Fintech

Are The Bankers Taking Over Fintech?

June 27, 2019

For Rochelle Gorey, the chief executive and co-founder of SpringFour, a “social impact” fintech company, mingling with industry movers and shakers at this year’s LendIt Fintech Conference was just what the doctor ordered. “I went mainly for the networking opportunities,” Gorey told deBanked.

SpringFour, which is headquartered in Chicago, works with banks and financial institutions in the 50 states to get distressed borrowers back on track with their debt payments. It does this by digitally linking debtors with governmental and nonprofit agencies that promote “financial wellness.

The indebted parties—more than a million of whom had referrals that were arranged by Gorey’s tech-savvy company last year—constitute not only household consumers but also commercial borrowers. “Small businesses face the same issues of cash flow as consumers, and their business and personal income are often combined,” she says. “If their financial situation is precarious, it’s super-hard to get credit, a line of credit, or a business loan.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Armed, moreover, with a “networking app” on her mobile phone, Gorey was able to arrange targeted meetings, scoring roughly a dozen, 15-minute tete-a-tetes during the two-day breakout sessions. These included audiences with community bankers, financial technology companies, and “small-dollar” lenders. “And it went both ways,” she says. “I had people reaching out to me”—just about everyone, it seemed, appeared receptive to “finding ways to boost their customers’ financial health.”

Gorey’s success at networking was precisely the experience that the event’s planners had envisioned, says Peter Renton, chairman and co-founder of the LendIt Fintech Conference. Organizers took pains to make schmoozing one of the key features of this year’s gathering. Not only did LendIt provide attendees with a bespoke networking app, but planners scheduled extra time for meet-ups. “We had around 10,000 meetings set up by the app,” Renton says, “about double the number of last year.”

deBanked did not attend the LendIt USA conference on the West Coast this year. But the publication sought out more than a half-dozen attendees—including several financial technology executives, a leading venture capitalist, a regulatory law expert, and the conference’s top administrators—to gather their impressions. While informal and manifestly unscientific, their responses nonetheless yielded up several salient themes.

The popularity—and effectiveness—of networking was a key takeaway. Most seized the opportunity to rub elbows with influential industry players, learn about the hottest startups, compare notes, and catch up on the state of the industry. Most importantly, the event presented a golden opportunity to make the introductions and connections that could generate dealmaking.

“My goal this year was to strike more partnerships with lenders and fintech companies,” says Levi King, chief executive and co-founder at Utah-based Nav, an online, credit-data aggregator and financial matchmaker for small businesses. “We had great meetings with Fiserv, Amazon, Clover Network (a division of First Data), and MasterCard,” he reports, rattling off the names of prominent financial services companies and fintech platforms.

James Garvey, co-founder and chief executive at Self Lender, an Austin-based fintech that builds creditworthiness for “thin file” consumers who have little or no credit history, said his goal at the conference was both to serve on a panel and “meet as many people as I could.”

Self Lender is in its growth stage following a $10 million, series B round of financing in late 2018 from Altos Ventures and Silverton Partners. Garvey reports having meetings with Bank of America and venture capitalist FTV Capital “over coffee” as well as F-Prime Capital, another venture capitalist. “It’s just about building a relationship,” he said of making connections, “so that at some point, if I’m raising money or want to partner, I can make a deal.”

There was a concerted effort to recognize women, as evidenced by a packed “Women in Fintech” (WIF) luncheon that drew roughly 250 persons, 95% of whom were women. (“Many men are big supporters of women in fintech and we didn’t want to exclude them,” Renton says). The luncheon was preceded by a novel event—a 30-minute, ladies-only “speed-networking” session—which attracted 160 participants, reports Joy Schwartz, president of LendIt Fintech and manager of the women’s programs.

At the luncheon, SpringFour’s Gorey says, “it was empowering just to see lot of women who are senior leaders working in financial services, banks and fintechs.” The keynote speech by Valerie Kay, chief capital officer at Lending Club, was another highlight. “She (Kay) talked about taking risks and going to a fintech startup after 23 years at Morgan Stanley,” Gorey reports, adding: “It was inspiring.”

The women’s luncheon also marked the launch of LendIt’s Women In Fintech mentor program, and presentation of a “Fintech Woman of the Year” award. The recipient was Luvleen Sidhu, president, co-founder and chief strategy officer at BankMobile, a digital division of Customers Bank, based near Philadelphia, which employs 250 persons and boasts two million checking account customers.

I am honored to be the 2019 Fintech Women of the Year and thrilled that @BankMobile won Most Innovative Bank. It’s very exciting to be recognized by @LendIt Fintech with this prestigious award and I congratulate the finalists in all the categories. https://t.co/qjADuKEMrB pic.twitter.com/hFJVFw1fLS

— Luvleen Sidhu (@LuvleenSidhu) April 11, 2019

BankMobile, which also won LendIt’s “Most Innovative Bank” award, has an alliance with Upstart to do consumer lending and a partnership with telecommunications company T-Mobile. Known as T-Mobile Money, the latter service provides T-Mobile customers with access to checking accounts with no minimum balance, no monthly or overdraft fees, and access to 55,000 automated teller machines, also with no fees. (At its website, T-Mobile Money describes itself as a bank and uses the slogan: “Not another bank, a better one.”)

The impressive salute to women notwithstanding, their ranks remained fairly thin: just 733 attendees identified themselves as “female” on their registration forms, LendIt’s Schwartz says, a little more than 18% of total participants. Seventy-five of the 350 total speakers and panelists—or 21%—were female. (Schwartz also reports that another 157 registrants selected “prefer not to say” as their sexual orientation, while 22 checked the box describing themselves as “non-conforming.”)

In LendIt’s defense, deBanked, who caters to a similar audience, regularly reviews its readership demographics using several tools. They have consistently indicated that women make up 18% – 23% of the total, in line with what LendIt experienced at its most recent event.

By all accounts, many panels were informative, jampacked and attendees were engaged. King, who moderated a panel on regulatory changes in small business lending, which dealt with such topics as California’s commercial “truth-in-lending” law and controversial “confessions of judgment” laws, says: “They didn’t have to lock the door but the room was pretty full and people seemed to be paying attention. I didn’t see people studying their cellphones.”

The Expo Hall was teeming with budding fintech entrepreneurs, financial services companies and multiple vendors hawking their wares. But as numerous fintechs were angling to forge lucrative symbiotic relationships with banks, some participants—even those who were hailing the conference for its networking and deal-making opportunities—lamented the heavy presence of the establishment.

The banks’ ubiquitousness especially vexed Matthew Burton, a partner at QED Investors, an Arlington, (Va.)-based, venture capital firm and a veteran fintech entrepreneur. Before signing on with QED last year, Burton had been the co-founder of Orchard Platform, an online technology and analytics vendor for fintech and financial services companies which was purchased by fintech lender Kabbage.

Not only did bankers seem to playing a more prominent role at the LendIt conference, Burton notes, but “big four” accounting firm Deloitte had signed on as a major sponsor. “The energy level seemed a bit lower than in past years,” Burton told deBanked. “It’s not like people were depressed but it wasn’t bubbling with excitement. A couple of years ago we thought all these new fintechs would replace the banks,” he explains. “Now the discussion is over how to partner and collaborate with banks. It’s not as exciting as when everyone thought banks were dinosaurs.

“I couldn’t really tell if there were more bankers attending this year,” Burton adds, “but it sure felt like it.”

King, the Nav executive, told deBanked: “It was a little bit subdued. I don’t know if it was nervousness about the economy or politics, but the subject of risk came up more often in side conversations with venture-backed businesses and banks and alternative fintech lenders. One large bank we deal with,” he adds, “told me it’s spending most of its time working on risk.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute who participated in a standing-room-only session on state and federal fintech regulation, declares: “I’ve been to three of their conferences, including one in New York, and I would say that this one did not have as much pizzazz. It may be that the industry is maturing.”

For his part—when asked whether there was a palpable absence of passion this year—LendIt’s Renton told deBanked: “I would say that it felt more businesslike. Fintech has had a lot of hype and we have had conferences that were ridiculously over-hyped in 2015 and 2016. And in 2017 (the mood) was much more somber. This one felt optimistic and businesslike.”

There were 750 bankers in attendance, almost one in five participants. “The number of bankers was not up significantly” over last year, Renton says, “but the seniority of the bankers was higher. We worked very hard to get senior bankers to attend this year.”

Renton was bullish on the closer ties developing between nonbank online lenders and banks. That was reflected as well in the several panels exploring ways to develop partnerships between the two sides. He noted that a session called “How Banks are Matching Fintechs on Speed of Funding and User Experience” drew a heavy crowd. “It brought more bankers than we’ve ever had before,” Renton says.

Moderated by Brock Blake, founder and chief executive at the fintech Lendio, the panel was composed of three bankers: Ben Oltman, the Philadelphia-area head of digital lending and partnerships at Citizens Bank; Gina Taylor Cotter, a senior vice-president at American Express (the highest-ranking woman at the company); and Thomas Ferro, a senior marketing manager at Bank of America. “The banks came to LendIt not just to learn but to decide whom they’re going to partner with,” Renton says. “Fintechs need banks and banks need fintechs. That is the narrative you hear on both sides.”

(Asked whether any banks sponsored this year’s conference, Renton replied: “They are not sponsoring yet in any number but we are working on that.”)

OnDeck, a top-tier fintech lender to small-businesses in the U.S., which has been making forays abroad to Australian and Canadian markets, is an enthusiastic champion of the fintech-bank union. So much so that it claimed LendIt’s “Most Promising Partnership” award for the cooperative relationship it struck with Pittsburgh-based PNC Bank, which uses OnDeck’s platform to make small business loans. (Among the partnerships that OnDeck-PNC beat out: Gorey’s SpringFour, which was named a finalist in the competition for its association with BMO Harris Bank.)

“We were the first fintech lender to strike a true platform relationship with a bank,” Jim Larkin, head of corporate communications at OnDeck says, noting that the PNC deal follows on the New York-based fintech’s similar, innovative arrangement with J.P. Morgan Chase. “Others may do referrals,” he explains. “What we do is actually provide the underlying platform to accelerate a bank’s online lending capabilities. We deliver the software and expertise to construct the right type of online lending engine.”

Meanwhile, there was avid interest about the stock performance of publicly traded fintechs—for example, Square and GreenSky—both of which had seen their share prices tumble and then recover.

Burton noted that, among venture-backed firms, the most excitement seemed to be coming from Latin America. “Everyone was very bullish on a Mexican company, Credijusto, an alternative small business lender that was written up the in the Wall Street Journal,” he says. “It’s not going public yet but it had a large debt-and-equity raise of $100 million from Goldman Sachs. And SoftBank Group announced a $5 billion Latin American tech fund.

“There was a lot of talk,” he adds, “about how money was flowing into Mexico and Brazil.”

Ocrolus Secures $24M in Series B

June 26, 2019 A fresh logo and new company jumpers aren’t the only recent additions to the Ocrolus offices this month, as the business has secured $24 million in Series B funding.

A fresh logo and new company jumpers aren’t the only recent additions to the Ocrolus offices this month, as the business has secured $24 million in Series B funding.

This development marks the $33 million point in investments for the automation platform. Led by Oak HC/FT, and backed by FinTech Collective,

Bullpen Capital, QED Investors, among other investors, the funds will be put to use expanding upon Ocrolus’s software and staffing.

With 40 employees currently working at Ocrolus, Co-founder and CEO Sam Bobley said that the company hoped to double this number over the next 12 months, aiming to have “a little over north of 80 this time next year.” As well as this, plans are underway to expand the capabilities of their product. Built to analyze financial documents, such as bank statements, pay stubs, and IDs, with 99% accuracy, Bobley explained that he plans for Ocrolus to be able to extract data from invoices and mortgage documents as well.

And while work on their software continues, the company is also looking to develop their customer base. With intentions to both deepen their core clientele, which is small business lenders, while also opening up their product to new markets, Ocrolus is set to put this $24 million towards building upon what they have established since opening their doors in 2014.

As New Regulations Sweep The Industry, Find Out Where The Next Big Opportunities Are

June 25, 2019

Connect with peers, learn from the pros, and find out what the future holds!

Senator Elizabeth Warren Questions Federal Agencies About Discrimination in Fintech Lending

June 12, 2019 Senator Elizabeth Warren and colleague Senator Doug Jones (D-AL) addressed a letter to multiple federal agencies this week to inquire about their individual roles in overseeing fintech, particularly as it pertains to potential discriminatory underwriting.

Senator Elizabeth Warren and colleague Senator Doug Jones (D-AL) addressed a letter to multiple federal agencies this week to inquire about their individual roles in overseeing fintech, particularly as it pertains to potential discriminatory underwriting.

The senators cited a UC Berkeley study that examined discrimination in the era of algorithmic underwriting. “With algorithmic credit scoring,” the researchers write, “the nature of discrimination changes from being primarily concerned with human biases – racism and in-group/out-group bias – to being primarily concerned with illegitimate applications of statistical discrimination. Even if agents performing statistical discrimination have no animus against minority groups, they can induce disparate impact by their use of Big Data variables.”

The letter tasked the Federal Reserve Chairman, OCC Comptroller, CFPB Director, and FDIC Chairman with responding to 5 questions by June 24th. They are:

1. What is your agency doing to identify and combat lending discrimination by lenders who use algorithms for underwriting?

2. What is the responsibility of your agency with regards to overseeing and enforcing fair lending laws? To what extent do these responsibilities extend to the fintech industry or the use of fintech algorithms by traditional lenders?

3. Has your agency conducted any analyses of the impact of fintech companies or use of fintech algorithms on minority borrowers, including differences in credit availability and pricing? If so, what have these analyses concluded? If not, does your agency plan to conduct these analyses in the future?

4. Has your agency identified any unique challenges to oversight and enforcement of fair lending laws posed by the fintech industry? If so, how are you addressing these challenges?

5. Has your agency identified increased cases of lending discrimination in financial institutions that participate in the fintech industry? Are there additional statutory authorities that would help your agency enforce fair lending laws or protect minority borrowers from discrimination in their interactions with the fintech industry?

CLA’s Credit Invisibles Event Kicks Off

June 5, 2019The Canadian Lenders Association event kicks off today in Toronto. Hosted by Perc Canada and TransUnion at Blake, Cassels & Graydon LLP, this is the second in the series on “Credit Invisibles” and “Credit Deserts.”

The CLA’s purpose is to support the growth of companies that are in the business of lending, or providing other means of credit, to small business and individuals by non-conventional or innovative means to exchange ideas and explore ways of improving the sector; encourage principled and professional practices by Innovative Lenders; educate the public at large about Innovative Lending; encourage individual potential borrowers to be informed about the appropriateness of Innovative Lending to the borrowers’ circumstance; and to advocate on behalf of, and represent the interests of Innovative Lenders.

deBanked president Sean Murray will be in attendance.

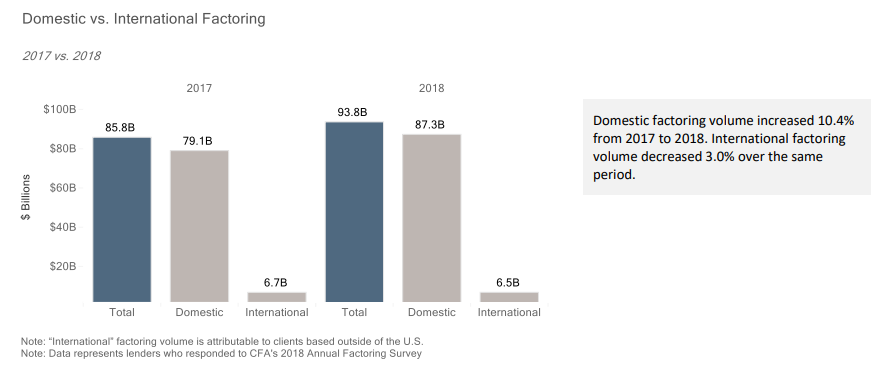

CFA Report Shows Increase in US Factoring Volume

May 30, 2019The Commercial Finance Association (CFA) recently published a report on asset-based lending and factoring which showed a 10.4 % increase in domestic factoring volume in 2018 compared to 2017. While the increase isn’t enormous, it is consistent with a gradual growth in factoring, according to Jeff Goldrich, CEO at Princeton, NJ-based North Mill Capital, which provides invoice factoring.

“It’s not a hockey stick, it’s gradual growth,” Goldrich said.

Goldrich attributed the growth, albeit moderate, to two factors. One is that, while not everywhere, he said there’s been some tightening of credit with banks, which leads companies to consider factoring.

The other is that he said large sized companies are increasingly using factoring as a financing option. While factoring is generally more expensive than taking out a bank loan, companies don’t have to worry about having stellar financial history because factors are less concerned with the financial health of the borrower and more concerned with the strength of the receivable.

Another finding in the CFA report is that Recourse factoring increased by roughly 11% in 2018 compared to 2017. Recourse factoring is when a factor has recourse if a company fails and is unable to pay a receivable to a factor’s client, according to Harvey Gross, Executive Director of the New York Institute of Credit. This is unlike the more common Non-Recourse factoring, where the factor can do nothing if the company that the owes the receivable goes out of business. Gross says that Recourse factoring is becoming more common as factors don’t want to take on as much risk.

Gross said that the older, traditional factors (which often cater to the apparel and toy industries, for example) are still Non-Recourse factors. They shoulder the loss if a company can’t pay its invoices. But at the same time, Gross said that these factors want clients with a large volume of invoices and invoices from solid companies.

BlueVine is one of the few companies that offers factoring online, where a company can get funded online without first interacting with a company representative.

“I see a continuation of factoring marrying fintech,” Goldrich said. “That’s where the big backers have interest.”

Canadian Alternative Finance Event Calendar

May 28, 2019Here’s what’s on the agenda this Summer for the Canadian alternative finance industry:

June 5th

Credit Invisibles Summit – Presented by the Canadian Lenders Association

July 25th

deBanked CONNECT Toronto – Presented by deBanked

Online Loans You Can Take To The Bank

April 16, 2019

OnDeck, the reigning king of small business lending among U.S. financial technology companies, is sharpening its business strategies. Among its new initiatives: the company is launching an equipment-finance product this year, targeting loans of $5,000 to $100,000 with two-to-five year maturities secured by “essential-use equipment.”

In touting the program to Wall Street analysts in February, OnDeck’s chief executive, Noah Breslow, declared that the $35 billion, equipment-finance market is “cumbersome” and he pronounced the sector “ripe for disruption.”

While those performance expectations may prove true – the first results of OnDeck’s product launch won’t be seen until 2020 – Breslow’s message seemed to conflict with OnDeck’s image as a public company. Rather than casting itself as a disruptor these days, OnDeck emphasizes the ways that its business is melding with mainstream commerce and finance.

Consider that the New York-based company, which saw its year-over-year revenues rise 14% to $398.4 million in 2018, is collaborating with Visa and Ingo Money to launch an “Instant Funding” line-of-credit that funnels cash “in seconds” to business customers via their debit cards. With the acquisition of Evolocity Financial Group, it is also expanding its commercial lending business in Canada, a move that follows its foray into Australia where, the company reports, loan-origination grew by 80% in 2018.

Consider that the New York-based company, which saw its year-over-year revenues rise 14% to $398.4 million in 2018, is collaborating with Visa and Ingo Money to launch an “Instant Funding” line-of-credit that funnels cash “in seconds” to business customers via their debit cards. With the acquisition of Evolocity Financial Group, it is also expanding its commercial lending business in Canada, a move that follows its foray into Australia where, the company reports, loan-origination grew by 80% in 2018.

Perhaps most significant was the 2018 deal that OnDeck inked with PNC Bank, the sixth-largest financial institution in the U.S. with $370.5 billion in assets. Under the agreement, the Pittsburgh-based bank will utilize OnDeck’s digital platform for its small business lending programs. Coming on top of a similar arrangement with megabank J.P. Morgan Chase, the country’s largest with $2.2 trillion in assets, the PNC deal “suggests a further validation of OnDeck’s underlying technology and innovation,” asserts Wall Street analyst Eric Wasserstrom, who follows specialty finance for investment bank UBS.

“It also reflects the fact that doing a partnership is a better business model for the big banks than building out their own platforms,” he says. “Both banks (PNC and J.P. Morgan) have chosen the middle ground: instead of building out their own technology or buying a fintech company, they’ll rent.

“J.P. Morgan has a loan portfolio of $1 trillion,” Wasserstrom explains. “It can’t earn any money making loans of $15,000 or $20,000. Even if it charged 1,000 percent interest for those loans,” he went on, “do you know how much that will influence their balance sheet? How many dollars do think they are going to earn? A giant zero!”

“J.P. Morgan has a loan portfolio of $1 trillion,” Wasserstrom explains. “It can’t earn any money making loans of $15,000 or $20,000. Even if it charged 1,000 percent interest for those loans,” he went on, “do you know how much that will influence their balance sheet? How many dollars do think they are going to earn? A giant zero!”

Similarly, Wasserstrom says, spending the tens of millions of dollars required to develop the state-of-the art technology and expertise that would enable a behemoth like J.P. Morgan or a super-regional like PNC to match a fintech’s capability “would still not be a big needle-mover. You’d never earn that money back. But by partnering with a fintech like OnDeck,” he adds, “banks like J.P Morgan and PNC get incremental dollars they wouldn’t otherwise have.”

The alliance between OnDeck and old-line financial institutions is one more sign, if one more sign were needed, that commercial fintech lenders are increasingly blending into the established financial ecosystem.

Not so long ago companies like OnDeck, Kabbage, PayPal, Square, Fundation, Lending Club, and Credibly were viewed by traditional commercial banks and Wall Street as upstart arrivistes. Some may still bear the reputation as disruptors as they continue using their technological prowess to carve out niche funding areas that banks often neglect or disdain.

Yet many fintechs are forming alliances with the same financial institutions they once challenged, helping revitalize them with new product offerings. Other financial technology companies have bulked up in size and are becoming indistinguishable from any major corporation.

Big Fintechs are securitizing their loans with global investment banks, accessing capital from mainline financial institutions like J.P. Morgan, Goldman Sachs and Wells Fargo, and finding additional ways — including becoming publicly listed on the stock exchanges – to tap into the equity and debt markets.

One example of the maturation process: through mid-2018, Atlanta-based Kabbage has securitized $1.5 billion in two bond issuances, 30% of its $5 billion in small business loan originations since 2008.

One example of the maturation process: through mid-2018, Atlanta-based Kabbage has securitized $1.5 billion in two bond issuances, 30% of its $5 billion in small business loan originations since 2008.

In addition, fintechs have been raising their industry’s profile with legislators and regulators in both state and federal government, as well as with customers and the public through such trade associations as the Internet Lending Platform Association and the U.S. Chamber of Commerce. Both individually and through the trade groups, these companies are building goodwill by supporting truth-in-lending laws in California and elsewhere, promoting best practices and codes of conduct, and engaging in corporate philanthropy.

Rather than challenging the established order, S&P Global Market Intelligence recently noted in a 2018 report, this cohort of Big Fintech is increasingly burrowing into it. This can especially be seen in the alliances between fintech commercial lenders and banks.

“Bank channel lenders arguably have the best of both worlds,” Nimayi Dixit, a research analyst at S&P Global Market Intelligence wrote approvingly in a 2018 report. “They can export credit risk to bank partners while avoiding the liquidity risks of most marketplace lending platforms. Instead of disrupting banks, bank channel lenders help (existing banks) compete with other digital lenders by providing a similar customer experience.”

It’s a trend that will only accelerate. “We expect more digital lenders to incorporate this funding model into their businesses via white-label or branded services to banking institutions,” the S&P report adds.

Forming partnerships with banks and diversifying into new product areas is not a luxury but a necessity for Fundation, says Sam Graziano, chief executive at the Reston (Va.)-based platform. “You can’t be a one-trick pony,” he says, promising more product launches this year.

Fundation has been steadily making a name for itself by collaborating with independent and regional banks that utilize its platform to make small business loans under $150,000. In January, the company announced formation of a partnership with Bank of California in which the West Coast bank will use Fundation’s platform to offer a digital line of credit for small businesses on its website.

Fundation lists as many as 20 banks as partners, including most prominently a pair of tech-savvy financial institutions — Citizens Bank in Providence, R.I. and Provident Bank in Iselin, N.J. — which have been featured in the trade press for their enthusiastic embrace of Fundation.

Fundation lists as many as 20 banks as partners, including most prominently a pair of tech-savvy financial institutions — Citizens Bank in Providence, R.I. and Provident Bank in Iselin, N.J. — which have been featured in the trade press for their enthusiastic embrace of Fundation.

John Kamin, executive vice president at $9.8 billion Provident reports that the bank’s “competency” is making commercial loans in the “millions of dollars” and that it had generally shunned making loans as meager as $150,000, never mind smaller ones. But using Fundation’s platform, which automates and streamlines the loan-approval process, the bank can lend cheaply and quickly to entrepreneurs. “We’re able to do it in a matter of days, not weeks,” he marvels.

Not only can a prospective commercial borrower upload tax returns, bank statements and other paperwork, Kamin says, “but with the advanced technology that’s built in, customers can provide a link to their bank account and we can look at cash flows and do other innovative things so you don’t have to wait around for the mail.”

Provident reserves the right to be selective about which loans it wants to maintain on its books. “We can take the cream of the crop” and leave the remainder with Fundation, the banker explains. “We have the ability to turn that dial.”

The partnership offers additional side benefits. “A lot of folks who have signed up (for loans) are non-customers and now we have the ability to market to them,” he says. “After we get a small business to take out a loan, we hope that we can get deposits and even personal accounts. It gives us someone else to market to.”

As a digital lender, Provident can now contend mano a mano with another well-known competitor: J.P. Morgan Chase. “This is the perfect model for us,” says Kamin, “it gives us scale. You can’t build a program like this from scratch. Now we can compete with the big guys. We can compete with J.P. Morgan.”

For Fundation, which booked a half-billion dollars in small business loans last year, doing business with heavily regulated banks puts its stamp on the company. It means, for example, that Fundation must take pains to conform to the industry’s rigid norms governing compliance and information security. But that also builds trust and can result in client referrals for loans that don’t fit a bank’s profile. “For a bank to outsource operations to us,” Graziano says, “we have to operate like a bank.”

Bankrolled with a $100 million line of credit from Goldman Sachs, Fundation’s interest rate charges are not as steep as many competitors’. “The average cost of our loans is in the mid-to-high teens and that’s one reason why banks are willing to work with us,” Graziano says. “Our loans,” he adds, “are attractively structured with low fees and coupon rates that are not too dramatically different from where banks are. We also don’t take as much risk as many in the (alternative funding) industry.”

Despite its establishment ties, Graziano says, Fundation will not become a public company anytime soon. “Going public is not in our near-term plans,” he told deBanked. Doing business as a public company “provides liquidity to shareholders and the ability to use stock as an acquisition tool and for employees’ compensation,” he concedes. “But you’re subject to the relentlessly short-term focus of the market and you’re in the public eye, which can hurt long-term value creation.”

Graziano reports, however, that Fundation will be securitizing portions of its loan portfolio by yearend 2020.

PayPal Working Capital, a division of PayPal Holdings based in San Jose, and Square Inc. of San Francisco, are two Big Fintechs that branched into commercial lending from the payments side of fintech. PayPal began making small business loans in 2013 while Square got into the game in 2014. In just the last half-decade, both companies have leveraged their technological expertise, massive data collections, data-mining skills, and catbird-seat positions in the marketplace to burst on the scene as powerhouse small business lenders.

PayPal Working Capital, a division of PayPal Holdings based in San Jose, and Square Inc. of San Francisco, are two Big Fintechs that branched into commercial lending from the payments side of fintech. PayPal began making small business loans in 2013 while Square got into the game in 2014. In just the last half-decade, both companies have leveraged their technological expertise, massive data collections, data-mining skills, and catbird-seat positions in the marketplace to burst on the scene as powerhouse small business lenders.

With somewhat similar business models, the pair have also surfaced as head-to-head competitors, their stock prices and rivalry drawing regular commentary from investors, analysts and journalists. Both have direct access to millions of potential customers. Both have the ability to use “machine learning” to reckon the creditworthiness of business borrowers. Both use algorithms to decide the size and terms of a loan.

Loan approval — or denials — are largely based on a customer’s sales and payments history. Money can appear, sometimes almost magically in minutes, in a borrower’s bank account, debit card or e-wallet. PayPal and Square Capital also deduct repayments directly from a borrower’s credit or debit card sales in “financing structures similar to merchant cash advances,” notes S&P.

At its website, here is how PayPal explains its loan-making process. “The lender reviews your PayPal account history to determine your loan amount. If approved, your maximum loan amount can be up to 35% of the sales your business processed through PayPal in the past 12 months, and no more than $125,000 for your first two loans. After you’ve completed your first two loans, the maximum loan amount increases to $200,000.”

PayPal, which reports having 267 million global accounts, was adroitly positioned when it commenced making small business loans in 2013. But what has really given the Big Fintech a boost, notes Levi King, chief executive and co-founder at Utah-based Nav — an online, credit-data aggregator and financial matchmaker for small businesses – was PayPal’s 2017 acquisition of Swift Financial. The deal not only added 20,000 new business borrowers to its 120,000, reported TechCrunch, but provided PayPal with more sophisticated tools to evaluate borrowers and refine the size and terms of its loans.

“PayPal had already been incredibly successful using transactional data obtained through PayPal accounts,” King told deBanked, “but they were limited by not having a broad view of risk.” It was upon the acquisition of Swift, however, that PayPal gained access to a “bigger financial envelope including personal credit, business credit, and checking account information,” King says, adding: “The additional data makes it way easier for PayPal to assess risk and offer not just bigger loans, but multiple types of loans with various payback terms.”

While PayPal used the Swift acquisition to spur growth and build market share, its rival Square — which is best known for its point-of-sale terminals, its smartphone “Cash App,” and its Square Card — has employed a different strategy.

OF A FREIGHT TRAIN

By selling off loans to third-party institutional investors, who snap them up on what Square calls a “forward-flow basis,” the Big Fintech barged into small business lending with the subtlety of a freight train. In just four years, Square originated 650,000 loans worth $4.0 billion, a stunning rise from the modest base of $13.6 million in 2014.

Square’s third-party funding model, moreover, demonstrates the benefits afforded from being deeply immersed in the financial ecosystem. Off-loading the loans “significantly increases the speed with which we can scale services and allows us to mitigate our balance sheet and liquidity risk,” the company reported in its most recent 10K filing.

Square’s third-party funding model, moreover, demonstrates the benefits afforded from being deeply immersed in the financial ecosystem. Off-loading the loans “significantly increases the speed with which we can scale services and allows us to mitigate our balance sheet and liquidity risk,” the company reported in its most recent 10K filing.

Square does not publicly disclose the entire roster of its third-party investors. But Kim Sampson, a media relations manager at Square, told deBanked that the Canada Pension Plan Investment Board — “a global investment manager with more than CA$300 billion in assets under management and a focus on sustained, long term returns” – is one important loan-purchaser.

Square also offers loans on its “partnership platform” to businesses for whom it does not process payments. And late last year the company introduced an updated version of an old-fashioned department store loan. Known as “Square Installments,” the program allows a merchant to offer customers a monthly payment plan for big-ticket purchases costing between $250 and $10,000.

Which model is superior? PayPal’s — which retains small business loans on its balance sheet — or Square’s third-party investor program? “The short answer,” says UBS analyst Wasserstrom, “is that PayPal retains small business loans on its balance sheet, and therefore benefits from the interest income, but takes the associated credit and funding risk.”

Meanwhile, as PayPal and Square stake out territory in the marketplace, their rivalry poses a formidable challenge to other competitors.

Both are well capitalized and risk-averse. PayPal, which reported $4.23 billion in revenues in 2018, a 13% increase over the previous year, reports sitting on $3.8 billion in retained earnings. Square, whose 2018 revenues were up 51 percent to $3.3 billion, reported that — despite losses — it held cash and liquid investments of $1.638 billion at the end of December.

King, the Nav executive, observes that Able, Dealstruck, and Bond Street – three once-promising and innovative fintechs that focused on small business lending – were derailed when they could not overcome the double-whammy of high acquisition costs and pricey capital.

“None of them were able to scale up fast enough in the marketplace,” notes King. “The process of institutionalization is pushing out smaller players.”