Business Lending

ForwardLine, One of the Original Funding Companies, is Back

June 5, 2019 Steve Carlson, CEO, ForwardLine

Steve Carlson, CEO, ForwardLineForwardLine Financial originated well over $65 million in loans in 2018, according to CEO Steve Carlson. ForwardLine would not share its origination numbers, but Carlson said the company is comfortably on the deBanked list of top originators. ($65 million is the lowest origination number on the list).

Last week, the company announced that it secured a $100 million credit facility from Credit Suisse AG and Neuberger Berman private equity funds. This is the company’s largest credit facility to date. Its previous credit facility was with East West Bank and that relationship is still in place.

ForwardLine is a direct marketer that provides working capital loans of up to $200,000 to small businesses.

Carlson told deBanked that ForwardLine, which was founded in 2003, has been scaling its business dramatically over the past year and a half. This is no coincidence. Instead, Carlson said this is the result of years worth of planning following a majority investment in ForwardLine in 2015 by a private equity firm called Vistria Group.

“We spent 2016 and 2017 very thoughtfully building out a technology platform, a data infrastructure, and a management team to scale the business,” Carlson said. “We’re now actioning on that plan. So this is all part of a multi-year strategy.”

A company statement said that the company’s loan performance in 2018 was record-breaking. ForwardLine increased year-over-year total originations by over 300% in the first quarter of 2019.

Carlson said that the new facility will be used primarily to grow the business. ForwardLine is located in Woodland Hills, CA, and it employs 110 people, more than half of whom work in the sales department. Other employees include underwriters and data and analytics people.

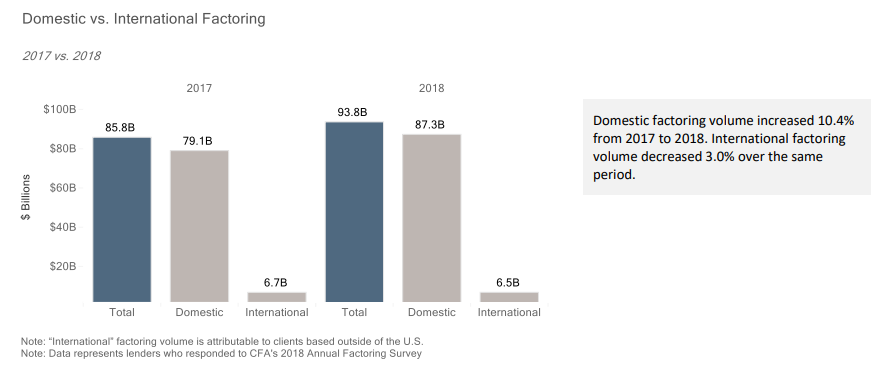

CFA Report Shows Increase in US Factoring Volume

May 30, 2019The Commercial Finance Association (CFA) recently published a report on asset-based lending and factoring which showed a 10.4 % increase in domestic factoring volume in 2018 compared to 2017. While the increase isn’t enormous, it is consistent with a gradual growth in factoring, according to Jeff Goldrich, CEO at Princeton, NJ-based North Mill Capital, which provides invoice factoring.

“It’s not a hockey stick, it’s gradual growth,” Goldrich said.

Goldrich attributed the growth, albeit moderate, to two factors. One is that, while not everywhere, he said there’s been some tightening of credit with banks, which leads companies to consider factoring.

The other is that he said large sized companies are increasingly using factoring as a financing option. While factoring is generally more expensive than taking out a bank loan, companies don’t have to worry about having stellar financial history because factors are less concerned with the financial health of the borrower and more concerned with the strength of the receivable.

Another finding in the CFA report is that Recourse factoring increased by roughly 11% in 2018 compared to 2017. Recourse factoring is when a factor has recourse if a company fails and is unable to pay a receivable to a factor’s client, according to Harvey Gross, Executive Director of the New York Institute of Credit. This is unlike the more common Non-Recourse factoring, where the factor can do nothing if the company that the owes the receivable goes out of business. Gross says that Recourse factoring is becoming more common as factors don’t want to take on as much risk.

Gross said that the older, traditional factors (which often cater to the apparel and toy industries, for example) are still Non-Recourse factors. They shoulder the loss if a company can’t pay its invoices. But at the same time, Gross said that these factors want clients with a large volume of invoices and invoices from solid companies.

BlueVine is one of the few companies that offers factoring online, where a company can get funded online without first interacting with a company representative.

“I see a continuation of factoring marrying fintech,” Goldrich said. “That’s where the big backers have interest.”

Funding These Franchises? Read This First

May 29, 2019

United States Senator Catherine Cortez Masto is concerned with the abilities of four major franchises to repay business loans, according to a letter penned to the Small Business Administration. They include Subway, Complete Nutrition, Dickey’s Barbecue, and Experimac. The issues raised should be on the radar of every provider of capital.

For Subway, Cortez Masto cites a New York Post article that alleged Subway Restaurants is plotting to put its own franchisees out of business through the enforcement of minor handbook violations. A whopping 1,108 Subway stores closed last year alone.

For Complete Nutrition, the franchisor is reportedly dismantling its own franchise. Cortez Masto says it first raised the prices of goods, wiping out franchisee profit margins. Following that, it eliminated its franchise model altogether, took away their franchisees’ POS systems, removed their locations from the Complete Nutrition website, and informed Complete Nutrition customers that the stores had been sold and to order online going forward instead of from the stores. At least 12% of SBA loans made to Complete Nutrition locations have been charged off.

For Dickey’s Barbecue, the franchise is experiencing more stores closing than opening. Cortez Masto suspects that the franchisor is providing misleading and inaccurate information to potential franchisees, resulting in failed stores and bankrupt business owners. A franchise blogger says, “The Dickey’s business model seems odd, continually selling new franchises to replace closed units, but seemingly doing little to fix the profit structure so existing franchisees survive.”

For Experimac, Cortez Masto says that most of the SBA loans made to Experimac were originated by Celtic Bank and that to-date 23% of these loans have failed.

Canadian Alternative Finance Event Calendar

May 28, 2019Here’s what’s on the agenda this Summer for the Canadian alternative finance industry:

June 5th

Credit Invisibles Summit – Presented by the Canadian Lenders Association

July 25th

deBanked CONNECT Toronto – Presented by deBanked

Jonathan Braun Sentenced to 10 Years

May 28, 2019

Jonathan Braun, who Bloomberg Businessweek profiled in a merchant cash advance story series, was sentenced to 10 years for drug related offenses this morning at the federal courthouse in Brooklyn. He will get credit for 17 months previously served in 2010 – 2011. He is scheduled to surrender on August 25th.

Prior to the judge’s order, Braun was given an opportunity to speak and proclaimed himself a changed man. The judge took many things into consideration including letters supporting Braun’s transformation as well as some new lawsuits and allegations that cast him in a negative light. Nevertheless, the judge explained that no new charges had been brought against Braun since he pleaded guilty 8 years ago. The 10-year sentence was the mandatory minimum.

Does The Borrower Even Exist? Image Algorithms, Site Inspectors Spot The Fakers

May 24, 2019 Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Most of the pictures were genuine, but the microscope was not. Truepic, a virtual site inspection and photo verification company that the lender had relied on, algorithmically determined that the microscope was actually a photo of a photo, one that had been grabbed off the web.

If they had just emailed these photos directly to the lender, the loan would’ve been issued, but this image analyzing technology changed everything.

Truepic founder and COO Craig Stack said that they were able to identify the false ones because of software they have that can detect when a photo is being taken of a two-dimensional image. Truepic didn’t just obtain the photos, they were taken in real time using their mobile photo-taking app. In addition to detecting only two dimensions, Truepic also found the real photos online through a reverse-image search to show where the photos came from.

Photo verification isn’t brand new. Nationwide Management Services has been providing these very same services to their customers since 2015, according to its CEO John Marsh. Marsh started his company in 2005 and originally provided traditional on-site inspections with certified field agents taking pictures.

“You can’t tell the difference,” Marsh said of photos taken by a field agent, compared to those taken virtually by the owner of the store or office. In the virtual one, the merchant receives a text and clicks on a link that essentially turns the merchant’s phone into a live video feed for the lender.

Commonly, the lender wants to see, among other things, the company’s signage, credit card machine and merchant’s driver’s license. Using GPS technology, Nationwide Management Services can tell exactly where the merchant is, so they can’t be taking photos – in real time – of a different store.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh’s virtual video verification product is instantaneous, allowing the lender to see the merchant’s space – and face – in real time, virtually eliminating misrepresentation of the merchant’s store. Stack said that Truepic also has a video verification product that they will be releasing in less than three weeks.

Marsh said that would-be merchant fraudsters get scared as soon as they hear about a real time virtual inspection.

“When we reach out to them for the virtual inspection, they go dark,” Marsh said.

Most of the deception Marsh has encountered is of merchants giving a P.O. Box address as the address of their “physical store.”

Gayle Juhl, President and CEO of Metro Inspections, said that one of her field agents found a merchant with a far more unusual distortion of its company address. The field agent went to the address of the merchant only to find a 1970s bright blue Volvo station wagon with a sign on it, parked in front of the address listed, which belonged to a completely different store.

The man seeking funding, who came out of the car-turned-store, was apparently confrontational, according to the field agent’s report.

Juhl said that she will coordinate a virtual inspection upon request, but that her company primarily does onsite inspections.

“You can’t replace a handshake and an eye-to-eye to see what’s really going on,” Juhl said.

This may be true, but Marsh said that it can take 24 to 48 hours to collect photos for his onsite inspections whereas it can take as little as four minutes with his virtual video or virtual photo services. (This depends on how many images the lender is looking to capture.) Granted, Juhl said that Metro Inspections’ on-site inspections can be collected and delivered on the same day it was requested, given that the request comes early enough in the day.

Stack, who has only been servicing the online lending industry for about five months, says that he has gotten financial services clients who are very excited about the speed of virtual inspections and the fact that they are far less invasive for the merchant. Rather than have a stranger come in to take pictures – raising questions among employees and customers – the business owner can discreetly photograph their space at their convenience. Stack’s company has never offered onsite inspections and says he never will.

“Our camera doesn’t lie,” he said.

Lawyers: Earn CLE Credits While Learning About Alternative Finance

May 23, 2019

| June 13 Sessions | June 14 Sessions |

| Case Law Updates | Regulatory Download: The Complete Picture |

| TCPA: Defining ATDS, Exploring the TCPA and How Emails are Covered | Legislation, Business and Lobbying: How does it work and Does it work at all? |

| Bankruptcy Updates | Future Invoice Factoring and Traditional Factoring: Can’t We All Just Get Along? |

| Securities: A Lesson from Bitcoin and Recent Industry Case Law | Clean Contracts: Merchant Agreements, Inter-Creditor Agreements and ISO Agreements: What you MUST know to keep up with the times |

| Inside the UCC with Bob Zadek | |

| Collections in a Post Bloomberg World | |

| Ethics: Conflicts of Interest | |

| *Evening Social event at Lucky Strike in Manhattan Food, drinks and bowling! 7:00pm – 9:00pm* | *Rooftop Cocktail Reception, Castell Rooftop Lounge 3:00pm – 5:00pm* |

Admission Price List:

Admission for Members: $75

2-Day Ticket Includes:

- Day One: breakfast and lunch during the full day of panels. Evening at Lucky Strike with food and drinks.

- Day Two : Three panel discussions, lunch and cocktail hour immediately to follow.

Non-Member Attorneys $250.00 for the 2 day ticket

Non-Member Attorneys $150.00 for a 1 day ticket

(may only attend one of the two days.)

Corporate Guests (Day Two only) $150.00

Featuring the Following Speakers:

- Christopher Murray, Esq.

- Patrick Siegfried, Esq.

- William Molinski, Esq.

- Natalie Nahabet, Esq.

- David Fuad, Esq.

- Kate Fisher, Esq.

- Jamie Polon, Esq.

- Thomas Telesca, Esq.

- Richard J. Zack, Esq.

- Robert Zadek, Esq.

- Richard Simon, Esq.

- Anthony Giuliano, Esq.

- Mark Dabertin, Esq.

- Gregory Nowak, Esq.

Email Lindsey Rohan: lindsey@lrohanlaw.com

BFS Capital Joins ILPA

May 23, 2019

The Innovation Lending Platform Association (ILPA), a group of online small business financing and service companies, announced today the addition of BFS Capital. ILPA is known for creating the Straightforward Metrics Around Rate and Total Cost (SMART) Box.

“We believe that transparency matters,” Ruddock told deBanked.

“BFS Capital is committed to being both a responsible and an innovative lender,” Ruddock said. “Our membership in the ILPA allows us to work with industry leaders who are dedicated to advancing standards and best practices in the critical small business lending marketplace… [and] we believe that clarity and transparency is critical in helping [small businesses] make educated and informed financial decisions.”

As a new member of ILPA, BFS will join current members including OnDeck, Kabbage, BlueVine and 6th Avenue Capital.

“We applaud Mulligan Funding and BFS Capital for committing to adopt fair and transparent disclosure best practices to ensure small businesses are well informed when seeking funding,” said ILPA CEO Scott Stewart. (ILPA announced that Mulligan Funding has joined the association as well).

BFS is also a member of the Small Business Finance Association (SBFA) and Ruddock told deBanked that BFS will remain a member of that trade association as well.

Separately, BFS announced today that it has named Fred Kauber as the company’s new Chief Technology Officer and Chief Product Officer. Kauber was previously with fintech marketplace platform CAIS Group and he served in senior roles at First Data, Dun & Bradstreet and IBM.

“I’m confident that Fred is the right person to advance both our vision and our capabilities [at BFS,]” Ruddock said.