallion debt forgiveness briefly blocked the Brooklyn Bridge Wednesday. The protest, organized by the 21,000-member strong New York Taxi Workers Alliance union (NYTWA), was a release of fury over the astronomical debt they have faced during a global pandemic that has cut ridership by 80%.

Taxi drivers demanding Medallion debt forgiveness briefly blocked the Brooklyn Bridge Wednesday. The protest, organized by the 21,000-member strong New York Taxi Workers Alliance union (NYTWA), was a release of fury over the astronomical debt they have faced during a global pandemic that has cut ridership by 80%.

“Debt forgiveness now,” chanted Union Founder Bhairavi Desai through a megaphone, leading the drivers in a chant. That’s a lot of debt: To get a city-licensed taxi medallion, drivers had to pay inflated prices, up to $1.3M in 2014, before the advent of rideshare apps crashed prices to a fraction of what they were worth.

We shut down the Brooklyn Bridge because only direct action will get us what we need: medallion debt forgiveness now! pic.twitter.com/kmbQlBrOO3

— NY Taxi Workers (@NYTWA) February 10, 2021

In 2021, thousands of taxi drivers are paying up to $600,000 in debt on medallions that are only worth $120-$150k. Last year, Desai testified before the State House Financial Services Committee that Confessions of Judgment were used extensively to take hundreds of thousands in debt from the pockets of taxi drivers.

The day of action started with a gathering of union members at the mayor’s office at 9 am before senior members (62 yo+) testified that the medallion crash stole retirement savings at a City Council Committee on Immigration.

Dozens of taxis then formed a motorcade, blocking the bridge before gathering at the Park Slope home of Senator Chuck Schumer, Democratic Majority leader of the Senate, who NYTWA said is leading negotiations over the stimulus bill.

Protestors could be seen across from the north entrance to Prospect Park to encourage Schumer’s support to push bill H.R. 5617 through Congress. The Taxi Medallion Loan Forgiveness Debt Relief Act will eliminate the need to pay taxes on outstanding medallion debt, the NYTWA website states.

The union also calls for the leveling of taxi medallion debt to $250k per medallion. NYTWA holds that the city helped inflate medallion prices and should assume the leftover debt. The New York Times and Post reported a bailout of that size could top $500M.

“Till pandemic do us part” Divorce on rise, Weddings Furloughed

December 22, 2020 For couples who live together, forced “quality time” due to a pandemic has been considered an exciting change in the household’s dynamic, to say the least.

For couples who live together, forced “quality time” due to a pandemic has been considered an exciting change in the household’s dynamic, to say the least.

Trouble in paradise? Possibly, as one firm found, the amount of people inquiring about divorce loans has risen 62% in 2020, compared to last year.

If you didn’t know divorce loans were an option in the first place, Loanry, an online loan lead generator, said divorces could cost upwards of $12,000 in states like Delaware and New York, and in California up to $14,236.

Loanry looked through their loan transactions and found that not only were divorce loans higher by 68% in New York and 71% in Florida, but the wedding loan business was in trouble.

2020 has been a record year for marriages ending – and hundreds of thousands of couples being unable to hold a wedding in the first place.

According to Statista, over 2 million weddings occur every year in the US, at an average cost of $30,000. Wedding site The Knot found 93% of planned marriages were rescheduled. Loanry found 11% of planned weddings took out loans.

For those of you at home (most of you), couples are paying back $3.7 billion without even saying, “I do.”

Answering the question no one asked: what is the worst way to start a lifelong journey together?

Loanry has sets of advice to deal with the costs of both weddings and divorces, but the simplest seems to be “don’t do either.”

“Financing a wedding using a loan should be taken very seriously, and we don’t recommend it,” Ethan Taub, founder of Loanry.com, said. “Finding ways to cut costs on your wedding expenses is a far more effective alternative to avoid unnecessary debt yet still enjoy your big day.”

He went on to comment that while divorce in this stressful year is sad, make sure to research the best, most affordable option.

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

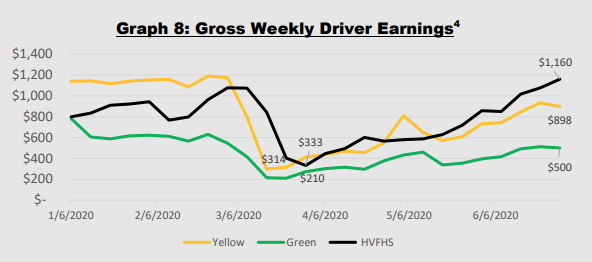

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.

What is ‘Lending as a Service?’

September 3, 2020I‘ve heard of SaaS, but now there’s LaaS, Lending as a Service. I recently spoke with Timothy Li, CEO of Alchemy, a fintech infrastructure company that offers that and more. You can check it out below!

Checkout in the time of COVID

August 10, 2020 Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

For these reasons, POS lending is one of the fastest growing segments in unsecured credit, with volume increasing at 40 percent year-over-year. COVID has further accelerated the demand for credit options at checkout.

According to McKinsey, annual growth is expected to jump to 150 percent thanks to an explosion in online shopping and government subsidy programs boosting retail sales. In Canada, firms such as Uplift, Paays, and PayBright are all seeing merchant demand skyrocket for their services, with the latter onboarding over 250 merchants per month.

K-Ching!

POS lenders are able to subsidize APRs by charging the merchant a fee of 4-6 percent of the purchase price. This is on average 2 percent more than the fees charged by credit cards companies. Despite the larger fee, BNPL is very attractive for retailers for a number of reasons. By providing point of sale financing retailers see:

- 30% increase in basket size

- 25% reduction in cart abandonment

- 20% increase in repeat traffic

With installment payments as an alternative, credit cards have seen a decrease in popularity among young shoppers, particularly on smaller ticket items under $500. There are a number of reasons why:

1. Clunky signup experience. Signing up for a credit card at checkout requires lots of paper, personal information, signatures and significant patience – antithetical to the one-tap checkout shoppers are accustomed to. Alternatively, BNPL approval is instant at checkout. 75% of merchants even advertise POS financing far before the register, at the beginning of the customer journey which can increase conversion by two to three times.

2. Challenge to qualify. 19 percent of consumers ages 22 to 30 lacked the credit history to be approved for credit cards in the first place. Many BNPL products do not perform credit checks, and those that do use alternative data sources to underwrite thin-file borrowers.

3. High APRs. With their parent’s household debt in their rear view mirror, many younger shoppers have an aversion to carrying revolving credit balances. Millennials on average carry two fewer cards than their parents. Psychologically, $1000 on your credit card looks scarier than four installments of $250 over time.

4. Customer confusion. Inactivity fees, late fees, over-the-limit fees, cash advance fees, are all poorly understood and masked within dense monthly statements. BNPL offers an elegant digital first experience and straightforward reporting.

The Supporting Cast

Today POS lenders are competing in a land grab for merchant partnership. But for FIs and fintechs who have yet to plant their flags, there are still ways of participating in the BNPL boom.

- Banks. Banks have largely participated indirectly in the BNPL sector, by providing portfolio financing to fintechs or by offering installment options for larger ticket items within their existing credit card programs. Wayne Pommen, CEO of PayBright, sees more bank and fintech collaboration in the next few years: “I predict more buying and partnering, Banks are too far behind to build this themselves.” Marcus Pay, the recently launched retail banking arm of Goldman Sachs is the only group to directly compete in the POS financing ring, with JetBlue as their launch partner.

- Platforms. E-commerce enablers that power millions of independent merchants are piling in to embed POS financing within their platforms. Marketplaces Ebay and Etsy have partnered with Afterpay and Klarna, while the digital infrastructure whale Shopify has an agreement with Affirm.

- Cards. Traditional credit card companies who have the most to lose from BNPL are getting ahead of the trend in several ways. Visa took a controlling stake in Klarna in 2007. More recently they launched Visa Installments, a developer tool for issuers in the Visa network to pilot branded installment products. Though Visa Installments stretches the definition of BNPL, David Fry, CEO of travel financing startup Paays does not mind the ambiguity. “I am not religious about the distinction between cards and installments. What we care about is what the customer is looking for, and what they have to pay to get access to that product”.

POS Lending has the potential to transform consumer lending as it’s evolution is inextricably tied to the growth of e-commerce. It is all about understanding the needs of the shopper and their digital journey. POS lenders are making it increasingly easy for merchants to streamline the buyer path to purchase.

The State of Securitizations in Alternative Lending

July 6, 2020Over the last few months, “securitizations” were frequently cited as a reference point for the health of a small business lender or alternative finance provider. Given the vague information and inferences that circulated, I decided to schedule a chat with Methodical Management co-founder Gunes Kulaligil to get his perspective. Our discussion on the state of securitizations in alternative lending below:

Forgiven Debts: The Hidden Tax Time Bomb That Could Kick Small Businesses While They’re Down

May 12, 2020 Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

At face value, it would appear that taxpayers who have non-PPP debt canceled, forgiven or discharged during the COVID-19 crisis and do not meet any of the specific exclusions mentioned in the report, would be subject to tax on the cancelled debt as income.

This tax treatment, which pre-existed COVID-19, could be devastating in this era where the prevalence of debt forgiveness is likely to reach unprecedented levels.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

One must also consider that a lender may just cancel some or all of a portion of a debt without any direct action of the debtor, with the end result being the same, a potential tax bill to the business on the cancelled portion.

It’s important to understand the various exclusions to the IRS guidelines that govern cancelled debt. The full report can be ACCESSED HERE.

The Story Behind The #BrokersAreBetter Super Bowl Commercial

February 7, 2020 Watching the Super Bowl, you may have seen a number of oddities: the resurrection of a peanut as an infant, the tattooed inside of a popular rapper’s head, Google’s plea to be the hub for all your elderly relatives’ memories, and, on top of it all, a cheeky spar between mortgage lenders.

Watching the Super Bowl, you may have seen a number of oddities: the resurrection of a peanut as an infant, the tattooed inside of a popular rapper’s head, Google’s plea to be the hub for all your elderly relatives’ memories, and, on top of it all, a cheeky spar between mortgage lenders.

Quicken Loans, the Detroit-based mortgage provider, had an ad that featured Hawaiian actor Jason Momoa reveal his ‘true’ self, all while explaining the values of Quicken’s Rocket Mortgage product. Par for the course with Super Bowl ads, until United Wholesale Mortgage’s advert aired. Throwing shade at it its competitor with the line: “Playing with rockets is great when you’re a kid, but when it’s time to get a mortgage, you quickly realize a rocket is complicated and expensive,” United promoted its FindAMortgageBroker.com website, which points potential customers towards a host of brokers local to themselves, before closing its ad with the #brokersarebetter hashtag.

Speaking to The Detroit News about the joke, United CEO Mat Ishbia said: “I don’t think we attacked (Rocket Mortgage); we had fun with it … I think it’s going to grow their business just like it’s going to grow ours. I think (Quicken founder) Dan Gilbert and (CEO) Jay Farmer are going to laugh when they see it. They won’t like it enough to chip in with the cost. The reality is we’re friendly competitors.”

Being a wholesale lender, United gains customers exclusively from its brokers, where as Quicken engages with both brokers and its own marketing efforts. In a call with deBanked, United’s Chief Marketing Officer, Sarah DeCiantis, explained that this was one of the main motivators behind the ad. Noting that for local, independent brokers it can be a struggle to compete with behemoth retail lenders, DeCiantis said that the ad was an answer to the question of ‘How do we allow them to get out there?’ “Retail are amazing at marketing and customer retention, so we try to do what we can to put [independent brokers] on the same playing field because they don’t have the same budget.”

And with only 30 seconds to express this, the challenge was on — not to mention how such ads are estimated to cost $5.6 million. “So much thought goes into every frame, every second,” remarked DeCiantis, who said she was proud of the final product. “We’ve gotten over 75,000 searches on the website just in the first few days after the ad.”

The high profile decision to purchase Super Bowl air time comes during what looks like will be a big year for United, with it planning to add an additional 3,000 employees to its already 5,000-strong staff in its Pontiac headquarters. Despite this, according to Ishbia the focus is still on the local: “If a consumer goes through an independent mortgage broker it will be faster, easier and more affordable than going through a retail lender or mega bank.” From his point of view, it just makes more sense to go independent, it isn’t rocket science.