Industry News

Finitive Appoints Neil Wolfson to Board

December 10, 2018 Finitive announced today that it has appointed Neil Wolfson to its Board of Directors. Wolfson also serves on the Board of Directors at OnDeck.

Finitive announced today that it has appointed Neil Wolfson to its Board of Directors. Wolfson also serves on the Board of Directors at OnDeck.

“Finitive has established an innovative platform to provide institutional investors with direct access to alternative lending investments,” said Wolfson. “Finitive’s platform brings further transparency to this asset class.”

According to an April 2018 deBanked story, Finitive was founded in August 2017 and has two kinds of clients: institutional investors and alternative lending companies. Back in April, the company had only four alternative lender clients. Today, they have eight.

“We are very selective [with our lending clients],” Finitive founder and Executive Chairman told deBanked. “We are not a list service.”

Wolfson spent the last decade as President and Chief Investment Officer of SF Capital Group, a private investment group for high net worth families. There, he invested in over 30 direct debt and equity investments in emerging technology companies with a focus on FinTech companies.

Prior to this, Wolfson spent five years as Chief Investment Officer and President of Wilmington Trust Investment Management, a $40 billion investment management firm, and before that, he was the National Partner in charge of KPMG’s Investment Consulting Practice, representing over $100 billion of assets.

“Neil’s experience investing in global technology companies, coupled with a deep understanding of alternative lending markets, makes him an ideal fit for Finitive’s board,” said Barlow.

Finitive is based in New York and has more than 10 employees.

OnDeck Expands Canadian Business with Merger

December 5, 2018 OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

“The combination of OnDeck’s Canadian operations with Evolocity will create a leading online platform for small business financing throughout Canada and represents a significant investment in the Canadian market,” said Noah Breslow, Chairman and CEO of OnDeck. “There is an enormous need among underserved Canadian small businesses to access capital quickly and easily online.“

According to the announcement, “the transaction will combine the direct sales, operations, and local underwriting expertise of the Evolocity team with the marketing and business development capabilities of the OnDeck team.”

As part of the merger, Neil Wechsler, who is the CEO of Evolocity, will become the CEO of OnDeck Canada. And the management team will include Evolocity co-founders David Souaid as Chief Revenue Officer and Harley Greenspoon as Chief Operating Officer. OnDeck Canada will be governed by a Board of Directors chaired by Breslow and composed of existing OnDeck and Evolocity management.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Investment in online small business lending in Canada is growing. IOU Financial, a Montreal-based small business funder that primarily funds American small businesses, told deBanked last month that they made a concerted marketing effort in the third quarter to reach Canadian small business owners. Meanwhile, Thinking Capital, a Canadian online small business funder, announced in July the launch of BillMarket, a service that provides Canadian small businesses with a credit grade (A through E), making it easier for them to get funded.

“BillMarket represents a cash flow revolution for the Canadian small business market,” said Jeff Mitelman, CEO of Thinking Capital, which has roughly 200 employees between its Toronto and Montreal offices.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

Evan Marmott, founder of Canadian small business funder, Canacap, told deBanked earlier this year that unlike the saturated small business market in the U.S., the Canadian small business market is still ripe for growth. Not only this, he said that while the market is smaller in Canada, the default rates are generally lower and he found that Canadian merchants do less shopping around. He also said he has seen less fraud in Canada than in the U.S.

“For brokers, while commissions are lower, you could actually speak to business owners who are not being bombarded with calls [as they are in the U.S.] and have a much higher closing rate,” Marmott said.

Evolocity has 70 full-time employees and offices in Montreal, Vancouver and Marham, in the Toronto area. OnDeck has funded over $10 billion to small businesses and became a public company (NYSE: ONDK) in 2014. OnDeck is headquartered in New York.

“We are excited to join forces with OnDeck…to enhance our best in class digital financing solutions to small businesses across Canada,” said Wechsler, Evolocity CEO. “Additionally, this transaction will augment our data science and analytics capabilities to help deliver an unparalleled merchant experience.”

What We Learned About Credibly From Credibly’s Securitization

November 29, 2018Today, Credibly CEO Ryan Rosett told deBanked that the company’s October securitization will be used, in part, to roll out its new Market Expansion Product (MXP), which will allow Credibly to service merchants with FICO scores as low as 500 and those that have been in business for less time.

“We believe the MXP will open up the funnel by allowing us to serve business owners that we previously couldn’t,” Rosett said.

Kroll Bond Rating Agency assigned preliminary ratings to three classes of notes as part of Credibly’s first securitization. Rosett said this securitization follows a large warehouse line of credit from SunTrust Bank which is also the primary underwriter, of the securitization.

In addition to the new MXP product, Rosett said that Credibly intends to launch a line of credit product in 2019. Currently, Credibly provides merchant cash advances up to $150,000, business expansion loans up to $250,000, with terms up to 24 months, and working capital loans up to $250,000 with terms up to 17 months. Rosett said that the company’s working capital loan is its most popular product.

In an interview yesterday with Benzinga, Rosett said that he has seen a strong increase in demand for Credibly’s products and that they are currently evaluating over 10,000 applications per month.

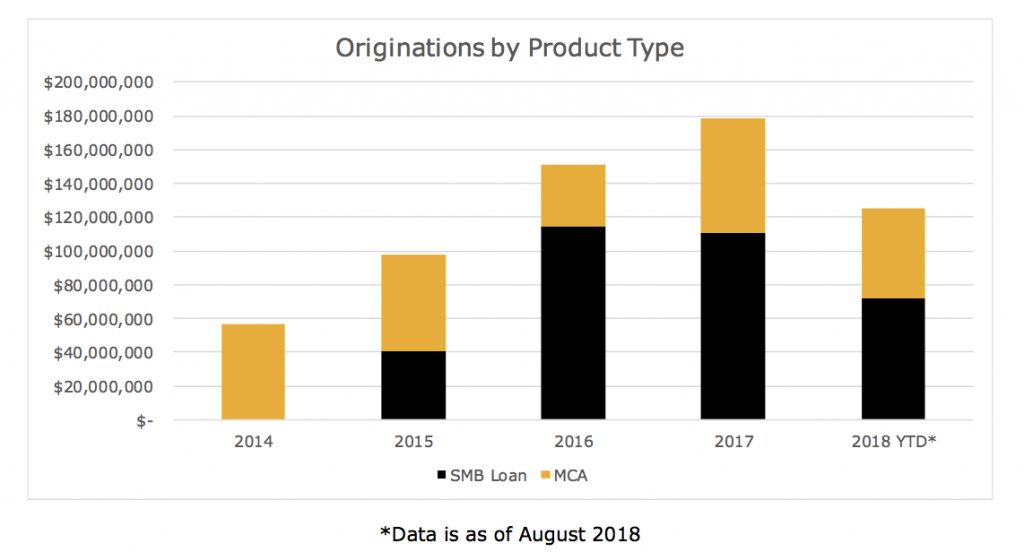

2017 net revenue before provisions: $33 million

2017 earnings: $1.4 million

Total shareholder equity: $18.7 million

Lifetime funding volume: $700+ million

Raw # of fundings: 17,000+

Majority owned by: Flexpoint Ford

# of employees: 140

Notable deal: Acquired the rights to service BizFi’s $250 million MCA portfolio in August 2017

Provides: Small business loans (in 37 states and D.C.) and merchant cash advances

Founded: 2010 by co-CEOs Edan King and Ryan Rosett

Generates deals via: Brokers and inside sales

BFS Capital Announces New CEO

November 28, 2018 BFS Capital announced today that it has appointed Mark Ruddock as CEO, effective immediately. Co-founder Marc Glazer, who has served as interim CEO since the departure of Michael Marrache earlier this year, will be Chairman.

BFS Capital announced today that it has appointed Mark Ruddock as CEO, effective immediately. Co-founder Marc Glazer, who has served as interim CEO since the departure of Michael Marrache earlier this year, will be Chairman.

“I sense there is tremendous potential in this firm,” Ruddock told deBanked. “It has in its DNA an innate understanding of the needs of small business and I think the opportunity for it is to leverage significant increases in data science and technology to help scale and deliver on this potential.”

Most recently, Ruddock served as interim CEO for nearly two years at 4finance, one of the largest European consumer focused online lenders, with more than 3,000 employees and customers across 17 countries. Ruddock said that at 4finance, every day they would issue more than 16,500 loans and make about 22,500 risk decisions. And the entire process was automated.

“There is an opportunity to achieve real scale [in small business lending] through the use of leading edge technology,” Ruddock said, and that is what he intends to do at BFS Capital. Ruddock is relocating to Florida from Berlin, Germany.

Glazer will remain a key part of the operations at BFS Capital.

“One of the biggest assets this company has is Marc Glazer,” Ruddock said. “The two of us see this very much as a joint endeavor moving forward…and I’m going to hold him to remaining actively involved here.”

Their offices are right beside each other, Ruddock said.

“[Ruddock] has an outstanding track record of transforming financial services and technology companies by accelerating their innovation and business growth,” Glazer said. “His diversity of experience, from founder to growth stage executive, across a wide variety of industries and geographies makes him an exceptional choice for BFS Capital at such a pivotal stage in our evolution.”

Ruddock was the founder and CEO of INEA Corporation, an enterprise software firm focused on the financial services industry that was acquired in 2005. Following INEA, he became CEO of mobile software company Viigo, whose flagship app became one of BlackBerry’s most downloaded apps of all time by the time the company was acquired by RIM (Blackberry) in 2010. He held a number of other positions before becoming interim CEO at 4finance in 2017.

Headquartered in Coral Springs, FL, BFS Capital funds American and Canadian small businesses with merchant cash advances and business loans. Through its affiliate, Boost Capital, the company also provides funding to small businesses in the UK. Since 2002, BFS Capital has funded more than $1.9 billion. The company also has offices in New York, California and the UK.

Elevate Funding Strengthens Compliance and Monitor Abilities

November 21, 2018Yesterday, Elevate Funding announced that it would be using the PerformLine Platform to enhance its compliance and email monitoring abilities.

“Terminology is very important in this industry,” said Elevate Funding CEO Heather Francis.

Francis said that much of Elevate’s decision to use PerformLine is to make sure that the correct terms are being used so that the company is consistent in how it presents its MCA product, both to merchants and to referral partners.

“We’ve always been very in tuned to our image, both with our referral partners and with our merchants, and we like to make sure it’s a consistent image,” Francis said.

Together with PerformLine, Elevate Funding created a list of 500 problematic words or phrases. If these terms are used in an email – written by an Elevate Funding employee, a merchant or a referral partner – the email will get flagged and brought to the attention of Francis. Some red flag key terms include “loan,” “term,” “payback” and “free.” Regardless of who wrote the word, the Elevate Funding employee will be asked to send a clarifying follow-up email.

For example, Francis said that if a merchant sends an email that reads “What is my loan balance?” this email would be flagged and the company employee would respond, clarifying that the MCA deal is not a loan. In addition to being clear with customers and referral partners, the PerformLine service is beneficial for compliance reasons.

“In today’s regulatory environment, Elevate must stay on top of its compliance procedures not only to satisfy industry requirements but to ensure the security of sensitive data,” Francis said. “This includes all levels of interactions with our referral partners and the small business owners we service. PerformLine has provided the opportunity to review this information with speed and accuracy, so our compliance team can address any issues as they occur.”

Other funders, like GreenBox Capital, have employed monitoring capabilities not just to protect themselves from legal liability, but to protect merchant data.

Based in Gainesville, FL, Elevate Funding employs about 20 people.

Bankers Healthcare Group Expands Beyond Healthcare

November 20, 2018Bankers Healthcare Group (BHG), which provides financing solutions to healthcare professionals, announced at the end of last week that it is expanding into small business lending with a new license to offer SBA loans through its wholly-owned subsidiary, FundEx Solutions Group. Fundex is now one of only 14 non-bank lenders in the country that offers an SBA 7(a) Loan Guarantee Program, according to the company.

“We’re thrilled to announce that we’ve earned licensure as a non-bank SBA lender,” said Mark Schmidt, CEO of FundEx. “Not only is this a great opportunity for the BHG brand to grow, but it’s a terrific new option for customers who may require loan amounts or terms that are not available through BHG in order to accomplish their business goals.”

BHG, through FundEx, will now be able to provide SBA-backed loans to licensed professions in a variety of sectors including accounting, architecture, law, engineering, financial services and insurance. Loans will go up to $5 million, with terms of up to 25 years. And the loans may be used for a number of different purposes, including real estate acquisition, renovation or expansion, purchase of equipment, business acquisition or commercial debt consolidation.

“There’s market demand for larger loans and we’re excited to offer another innovative lending solution to help licensed professionals grow their own businesses,” said Al Crawford, the original founder, Chairman and CEO of BHC. “We built FundEx Solutions Group based on our tenured success in medical financing to be flexible and fast with excellent customer service.”

Founded in 2001, BHG, based in Syracuse, New York, has provided more than $3.5 billion in funding to to over 110,000 healthcare professionals.

Happy Thanksgiving

November 19, 2018

Dan DeMeo is Back in Action… at Lendr

November 15, 2018 Daniel DeMeo has been hired as Chief Revenue Officer by the Chicago-based funder, Lendr.

Daniel DeMeo has been hired as Chief Revenue Officer by the Chicago-based funder, Lendr.

DeMeo has been working as an independent consultant for the last two years, according to LinkedIn. Prior to that he was the CEO of CAN Capital, a company he had dedicated himself to for nearly seven years until an internal account performance issue led to several senior executives taking an immediate leave of absence.

Under DeMeo, CAN enjoyed success as one of the nation’s largest non-bank small business financiers, partially attributed to the company’s major head start in pioneering merchant cash advance products when the company was founded in 1998. DeMeo even landed on the cover of deBanked’s November/December 2015 issue, around the time when the company was widely believed to be planning an IPO.

It never happened.

The systems issue that toppled CAN’s top execs including DeMeo, brought the company to its knees, putting all new funding on hold for six months until it was saved by a capital infusion from Varadero Capital in July 2017. CAN Capital survived while DeMeo has notably since then kept a low public profile.

Now he’s back in action at Lendr, an ambitious funding company that offers MCAs, small business loans, equipment financing, and just recently, factoring.

“Dan is a highly strategic and thoughtful leader with broad perspective of the industry that enables him to understand specific challenges we face as a growing company,” said Tim Roach, CEO of Lendr. “Dan’s experience is a perfect addition to the team as we accelerate our growth plans, raise Lendr’s brand recognition, and further increase our market share.”

“I’m thrilled to be joining such a dynamic and progressive company,” said DeMeo. “Lendr has emerged as one of the leaders in the financial solutions space and we are poised to build strategic partnerships and alliances with those who share the same zeal in helping small- and medium-sized businesses grow.”

Lendr is setting its sights high. “We’ll be north of $100 million in our first year of factoring,” Lendr co-founder and CEO Tim Roach told deBanked in September.

The company has also been showing off its technological and fundraising prowess as of late. This past March, they closed on a $25 million credit facility that’s expandable up to $50 million. That news was followed by the announcement of a new funding option made possible through virtual and physical debit cards.

Lendr has offices in Chicago and New York and employs over 45 people.