Legal Briefs

Merchant Cash Advances Are Not “Masked” Usury or Loans

May 17, 2018 A New York Supreme Court judge cited the decision rendered in Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC on Wednesday, when she dismissed usury claims brought against four merchant cash advance companies.

A New York Supreme Court judge cited the decision rendered in Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC on Wednesday, when she dismissed usury claims brought against four merchant cash advance companies.

The case at issue was Wilkinson Floor covering, Inc., Stephen Wilkinson v Cap Call, LLC, TVT Capital, LLC, Yellowstone Capital, LLC, Ace Funding Source, LLC (Index #160256/2016)

Champion set forth the general principle that the underlying agreement in that case was not a usurious transaction, she opined. Beside the plaintiff’s claim being procedurally deficient, the judge said that the plaintiffs had not established usury because a rudimentary element of usury is the existence of a loan or forbearance of money and when there is neither, there can be no usury.

Per the Honorable Carmen Victoria St. George:

In New York, there is a predisposition in this State against declaring that contracts are usurious. This is especially true with respect to commercial agreements, where “usurious agreement[s] will not be presumed from facts equally consistent with a lawful purpose.”

Additionally, because plaintiffs’ obligation to pay them future receivables is conditioned on plaintiffs’ receipt of such, the agreements at issue are not loans.

Judge Grants Restraining Order Against Deceptive Funding Company

May 6, 2018 JTT Funding, the company previously accused of having forged a Confession of Judgment, stands accused now of stealing the identity of a rival funding company. On May 3rd, New York Supreme Court Judge W. Franc Perry granted an injunction against JTT Funding from using the name, logo and likeness of Accel Capital from its marketing and contract materials.

JTT Funding, the company previously accused of having forged a Confession of Judgment, stands accused now of stealing the identity of a rival funding company. On May 3rd, New York Supreme Court Judge W. Franc Perry granted an injunction against JTT Funding from using the name, logo and likeness of Accel Capital from its marketing and contract materials.

Similar to the forged COJ suit (which was brought by FundKite), JTT Funding did not answer or contest the claims.

Plaintiff Accel Capital demonstrated in their papers that an agent of JTT was using a gmail address with “accelcapital” in the name and the company’s logo in its contracts. When a merchant funded by JTT Funding (who pretended to be Accel) inadvertently contacted the real Accel Capital, the scheme was revealed.

JTT Funding went on to ignore Accel’s Cease and Desist letter, court papers say, which led to the lawsuit and demand for an immediate injunction.

According to the Financial Times, JTT Funding is owned by Queens-born mixed martial arts fighter Jim “The Tyrant” Boudourakis. In his October 2017 interview with the publication, Boudourakis said, “There was a learning curve, going from being a fighter to a salesman. But I’m good with people.” FT also reported that his company had 18 full-time salespeople and was funding $4 – $5 million per month.

In the FundKite suit, it is alleged that Boudourakis’ first name Jim is an alias.

The Accel Capital suit can be found in the New York Supreme Court under Index Number: 153447/2018

Despite Movement of Negative Bill for MCA and Factoring Industries, Hope for a Solution

April 23, 2018 Last week, California State politicians gathered for a hearing on SB 1235, a bill that would require the disclosure of an Annual Percentage Rate (APR) for all loans and non-loans, including MCA and factoring products. This is very problematic because APR (which includes interest rate) cannot be calculated for most MCA and factoring products for one reason: time. What makes merchant cash advance and factoring unique is that the timing of payments is flexible, and therefore unknown.

Last week, California State politicians gathered for a hearing on SB 1235, a bill that would require the disclosure of an Annual Percentage Rate (APR) for all loans and non-loans, including MCA and factoring products. This is very problematic because APR (which includes interest rate) cannot be calculated for most MCA and factoring products for one reason: time. What makes merchant cash advance and factoring unique is that the timing of payments is flexible, and therefore unknown.

“It’s impossible to compute,” said veteran factoring lawyer Bob Zadek about calculating APR for most MCA and factoring products. “Interest = principal x rate x time. Since [they] cannot determine how long the advance will be outstanding – since repayment is a function of the borrower’s cash flow – the algebra doesn’t work.”

The bill, introduced by California State Senator Steve Glazer, moved out of the Senate committee on Banking and Financial Institutions and is headed to the Judiciary committee – closer to potential passage. Yet advocates of the MCA industry, one of whom testified in the assembly room in Sacramento, are hopeful.

“There were a number of state senators who clearly understood the problems with applying an APR to a commercial transaction and to a purchase and sale of receivables transaction,” said Katherine Fisher, a partner at Hudson Cook, LLP who spoke on behalf of the Commercial Finance Coalition (CFC). CFC is an alliance of financial companies that educates government regulators and elected officials on issues related to non-bank commercial finance. CFC Executive Director, Dan Gans, told deBanked that he believed the committee really understood what Fisher was trying to convey.

Another major advocacy group is the Small Business Finance Association (SBFA). They brought Joseph Looney, COO and General Counsel of RapidAdvance, to testify against SB 1235, and SBFA Chief of Staff Steve Denis sounded optimistic, saying that they have a very good relationship with State Senator Glazer’s office.

“To me, despite the fact that they moved [on] a bill that we’re opposed to through the process,” Denis said. “I think the folks that we’ve been meeting with out there – the senators – they’re all very open to our industry and open to having broader discussion about how to [best] disclose these terms and how to make sure we’re doing what’s in the best interest of small business owners. That’s a real positive, and I’m optimistic that we can get something done.”

As for concern about the bill moving forward, Denis said it’s what he expected.

“It’s just the way the process works in California,” Denis said. “If you look at committee history, they don’t really reject a lot of bills. They like to move bills forward so they can be discussed and negotiated.”

As of this story’s publication, SB 1235’s Judiciary committee hearing had not yet been scheduled.

Update 4/26/18: The hearing is scheduled for May 8, 2018 at 1:30 p.m. PST in Room 112.

Full video of the April 18th hearing below:

Champion Auto Sales Decision Brings Closure to Another Case

April 1, 2018A merchant seeking to have a judgment against them voided on the basis that the underlying Purchase and Sale of Future Receivables agreement they entered into was actually a usurious loan, has had their motion denied pursuant to the law as decided in Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, court records show.

3148521 Canada, Inc. and Amir Soghraty, through attorney Amos Weinberg, attempted to convince the Court that their MCA agreement with Principis Capital was actually a loan. After lingering in the court system for months, the Honorable David Benjamin Cohen, issued a decision on Friday, citing the appellate court ruling.

Specifically, plaintiff argues that the underlying judgment is based upon a usurious loan. Plaintiff and defendant entered into an arrangement where defendant purchased the future receivables that may (or may not) be collected. The Appellate Division, First Department, recently decided this very issue (argued by the same attorney as plaintiff herein) and held “the evidence demonstrates that the underlying agreement leading to the judgment by confession was not a usurious transaction” (Champion Auto Sales, LLC v Pearl Beta Funding, LLC, 2018 N.Y. Slip Op. 01645 [1st Dept 2018]).

The decision can be found under Index # 655008/2017 in the New York Supreme Court

Lawyers Weigh in on Champion Auto Sales, LLC v. Pearl Beta Funding, LLC

March 22, 2018In light of the recent Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC decision, which decided that the particular MCA contract at issue “was not a usurious transaction,” deBanked spoke to a handful of lawyers, including the plaintiff’s lawyer, Amos Weinberg, to get their thoughts on the decision.

“The contract at issue in Champion Auto v. Pearl Beta Funding was really no different than the contracts reviewed over a hundred years ago by the United States Supreme Court, in Home Bond Co. v. McChesney, 239 U.S. 568 [1916], where our nation’s highest court agreed that “the transactions were really loans, with the accounts receivable transferred as collateral security,” and “[i]n so far as the contracts in question here use words fit for a contract of purchase they are mere shams and devices to cover loans of money at usurious rates of interest.” Like most patrons of funding providers, Champion Auto was a one-person company that needed immediate, overnight cash. Presiding Justice Rolando T. Acosta of the Appellate Division remarked, at the argument, that Champion was a “sophisticated” party that “knew what they were getting into.” It is therefore painfully obvious that even though the NYS Legislature criminalized and voided loans to corporations exceeding 25% interest, and even though all victims of loan sharking knew what they were getting into, the courts are loathe to be used as escape hatches for companies trying to get out of paying back loans.”

Giuliano, McDonnell & Perrone, LLP

“It’s an appellate ruling a lot of people have been waiting for. It handles the usury issue in passing, almost as if it goes without saying.”

Hudson Cook, LLP

“The court confirmed that under New York law, a properly structured MCA transaction is not a loan. But I want folks to focus on the ‘properly structured’ piece of that…The court’s decision did not indicate much. But it did say that based on the documentary evidence, which is the contract, that the transaction was not a loan. So it’s important for folks to understand that for [an MCA contract] not to be a loan, it needs to be properly described…this case really shows us how important the contract is.

This case does not mean that all MCA companies are all in the clear. What it means is that MCA companies with properly drafted contracts, and good practices and procedures, are not making loans.”

Harris Beach, PLLC

“First of all, it was a unanimous decision by the three justices in the first department. That doesn’t always happen, so that’s a good thing. I personally would have liked to have seen more discussion out of the appellate department, but the language that’s there happens to be great for the industry. The one thing that I would caution, though, is not to interpret that all merchant cash advances are outside of transactions that would be subject to usury because it really is dependent on the language of the agreement.

[The decision] is a great tool in the arsenal, but I don’t see it as the tool that is going to prevent challenges.”

Hudson Cook, LLP

“This is a very important decision because New York State has a high volume of merchant cash advance companies…so having favorable case law in New York is great for the industry.”

Mavrides, Moyal, Packman, Sadkin

“I am very pleased with the outcome. There are more cases [to be decided], but this is very beneficial. It’s a win for the industry and I hope to see other decisions go in the favor of the advance industry.”

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

“The impact of the Champion decision was direct. We represent several MCA clients and we have a number of cases where Amos Weinberg is representing the merchant. And in one of our cases where a motion to open up a default judgment is at issue, the judge’s law clerk directly emailed us and wants to conference the case based on the Champion Auto Sales decision.”

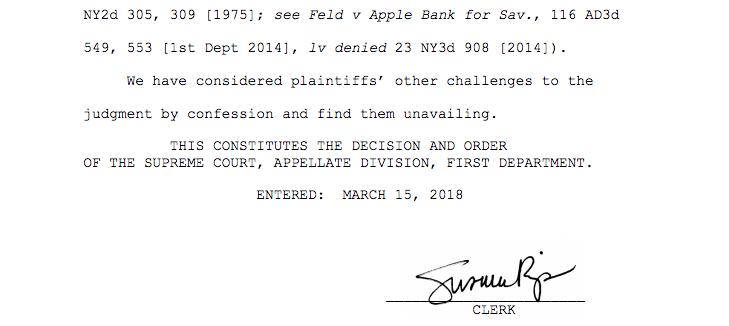

[Lafont also pointed out that even though it was a short decision, one of its two citations was to Feld v Apple Bank for Sav., which deals with overdraft protection and has interesting parallels to MCA.]

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

“Based on the email we just received from the court clerk today, this decision could expedite [future] litigation, and it could decrease certain attorney’s fees for a lot of MCA companies involved in this litigation.”

Debt Relief Scammers’ Assets To Be Auctioned Off

March 20, 2018 A crew of debt relief scammers that carried out an $80 million fraud are having some of their assets auctioned off in Pompano Beach, FL this week. Among them a Tesla, BMW i8, Range Rover and custom luxury buses.

A crew of debt relief scammers that carried out an $80 million fraud are having some of their assets auctioned off in Pompano Beach, FL this week. Among them a Tesla, BMW i8, Range Rover and custom luxury buses.

According to the FTC and the State of Florida in a lawsuit they filed against Jeremy Lee Marcus, Craig Davis Smith and Yisbet Segrea, the defendants “got people to pay hundreds or thousands of dollars a month by falsely promising they would pay, settle, or obtain dismissals of consumers’ debts and improve their credit. Over time, victims found their debts unpaid, their accounts in default, and their credit scores severely damaged – some were sued by their creditors, and some were forced into bankruptcy.”

A court ordered an injunction against the defendants last year.

In an even uglier twist to the scheme, “the defendants also called people who were already enrolled with debt relief providers claiming they were taking over the servicing of those accounts and falsely claiming they would provide the same or similar services. The defendants told these consumers to transfer their escrow money to defendants, and then debited up to $1,000 each month from the consumers’ bank accounts.”

All of the named entities subject to the court-appointed Receiver’s control can be found here.

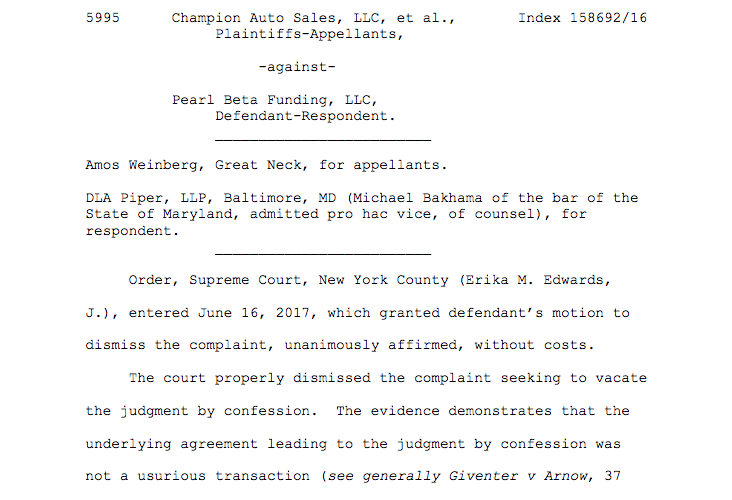

It’s Settled, Merchant Cash Advance Not Usurious

March 15, 2018It’s not a usurious transaction. That’s how trial courts across New York State have been ruling on merchant cash advances for years, but now, thanks to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, the matter has been settled in a key jurisdiction.

On Thursday, March 15th, The Appellate Division of The First Department published their unanimous decision that the underlying Purchase And Sale of Future Receivables agreement between the parties was not usurious.

In October 2016, the plaintiffs sued defendant Pearl in the New York Supreme Court alleging that the Confession of Judgment filed against them should be vacated because the underlying agreement was criminally usurious. As support, plaintiffs argued that the interest rate of the transaction was 43%, far above New York State’s legal limit of 25%.

The defendant denied it and moved to dismiss, wherein the judge concurred that the documentary evidence utterly refuted plaintiffs’ allegations.

With the case over, plaintiffs appealed the decision. Their major loss is spelled out below:

The decision is an interesting chapter in the story of Amos Weinberg, the attorney who represented the plaintiffs in this case. Prior to the appeal, he managed to file more than 100 lawsuits against merchant cash advance companies for usury. He has had very little success on the merits. Last May, deBanked reported that a judge in another lawsuit had admonished Weinberg for misleading the court over the actual wording of what a contract said.

Now he’s responsible for one of the biggest legal decisions in merchant cash advance history. And not in his favor.

The matter arose out of Index # 158692/2016 in the New York Supreme Court.

Princeton Alternative Funding Files Chapter 11

March 9, 2018Princeton Alternative Funding LLC filed for chapter 11 on Friday, court records reveal. A related entity, Princeton Alternative Income Fund, LP, also filed for Chapter 11.

Princeton Alternative Funding provides capital for businesses that make consumer loans in the non-prime market.

The Princeton Alternative Income Fund was previously reported to be a woe affecting Ranger Direct Lending after the blowup of online consumer lender Argon Credit.

AltFi reported in November that Ranger had written to Princeton to urgently seek information about Argon-related financial reporting prior to the commencement of arbitration proceedings.