Canada

Loans Canada Announces Online Lending Survey Results

August 9, 2021 Loans Canada published their annual online lending survey results on Monday morning. The company polled online personal loan applicants throughout Canada.

Loans Canada published their annual online lending survey results on Monday morning. The company polled online personal loan applicants throughout Canada.

Among the results, several statistics stand out.

40.8% of respondents said that they felt “pressured” to fill their loan application quickly, a compelling counter to the mainstream narrative that borrowers are demanding speed.

44.8% of respondents said they felt “pressured” to accept credit building services even though 85.3% of applicants that had been rejected for an online personal loan said they had been rejected on the basis that their credit score was too low.

Loans Canada noted large swaths of satisfaction and dissatisfaction alike, finding that applicants that have never been able to get approved for an online personal loan were highly likely to rank the online borrowing experience as “very bad” while those that have been approved were highly likely to rank the online borrowing experience as “good” or “very good.”

How to Think About Credit Invisibility

July 29, 2021Authored by:

Lily Cook, Researcher at Canadian Lenders Association

Tal Schwartz, Senior Advisor at Canadian Lenders Association

Recent research by PERC has highlighted the issue of credit invisibility in Canada, defined as “persons with either no account payment history in their credit report (referred to as “no files”) or fewer than three accounts in their credit report (referred to as “thin files);”

Recent research by PERC has highlighted the issue of credit invisibility in Canada, defined as “persons with either no account payment history in their credit report (referred to as “no files”) or fewer than three accounts in their credit report (referred to as “thin files);”

In Canada, credit scores are calculated using payment history, outstanding debt, credit account history, recent inquiries and types of credit. However, according to research from Cornerstone Advisors, the ‘on-ramps’ to being credit visible are limited and come with challenges. The most common paths are:

- Credit cards:

- Collections: Collections as a point of entry into a credit system immediately sets the consumer at a disadvantage, since the first thing to identify them is a negative characteristic.

In general, Canadians under 25 tend to use credit cards at far lower rates. Those in that age group who do have a credit history have the highest percentage of credit scores below 520, according to Equifax Canada.

The rate and impact of credit invisibility in Canada is significant:

- 35.3% of Canadians are credit invisible vs. 19.3% in the US.

- the issue disproportionately affects immigrants, minority communities or younger individuals.

How are fintechs addressing this?

1. Access to alternative data

Canadian data aggregators provide lenders with access to non-traditional credit information that advanced firms can apply ML to in order to better adjudicate credit.

- Open banking data providers like Flinks and Inverite provide consumer transaction history information that allows fintech lenders to underwrite credit invisibles based on their cash flow instead of their credit score.

- Commercial data providers like Forward AI, Boss and Railz pull financial data from accounting systems, payroll, and point of sale terminals in order to give lenders a more fulsome picture of a businesses health.

2. Make alternative data mainstream

PERC Canada recommended that the CFPB explicitly include non-financial institutions in their definition of a ‘creditor’ in order to report positive payment data to credit bureaus. Credit reports that could ‘reward’ customers for paying telecommunications bills on time, for example, could make the credit system more forgiving in the future.

- Billi, for example, a Canadian fintech allows users to integrate on-time payments for their Amazon Prime and Netflix accounts into their credit reports in order to improve them.

Canadian credit bureaus have also taken active steps to being more inclusive of alternative data. A prime (no pun intended) example is Landlord Credit Bureau’s (LCB) and Equifax’s partnership to allow rent payments to count towards credit scores.

- Both as a way to reduce risk for landlords and give tenants a leg up in the market, this shared use of alternative data is “ninety-plus per cent….positive in nature, so overwhelmingly landlords use this to reward tenants,” LCB’s CEO, Zachary Killam said.

3. Create a better on ramp to credit building

Credit building loans can unlock credit for those with minimal histories or challenging track records. These are installment loans that only pay out once the customer has paid them off, and are offered by fintechs like as Spring, Marble and Refresh.

Essentially reverse loans, the reverse structure protects the lender, in the event that the customer doesn’t make all their payments. Over the course of the loan term, the customer’s payments are reported to the credit bureaus. Borrowell, which recently acquired Refresh’s credit building loan portfolio, is now one of the largest providers of this service in Canada.

So what’s the solution?

In order to drive meaningful change on the issue of credit invisibility, fintechs must continue to enable lenders to challenge the limitations of the credit system – by improving access to alternative data, normalizing its use and building better on-ramps to the credit system than collections and credit cards.

Credit invisibility is caused largely by structural issues within Canada’s data markets, but fintechs are starting to fill these gaps.

Selling Finance Door-to-Door During Covid

April 9, 2021 This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

“We just went back into lockdown. The whole province, everything just shut down,” CEO Patrick Labreche said. “We were getting 20 to 30 new cases a day, and then it jumped to like 200 a day.”

Meanwhile, 110 miles down south at deBanked, de Blasio announced NYC public beaches would be opening up by Memorial Day. Because of the wide range of government shutdowns this past year, Labreche said it is hard to admit to some that his business is booming.

“I was having a conversation with a guy who does payment processing, he makes residuals on his customers, and so his book of business was not making any money right now; he’s hurting,” Labreche said. “So it’s kind of hard to tell a guy like that that we’re flourishing, and maybe you should come work with us.”

Labreche said that the processor was actually going to work with Canadian Financial. Success this past year came from leveraging the interpersonal skills that make an excellent door-to-door salesperson thrive, Labreche said.

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

With a team of salespeople connected through weekly department meetings and messaging groups to keep the energy up, the deals kept rolling in throughout covid. Labreche said his firm is set apart from a good portion of Canadian alt finance: they offer a smorgasbord of financial products directly to the borrower instead of using lead generators.

While most fintechs think all business owners want a one-button final product, Labreche attests to the opposite- his firm sends out salespeople to make sure businesses know they have a rep to rely on.

“I have nothing bad to say about aggregators; that’s their business model, not ours,” Labreche said. “Our business model is going into a business that didn’t even know that the solution was available. When you’re looking online, you’re looking for a solution that you already know is available.”

Labreche favors traditional finance. His firm offers MCAs and other alternative forms of funding but said those are mostly band-aid solutions and he regularly sees MCA deals taking advantage of merchants. For example, Labreche said he walked into an ESCO gas station last month, and through talking to the owner, discovered an opportunity. The owner had taken an MCA from a big Canadian firm but was confused about the cost of capital- he thought he was paying 17%, but Labreche read a recent statement and discovered the rate was really 50%.

“Right there and then he was like, ‘oh my God, that’s crazy I didn’t know,’ he was misled, and it’s like that across the board. So I ended up getting him a quarter-million dollars at four and a half percent on a term loan,” Labreche said. “Nobody’s ever walked into his business or called him, offering him traditional money. We feel like there’s a huge underserved, undereducated market.”

This week, walk-ins have become less of a possibility, with a lockdown banning all non-essential travel. Still, business development manager Julian Hulan looked forward to when things would open back up. He had masked up and gone out on sales calls throughout the year when the government wasn’t in shutdown mode. Recently he traveled to 20 car dealerships to offer financing in a two-day period and said he found merchants excited to see him in person instead of over email.

“They were like ‘oh, I can actually sit down and talk to this guy?’ and that’s when they eat it up,” Hulan said. “They know because they’ve already made that connection face to face, they can call me directly. We don’t do this whole 1-800 Number. You’re going to call me directly and if I don’t answer, you leave me a voicemail, I call you back, it’s that personal relationship between me and that client.”

Canada’s Top Lending Leaders of 2021

December 16, 2020 The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

All CLA members are vetted and accredited based on their corporate standards

and values. Their role is to support the highest level of lending in Canada,

servicing a wide spectrum of business and consumer borrowers’ growth requirements.

See previous year’s leading lending companies

See previous year’s leading lending executives

2021 Award Winners:

Lending Woman of the Year

|

Tiffany Kaminsky | Co-Founder of Symend

Tiffany Kaminsky is the co-founder of Symend, a fintech that uses analytics and behavioural science to create individualized debt recovery programs. The startup, which has offices in Calgary, Toronto and Denver, received USD $52 million in funding earlier this year and plans to hire up to 200 more roles in 2021. |

|

Nicole Benson | CEO of Valeyo

Nicole Benson is the President & CEO of Valeyo, a business solutions provider to financial institutions in Canada. Nicole drives every facet of business forward, with a focus on growing, evolving, and innovating Valeyo’s suite of solutions to meet the changing needs of its clients and the financial services industry. |

|

Andrea Fiederer | CMO of goeasy

Andrea Fiederer is EVP & CMO of goeasy, a leader in non-prime financial services with over 2000 employees. Andrea is responsible for goeasy’s overall marketing and brand strategy for both the easyhome and easyfinancial business units. |

|

Elena Ionenko | Co-Founder of Turnkey Lender

Elena Ionenko is the Co-Founder of Turnkey Lender, a loan origination platform. Under Elena’s leadership, the company has entered 50+ local markets, raised over $3.5 million in venture capital and launched regional offices all over the globe. |

|

Minal Shankar | CEO of Easly

Minal is the CEO of Easly, a SR&ED financing firm. This year Minal has doubled Easly’s capital under management & customer base. Prior to leading Easly, Minal was an investment manager for the VC firm Northgate Capital and an associate in the Technology Investment Banking group at J.P. Morgan Chase. Minal holds an MBA from the NYU Stern School of Business. |

Fintech Innovator the Year

|

Flinks

Flinks is a data company that empowers businesses to connect their users with the financial services they want. |

|

REPAY

REPAY is a leading provider of vertically-integrated payment solutions. |

|

VoPay

VoPay seamlessly connects you to the banking ecosystem enabling anyone to offer efficient and simple bank account payment processing. |

|

Fundmore

FundMore.ai is an automated underwriting system that uses machine learning to streamline the Pre-Funding process for loans. |

|

Provenir

Provenir offers a suite of risk analytics tools for lenders to make adjudication faster and simpler. |

Executive of the Year

|

Jason Mullins | CEO of goeasy

Jason Mullins is the President & CEO of goeasy, a leader in non-prime financial services with over 2000 employees. Since joining goeasy in 2010, Jason has helped the company scale to $1 billion in market capitalization with compound earnings growth of 28%. Jason is a recipient of Canada’s Top 40 Under 40 Award. |

|

Wayne Pommen | CEO of PayBright

Wayne Pommen is the CEO and Founder of PayBright, a Canadian leader in the BNPL space. His firm has partnered with 7,000 domestic and international retailers, and has approved over $1 billion in consumer credit. This year PayBright was acquired by Affirm in a $340 million transaction. |

|

Lawrence Krimker | CEO of Simply Group

At just 33 years of age, Lawrence Krimker has built Simply Group into a category leader in home equipment financing. This year his firm acquired competitors Dealnet & SNAP Financial in transactions that totalled over $750 million and brought his firm to $1.45 billion in assets under management. |

|

Andrew Graham | CEO of Borrowell

Andrew Graham is the CEO and Co-Founder of Borrowell, Canada’s first fintech to provide free credit monitoring. This year Andrew launched Borrowell Boost to help the 53% of Canadians living paycheck to paycheck meet their bill payments. |

|

Maria Soklis | President of Cox Automotive

In the 6 years that Maria Soklis has led Cox Automotive Canada, the company has become a category leader in software and financing solutions for consumers and dealers across the country. Maria has also left her mark with initiatives that promote diverse and inclusive workplaces, and this year signed the BlackNorth Initiative CEO Pledge. |

Emerging Lending Platform of the Year

|

Moselle

Moselle is a digital platform that simplifies the importing workflow for small medium business owners. |

|

Moves

Moves is a financial services platform for independent “gig” workers. |

|

Vendor Lender

VendorLender is Canada’s first POS lender for dealers in the equipment finance space. |

|

Lendle

Lendle is Canada’s first interest free credit provider. |

|

goPeer

goPeer helps everyday Canadians to achieve financial freedom through Peer-to-Peer Lending |

Small Business Lending Platform of the Year

|

Merchant Growth

Merchant Growth is a leading Canadian financial technology company that specializes in small business financing. Over the past decade, Merchant Growth has supported Canadian businesses with hundreds of millions of dollars in growth financing. |

|

Loop

Launched this year, Loop builds credit & payment products specifically for online merchants. The company is operated by the LendingLoop team that popularized P2P lending in Canada. |

|

Thinking Capital

Thinking Capital is one of Canada’s best known fintech lenders to the small business sector. This year the firm has forged relationships with multiple Credit Unions and hit $1 billion in loans deployed. |

|

OnDeck

Since its launch in 2015, OnDeck Canada has |

| Clearbanc

Canadian based Clearbanc is the world’s largest e-commerce funder. Their data-driven approach takes the bias out of decision making. Clearbanc has funded 8x more female founders than traditional VC. |

Consumer Lending Platform of the Year

|

Flexiti

Flexiti is a leader in point of sale financing for retailers and has been named one of Canada’s fastest growing companies two years straight. |

|

CHICC

CHICC is one of the country’s leading rental & homeimprovement financing companies. |

|

Marble Financial

Marble uses fintech to empower Canadians to improve their credit score, manage debt, and budget to achieve financial goals. |

|

PayBright

PayBright is one of Canada’s leading buy now, pay later providers. This year the firm was acquired by BNPL giant, Affirm for $340 million. |

|

goeasy

Canada’s leading alternative financial services provider servicing non-prime Canadians through its easyhome and easyfinancial divisions. |

Auto Lending Platform of the Year

|

GoTo Loans

GoTo Loans is a fintech lender focused on helping consumers access the equity from their vehicle and the leading provider in Canada for automotive repair loans. |

|

Auto Capital Canada

AutoCapital Canada is a national auto finance company that works with dealer partners to help clients finance the purchase of new and used vehicles. This year the firm acquired competitor Rifco. |

|

Carfinco

The Western Canada based lender is a leader in non-prime lending to the auto sector. |

|

Canada Drives

Canada Drives is a leader in fintech auto lending. This year the firm hit over 400 employees and 1 million transactions, servicing consumers across Canada, the US, and the UK. |

|

Clutch

Clutch aims to bring speed and convenience to used car sales by taking the experience completely online. The fintech raised a $7 million round this year from Real Ventures. |

Technology Lending Platform of the Year

|

BDC

Launched only five years ago, BDC’s Tech Group has become a leader in lending to Canadian technology entrepreneurs. |

|

TIMIA

TIMIA is a specialty finance company that provides growth capital to technology companies in exchange for payments based on monthly revenue. |

|

Flow Capital

Flow Capital Corp. is a diversified alternative asset investor, specializing in providing minimally dilutive capital to high-growth businesses. |

|

Venbridge

Venbridge is a Canadian finance company offering non-dilutive venture debt, SR&ED financing, and tax credit consulting services. |

|

SVB

SVB has lead the technology lending movement for 35 years. The firm opened their first Canadian office last year. |

Smarter Loans Co-Founder: Study shows Fintech in Canada Seeing Accelerated Growth

November 24, 2020 There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

The findings show an accelerated shift to digital transactions, which Smarter loans co-founder Vlad Sherbatov attributed to a pandemic-acceleration of the tech-leaning trends that were already coming.

“One of the central insights from this year’s study is the overall increase of fintech adoption and lending,” Sherbatov said. “We’ve also noticed the fact that people are just much more likely to manage their finances online today than they were at this time 12 months ago or a year ago.”

Intending to gain insight into Canada’s fintech industry, Smarter Loans began sending questionnaires to their users starting in 2018.

“We survey some of the people that flow through our website that have used a fintech lending product in the past 12 months, we ask them questions about their experience,” Sherbatov said. “The purpose is to extract insights so that we can help push the industry forward and improve it.”

Even just two years ago the industry was a much smaller space but has ballooned since, and the Smarter Loans survey has become a one-of-a-kind focus on Canadian fintech markets. Featured with this year’s results is commentary from Canadian industry leaders like the Canadian Lenders Association, and deBanked’s own Sean Murray.

“It’s become a bit of a staple in the lending industry,” Sherbatov said. “Because it’s the only piece of research in Canada that is laser-focused on fintech lending.”

With three years of data to compare, Sherbatov said he could see a significant increase in online activity. Part of this is just due to where the world is heading, as Sherbatov described the younger generations just stepping into the financial world.

“This is something that’s been happening for years; this is a trend that has started a long, long time ago,” Sherbatov said. “For younger generations, the way that they approach financial products and companies is very different from someone in my generation or older. Online is the standard of doing business, on-the-go, and mobile is the standard of managing your financial affairs.”

Fintech in Canada, Sherbatov said, tends to lag behind the growth of the fintech industry in other countries but is on the rise due to the Coronavirus. The digital adoption trend was pushed forward, as some customers that had been reluctant to bank online were forced to do so by necessity. Now, these changes to the way business is transacted are here to stay, Sherbatov said.

Like the surge in eCommerce activity, people are going online to make financial transactions.

“You go to Amazon to buy laundry detergent, and you go online to open up a checking account to pay some bills,” Sherbatov said. “Everybody needs financial services, just like everybody else needs household items; it’s how we’re going about obtaining them. This has changed and has accelerated due to Covid.”

State of Fintech Lending in Canada Report Reveals Key Information for Lenders

November 23, 2020 Smarter Loans, Canada’s loan comparison giant, has published its 3rd annual State of Fintech Lending report.

Smarter Loans, Canada’s loan comparison giant, has published its 3rd annual State of Fintech Lending report.

“As Canadians stayed home longer, adoption of fintech products has accelerated dramatically,” the report says, accelerating trends that had already been developing for years. The data is based on survey results submitted by nearly 2,600 fintech lending customers.

While there are dozens of important takeaways, respondents indirectly signaled how valuable it is to be among the brands that are found first by borrowers.

That’s because loan applicants said that they researched fewer lenders than ever before (35% only researched 1 or 2 lenders before applying) and they spent less time researching lenders than ever before (31% said they spent less than 1 hour researching). Furthermore, 51% of respondents said that they only applied with a single provider.

This approach worked. Of those that got approved, 89% of respondents said that they were satisfied or very satisfied with their loan provider.

The trend should signal to lenders that borrowers may simply come to expect a satisfactory experience regardless of where they apply and that there is tremendous value in simply being the first 1-2 lenders that a prospective borrower considers.

And hint hint, it pays to be easily discoverable online. Fifty eight percent of respondents said they discovered their loan provider through online search.

Click here to view the full survey results in Smarter Loans’ official State of Fintech Lending.

Lendified Survives, Under New Management

October 23, 2020 Toronto-based Lendified has returned from the brink. The Canadian alternative small business lender has a new CEO and has resumed the origination of new loans.

Toronto-based Lendified has returned from the brink. The Canadian alternative small business lender has a new CEO and has resumed the origination of new loans.

In June, deBanked published a story that described the company’s impending doom after it was placed in default with its credit facilities, could no longer originate new loans, and had virtually no capital to continue its operations.

The company was since able to partially recapitalize and John Gillberry has come on as the new CEO. Gillberry is described as a “seasoned senior executive with nearly three decades of experience in areas of managing the finance and operations of special situations and venture capital backed enterprises.”

In an announcement, Gillberry expressed optimism for Lendified’s future. “I am excited about the opportunity that Lendified presents and it is uniquely positioned to take advantage of a very large and underserved market,” he said. “The credit underwriting foundation that we are starting from is distinct from any other in this market and we are pleased to be once again originating new loans to independent business owners.”

The company’s primary senior lenders have resumed financing new loans.

Loans Canada Survey Shows Areas to Improve Online Lending

October 14, 2020 As part of the mission to find the best loan options, Loans Canada, a loan matching service, surveyed 1,477 people who have borrowed from online payday lenders. The goal was to look at the average person’s experience that gets an online or payday loan, and the respondents reported problems with the unregulated nature of payday lending.

As part of the mission to find the best loan options, Loans Canada, a loan matching service, surveyed 1,477 people who have borrowed from online payday lenders. The goal was to look at the average person’s experience that gets an online or payday loan, and the respondents reported problems with the unregulated nature of payday lending.

The sample was composed of “credit-constrained” individuals, with 76.2% reporting they had been rejected for a loan in the past year, and 61.5% reporting that they had a low credit score. The data shows that borrowers with poor credit will have to rely on alternative lenders, the survey outlined.

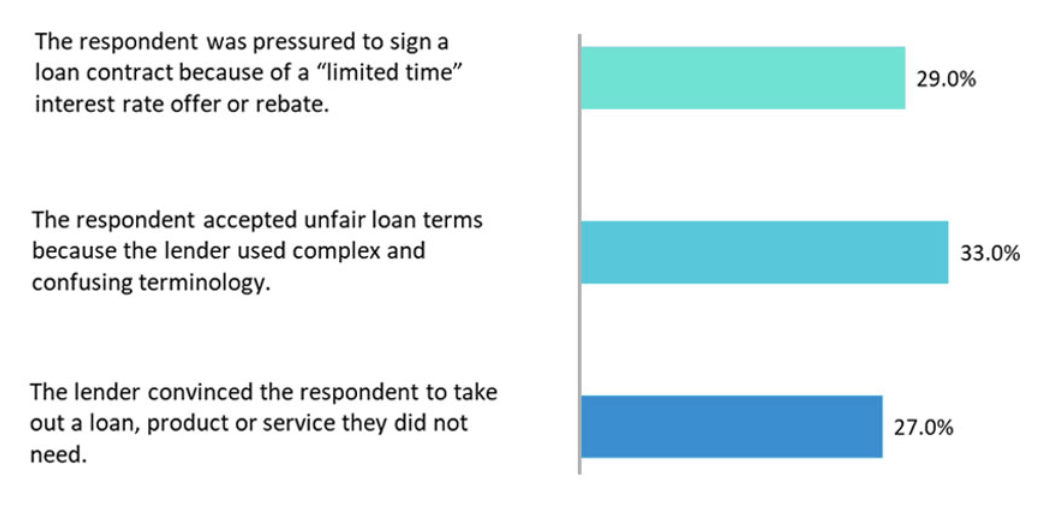

Of those surveyed, more than a fourth reported unfair, problematic lending and debt collecting practices. 33% of respondents said they accepted unfair loan terms because the lender used confusing language and 27% said they took a loan product or service they did not need, convinced by aggressive sales tactics.

Undisclosed and hidden fees were also reported as a problem. 22.4% of respondents said they were charged undisclosed fees while 32.8% were charged fees that “were hidden in the fine print.” 28% of respondents said they were charged without consent at all.

Borrowers faced issues with pre-authorized debits, an agreement where the borrower gives their bank permission to send money to the lender. 33.6% of respondents complained their lender debited their bank when asked not to do so, while 32.5% of respondents had to place a “stop payment” order on the lender.

When it came to paying on time, only 21.9% of borrowers did not miss any payments. Of those who did, over a fourth experienced aggressive behavior from a lender.

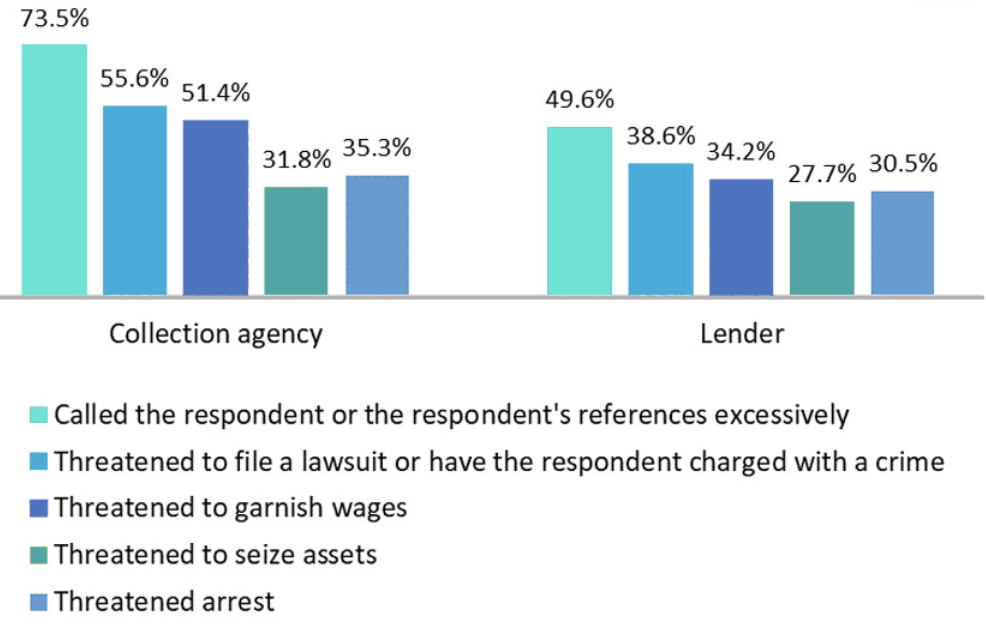

Finally, 32.9% of people who took out an online or payday loan had their debt sold to a collection agency. The paper argues that Canada’s debt collection businesses have to follow different regulations in different provinces. Sometimes, debt collectors can rely on Canadians not knowing their local rights by using unethical intimidation techniques.

Of those that had their debt sent to agencies, 62.1% reported the agency misrepresented themselves when they contacted the borrower, sometimes as law enforcement or as a law office. 52.7% of respondents sent to collections received calls from an agency masked to hide their true identity.

Among lenders themselves, threats to garnish wages, seizing assets, and arrest were in the toolbox for collecting delinquent payments

Loans Canada hopes the information shows problems with online payday lending but highlights credit lines are a two-way street. As lenders need to be held to standards that aim to fix unfair practices, borrowers need to uphold their side of the agreement. Overborrowing is a one-way street to missing payments, leaving lenders little choice.