Business Lending

A GIANT BUFFALO ‘BILL’: Fake Debt Settlement Company Allegedly Defrauded Merchants, Business Lenders and MCA Companies Out of Lots of Cash

November 2, 2016

Several companies controlled by an alleged fraudster run out of western New York, promised merchants they could settle MCA agreements and alternative business loans for cheap.

Sergiy Bezrukov AKA John Butler AKA Thomas Paris AKA Christopher Riley was arrested last week after being charged with mail fraud. A joint investigation between the Department of Homeland Security, the IRS and the US Postal Inspection Service concluded that he scammed more than 100 victims and caused damages in excess of over $500,000.

“The victims and losses are the direct result of Bezrukov’s scheme involving the mailing of thousands of fraudulent solicitations to vulnerable small business owners, luring them into paying him for a service he never intended to provide, and resulting in hundreds of defaulted loans, worth hundreds of thousands of dollars,” an affidavit signed by Postal Inspector Clinton E. Homer states.

$400,000 in hidden cash was seized by investigators. The prosecution argued he was a great flight risk after it was discovered Bezrukov has dual Ukranian citizenship and that an identical copy of his US passport exists which he claims is missing and cannot forfeit. That combined with his propensity to use fake aliases resulted in his bail being denied and his being detained pending trial.

Bezrukov is currently being charged with mail fraud.

Bezrukov is currently being charged with mail fraud.

Records, surveillance and witness interviews confirmed that he paid to have 75,000 mailings sent out to advertise his service just between the first week of August and the first week of October 2016. Those services allegedly included an offer to reduce a small business owner’s short term debt by as much as 75% in just 6 to 12 hours.

One small business owner said that after signing up, they were directed to send an initial $1,250 to Corporate Restructure, Inc. via wire transfer. It was suspicious bank activity like this that would ultimately play a role in the scheme unraveling.

“The Postal Inspection Service received a referral from a fraud investigator for Citizens Banks related to multiple accounts with suspicious activity,” Federal Agent Homer wrote in his affidavit.

Bezrukov is alleged to have used over 30 different company names, numerous banks, post office boxes, UPS Store boxes, and employees in an effort to ensure the success of his scheme, and in an effort to hide his true identity and location of operations. Most of the locations were in upstate New York, specifically in Salamanca, Jamestown, Irving, West Seneca, Cheektowaga, Buffalo and Sanborn.

Two other individuals were also charged in connection with the activity, Mark Farnham of Buffalo and Dustin Walker of Salamanca. Farnham is referred to as the Vice President of Bezrukov’s company, Corporate Restructure, Inc., while Walker was the Chief of Security. They are alleged to have committed bank fraud. More than $125,000 was deposited in their accounts just between June 21st and August 12th of this year.

Bezrukov himself was no stranger to alternative business finance. Numerous complaints online date back to his role in a company known as SBC Telecom Consulting, a purported business funding company that was also referenced in the affidavit attached to the criminal complaint against him.

Even in that business, Bezrukov who went by alias John Butler at the time, was known for being outrageous. Last year, shortly before he ventured into the alleged debt settlement scheme, his company filed a $45 million lawsuit against a former sales rep for among other similar claims, allegedly violating a non-compete agreement.

The Buffalo News reports that Bezrukov is being represented in his criminal case by Scott F. Riordan, who declined to comment on the allegations.

Funders Prep for the Holiday Rush

November 1, 2016

As the year draws to a close sending everyone into a dizzying holiday frenzy, funders are prepared to fire on all cylinders to fuel their retail customers with cash.

The last quarter is crunch time for funders alike, who start preparing months in advance — designing new products, marketing and selling them. deBanked spoke to a few to find out what business looks like at this time of the year and what’s in store for 2017.

For some, Christmas comes in August

At South Dakota-based Expansion Capital Group, the holiday prep started as early as August. “We think demand is going to be very strong and to accommodate for it, we started 60 days early,” said Marc Helman, director of strategic partnerships. The company launched four new products in August for a wide spectrum of borrowers — longer term products for existing customers and starter offers for new companies and those with challenged credit.

Since the demand peak is cyclical, most funders who have been around a while have the drill down to a science. For NYC-based funder Hunter Caroline, demand spikes up close to the tax extension period, in September and October. “We sit down with our marketing team, see which clients ramp up this time of the year and focus our sales efforts in that direction,” said Cody Roth, managing partner at Hunter Caroline. During the holiday season the company turns its attention to customers in mom and pop retail, restaurants, liquor stores and gift stores in small towns.

“We weigh a lot into seasonal businesses and have certain hybrid programs,” Roth said. “We collect a little bit more during the busy season and keep it down during the slow time.” For this year specifically, the two-year-old firm is pushing invoice factoring, purchase order financing and unsecured loan products apart from its usual business loan offering of up to $4 million for 24 months.

Plan, pilot, pivot

Q4 is also the time when companies plan and strategize for the year ahead. And for loan marketplace Bizfi, a lot of changes are in the offing. The company appointed John Donovan, a 30-year veteran in the payments and alternative finance industry as its new CEO. And while on track to approach nearly $600 million of fundings this year, Bizfi also decided to cut ties with some non-performing ISOs to increase efficiency. “We just told around a hundred sales offices we could not do business with them anymore to use resources for our own funding channels that have better conversion rates,” said Stephen Sheinbaum, founder and president of Bizfi.

Holiday Hangover

The holiday season is arguably one of the busiest times of the year for merchants, but it doesn’t have to be so for funders. Jason Reddish, CEO of New Jersey-based Total Merchant Resources advises all his clients to take the money when they don’t need it, asking clients to borrow early, put away the money and by November, have the capital pay for itself through the peak season. “The oldest problem with credit is that you get as much as you want when you don’t need it,” Reddish remarked. “You have access to cheap and the most flexible money when you don’t need it.”

The company tries to structure deals that way for some of its retail clients who see high holiday demand.“We see a pretty big spike going into the holidays and then there is a holiday hangover where they are absorbing all the money they borrowed,” Reddish remarked. “Until the hangover wears off in February and we get busy again.”

All things considered, funders are on their marks for the holiday. Will it be bright for them?

Smile, Dial and Trial? Why the Next Call Might be Your Worst Nightmare

October 26, 2016

Aaron Smith sued a merchant cash advance company in the United States District Court of Southern California earlier this year for allegedly making unsolicited calls to his personal cell phone registered on the Do-Not-Call list. His name has been changed for this story because he’s a vexatious litigator, even landing on an official list of vexatious litigants by the State of California in the early 2000s thanks to his tendency to file harassing lawsuits. But that’s not all, Smith has a criminal history that includes stalking and extortion and he’s served time in prison for his role in a multi-million dollar mortgage fraud RICO conspiracy.

These days he’s suing small business financing companies for alleged violating phone calls, at least five of which we could identify through San Diego court records just over the last several months. Two of the suits appeared while we were researching this story, which means that there could probably be even more by the time that you are reading this.

Smith presumably runs a business as his website has and still continues to advertise services to consumers. But if you are not an existing customer or have not been referred by an existing customer, his website warns that attempting to contact him by any means is a violation. Suffice to say that deBanked did not attempt to contact Smith to get his side of the story.

In one complaint, Smith claims that the phone number receiving the unsolicited calls is a “private personal cellular telephone.” To his credit, a cursory glance of his business website does not appear to list any phone number for it at all. However, the Internet Archive Wayback Machine which allows users to see archived versions of web pages across time, revealed that very same phone number being prominently displayed on his business website for several years including up to as recent as September, 2015, after which it was removed. There’s reason then to question if Smith might be up to no good.

While the merits of Smith’s claims will be up to the courts to decide, his background doesn’t inspire confidence. Countless other plaintiffs using the Telephone Consumer Protection Act (TCPA) to file lawsuits have colorful backgrounds in their own right, a lot of which can be found using Google. But a suggestion relayed by some of our readers is that plaintiffs appear to be doing what they do for profit, not because they have been harmed by the calls they allegedly receive. deBanked decided to conduct its own independent research on this issue.

SUING FOR PROFIT?

That’s just what the headline of a WDSU TV story alluded to in its coverage in 2004 of a stay-at-home Pennsylvania dad named Stewart Abramson. Titled, Man Who Turns Table On Telemarketers Turns Profit, Too, quotes Abramson as saying, “First, I’ll write them all and tell them that I’m willing to settle for the minimum statutory damages per call, which is $500, but if they don’t want to settle, then I’ll file a civil complaint.”

In a case he won against a debt consolidation firm for calling him with a prerecorded message, Abramson reportedly said, “It would have made sense for them to pay the minimum damages due me, but they wanted to put up a fight. I don’t mind. I’ll take more money.”

Abramson continued to say at the time that he felt empowered by Congress to stop this illegal activity and that he was just doing his part and making a little money for doing so. More than a decade later, Abramson’s name is still showing up as a plaintiff in TCPA cases, including in at least one complaint discovered by deBanked against a small business financing company.

Abramson continued to say at the time that he felt empowered by Congress to stop this illegal activity and that he was just doing his part and making a little money for doing so. More than a decade later, Abramson’s name is still showing up as a plaintiff in TCPA cases, including in at least one complaint discovered by deBanked against a small business financing company.

According to court records, the defendant contended that Abramson was “in the business of suing entities for violations of the TCPA,” an accusation the judge ruled irrelevant to the particular matter at hand.

Michael Goodman, a partner in the Washington DC office of law firm Hudson Cook, who was not asked about this case specifically, said in an emailed interview that generally accusing someone of being a serial plaintiff might not really help.

“Accusing a plaintiff of being a serial or professional TCPA plaintiff is unlikely to affect the outcome much, if at all,” Goodman said. “While there are outliers, the general rule is that the court will assess the merits of each case individually and will not ‘punish’ a plaintiff for being a serial or professional TCPA plaintiff.”

An email address for Abramson could not be located and given the special circumstances of his history, we did not attempt to call him.

If ever there was a TCPA celebrity however, it’d be Diana Mey, a self-described stay-at-home mom who started wrangling with telemarketers in 1998 after what her website described as “a series of intrusive telemarketing calls by a Sears affiliate pitching vinyl siding.”

She’s an important figure in TCPA history, not just because she’s been awarded millions through her lawsuits but also because she helped draft the FTC’s rules. Reports show her participating in FTC-hosted telemarketing forums in 2000 and 2002 and her name even appears in the footnotes of the FTC’s Telemarketing Sales Rule entered into the Federal Register in 2003. And so we followed Mey’s story online, noting that she has actually become famous for her pursuits, even appearing in a TV segment for ABC News in 2012. Her website at www.dianamey.com teaches others how they too can pursue monetary damages from telemarketers that engage in illegal practices.

“The first step is to write a formal ‘demand’ letter to the president of the company, stating that the letter is a formal claim for money […] for violations of the Telephone Consumer Protection Act of 1991,” her website advises.

It was quite a surprise then to discover that this Diana Mey was the same Diana Mey captioned as a plaintiff in a current case against a small business financing company. Almost two decades after her first experience, she is still filing lawsuits for alleged telemarketing violations.

Mey declined to respond to our questions even though they were not about that case, citing pending litigation.

“I’m a mom and I’m a housewife, and I’m an accidental activist,” Mey said in that 2012 ABC News interview. Others have referred to her as a “private attorneys general,” defined as someone who brings a lawsuit considered to be in the public interest.

That same title has been attributed to one Robert Braver who is the man behind www.do-not-call.com which launched in 1998 as “a consumer’s resource for stopping unsolicited telemarketing calls.” His comments appear in FCC records and he was also featured in a Dateline NBC special in 2002 about a new telemarketing scheme that was alarming consumers. Suffice to say Braver has been a consumer proponent in this area of the law for a long time, a role that has not come without risks.

According to Braver, the attorney for one telemarketer he sued, arranged to have his (then) elementary school age kids stalked and photographed, a terrifying ordeal that was only made worse after the attorney allegedly sent him a fax bragging about it. But he has continued on, noting that while he has gotten much fewer junk faxes, telemarketing calls have gotten more out of hand over time, to the point where they’re disruptive to everyday life.

“My wife is a middle school teacher,” Braver said. “She doesn’t work in the summer and gets home before I do when she is teaching. She typically leaves her phone in her purse in a spot in the kitchen and hangs out in in the den or back patio. It’s gotten so bad at times that when I need to call her, she doesn’t get up and run to look at her phone when it rings, and I have ignored unknown calls on my cell and let them go to voicemail, only to find out later that they were legit calls.”

And sometimes it’s a total mystery how they even get added to a list. “We have two teenage boys still at home, and they have cell phones too. Somehow my youngest son’s cell number got on a marketing list for student loan debt relief, and was getting 10-15 calls a day for a while,” Braver explained.

Contrast that with a story that appeared in the Dallas Observer in 2010 about one Craig Cunningham, another celebrity-like TCPA figure who still has active cases pending, public records reveal.

According to the story, Cunningham stays at home on a “dumpy couch” to wait for a particular type of phone call, “one from a representative of a debt collection agency or a credit card company, whom he’ll try to ensnare like a Venus fly trap,” the Observer reported. Cunningham is said to have learned his trade from online message boards, where we decided to look next to see if there was anyone out there indeed talking about TCPA lawsuits for profit.

On May 25, 2014, a participant using the pseudonym codename47 published a thread titled, TCPA enforcement for fun and for profit up to 3k per call on fatwallet.com, the exact kind of salacious headline that defendant companies have probably imagined in their worst nightmares. Codename47 has a big fan base it seems, with one user even suggesting to him that he should create and sell a “sue telemarketers” package so that people could do what he does for side income.

Codename47 is Craig Cunningham, who we reached out to with some questions through the fatwallet forum. He declined to answer them, citing pending litigation and the fact that he no longer does interviews.

One user on fatwallet in 2010 said of Cunningham, “It’s kind of hard to convince a Federal judge that you are a victim when you are trying to find a publisher for a book called CREDIT TERRORIST.”

WAIT, WHAT?

WAIT, WHAT?

It now being six years later, no such book can be found in Amazon or through Google. A link to where purported information on it once was leads to a page-not-found error. The Archive Wayback Machine however, produces an interesting find.

Tales Of A Debt Collection Terrorist: How I Beat the Credit Industry At Its Own Game and Made Big Money From the Beat Down is the title of a proposed book in 2010 by Craig Cunningham and Brian O’Connell. O’Connell is a writer/content producer for TheStreet.com and a well-known and widely published author. He tells deBanked that he wished he had written it with Cunningham but that they didn’t move forward with it.

But the proposal remains, including the description of Cunningham as being a highly sought after expert in the field of debt collection “revenge” industry.

Outside of fatwallet, the only other real mention of the proposed book could be found on a website called debtorboards.com. Lenders might find the website horrifying considering the forum’s tagline is “Sue Your Creditor and Win.” With more than 20,000 members and nearly 300,000 posts, the forum has an entire section dedicated to TCPA. Legal strategy is a dominant topic and it’s abundantly obvious that people are working together to stop companies from calling them.

Sadly, it’s not all innocent consumers out there. For example, the TCPA has invited abuse to the point where at least one person admitted to buying cell phones to maximize the chances of getting illegal calls so that they could sue. That’s what serial plaintiff Melody Stoops said in a June 2016 deposition as part of her case against Wells Fargo in the Western District of Pennsylvania.

Q. Why do you have so many cell phone numbers?

A. I have a business suing offenders of the TCPA business — or laws.Q. And when you say business, what do you mean by business?

A. It’s my business. It’s what I do.Q. So you’re specifically buying these cell phones in order to manufacture a TCPA? In order to bring a TCPA lawsuit?

A. Yeah.

Purchasing at least 35 phones, she even went so far as to register them with out-of-state area codes in places she thought were more economically depressed and therefore more likely to get violating calls. Stoops sent out so many pre-litigation demand letters and filed so many lawsuits that she could not be certain how many she sent out or how many suits she was in, according her to deposition.

Purchasing at least 35 phones, she even went so far as to register them with out-of-state area codes in places she thought were more economically depressed and therefore more likely to get violating calls. Stoops sent out so many pre-litigation demand letters and filed so many lawsuits that she could not be certain how many she sent out or how many suits she was in, according her to deposition.

Apparently Stoops found the line of legal perversion and crossed it. On June 24, 2016, the judge ruled in favor of Wells Fargo because she wasn’t injured by the calls she received, nor were the injuries she claimed within the “zone of interests” the law was meant to protect. “It is unfathomable that Congress considered a consumer who files TCPA actions as a business when it enacted the TCPA,” he wrote.

A TURNING POINT?

Hudson Cook law partner Michael Goodman said, “the impact of Stoops v. Wells Fargo is still to be determined, but I would say that it is significantly fact specific and therefore unlikely to result in large-scale changes in TCPA private actions. Stoops put a lot of effort into becoming a magnet for calls that could violate the TCPA. In many TCPA cases, consumers do not need to try that hard to receive a call that could prompt a TCPA suit.”

Stoops was pursuing calls while most of the advice and discussion uncovered online is about what to do if you get a call, not about how to create the calls in the first place. Even debtorboards, for example, is a registered non-profit, keeping consistent with its image as a consumer empowerment tool.

If the tide is turning though, it’s not in a direction favorable to telemarketers. Goodman said that “in July 2015, the FCC announced a new interpretation of the TCPA’s ‘autodialer’ standard that significantly expanded the definition and introduced a lot of unnecessary uncertainty as to what is and is not a regulated autodialer. That interpretation is currently being challenged in court. There’s a bit of a trend among courts requiring plaintiffs in autodialer cases to do more than simply allege that they were called with an autodialer. These courts, possibly in an effort to frustrate TCPA autodialer cases, are requiring plaintiffs to include circumstantial evidence of dialer use in their complaints: dead air, hang-up calls, generic messages, and so on. But the TCPA’s penalty structure still encourages suits that should not be brought.”

FCC Commissioner Ajit Pai, who was appointed by President Obama, voiced dissent to this new interpretation, echoing Goodman’s comments that it encourages frivolous suits.

An excerpt of Pai’s official dissent is below:

“Some lawyers go to ridiculous lengths to generate new TCPA business. They have asked family members, friends, and significant others to download calling, voicemail, and texting apps in order to sue the companies behind each app. Others have bought cheap, prepaid wireless phones so they can sue any business that calls them by accident. One man in California even hired staff to log every wrong-number call he received, issue demand letters to purported violators, and negotiate settlements. Only after he was the lead plaintiff in over 600 lawsuits did the courts finally agree that he was a “vexatious litigant.”

The common thread here is that in practice the TCPA has strayed far from its original purpose. And the FCC has the power to fix that. We could be taking aggressive enforcement action against those who violate the federal Do-Not-Call rules. We could be establishing a safe harbor so that carriers could block spoofed calls from overseas without fear of liability. And we could be shutting down the abusive lawsuits by closing the legal loopholes that trial lawyers have exploited to target legitimate communications between businesses and consumers.

Instead, the Order takes the opposite tack. Rather than focus on the illegal telemarketing calls that consumers really care about, the Order twists the law’s words even further to target useful communications between legitimate businesses and their customers. This Order will make abuse of the TCPA much, much easier. And the primary beneficiaries will be trial lawyers, not the American public.”

The FCC reviewed 19 individual petitions on the matter, some of which included relatively recent comments from the individuals we’ve mentioned so far. The appearance is that the FCC has collaborated with some individuals continuously over time or that individuals have collaborated continuously with the FCC. It might not matter though. Michael Goodman says that “the TCPA gives distinct enforcement rights to the FCC as well as persons who receive a call that violates the statute.”

“It isn’t really a matter of whether a particular violation should be handled by the FCC or privately,” Goodman adds. “Private plaintiffs have independent incentive to sue thanks to the TCPA’s penalty structure, and, compared to the FCC, private plaintiffs do not have to be as choosy in picking targets for actions.”

And what are the violations and penalties exactly? Goodman explained as follows:

“Depending on the specific TCPA provision at issue, private actions may be brought by individual consumers as well as businesses. The autodialer and prerecorded message provisions can be enforced by individuals and consumers, and they can sue based on a single improper call. For these provisions, the TCPA directs courts to award $500 per violation; courts do not have discretion to award a lesser figure. Courts do have discretion to award up to three times that amount (i.e., up to $1,500) per violation for willful or knowing violations. The TCPA’s do-not-call provisions are enforced by individual consumers, and this type of action requires more than one unlawful call in a 12-month period. For the do-not-call provisions, courts do have discretion to award less than $500 per violation (and can triple the penalty for willful or knowing violations).

The FCC has authority to obtain penalties of up to $16,000 per day of a continuing violation or per violation. FCC rules establish factors for the FCC to consider in calculating a proper penalty figure, including the nature of the violation, history of prior offenses, and ability to pay.”

“The base $500 per violation in statutory damages that consumers are entitled to hasn’t increased since the TCPA went into effect in 1992,” said activist Robert Braver. “This should be increased, especially since the TCPA does not allow for the recovery of attorney’s fees.”

Goodman said that private actions are much more common than FCC enforcement actions. That much is obvious. Private actions are becoming all too common in the small business financing industry where so many cases were uncovered through public records that we lacked the resources to follow them all.

More lawsuits might not be the cure though, according to Braver. He said that “more egregious telemarketing (massive robocall campaigns) should be criminalized on the federal level,” adding that “it’s one thing for an unscrupulous telemarketer to allow their shell corporation to have an uncollectible money judgment, but it’s another thing when individuals can wind up with a felony conviction on their records, and possible jail time.”

More lawsuits might not be the cure though, according to Braver. He said that “more egregious telemarketing (massive robocall campaigns) should be criminalized on the federal level,” adding that “it’s one thing for an unscrupulous telemarketer to allow their shell corporation to have an uncollectible money judgment, but it’s another thing when individuals can wind up with a felony conviction on their records, and possible jail time.”

While that suggestion might antagonize telemarketers, Braver said that his cell phone, which is listed on the Do-Not-Call-Registry, can receive as many as 4-5 telemarketing calls per day, generally robocalls.

Whether plaintiff allegations from cases in this industry are true or not, legal fees over TCPA cases have continued to be an expense that many small business financing companies are contending with. Those costs have a way of being tacked on to the price of financing for small businesses that need capital, making it a lose-lose situation.

One marketing company in the industry who had to remain anonymous because settlement negotiations at the time were likely to include a non-disclosure clause, posed the question, “how are you supposed to help small businesses if you can’t actually call small businesses?”

“More and more merchants are using their cell phone as their business phone,” he argued. “The TCPA regulations need to be changed so that a merchant can’t claim his cell phone is his business phone one minute and his personal phone the next.”

Indeed, the motivations, facts and alleged damages in TCPA complaints are not always clear. And even though the plaintiffs don’t always win, the laws as they are, can make telemarketing difficult no matter how careful one is.

Still dialing for dollars these days? Just know that some folks may be just a little too happy that you called them. And for all the wrong reasons.

Good luck out there.

Grandpa Breslow and What’s in the Deck for OnDeck

October 25, 2016At Money2020, Lendio CEO Brock Blake shared a joke that was made backstage about OnDeck’s CEO, Noah Breslow. “He’s the senior citizen of the industry,” he told a public audience, which referred to how long OnDeck has been around. It’s a label that Breslow lightheartedly embraced on an SMB lending panel he participated in on Tuesday morning.

Just a day earlier, deBanked met with executives from OnDeck, including Breslow to speak among other things, a collaborative initiative to codify business loan disclosures. APRs are among one metric they have recently agreed to display on their contracts, though in fairness they already did that on their line-of-credit product and on all of their loan products in Canada, the company asserted. While they don’t expect it will necessarily increase or reduce borrower interest, they believe that it may help a prospect make comparisons in what has become an increasingly competitive, yet fragmented market. “The use-case for the borrower isn’t changing,” Breslow said.

OnDeck will remain focused on small businesses as the customer and there are no plans to venture into mortgages or student loans like several of their counterparts in consumer lending. There’s also no plans to follow SoFi and integrate a dating feature into their mobile app. Instead their mobile app offers a frictionless experience for their existing line-of-credit customers to draw funds or make payments.

OnDeck will remain focused on small businesses as the customer and there are no plans to venture into mortgages or student loans like several of their counterparts in consumer lending. There’s also no plans to follow SoFi and integrate a dating feature into their mobile app. Instead their mobile app offers a frictionless experience for their existing line-of-credit customers to draw funds or make payments.

The JPMorgan Chase-OnDeck partnership is still in the “initial rollout,” according to Breslow, despite the deal being announced almost a year ago. Metrics such as the number of loans originated through the arrangement have not been disclosed, but for the record, it’s restricted to customers that are applying for a loan online, not those applying in person at a Chase branch.

On the SMB lending panel, Breslow and others asserted that their initiative to be more transparent is not about encouraging business lending to be regulated like consumer lending. “If we regulate commercial lending more like consumer, ultimately less capital is going to flow, when the goal should be to get more capital to flow,” he said. Wise words from an industry senior citizen.

A Glimpse into Square Capital’s Marketing

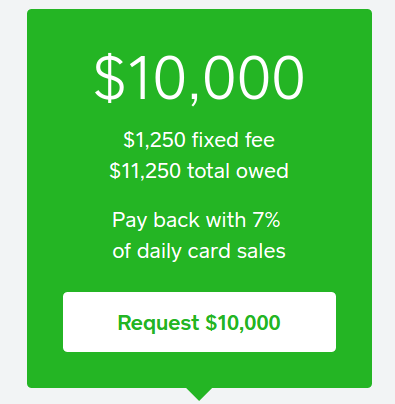

October 20, 2016As a merchant, Square has marketed their Square Capital program to me before. But this is the first time I’ve received direct mail marketing from them. Here’s a snapshot of what that looks like:

To view the potential offers, merchants are directed to log in to their Square accounts where they will see multiple terms. Even though their particular product is a loan made possible through Celtic Bank, all of the proposed loan offers are presented using the Total Cost of Capital method. That means cost is disclosed as a precise dollar amount so that potential borrowers will know exactly how much they will have to pay. Several studies have indicated that this is the easiest to understand, though it has been subject to some debate.

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

One of the defining features that makes Square Capital’s loan product different from a merchant cash advance or a purchase of future sales, is that Square enforces a fixed 18 month term. “If the loan hasn’t been repaid in full at the end of 18 months, the remaining loan balance will be due in full,” they state. That is completely unlike a purchase transaction in which there is no deadline or term. Even MCA purchase transactions that stipulate fixed daily payments do not actually have fixed terms. That’s usually because if a merchant’s sales activity rises or falls, they have the contractual right to request an adjustment to those payments to effectuate the basis of the agreement, that future sales be delivered in accordance with the unpredictable ebb and flow of business. That makes the date in which delivery will be satisfied in full unknowable. It’s that unknowable that can cause MCA transactions to be more expensive than their loan counterparts, though that is absolutely not always the case.

For Square, unknowable contract satisfaction dates likely made it difficult to bundle these deals up to sell off to institutional investors. Square Capital head Jackie Reses articulated this challenge during her appearance on an April 2016 LendIt stage. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date,” she said.

Even institutional investors recognize and understand that MCA purchase agreements do not have fixed terms.

Some Alternative Funders See Pot As Next Big Market Opportunity

October 17, 2016

For some funders, marijuana is not just about sewing their wild oats. Rather, they see the business potential of being early to what’s expected to be a highly profitable and long-lasting party.

Indeed, for the right type of funder, doling out money to marijuana-related businesses is a promising market—certainly in the short term because these companies are so capital-starved. Because marijuana is still classified by the feds as an illegal drug, many related businesses can’t even get a bank account much less access to bank loans or more traditional funding. Many alternative funders are also unwilling to lend to marijuana-related businesses, which has left a significant void that’s beginning to be filled by opportunistic private equity investors, venture capitalists and others.

Meanwhile, rapidly shifting public opinion and state-centered initiatives bode well for what many estimate is a multi-billion dollar market. Indeed, industry watchers say marijuana funding will eventually be an even stronger niche than lending to alcohol producers, tobacco companies or pharmaceuticals because of all the ancillary business opportunities related to medical marijuana use.

“I think it’s probably the biggest opportunity we’ve seen since the Internet,” says Steve Gormley, managing partner and chief executive at Seventh Point LLC, a Norwalk, Connecticut-based private equity firm that invests in the cannabis industry. “Consumption continues to grow and demand is there,” he notes.

“I think it’s probably the biggest opportunity we’ve seen since the Internet,” says Steve Gormley, managing partner and chief executive at Seventh Point LLC, a Norwalk, Connecticut-based private equity firm that invests in the cannabis industry. “Consumption continues to grow and demand is there,” he notes.

Despite shifting public opinion, legalized marijuana use is still quite controversial. So, all things considered, it takes a particularly thick-skinned funding company—one that has no moral objectives to marijuana and is also willing to accept a significant amount of legal, business and reputational risk—to throw its hat in the ring.

One of the biggest challenges keeping banks and many mainstream funders at bay is that cannabis remains illegal under law. Despite numerous attempts by proponents to scrap marijuana’s outlaw status, the DEA recently dealt out a significant blow by opting to maintain the status quo. This means that for the foreseeable future marijuana remains a Schedule I drug, on par with LSD and heroin, and as a result many lenders will choose to remain on the sidelines for now.

It remains promising, however, that over the past several years, the federal government has taken a more laissez-faire approach, giving individual states the authority to decide how they will deal with legalizing marijuana use. Forty-two states, the District of Columbia, and the U.S. territories of Puerto Rico and Guam have adopted laws recognizing marijuana’s medical value, according to the Marijuana Policy Project, an advocacy group. Four states—Alaska, Washington, Oregon, and Colorado—as well as the District of Columbia have gone even further. They allow the recreational use of marijuana for adults, with certain restrictions. Meanwhile, marijuana initiatives are on the November ballot in numerous states.

As these changes have percolated, forward-thinking alternative funders have been dipping their toes in the market—getting an early start on a market that’s hungrily looking for growth capital. “The last couple years there have been fewer investors than capital needed, but we believe that tide is changing,” says Morgan Paxhia, managing director and chief investor of Poseidon Asset Management LLC in San Francisco, an investment management company founded in 2013 to invest exclusively in the cannabis industry.

Paxhia says he’s starting to see more venture capitalists, lease-finance companies and private equity investors willing to provide liquidity to marijuana-based companies that are seeking to grow. The short-term cash advance marketplace, however, is not there yet. The challenge is finding funders willing to do the business with them.

“The people that are building these businesses have to always be worried about their cash. It’s not a given that they’ll get new additional investment,” Paxhia says. “Most people are quick to brush it aside. They won’t give it a minute to take a serious look at it and understand that it is already a multi-billion dollar market growing at 30 percent annualized for the next several years,”

A QUIETLY GROWING INDUSTRY

There are a number of private investors and venture capitalists who have spent the last several years researching and ramping up to invest in what they see as a goldmine of business opportunities. Many of these companies aren’t shy about publicly expressing their support for change.

“We see this as an opportunity of a lifetime to witness a societal change and we want to be a part of it,” says Paxhia who together with his sister runs a $10 million investment fund.

At the same time, there are also some alternative funders who dabble in this space and won’t discuss it publicly—partly because of the perceived stigma and partly out of concern that their financial backers won’t approve. To cover themselves, some are only willing to deal with companies that have hard assets. Often times the rates they offer are much higher than businesses in other industries with comparable financials would pay.

Andrew Vanam, founder of Rx Capital Funding LLC, an ISO in Norwalk, Connecticut, who focuses on the healthcare and medical industry, has helped a handful of few marijuana-related businesses get funding in the past few years and would love to help facilitate more deals. But he says it’s extremely difficult to find lenders that are willing to fund cannabis-related businesses as well as offer reasonable rates. Many of the files he generates in the cannabis space have incredible financials, positive cash flow, and month-on-month growth. However, lenders still treat these businesses as high-risk and offer rates so high it’s not even worth bringing back to a client. Instead, “they are taking hard money loans from private investors that put these cash advance offers to shame,” he says.

ASSESSING THE RISKS

ASSESSING THE RISKS

Certainly there are risks to funding marijuana businesses. In Colorado—one of the first states to legalize the recreational use of marijuana—values are getting lofty, and people are overpaying for properties that house marijuana-related businesses, notes Glen Weinberg, a partner in Fairview Commercial Lending, a hard-money lender with offices in Atlanta and Evergreen, Colorado.

Weinberg has financed between 75 and 100 commercial real estate loans where marijuana businesses were involved, but says recently he’s shied away. “I’m not comfortable with the valuations at a lot of these marijuana properties,” he says.

Even investors who are bullish on the space urge caution. “If you’re in a [nationwide] market that is growing at about 64 percent per year, that rising tide floats all boats, but there’s a lot of risk, so you have to be careful,” says Chet Billingsley, chief executive of Mentor Capital Inc., a public operating company in Ramona, California, which acquires and provides liquidity for medical and social use cannabis companies.

Billingsley says he has learned some hard lessons through his dealings with about nine marijuana-related companies. For example, he recently won a court judgment against a company that Mentor had supplied with millions of dollars in cash and stock. The company later balked at the terms of the deal and tried to renege, but Mentor ultimately prevailed in court. Still, Billingsley says Mentor went through many unnecessary hassles and racked up $300k in legal costs over the course of its two-and-a-half-year legal battle.

Many business owners in the marijuana space started out during a period when it w as completely illegal. Often these companies march to the beat of their own drum; to protect themselves, lenders need to do more than offer a standard funding contract and hope for the best, Billingsley says.

“The contract has to be solid and it has to be explained in detail to the marijuana operator who is often not sophisticated with regard to contracts.” If you leave things open to interpretation, you’re likely to end up in court, where anything can happen, he cautions.

Companies that fund cannabis businesses say they have very extensive vetting processes—so much so that they turn away a good portion of requests. Jeffrey Howard, managing partner of Salveo Capital in Chicago, says about two-thirds of the companies that come across his desk don’t make it past the company’s initial criteria. “We see a ton of companies and business plans from companies seeking capital to raise money,” he says. “We are going to be very selective about who we invest in and how much.”

Gormley, of Seventh Point, leverages all the same resources he would if he were buying any retail or production manufacturing outfit. He does extremely invasive vetting of the individuals involved and uses private detectives to help.

It many cases it comes down to the business’s management team, according to Paxhia of Poseidon Asset Management. “All the businesses are very early-stage and most companies have a very short track record, so you have to place a greater emphasis on the people,” he says.

OPPORTUNITIES ABOUND

Despite the risks, funders that work in the marijuana space say they are filling an important need by providing capital to marijuana-related businesses. For Gormley of Seventh Point, it’s a calculated risk in an area he’s been following for quite some time. “How often do you get to be part of history, and how often do you get to participate in a burgeoning market?” he says.

Industry participants stress the many funding opportunities aside from companies that cultivate and distribute the plant. Indeed, there are many ancillary businesses that provide products and services geared towards patients and cannabis users without having anything to do with the actual plant.

Howard of Salveo Capital, says his company is gearing up to provide private equity and venture capital to several marijuana-related businesses through its Salveo Fund I and will only make select investments into companies that “touch the plant.” The goal is to eventually have $25 million of committed capital to invest in multiple early-stage companies that offer ancillary products and services to the marijuana industry. “We think there’s more exciting opportunities than ‘touch the plant’ investments,” he says.

Crowdfunding platforms are another avenue for companies in the marijuana space. This type of funding hasn’t yet been utilized to its full potential, industry watchers say.

Eaze Solutions, a San Francisco-based provider of technology that optimizes medical marijuana delivery, is one example of a company that turned to crowdfunding. It raised part of a $1.5 million infusion to fund its expansion via the crowdfunding site AngelList in 2014. Loto Labs, in Redwood City, California, is another example. It raised more than $220k via Indiegogo to fund production of its Evoke vaporizer. There’s also CannaFundr, an online investment marketplace for companies in the cannabis industry to gain access to capital.

Seth Yakatan, co-founder of Katan Associates in Hermosa Beach, California, suggests that crowdfunding will become more of an option for certain types of cannabis based companies, specifically those that aren’t as closely tied to the actual production of the plant. “Until federal regulations change, it’s going to be hard to raise money for an entity where you are actively engaged in the cultivation, distribution or sales of a product that’s federally illegal,” says Yakatan, whose company invests in and advises cannabis-related companies that have a biotech or pharmaceutical orientation.

Seth Yakatan, co-founder of Katan Associates in Hermosa Beach, California, suggests that crowdfunding will become more of an option for certain types of cannabis based companies, specifically those that aren’t as closely tied to the actual production of the plant. “Until federal regulations change, it’s going to be hard to raise money for an entity where you are actively engaged in the cultivation, distribution or sales of a product that’s federally illegal,” says Yakatan, whose company invests in and advises cannabis-related companies that have a biotech or pharmaceutical orientation.

Because laws on legalized marijuana are still in limbo, industry watchers say the market is still many years away from being mainstream. “Public perception will be similar to alcohol in 10 years from now,” predicts Weinberg of Fairview Commercial Lending, adding that he expects banks to enter the funding arena in five to 10 years.

In the meantime, alternative funders who can stomach risk continue to pave the path for others. Howard of Salveo Capital expects private equity investors, venture capitalists and other alternative players to continue playing a big role in getting the nascent industry off the ground.

“I strongly believe that in the interim there’s a significant advantage for players like us to be funding and to be in on the ground floor of this industry before it changes,” Howard says.

Indeed, many alternative funders believe the potential upside significantly outweighs possible negative consequences. “The perceived risk at this point is far greater than the actual risk,” says Paxhia of Poseidon Asset Management.

Secretary Clinton Spoke About Small Business Lending in Goldman Sachs Speech, Wikileaks Reveals

October 16, 2016 On October 29th, 2013, former Secretary of State Hillary Clinton said that one of the biggest complaints she gets as she travels around the country is “how do we get more access to credit in today’s current system for small businesses?” This comment was made at a private Goldman Sachs event hosted at the Ritz-Carlton Dove Mountain in Marana, Arizona, according to a transcript published by Wikileaks.

On October 29th, 2013, former Secretary of State Hillary Clinton said that one of the biggest complaints she gets as she travels around the country is “how do we get more access to credit in today’s current system for small businesses?” This comment was made at a private Goldman Sachs event hosted at the Ritz-Carlton Dove Mountain in Marana, Arizona, according to a transcript published by Wikileaks.

As a contender to become the President-elect in just a few weeks, she appears to understand that small businesses lack access to capital and the shortcomings of the current system. Transcript excerpt below:

ATTENDEE: Secretary Clinton, I’m Patty Greene from Boston College’s Goldman Sachs 10,000 Small Businesses. And first off, thank you for all the work you’ve done with women entrepreneurs both domestically and globally over your career. That’s really meant a lot.

My question is more domestic based. We have the rather unusually organized Small Business Administration, we have the Department of Commerce, and we have programs for entrepreneurs with small business pretty much scattered across every single other agency. How do you see this coming together to really have more of a federal policy or approach to entrepreneurship and small businesses?

SECRETARY CLINTON: I would welcome your suggestions about that because I think the 10,000 Small Business Program should give you an opportunity to gather a lot of data about what works and what doesn’t work. Look, neither our Congress nor our executive branch are organized for the 21st Century. We are organized to be lean and fast and productive. And I’m not — I’m not naive about this. It’s hard to change institutions no matter who they are. Even big businesses in our country are facing competition, and they’re not being as flexible and quick to respond as they need to be.

So I know it wouldn’t be an easy task, but I think we should take a look at how we could, you know, better streamline the sources of support for small businesses because it still remains essential. You know, one of the things that I would love to get some advice coming out of the 10,000 Small Businesses about is how do we get more access to credit in today’s current system for small businesses, growing businesses, because that’s one of the biggest complaints I hear everywhere as I travel around the country. People who just feel that they’ve got nowhere to go, and they don’t know how to work the federal system. Even if they do, they don’t feel like they’ve got a lot of opportunities there. So we do — this is something we need to look at.

You know, I don’t think — I don’t think our credit access system is up to the task right now that is needed. I mean, there are a lot of people who would start or grow businesses even in this economic climate who feel either shut out or limited in what they’re able to do. So we need to be smarter about both private and public financing for small businesses.

—

More recently, Clinton’s campaign has publicly stated that she wants to “harness the potential of online lending platforms and work to safeguard against unfair and deceptive lending practices.”

UK Banks Will No Longer Be Allowed to Decline Small Businesses For Loans as Alt Lending Wins

October 10, 2016UK Banks better have a strong reason to turn down loan applicants, and if not, turn them over to another lender.

In an attempt to break the might of the big banks and back the thriving alternative finance industry, the UK Treasury will make it obligatory for banks to refer rejected small businesses to other lenders. Nine of the country’s largest banks including Royal Bank of Scotland, Lloyds, Barclays and HSBC will be legally obligated to do so when the plan goes into effect in the next three months, The Times reported.

The applicants will be referred to three loan marketplaces — Funding Options, Funding Xchange and Bizfitech that will make referral fees for loans funded on their platforms.

Online lending across the pond operates differently. The UK online alternative finance sector grew 84 percent in 2015, with support from the government and was one of the first countries to establish a regulatory framework where The Financial Conduct Authority (FCA) defines and categorizes crowdfunding, P2P lending and online lending. The UK is home to many early starters in the industry like Zopa and RateSetter.