Fintech

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

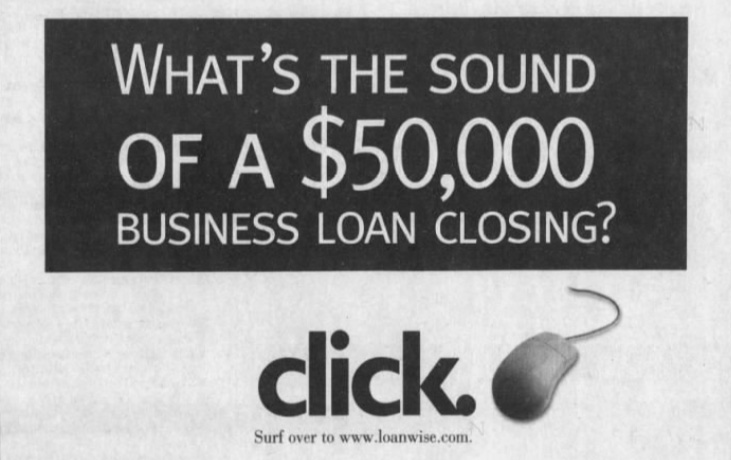

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

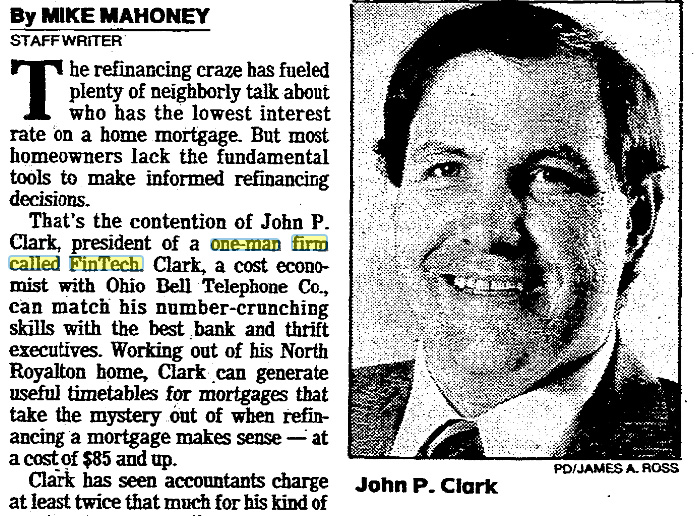

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

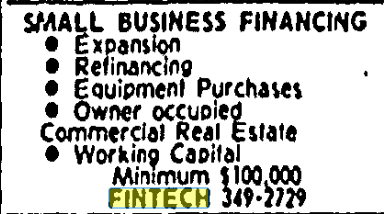

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

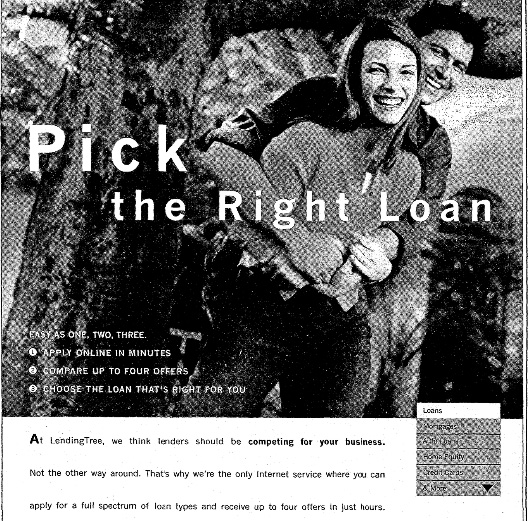

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

New Jersey Continues to Heavily Court Fintech Companies

September 30, 2021 New Jersey’s recent announcement of tax breaks to the fintech company Fiserv in exchange for the company’s commitment to a major hub in the state showcases one of the top private corporate tax breaks in Governor Phil Murphy’s tenure. The move is one of many by the state in recent years as they continue their push to establish a permanent home for fintech.

New Jersey’s recent announcement of tax breaks to the fintech company Fiserv in exchange for the company’s commitment to a major hub in the state showcases one of the top private corporate tax breaks in Governor Phil Murphy’s tenure. The move is one of many by the state in recent years as they continue their push to establish a permanent home for fintech.

Fiserv is seeking the benefits of the state’s Emerge program, an economic development plan that provides businesses with tax incentives based on the number of jobs created. Fiserv’s relocation to a brand-new 428,000 square foot campus in Berkeley Heights will probably come alongside approximately 2,000 new hires, according to the company.

“This announcement from Fiserv is exactly what we envisioned when we created the Emerge program – an innovative company that provides high-paying jobs choosing to expand in New Jersey,” said Murphy. “We’re excited that Fiserv sees what we see in New Jersey, and we look forward to the company’s continued success.”

Fiserv’s brass noted that the move to the new offices is a great opportunity to expand their presence while providing opportunities in an area where current employees and customers are familiar with.

Fiserv’s brass noted that the move to the new offices is a great opportunity to expand their presence while providing opportunities in an area where current employees and customers are familiar with.

“[This company] has been in New Jersey for decades” said Frank Bisignano, President and Chief Executive Officer of Fiserv. “Our new location in Berkeley Heights will be a dynamic hub of collaboration and innovation, bringing our people together in an inspiring workplace environment to create opportunity for unmatched energy and career growth experiences as we move payments and financial services forward on behalf of our clients.”

The neighborhood is also embracing the company’s big arrival, as the move drew support from local politicians. Mayor of Berkeley Heights Angie Devanney praised the move, referring to Fiserv as a “great partner” of the city.

“The company’s technology focus and commitment to diversity are an ideal complement to our community, and we look forward to a long-term partnership that will continue to grow,” said Devanney.

According to Fiserv, they have intentions to partner with universities in the area to create programs for students and graduates. Programs with universities would allow Fiserv to have a direct pipeline from top colleges in New Jersey to their employment applicant pools. Rutgers University was the only school mentioned by name in the company’s press release.

Already employing over a thousand New Jersey residents, the move will have more of an impact on how the company is perceived in the area. Their new offices will have a “Leadership in Energy” and “Environmental Design” (LEED) certificate, alongside a pledge to provide $50 million to help minority-owned small businesses return to pre-pandemic normalcy.

Fiserv’s top executive expressed the company’s desire to have a positive impact on its new community as its tax-motivated investment comes to fruition. “As part of our investment in this new Fiserv location, we look forward to being a force for good by engaging in and creating positive and meaningful impact in the Berkeley Heights community,” Bisignano said.

Fintech Company Launching Money Managing App with Big Incentives

September 29, 2021![]() The fintech company Enzo is set to launch a money managing app within the end of the year and is handing out tremendous incentives to draw customers. The company is offering 10% cash back on Uber rides, 5% cashback on Doordash, 1.5% cashback on rent payments, and 1.25% cashback on everything else. Checking accounts offered by Enzo will also get a 0.50% interest rate.

The fintech company Enzo is set to launch a money managing app within the end of the year and is handing out tremendous incentives to draw customers. The company is offering 10% cash back on Uber rides, 5% cashback on Doordash, 1.5% cashback on rent payments, and 1.25% cashback on everything else. Checking accounts offered by Enzo will also get a 0.50% interest rate.

Enzo’s cashback program has its limits. Annual cashback bonuses are capped at $500, and monthly cashback bonuses are capped at $65. According to their site, if a user spends $2,000 on rent, $150 on Uber, and $400 on DoorDash in one month, they would be credited $65 at the end of the month into their Enzo checking account. Once the monthly and/or annual cap has been triggered, an account will continue to earn 1.25% cashback on all other purchases.

“We started Enzo because we kept seeing our friends make the same money mistakes over and over,” said Jeremy Shoykhet, CEO of Enzo. “We saw people who excelled at every aspect of their lives struggling to get their finances in order [and] we felt there had to be a better way.”

Enzo will also be offering their first batch of account holders equity in the company.

“We feel very strongly about helping our members build and steward wealth,” said Shoykhet when asked about the company’s equity offer. “In connection with that mission, we are launching a first of its kind equity program where we will be giving equity to early evangelists of the Enzo brand, more information about the specific mechanics of the program will be available toward year-end,” he said. “The program does not require opening an Enzo account and is subject to terms and conditions.”

The company also has a stock trading interface within its mobile app, so customers can manage liquid cash and investments in the same place. According to Enzo’s website, customers can automatically track gains, dollar cost average over time, customize portfolios, and manage checking accounts all in the Enzo app.

“At our core, we want to help the millennial generation build the financial foundations that help them live the lives they desire,” Shoykhet said.

The company’s banking services will be FDIC insured through Blue Ridge Bank, who will hold all the money and process the transactions. They are also partnered with Unit for the backend technology in the software. Customers will have access to funds in their checking accounts with an Enzo debit card, which will be uniquely designed by artists for the first ten thousand account holders.

Enzo’s webpage claims that their inaugural staff is a “diverse team of veteran Wall Street investors, engineers, operations, and product folks.” They claim to have gathered top level employees from some of the top financial institutions around the globe.

Enzo’s accessibility and seemingly user-friendly software combined with their incentives for account holders portrays a very interesting notion in non-bank finance. Customers are looking for an easy to use, easy to understand, and easy to access multi-platform money management system with perks and incentives.

Enzo has a waiting list approaching 14,000 potential account holders as of Wednesday. As of now, according to Shoykhet, the program will launch as invite-only. They will add new customers into the program on a rolling basis.

This may not be the end of new financial services for Enzo, according to Shoykhet. He hinted to the company’s future plans in his explanation of the product. “We are also planning to launch innovative financial planning features through a mix of human advice [and] technology-powered advice.”

Homegrown Software Enables FundKite to Reconcile MCAs Daily Rather Than Monthly

September 21, 2021 “Data is the future,” said Alex Shvarts, CEO of FundKite. Through his own proprietary software that he personally built, Shvarts and his team can see daily deposits from merchants that FundKite has funded while also viewing the real-time financial condition of their customers. There are no assumptions, no end-of-month scrambling to do MCA reconciliations, and there are significantly less defaults, he says.

“Data is the future,” said Alex Shvarts, CEO of FundKite. Through his own proprietary software that he personally built, Shvarts and his team can see daily deposits from merchants that FundKite has funded while also viewing the real-time financial condition of their customers. There are no assumptions, no end-of-month scrambling to do MCA reconciliations, and there are significantly less defaults, he says.

Shvarts believes that he has a better chance of retaining clients and keeping deals in place when customers face difficulties. “When merchants are in trouble, they are being coached not to pay,” he said, hinting at third parties in the industry that lobby customers to stop payment in exchange for some kind of alleged assistance.

“Our merchants don’t go under,” Shvarts said.

The premise is that FundKite’s tech enables both themselves and the customer to keep track of how much money is going in and out in real time. That allows them to apply the precise holdback on a daily basis instead of waiting for a bank statement at the end of the month to see what the difference was.

“Our goal is to use our software to be extremely merchant friendly,” said Shvarts.

By compiling different data sets about the merchant, potential clients can be pre-approved and fully funded in less than an hour through a completely digital application process. While this process of instant pre-approval isn’t new to the industry, it’s the idea of having access to client’s banking information that is key to the software’s accuracy and success in funding packages and payment options.

By compiling different data sets about the merchant, potential clients can be pre-approved and fully funded in less than an hour through a completely digital application process. While this process of instant pre-approval isn’t new to the industry, it’s the idea of having access to client’s banking information that is key to the software’s accuracy and success in funding packages and payment options.

The idea of end-of-month reconciliation doesn’t work for many merchants, according to Shvarts, who was speaking in reference to merchant cash advance transactions. “A month later, they could already be in the hole,” he said. “This product [where debits vary daily based upon true sales] works better for merchants, it works better for portfolios, if you’re actually reconciling and pulling what you’re supposed to, and not what you’re anticipating.”

The system is maintained in-house at the firm’s downtown Manhattan offices, with a fully temperature-controlled server room that is home to dozens of computers that host the company’s software. Backed up in the cloud as a failsafe, the system is as much of a presence in the office, both physically and virtually, as the individuals that work there.

“I’ve always had coding implanted in my mind, it’s an everyday process to make things simpler and faster,” he said. Shvarts explained that his love for coding and finance stems from a childhood passion for chess. “Chess taught me the ability to analyze moves.”

Columbia University’s Fintech Bootcamp Starts Dec 8

September 15, 2021 Columbia University will be launching an intensive Fintech course through the Fu Foundation School of Engineering and Applied Science starting on December 8. The 24-week program advertises that students will learn the intricacies of participating and contributing in the fintech world.

Columbia University will be launching an intensive Fintech course through the Fu Foundation School of Engineering and Applied Science starting on December 8. The 24-week program advertises that students will learn the intricacies of participating and contributing in the fintech world.

According to Columbia’s website, the program will teach students about Python programming, financial libraries, machine learning algorithms, solidity smart contracts, Ethereum, blockchain, and more. The course also promises “real world experience” by completing data set related finance projects.

The workshop will be three days a week, part time, and is designed to be attended alongside a work schedule, according to Columbia’s website. The workshop will be held fully in-person and will require students to participate in projects both in and out of the classroom. “The goal is to give you a comprehensive learning experience and true insight into a “day in the life” of a fintech professional, according to the curriculum.

Part-time bootcamps through Columbia can be costly, as the standard rate sits at $13,995 before any type of scholarship or payment plans.

Columbia will also give members of the workshop full access to their wide array of career services, so that participants can find employment after the program is over.

Columbia University did not immediately return a request for comment about the course.

America’s Football Fans Are About to Meet SoFi

September 9, 2021 When fans of the Los Angeles Rams return to the team’s new stadium for a Week-1 matchup with the Chicago Bears on Sunday, a large fintech brand will be there to welcome them. SoFi, the non-bank that shunned banks until it became a bank itself, secured the naming rights to the football stadium last season in Inglewood where both the Rams and Los Angeles Chargers play home games. (Covid prevented fans from actually attending in 2020.)

When fans of the Los Angeles Rams return to the team’s new stadium for a Week-1 matchup with the Chicago Bears on Sunday, a large fintech brand will be there to welcome them. SoFi, the non-bank that shunned banks until it became a bank itself, secured the naming rights to the football stadium last season in Inglewood where both the Rams and Los Angeles Chargers play home games. (Covid prevented fans from actually attending in 2020.)

It’s one of the boldest marketing campaigns ever taken on by a fintech player, a $400 million gamble of a deal that attempts to bring the legitimacy of the brand to a new level. Whether SoFi’s ambitions will bring millions of new customers into their fold or if the group has been overcome by vanity will be played out over the course of the 20-year deal between the stadium and SoFi.

A big thank you to @lapublichealth, the medical community and first responders + everyone doing their part.

WE’LL SEE YOU AT @SOFISTADIUM THIS FALL!

— Los Angeles Rams (@RamsNFL) May 25, 2021

Sofi’s logo is not just exclusive to the rafters of the 70,000+ seat stadium. It’s on the tickets, television broadcasts, repeatedly said on radio broadcasts, and will be mentioned on millions of social media posts throughout the upcoming seasons. Superbowl 56 will be played this February at SoFi Stadium, and the venue will be a major contributor to Los Angeles’ hosting of the Summer Olympics in 2028.

The stadium can also reach potential customers outside of the sports world. The Rolling Stones, Kenny Chesney, Motley Crue, and Def Leppard are scheduled to hold concerts at SoFi over the next few years, bringing hundreds of thousands of people to the stadium — all of whom will be exposed to the SoFi brand.

Rams owner Stan Kroenke, who used $5 billion dollars of his own money to build SoFi stadium, resonated with the company’s goals when announcing the stadium’s name last year. “It would be impossible to build a stadium and entertainment district of this magnitude without incredible and innovative partners who share our ambitions for Los Angeles, our fans worldwide and the National Football League” said Kroenke. “Since breaking ground at Hollywood Park, more than 12,000 people have worked side-by-side on this project, and we are proud to now have SoFi join us on this journey”.

Much like big banks that have name recognition, SoFi is just one of many who have their name on a stadium. Chase Field in Arizona, TD Garden in Boston, and Citi Field in New York are some of the costliest stadium naming rights in the industry.

It seems that if you want to be a big bank, having your name on a stadium is a rite of passage.

Ikea Invests in BNPL Service, Will Use Own Brand for Lending

August 31, 2021 Ikea’s majority parent company Ingka Group announced on Tuesday that they will join the buy-now-pay-later (BNPL) space with Jifiti, a group that offers flexible payment options. Jifti will also allow Ikea to keep their name, making it appear to consumers that Ikea is offering the service themselves — not a third party.

Ikea’s majority parent company Ingka Group announced on Tuesday that they will join the buy-now-pay-later (BNPL) space with Jifiti, a group that offers flexible payment options. Jifti will also allow Ikea to keep their name, making it appear to consumers that Ikea is offering the service themselves — not a third party.

What separates Jifiti from other BNPL services is their willingness to allow companies to use their own names in the borrowing process, so the company themselves appear as the lender. This use of their own brand in the checkout process when offering the BNPL service encourages customers to use the service as Ikea’s brand recognition and reputation are universally top tier in their industry. Combined with their business model of cost efficiency and great service through do-it-yourself assembly, customers may be intrigued to use BNPL if they are under the impression that they are borrowing from a company they already trust.

Jifiti will require credit checks, and may charge interest to buyers who choose to utilize the payment options, but Ikea has the option to pay the interest on products financed through these services in a promotional capacity, to encourage customers to use the service to purchase more. By taking a stake of $20 million in Jifiti and not just using their service, Ingka group will be able to see how these tools are utilized and get insight on how the industry works between both the lending process, consumer payback, and default rates throughout Jifiti’s entire book of business.

This is one of the many moves in an exploration of the financial scene for Ikea’s parent company, as Ingka Group acquirred 49% of Swedish Bank Ikano in Feburary. It seems as if as the company is looking to host a full array of financial services both in store and online at Ikea sometime in the future.

Despite offering access to credit for more expensive items previously, Ikea will partner with Jifiti so that consumers can have access to flexible payment options on products that aren’t priced in the thousands. While it may encourage customers to overspend or indulge if they choose to use the service, those same customers will not be able to purchase in the future if they’re still paying off their previous purchases.

Affirm Continues Surge after Exclusive Amazon Deal

August 30, 2021 In a move announced Friday that can change the way consumers interact with the largest online retailer, Amazon and Affirm have partnered together to bring flexible payment options to Amazon customers. A leader in the buy-now-pay-later (BNPL) space, Affirm saw share prices soar as high as 40% Monday morning after inking the exclusive agreement.

In a move announced Friday that can change the way consumers interact with the largest online retailer, Amazon and Affirm have partnered together to bring flexible payment options to Amazon customers. A leader in the buy-now-pay-later (BNPL) space, Affirm saw share prices soar as high as 40% Monday morning after inking the exclusive agreement.

According to the deal, Affirm plans to offer financing options for purchases greater than $50 for qualified Amazon customers. Buyers are approved, given the cost of financing and the price of their product prior to purchase upfront, and allowed to make payments via installments on those products. Customers who choose to finance through Affirm will not be charged any late or hidden fees.

“By partnering with Amazon we’re bringing the transparency, predictability and affordability that Affirm provides today to the millions of people who shop on Amazon.com in the U.S.,” said Eric Morse, Senior Vice President of Sales at Affirm in a press release. “Offering Affirm’s alternative to credit cards also delivers more of the payment choice and flexibility consumers on Amazon want.”

After an exclusive deal with Walmart in February of 2019, the company is continuing their attempt at a market takeover by striking a deal with Apple’s Canadian market and Shopify in the states — both within the last month. Affirm is quickly beginning to show dividends by putting together some of the largest exclusive flexible payment option deals out there.

With competition heating up in the BNPL industry, Affirm isn’t the only one trying to incorporate exclusive deals with large markets. Square, a company founded by Twitter’s Jack Dorsey recently acquired the Australian firm Afterpay for $29 billion. Paypal has also made their presence known by offering similar services. With a market cap at over $26 billion, Affirm will be in the fight to compete in the flexible payment option space. With competition from companies like Paypal and moguls like Dorsey, Affirm CEO Max Lechvin is in familiar territory. Prior to starting Affirm, Lechvin was a co-founder at Paypal.

With transparency a major component of their business model, Affirm customers may begin to spend more while initially paying less, a move that can provide a better experience for customers— something that seems like a no-brainer for any company selling pricey consumer-based products.