Fintech

OnDeck Takes Advantage of New Same-Day ACH Technology

April 12, 2019 Same-day ACH is here, thanks to NACHA’s planned upgrade, and OnDeck, a small business lender, has already incorporated it into its platform.

Same-day ACH is here, thanks to NACHA’s planned upgrade, and OnDeck, a small business lender, has already incorporated it into its platform.

Shaleen Prakash, OnDeck’s Vice-President of Product Management, told deBanked:

“We are hyper-focused to get customers faster access to funding that’s already been

approved for them.”

Small business owners can now access up to $25,000 in funding on the same day they book a loan or make a withdrawal.

“As long as the request is made before the cutoff, funds reach the account by 5 p.m. It doesn’t matter if you are in New York or California,” Prakash said. The same-day cuttoff time and the $25,000 limit are also set by NACHA. OnDeck can lend larger amounts, obviously, up to $500,000, but not through same-day ACH.

OnDeck has already processed “millions of dollars over the new rails,” said Prakash. “Anybody who cares about when they get money and when it gets debited back from their account will benefit from this service. If there’s a cash crunch, the predictability and certainty from same day funding are fundamental to managing a business,” he added.

OnDeck’s same-day funding model is two-pronged, working both for accessing capital or processing payments to the online lender. On the cash management side, entrepreneurs gain access to the funds when they need it, even if they forget about a payment due on a Friday morning.

“A small business owner has to pay suppliers on time or meet payroll. Now they can be certain that the funds will reach the account and they will be able to manage cash flow better,” said Prakash.

OnDeck’s same-day transfers are equally important for making payments back to the lender.

“Think about the small business owner dealing with the challenges of managing cash already and how some have cash sitting in their account for three days,” he said.

Meanwhile, if OnDeck says an account is debited on a Wednesday, they really mean the funds are debited from the account on Wednesday.

NACHA, the National Automated Clearing House Association, created same-day ACH transfers in three phases. Phase one and two were limited to credit and debit transactions, which left out some of the small business population. It didn’t make sense for OnDeck to integrate the technology until now.

“Through the process of providing a loan to customers, we collect their account information, so we already have it. Now we can meet their needs of getting funding faster without introducing any new friction to the customers,” he added.

OnDeck, which boasted origination volume of $658 million in Q4 2018, is scheduled to report Q1 2019 financial results on May 2.

Online Lenders Square Off, Offer The Kabbage In Brooklyn Food Court

April 10, 2019

In a fast gentrifying section of Downtown Brooklyn, online lenders are waging a silent turf war. Each day, hungry consumers flock to DeKalb Market, a subterranean hipster food court where lunch and a drink can cost $17. The maze-like space with retro neon signs and rustic wood countertops offers a dizzying array of cuisines, and with it, the opportunity to indulge in one’s own individual preferences. But if you’re looking for the vendor’s payment machines, you’ll notice an eerie sameness amidst a cacophony of color.

Square processed $85 billion in payments in 2018 and here in DeKalb Market, 75% of the vendors deBanked surveyed relied on Square’s Point-Of-Sale technology. The publicly traded company generated $2.5 billion in payment transaction fees last year alone, but it’s the add-on products like Instant Deposit, Cash Card, Caviar, and Square Capital that are propelling the growth. 244,000 businesses received a loan from Square in 2018 for a total of $1.6 billion. Borrowing is as simple as clicking a few buttons on the POS dashboard, making Square the presumptive lender of choice for businesses in the food court.

But the rankings on a national level say that Square trails behind Kabbage, an online lender with no reliance on a POS system. Kabbage’s growth trajectory has been epic, once a lending service for eBay merchants, the company is now one of the largest online small business lending companies in the United States.

Undeterred by the sea of Square dashboards, billboard advertisements for Kabbage once blanketed the periphery. The ads, which few consumers seemed to gaze at, were clearly meant for the business owners in between the food court and the mall above it. There was also a competitive feel to it, as if Kabbage was subconsciously communicating to Square that they were not alone.

Nowhere to be found was OnDeck, an online lender headquartered a short distance away in Manhattan that does more in loan volume each year than Square and Kabbage. But just because they can’t be seen doesn’t mean they’re not there. Blending into the crowd of consumers, deBanked spots business loan brokers, ones reputed to refer business to alternative capital sources and online lenders, OnDeck among them. 29% of OnDeck’s business in 2018 was attributed to Funding Advisors, an army of independent sales professionals across the country.

But they’re here for lunch just like everybody else, or are they? Their in-person presence may complicate their rivals’ efforts. Can a face and a handshake trump familiar software and the Internet? OnDeck’s $2.5 billion in 2018 loan volume suggests that their diverse sales strategy, including the use of Funding Advisors, has an impact.

Some vendors in DeKalb Market fail and go out of business. Others, like Cuzin’s Duzin, a homemade donut vendor made semi-famous by its feature on a Vice Media TV Show, The Hustle, recently completed renovations and further expanded its business into the nearby Barclay’s Center. Public records show the company just received financing from an equipment leasing company based in Washington State, a possible missed opportunity for the online lenders canvassing the space. Not for long, perhaps, as OnDeck announced it would be entering the equipment finance market this year.

As for Square, the love for the POS product presents a perceived edge. A general manager of Two Tablespoons, another food vendor, told deBanked that he thinks the Square system they rely upon is very easy to use. He said it also creates promotions that allow businesses like them to track customer spending and text a customer (with their permission) if they’ve earned, say, $5 off at a store.

But converting these vendors into borrowers is not guaranteed. Kabbage’s ads could not be found on a recent trip to the food court. And one shop selling burgers there told deBanked that they were aware of the loan product through Square because they use the POS for payments, but that they had no interest in using it to borrow money.

“It’s like a credit card,” she said. “What you take out, you owe. And we choose not to owe.”

Computers Continue to Fine Tune Underwriting

April 5, 2019 What’s the present role of computers in the underwriting process?

What’s the present role of computers in the underwriting process?

“It’s faster and more accurate,” CEO of Kapitus Andy Reiser said of the company’s new AI process. “We get thousands of pages a day of bank statements, and we can digitally read it through [our system] and then manipulate that data and analyze it.”

Co-founder of Clearbanc Michele Romanow said they don’t even have underwriters on staff. Instead, they have data scientists who work to improve their automated process.

CEO of Idea Financial Justin Leto said they have a robust AI model. It receives information like credit score, business type and details about other positions the company has; with that, it generates the term, rate and amount for a deal. But at Idea Financial, the human underwriters evaluate this information and make a decision.

“Human underwriting is still a critical part of funding,” Leto said. “There is an art to underwriting. It’s not just a science. It can’t be cookie cutter.”

Kapitus also employs underwriters. Despite continuing improvements to its AI system, Reiser acknowledged that there are always exceptions that require an underwriter, like if a merchant’s credit is extremely low. Also, underwriters generally get involved on deals for $150,000 or more, implying that more careful consideration by a human being has value, particularly when there’s more money at stake.

“There’s been a big uplift in the amount and quality of data available,” said Farrah Lakhani, Director of Growth and Operations for OakNorth Analytical Intelligence, which ultimately makes small business underwriting decisions mostly using AI.

“The more data you give [the AI machine], the better it learns…but you have to give the machine the right data.”

The right data, she explained, is similar enough data so that it can start to detect patterns and irregularities.

“All the data is useless if you’re not getting insights from it,” she said.

As for AI replacing human beings altogether, Lakhani doesn’t believe that will happen. She thinks we will always need human beings to think and reason.

“AI is replacing tasks, not people,” said Alex Jaimes, SVP of AI & Data Science at Dataminr at the Disruption Forum Fintech conference in New York this week. “So if all you do is tasks, then you might lose your job to AI.”

Top Minds in Fintech Came Together in Manhattan Last Night

April 3, 2019 More than 200 people packed into a Manhattan office last night to hear panelists from top fintech companies discuss everything from Artificial Intelligence (AI) in fintech to U.S. regulations to diversity. The event, called Disruption Forum Fintech NYC, was organized remotely by a Poland-based software and technology consulting company called Netguru. This was their third event, following one in Berlin and another in London.

More than 200 people packed into a Manhattan office last night to hear panelists from top fintech companies discuss everything from Artificial Intelligence (AI) in fintech to U.S. regulations to diversity. The event, called Disruption Forum Fintech NYC, was organized remotely by a Poland-based software and technology consulting company called Netguru. This was their third event, following one in Berlin and another in London.

The event took place at the office of Work-Bench, a VC firm, and most panelists during the four panel event discussed regulations in some form or another.

“We have a conversation with customers before thinking about regulations,” said Katherine Kornas, Senior Director of Product at Betterment, an online financial advice company. “I try to free my team of constraints.”

Afterwards, they address constraints and work creatively with them, she said. But at least they know that they started off from a place of trying to solve a problem for the customer.

“Hire a really fun and creative Chief Compliance Officer,” said Melissa Cullens, Chief Design Officer at Ellevest, which provides investing advice geared towards women. “We wanted to create profiles with people’s faces and she said “No.” But then we ended up coming up with a different idea that was also really great.”

Melissa Cullens, Chief Design Officer at Ellevest, Katherine Kornas, Senior Director of Product at Betterment, Sudev Balakrishnan, Chief Product Officer at Stash

One theme was how U.S. regulations have made it difficult for fintech companies to enter the highly coveted U.S. market, particularly when compared to Europe.

“Regulators in the U.S. decided to go after the banks after the [financial crisis in 2008,]” said Arshi Singh, North America Head of Product at Currencycloud, a London-based company that improves B2B payments. “The UK went the opposite way and made it very lax for fintechs so they could compete with banks.”

In the U.S., fintechs must partner with banks to carry out many services and some banks are friendlier to fintechs than others.

Charley Ma, NYC Growth Manager at Plaid, Jody Perla, MD of Global Banking & Payment Infrastructure at Payoneer

Andrew Boyajian, Head of Banking, North America at Transferwise, which makes it cheaper to send money across country borders, said that part of his job is to find U.S. banks that are willing to work with them. He said that some of them are, but other banks still have policies against working with companies like his that deliver bank-like services.

Nicolas Kopp, U.S. CEO at N26, Dan Westgarth, North America General Manager at Revolut, Arshi Singh, North America Head of Product at Currencycloud, Andrew Boyajian, Head of Banking, North America at Transferwise

One panel focused on AI in fintech.

“All the data is useless if you’re not getting insights from it,” said Farrah Lakhani, Director of Growth and Operations for OakNorth Analytical Intelligence, which analyzes data to fund business loans. “I ask ‘How are we doing this faster with this data?’ How does this add to our value proposition? This helps me get through the wall of lingo.”

With regard to the notion of AI replacing human beings altogether, Lakhani said she thinks we all need to get that idea out of our heads.

“You do need human beings to think and reason,” she said.

Regarding the fear that robots may become as human-like as humans, AI specialist and panelist Alex Jaimes joked that he’s met some humans who he could have sworn were robots.

Farrah Lakhani, Director of Growth and Operations at OakNorth Analytical Intelligence, Alex Jaimes, SVP AI & Data Science at Dataminr

With seven offices in Poland, Netguru employs 600 people, a quarter of whom work remotely. They company was founded in 2008 and more than 90% of its business comes from the U.S., the UK and Germany.

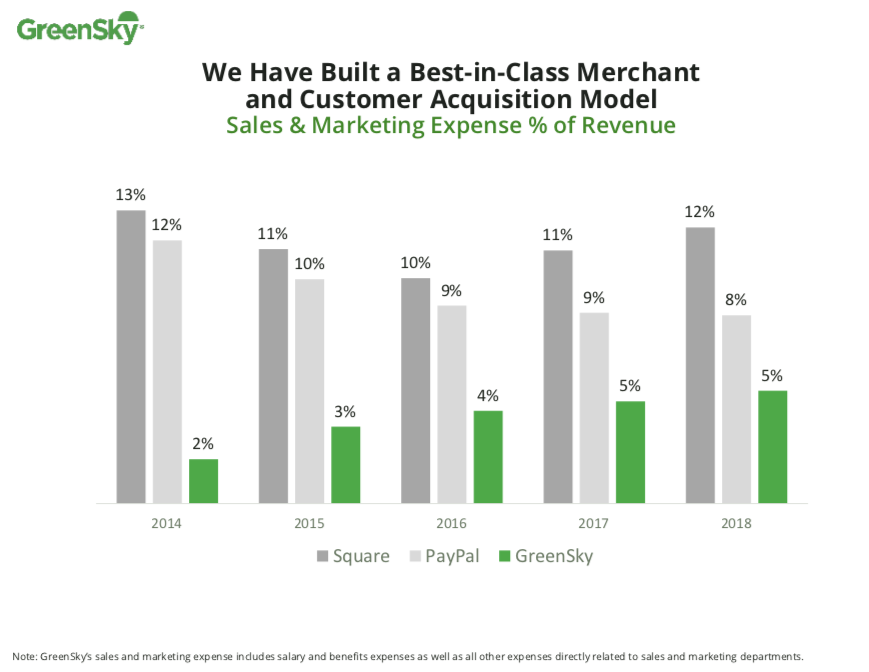

Acquisition Costs Compared for GreenSky, Square, PayPal, OnDeck, Lending Club, and Prosper

March 5, 2019 Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

deBanked examined three additional fintech lending companies and ranked them as follows:

| Company Name | 2018 Sales & Marketing Ratio | 2017 |

| GreenSky | 5% | 5% |

| PayPal | 8% | 9% |

| OnDeck | 11% | 15% |

| Square | 12% | 11% |

| Lending Club | 39% | 40% |

| Prosper Marketplace | 76%* | 72% |

*indicates an estimate

The closeness between Square and OnDeck is notable in that Square markets its payment services first and then offers loans (and other products) as an add-on, while OnDeck only offers loans. Despite that, sales & marketing as a percentage of revenue are still virtually the same for each of them. Square is outspending OnDeck on marketing by more than 10:1, however, and is on pace to surpass OnDeck’s annual loan volume.

Prosper, meanwhile, is doing just as poorly as its wacky ratio looks. The company is losing tens of millions of dollars a year with no end in sight.

Square Capital On Pace to Overtake OnDeck in Small Business Lending

February 28, 2019 OnDeck’s annual loan origination volume has more than doubled since 2014, from $1.2 billion to $2.5 billion, allowing them to retain the top spot in deBanked’s small business funder rankings. But Square Capital, the small business lending division of Square, has grown by 16x since 2014. In the course of 5 years, they’ve gone from being a footnote compared to OnDeck to a fierce rival that is rapidly closing the gap in loan volume.

OnDeck’s annual loan origination volume has more than doubled since 2014, from $1.2 billion to $2.5 billion, allowing them to retain the top spot in deBanked’s small business funder rankings. But Square Capital, the small business lending division of Square, has grown by 16x since 2014. In the course of 5 years, they’ve gone from being a footnote compared to OnDeck to a fierce rival that is rapidly closing the gap in loan volume.

Square’s secret is the ability to generate loan volume at virtually no cost because the product is merely an add-on to their payments-first business. And that’s a problem for OnDeck, because Square has a lot of money to spend on marketing its payments business. More than $400 million a year to be precise. OnDeck, meanwhile, only spent $44 million last year on sales and marketing.

With OnDeck being outspent by a factor of 10, there is a likelihood that Square will overtake OnDeck in the business loan market within the next two years.

And Square’s strength is the ecosystem it’s building. On the Q4 earnings call, company CEO Jack Dorsey said, “I believe the ecosystem is extremely sticky, because it builds durable relationships. If we’re just focused on providing payments in the Register, certainly, there are so many other competitors out there. But when people come in for payments in the Register and then they use [our] payroll for their restaurant and they use Caviar and are really getting offers from Square Capital, it’s really hard to find that mix anywhere else and that builds durability.”

Small Community Banks Power Fintech Revolution

February 15, 2019 “A few years back there was a lot of disruption talk about how the fintechs were going to destroy the banks,” said Jo Ann Barefoot, co-founder of Hummingbird Regtech and a former deputy U.S. Comptroller of the Currency, which regulates national banks. “There’s much more talk in the last few years about the need for banks to partner [with fintechs].”

“A few years back there was a lot of disruption talk about how the fintechs were going to destroy the banks,” said Jo Ann Barefoot, co-founder of Hummingbird Regtech and a former deputy U.S. Comptroller of the Currency, which regulates national banks. “There’s much more talk in the last few years about the need for banks to partner [with fintechs].”

This quote was cited in a CNBC story published today and judging from the recent bank partnerships with some of the largest fintech companies – including Square, Stripe and Robinhood – this could not be more evident. The CNBC story points out that most of these fintech/bank partnerships are not with household name banks, but rather with small community banks that welcome the business. These banks, including Sutton Bank, headquartered in Attica, OH, Cross River Bank, headquartered in Fort Lee, NJ, and Celtic Bank, headquartered in Salt Lake City, UT, are handling the banking activities for these growing fintechs – activities like holding customer deposits and underwriting consumer and business loans. And significantly, making sure that everything is up to snuff with government regulations.

A number of fintechs, including Square and SoFi, have tried to take the banking component of their businesses into their own hands by applying to become an ILC bank. But they have been met with tough resistance, much of it coming from, interestingly, community banks.

“No one envisioned when they wrote the ILC charter that we would have fintech companies that finance mortgages and student loans from private equity capital and not deposits,” President and CEO of the Consumer Bankers Association told deBanked last year. “It’s a new world. Like with all rules and regulations, federal regulators should periodically review longstanding policy.”

So far, the opposition has been relatively successful but time will tell if it keeps up. Square and SoFi withdrew their ILC loan their applications, but Square eventually reapplied. At the 2018 Money 2020 conference in Las Vegas, SoFi CEO Anthony Noto said he would entertain seeking ILC bank status.

Fintech Inevitable, But Petrou Says Risks Abound

February 12, 2019 At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

If large bank mergers are a trend, Managing Director of Federal Financial Analytics Karen Petrou told MarketWatch that this is in part because banks realize that they can combine resources to develop mobile banking capabilities to compete with online banks.

“If banks don’t come up with ways to innovate, they die,” Petrou told MarketWatch yesterday. “Then consumers are left to do their banking with nonbanks.”

Federal Financial Analytics, where Petrou is the managing director, is a Washington, D.C.-based consulting firm and Petrou is a highly regarded voice in the financial regulation space.

While Petrou acknowledges that online banking is the only alternative if traditional banks don’t innovate, she sees serious problems in fintech which she outlined in a paper published earlier this month, according to American Banker.

For instance, she wrote about the danger of a company like Amazon getting into banking and being able to charge individuals different amounts for the same item based on its knowledge of how much money the customer has. Or, the implementation of better banking policies for people who exercise and eat healthier. Petrou says this favors wealthier people with more time for exercise and greater access to more expensive, healthier food.

“I am all for technology,” Petrou said. “But I spent a lot of time when I was a student at MIT studying tech policy, and there is one after another example of seemingly promising technologies with terrible, unintended consequences.”