Industry News

C-level Credit Exec Leaves Lending Club for Affirm

September 21, 2017Lending Club’s Chief Credit Officer and Interim General Manager, Sandeep Bhandari, has joined fintech lender Affirm, according to Affirm CEO Max Levchin. Levchin posted the following on LinkedIn:

I am excited to announce and welcome Sandeep Bhandari to Affirm, Inc. as Chief Strategy and Risk Officer (CSRO).

Sandeep joins us from Lending Club where he was the Chief Credit Officer (CCO). Prior to Lending Club, he was at Capital One for many years, where he was Assistant Chief Credit Officer at Capital One Bank (Credit Risk Management) and Venture Partner (Capital One Ventures). Prior to that Sandeep held a variety of roles requiring expertise in strategy, credit risk management, marketing, product development, and underwriting across several lines of business including consumer and small business credit card, auto lending, and mortgage and home equity lending.

We are excited for Sandeep to join us for our next phase of rapid growth and to help us fulfill our mission of delivering honest financial products that improve lives.

The move comes on the heels of Lending Club announcing their “most advanced and predictive credit model ever.” Bhandari was responsible for credit strategy and overall credit risk management at Lending Club and presumably would’ve overseen that.

Talkative investors on the LendAcademy forum were not immediately sold on Lending Club’s new system, however. Some users bemoaned that Lending Club is ignoring common sense in favor of data. In one instance, the CEO of PeerCube referenced an interest rate anomaly alleged to be discovered in Lending Club’s pricing as “Data-driven but knowledge-unaware.”

Affirm and Lending Club differ. Whereas Lending Club targets the credit card refinancing market, Affirm helps consumers finance purchases. Last month, Affirm and Walmart were reportedly in talks to offer financing to consumers.

New CTO at Breakout Capital is Former CTO of Capital One Labs

September 18, 2017 Firoze Lafeer, the former Capital One Head of Tech Fellows Program and CTO, Capital One Labs, is now the CTO of Breakout Capital, a Breakout representative confirmed. Lafeer was with Capital One for five years, most recently running the company’s experimental product & technology incubator and accelerator.

Firoze Lafeer, the former Capital One Head of Tech Fellows Program and CTO, Capital One Labs, is now the CTO of Breakout Capital, a Breakout representative confirmed. Lafeer was with Capital One for five years, most recently running the company’s experimental product & technology incubator and accelerator.

Breakout Capital is a fintech small business lender based in Mclean, VA where Lafeer will lead technology, including scaling their tech platform.

Last month, Breakout hired Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. Fleischmann was previously Director of Strategic Partnerships at RapidAdvance. McCammon was previously the Director of Portfolio Management and Credit Operations at OnDeck.

PayPal’s Global Head of Product Comm Joins Lending Club

September 14, 2017Anuj Nayar, PayPal’s global head of product communications, has moved on to Lending Club as VP and head of communications, according to published reports. Nayar was also previously Head of Mac Public Relations at Apple from 2003 to 2008.

At PayPal, Nayar was the primary spokesperson on a range of proactive and reactive issues, according to his LinkedIn profile.

Lending Club has struggled in the PR department since May 2016 when the company’s founder resigned.

SOS Capital Offers Super Bowl Tickets As Part of Charity-Driven Football Contest

September 10, 2017 Think you’re good at NFL predictions? SOS Capital is offering anyone the chance to win Super Bowl tickets in their football eliminator contest. The entry fee is a $100 donation to the JJ Watt Foundation to support Hurricane Harvey flood relief in Houston, TX.

Think you’re good at NFL predictions? SOS Capital is offering anyone the chance to win Super Bowl tickets in their football eliminator contest. The entry fee is a $100 donation to the JJ Watt Foundation to support Hurricane Harvey flood relief in Houston, TX.

Pool Details:

- $100 Donation Entry Fee

- Winner Receives 2 Super Bowl Tickets- Courtesy of SOS Capital

- 100% of proceeds will be donated to JJ Watts Charity

- Unlimited Entries Allowed

- Kicks Off Week 2 of the NFL Season

- Deadline to enter is Thursday Sept 14th 2pm

Contact SOS Capital for details on how to join and donate. Call 212-235-5455 or email Charity@soscapital.com

I have already made my donation to the JJ Watt Foundation and joined. I hope to see many others of you in the contest!

Square Wants to Become a Bank

September 6, 2017 Square is expected to apply for an Industrial Loan Company (ILC) bank charter this week, according to American Banker and other sources. Like SoFi, who is busy trying to do the same thing, their attempt will also face competitive resistance.

Square is expected to apply for an Industrial Loan Company (ILC) bank charter this week, according to American Banker and other sources. Like SoFi, who is busy trying to do the same thing, their attempt will also face competitive resistance.

In June, Richard Hunt, president and CEO of the Consumer Bankers Association (CBA), told deBanked that in the case of SoFi, “The whole world is evolving, fintech is evolving. This was inevitable one way or another.” It is therefore not entirely surprising that Square is following SoFi. Others may wait to see how the regulatory debate plays out before putting in applications of their own, however.

“No one envisioned when they wrote the ILC charter that we would have fintech companies that finance mortgages and student loans from private equity capital and not deposits. It’s a new world. Like with all rules and regulations, federal regulators should periodically review longstanding policy,” Hunt said.

Several people from the banking industry argue that the ILC charter route is a loophole and that if fintech companies exploit it and screw up, they could put the entire banking system at risk.

Christopher Cole, executive vice president and senior regulatory counsel at the Independent Community Bankers of America (ICBA), previously said, “We have been fighting the ILC charter for over a decade. When Walmart tried to apply for an ILC charter in 2006 we objected at that point. And that resistance was part of the reason why they never got a charter.”

On August 25th, Congresswoman Maxine Waters requested that a hearing be held on ILC charters to weigh all the concerns before acting on new ILC applications.

Until then, just because Square wants to become a bank, doesn’t mean they will succeed in doing so.

No, Able is Not Going Out of Business, Company Says

September 5, 2017

An industry blog appears to have stretched the truth, again.

On September 1st, Lending Times published a story that relied on an anonymous source to suggest that Austin,TX-based Able Lending is going bankrupt and selling their portfolio. No other compelling evidence is offered other than Lending Times not having their messages returned. No clues as to what kind of knowledge the source might have and why they have it is provided.

Another blog piled on top of that story by circulating an email this afternoon with “Able Lending closing down?” in the subject line. That blog also wrote that their messages were not returned.

I personally reached out to Able and received an immediate response. Company CEO Will Davis pointed out a flaw with Lending Times’ anonymous source. “This anonymous source doesn’t seem to be anyone close to Able, because Able does not own a portfolio of loans (it originates and distributes loans to direct lenders, who then hold those loans on their balance sheet) and therefore has no portfolio to sell,” he said.

Davis also speculated that there could be an ulterior motive. “We believe this story originated by the fact that we’ve been in active discussions with a number of originators to acquire Able, and there’s a non-zero chance this story was placed in order to throw an interested party off the trail,” he explained.

“In any event, we have no plans to go out of business and no plans to declare bankruptcy,” he concluded.

You’re Under Arrest: Funder Takes Extreme Measures to Counter Data Theft

September 4, 2017

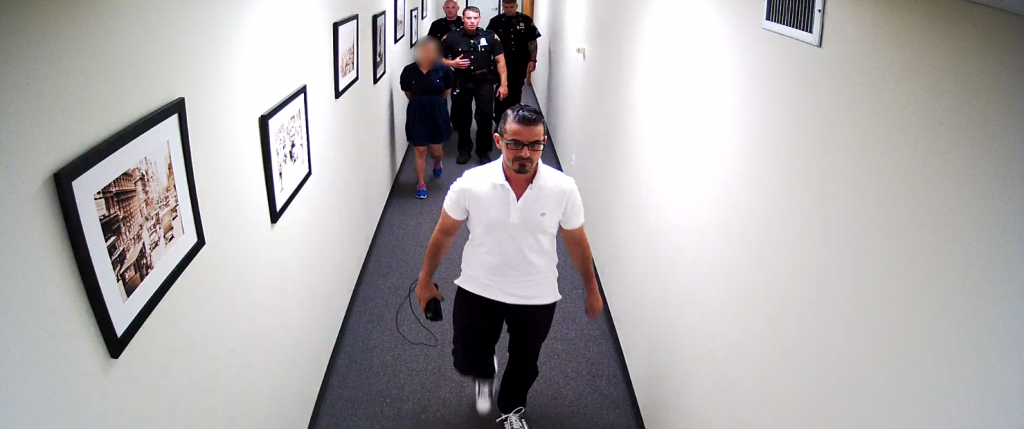

An employee of Yellowstone Capital was arrested last month, according to a source who witnessed the events. At the company’s behest, local police entered Yellowstone’s Jersey City office and handcuffed a female employee who was believed to be engaged in the theft and misappropriation of financial data.

A spokesperson for Yellowstone would not comment on the events nor release the name of the accused. deBanked nevertheless obtained a photo of the individual being escorted out by police. We’ve blurred out her face to protect her identity. Several of those present, who spoke on the condition of anonymity, said that she had been employed by the company for several years.

When asked more generally about the risks of data leakage in the industry, Yellowstone Capital CEO Isaac Stern said that his company is operating on the edge of hyper vigilance. “Yellowstone is investing tons of time, money, and effort to prevent data theft,” Stern said. “We are doing everything in our power, everything, to address it, and we have even enlisted the assistance of an outside security firm.”

The incident does not stand alone. Last year, a man on Long Island pled guilty to attempted criminal possession of computer related material after being implicated in a merchant cash advance backdooring scheme.

Backdooring is industry jargon for when a broker submits a potential deal to a funder and that file ultimately leaks out to third parties whom the broker did not authorize to handle the information. Often times brokers will point their fingers at the funder for mismanaging data they suspect is escaping out the back door. Such accusations can be detrimental to a funder’s reputation not only with the broker community but also with customers they advance funds to. That’s why some funders are taking data security to new levels.

Greenbox Capital, for example, a funder in Miami, FL told deBanked back in March that their company designed proprietary software to monitor the actions of all users on their system, which allows them to know who clicked on what when, and for how long. They also developed algorithms to detect suspicious behavior and their security team receives an alert whenever it gets triggered. Greenbox had initially conducted a 90-day probe and discovered that two employees were stealing data. They don’t want that to ever repeat itself.

Using a cell phone to take pictures of confidential data may not help rogue employees evade detection, according to several funders who have said there are methodologies to spot this behavior but declined to explain what they are. And the risk of getting caught may not merely be termination, as evidenced by arrests that have taken place thus far. These funders say there have been other arrests over the last few years but that the companies did not want to draw attention to them.

Indeed, of the two backdooring-related arrests deBanked has reported on now, neither would officially confirm them.

“We take ISO information extremely serious,” Yellowstone’s Stern explained, lamenting that the value of deal data can inevitably foster rogue behavior, which they are constantly monitoring for.

Put another way, the personal information of a single performing client could be worth as much as $10,000 or more if it gets into the wrong hands. That’s because it could be used to offer that client a loan, advance or other service. The profit could come in the form of a commission, interest, RTR, a closing fee, or even something more nefarious like stealing their identity.

“We know about the pressure people face to illegally transmit data,” Stern said. “They think we don’t know, but we know the industry. Ultimately we will catch you.”

Marketplace Lending Investors Ponder Loan Defaults, Issues in Harvey’s Path

September 1, 2017On the LendAcademy Forum, a Lending Club investor posted that he had been selling notes belonging to Houston borrowers in anticipation of payment issues stemming from Hurricane Harvey. Other users chimed in with assessments of their own personal exposure, including one who noticed that affected zip codes made up a little under 4% of his outstanding principal. By now, secondary note buyers probably have their radar up to heed caution with these.

Elsewhere in the industry, MCA firm Strategic Funding and lender Breakout Capital both announced that they were suspending debits to businesses they’ve funded in the Hurricane’s path.

A message for our customers located in flood-affected areas of Texas pic.twitter.com/4nc8bjWzg5

— Strategic Funding (@SFSCapital) August 28, 2017

The OCC is also advocating that banks suspend payments in those areas from ATM fees to loans. They should consider “restructuring borrowers’ debt obligations, when appropriate, by altering or adjusting payment terms. Payment extensions should reflect individual borrower situations and generally should not exceed 90 days,” according to a statement.