Business Lending

An Amazon Capital Lending Loan

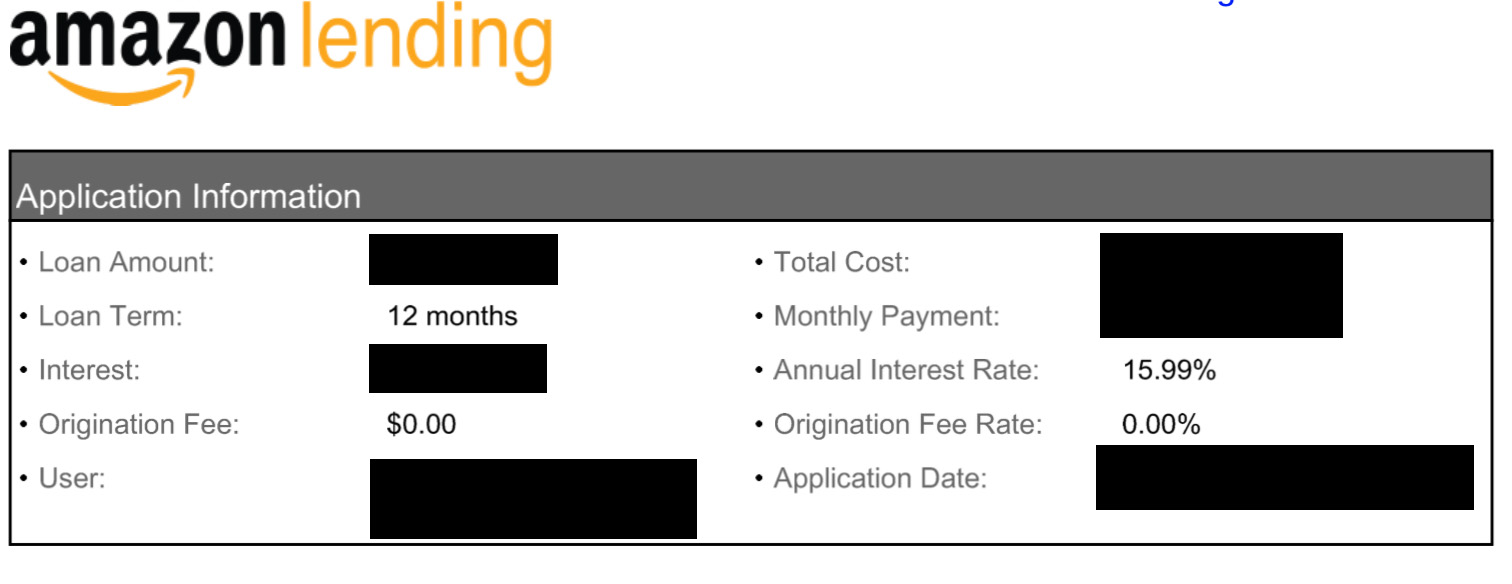

February 2, 2021Amazon’s small business lending business is no small operation. deBanked recently viewed a loan agreement between Amazon Lending and an Amazon seller in which the seller received a loan of $300,000 at an annual interest rate of 15.99%.

In 2019, we estimated that the company had originated $1.5B in small business loans, placing them in the #5 slot on our list, but the company is possibly on track to be #1.

Double Dipped: What’s Next For New York’s Small Business ‘Truth in Lending’ Act

January 11, 2021 Last year, when the Small Business ‘Truth in the Lending’ bill came through the New York State Senate Banking Committee, Senator George M. Borrello said he and other members went to work. Their job: to write a version everyone would like, which fell apart when the bill passed in July and it was signed into law just before Christmas.

Last year, when the Small Business ‘Truth in the Lending’ bill came through the New York State Senate Banking Committee, Senator George M. Borrello said he and other members went to work. Their job: to write a version everyone would like, which fell apart when the bill passed in July and it was signed into law just before Christmas.

“I’m a small business owner myself, but I also come from local government, and in local government, the committee is where the work gets done,” Borrello said. “We had the opportunity to fix this in committee. By the time it got to the floor, the governor basically reversed all the things I presented that were flaws, and he signed it.”

That’s the story of how S5470B came to be in Albany. Instead of ironing out the kinks in committee, Borrello said he watched as the bill with all its problems passed over the summer. There was a process to clean it up afterwards to make it suitable for Governor Andrew Cuomo’s signature, since it’s said that even he himself had expressed reservations about the language. But then he signed the original version and all the edits were discarded.

Politics are suspected to have played a role in that.

Politics are suspected to have played a role in that.

“When the governor finds something is flawed, he usually vetoes and sends it back,” Borrello said. “It concerns me that there is an underlying political angle that has nothing to do with the Truth in Lending.”

Steve Denis, the executive director of the Small Business Finance Association, said that he doesn’t think that the signed bill that is up on the state senate website will be the final version.

“It is so poorly drafted that even companies that support the bill have liability and will be the first to get sued,” Denis said. “The SBFA will be a lot more aggressive; the legislature has a lot to work on in the next session. It has been a wake-up call, unifying the industry. We will be more aggressive to create a more favorable version.”

Denis has attested to the harm the bill will do to the SMB finance industry in New York, costing billions of dollars in fines and litigation. He pointed out that major companies like PayPal have fought against the bill, and the proponents “recognized it was not a good bill, but passed it to fix it.”

Borrello said that it is common in Albany to encounter legislation written by lawmakers who don’t understand small business owners who deal with regulation every day. Borrello and his wife worked in the hospitality business for years before going into public service. Borello said he feels business owners’ pain during the pandemic, especially in the restaurant and hotel industry.

He said the end result of this new bill when it comes into effect this July: funding and lending companies will stop providing services in New York State, directly harming the small businesses the bill claims to help.

“One of my frustrations, being on the banking committee, is that we do things that ultimately make it more difficult for people to access credit and financing in New York State,” Borrello said. “You’re talking about small businesses that are already hurting, having financial difficulties accessing lines of credit. This disclosure law passing during this pandemic is one more nail in the coffin for small business.”

The Legislature, the Governor, and the Department of Financial Services (DFS) all reportedly had issues with the bill: yet it passed. Borrello said a problem with “nonsense lawmaking” comes from competition with other states. New York compares itself with California to “prove we’re the most progressive.” Borrello also pointed out that California passed its version of a lending disclosure bill more than two years ago, and their version of the DFS still cannot find a way to calculate an APR metric for factoring or MCA.

The Legislature, the Governor, and the Department of Financial Services (DFS) all reportedly had issues with the bill: yet it passed. Borrello said a problem with “nonsense lawmaking” comes from competition with other states. New York compares itself with California to “prove we’re the most progressive.” Borrello also pointed out that California passed its version of a lending disclosure bill more than two years ago, and their version of the DFS still cannot find a way to calculate an APR metric for factoring or MCA.

As the bill was argued on the legislative floor, Borrello brought up the controversial “double-dipping” term that had been inserted in the language. Borrello came to the same conclusion as Denis, that there is no double-dipping term: It was just conjured up for the bill to sound scary, negative, and damaging.

“Other than talking about potato chips, I’m not sure what you’re talking about,” Borrello said. “When you haven’t defined it, in the legislature, it comes down to a political talking point and dog whistle. You enshrine a rather vague piece of jargon in the legislation, and it shows how deeply flawed it is.”

Borrello now plans to work with the Governor, DFS, and legislature to amend and change the bill. He is also fighting for a Republican banking overhaul to provide further credit access to small businesses.

“The next step now is to go back and see what needs to be fixed,” Borrello said. “Hopefully, my role now as the ranking member of the banking committee, we can have a common-sense conversation about how to actually fix it.”

Lendio Starts Funding Engines, PPP is On The Way

December 30, 2020 President Trump officially signed the economic relief package Sunday night. While the House, President, and Senate can’t agree on the checks individual Americans will get from Uncle Sam, $284 billion for PPP is on the way.

President Trump officially signed the economic relief package Sunday night. While the House, President, and Senate can’t agree on the checks individual Americans will get from Uncle Sam, $284 billion for PPP is on the way.

In preparation, Lendio, an online loan marketplace that facilitated $8 billion in PPP funds over the summer, has already opened the application floodgates. But when is the bill landing?

“The SBA has ten days from the time it was signed into law, January sixth, when they have to give guidance,” Lendio CEO Brock Blake said. “Then, they have some time after that they’ll open it up, my guess is that it will likely go live somewhere between the 10th to 15th.”

Firms, start your funding engines; the money is coming in about two weeks. And Blake said that with the demand for capital this high—the funds would go quick.

“My guess is that it will be two to three weeks, maybe a little longer,” Blake said. “One of the reasons it will last a little bit longer is because they reduced the loan maximum size from ten million to two million. As a result, two to three weeks or more like, you know, three or four.”

Lawmakers initiated limits to the high end this time around to halt concerns that “small business” bailout money was going to larger sized firms. That isn’t the only change for what some say could be the final round of government stimulus.

“I like what they’ve done this time around, addressing some of the key issues, first of which allowing borrowers to have a second turn on PPP loans,” Blake said. “This pandemic has lasted longer than anyone expected, and there’s a lot of restrictions on these business owners.”

The first time around, the Fed handed out forgivable funds based on two and a half months of payroll, and that went real quick, Blake said. For a firm to meet the criteria for a second loan, they have to prove they have a 25% reduction in revenue from 2019 to 2020.

Blake said he was excited that the new aid is granting industries especially hard hit, like restaurants and hotels, to get larger loans “three and a half time instead of two and a half times.” Blake’s favorite part of the new program is incentivizing lenders to serve genuine smaller businesses, where last time they were not.

“Last time, so many of the smallest small businesses were at a disadvantage because we all know lenders prioritize the largest loan sizes first,” Blake said. “They left the smallest of small business out.”

Lendio and fintech lenders focused on this underserved market of small businesses last time, Blake said. After advocating on behalf of small borrowers, Blake said there are incentives for lenders to give to the underserved and actually make money.

“Thankfully, in this new PPP program, they created a new incentive package for loans smaller than $50,000,” Blake said. “That makes these smaller loans a priority, instead of put toward the back of the list.”

Ho Ho… Hold Up. NY Governor Signs Industry-Altering Small Business Lending Law

December 24, 2020 Merrrrry Christmas. New York Governor Andrew Cuomo reportedly signed SB 5470 into law late last night, a bill that forever changes and complicates nearly all forms of small business financing in the state.

Merrrrry Christmas. New York Governor Andrew Cuomo reportedly signed SB 5470 into law late last night, a bill that forever changes and complicates nearly all forms of small business financing in the state.

The law gives regulatory enforcement authority to New York’s Department of Financial Services, requires APR disclosures on contracts where one can’t be mathematically calculated, and mandates that customers be told if there is any “double dipping” going on. And that’s just the beginning of what it contains.

A coalition of small business capital providers fiercely opposed the language of the bill. Steve Denis, executive director of the Small Business Finance Association, wrote in an op-ed that “the lack of cogency and lazy approach to this legislation is a disservice to the hard-working entrepreneurs who continue to open their businesses while facing daily economic uncertainty.”

The bill was also opposed by fintech lenders like PayPal.

Proponents of the bill celebrated the news on social media in the early morning hours of Christmas Eve.

Ryan Metcalf at Funding Circle, a company not even based in New York that moved all of its tech jobs out of the US to the UK this summer, wrote on LinkedIn that the bill will “save New York #smallbiz between $369 million and $1.75 billion annually.” Funding Circle, as a member of the Responsible Business Lending Coalition (RBLC), was heavily engaged in the advocacy process.

Several of RBLC’s members have already ceased small business lending in the US, some permanently.

Unique circumstances also exist at an ally of the RBLC, the Innovative Lending Platform Association (ILPA), which Funding Circle is also a member of. Two out of the 11 members were acquired before the bill could even be signed, Kabbage and OnDeck.

NY State Assemblyman Ken Zebrowski and State Senator Kevin Thomas, who sponsored the bill, cheered the signing of it.

“Thanks to Governor Cuomo for signing our Small Business Truth in Lending Act,” Zebrowski tweeted. “Extremely proud to have worked with many to establish the most comprehensive small business disclosure law in the nation. With the pandemic surging on, small biz owners need these critical protections now.”

“The signing of the New York State Small Business Truth in Lending Act is a victory for New York’s small business owners,” Thomas wrote on twitter. “Thank you for signing New York’s first-ever small business lending transparency bill into law.”

“I think that the companies and organizations that support this legislation don’t fully understand what’s actually in the bill,” SBFA’s Steve Denis said to deBanked in August. “[…] They have no problem pounding the table and taking credit for its passage, but I guess they don’t realize it will subject them and the rest of the alternative finance industry to massive liability, massive fines—upwards of billions of dollars worth of fines.”

And yet Senator Thomas tweeted, “This will help a lot of small businesses trying to get back on their feet during this pandemic.”

It is unclear, of course, who they expect to provide such capital now to do this.

Failing Main Street NY

December 21, 2020 During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

The struggle between understanding and posturing is on display right now in Albany. While small business owners struggle to open their doors, the legislature passed a so-called “truth in lending for small business” bill that claims to provide more disclosure to business owners seeking financing. Led by Senator Kevin Thomas and Assemblyman Ken Zebrowski the bill is currently pending before Governor Cuomo. The legislators recently authored an op-ed that further demonstrates their failure to recognize that the innocuously named bill is rife with faults and lacks a competent grasp of small business issues. The critical blind spots in the bill’s design threatens billions of dollars in capital leaving New York—a failing small businesses owners can scarcely afford at such a difficult time.

Yet, rather than incentivizing finance providers to stay in New York, the legislature is focused on complex disclosures that lack real meaning or understanding to small business owners. Senator Thomas opined on the Senate floor “… the reason I introduced this bill is because people don’t use standard terminology.” Interestingly, this bill creates several new terms and metrics that would be required to be disclosed that have never been used before in finance. Terms like “double-dipping” and new confusing metrics that even the CFPB under President Obama labeled as “confusing and misleading” to consumers. This bill’s fatal flaw is that it has confused information volume with transparency, somethings a recent study proved would harm small business owners.

Even Senator Thomas acknowledged the legislation’s myriad of problems while still encouraging its passage. In his colloquy with Senator George Borrello on the Senate floor, right before he called New York small business owners “unsophisticated,” he mentioned how his bill had “many issues” that he “hoped” would be worked out before implementation. Hope is not a strategy and it won’t help small business owners obtain the financing they need to stay in businesses. Advancing legislation that would limit options for entrepreneurs working to stay in businesses during a pandemic that has crippled the New York economy represents a reprehensible failure of leadership.

Minority-owned businesses have faced a disproportionate economic impact from the pandemic. According to the Fed, Black-owned businesses have declined by 41% since February, compared to only 17% of white owned businesses. Further, the Paycheck Protection Program (PPP), the federal government’s signature relief program for small businesses, has left significant coverage gaps: these loans reached only 20% of eligible firms in states with the highest densities of minority-owned firms, and in counties with the densest minority-owned business activity, coverage rates were typically lower than 20%. Specific to New York, only 7% of firms in the Bronx and 11% in Queens received PPP loans. Moreover, less than 10% of minority-owned businesses have a traditional banking relationship—something that was initially required to have access to the PPP.

The lack of cogency and lazy approach to this legislation is a disservice to the hard-working entrepreneurs who continue to open their businesses while facing daily economic uncertainty. Governor Cuomo has worked tirelessly to continue to provide economic relief to both businesses and consumers—removing billions in financing for small businesses will only hinder this effort. New York can do better.

Steve Denis

Executive Director

Small Business Finance Association

Aspiria Co-Founder On Successful Funding in Mexican SME Space: Still Lots of Room to Grow

December 5, 2020 After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

Aspria, Hernandez’s online lending firm, had planned on completing a Series A from international investor Oikocredit, but the deal went into the icebox as the cases came.

“In the beginning of the year, things were doing very well in Mexico, the whole economy was booming,” Hernandez said. “Out of nowhere, we got hit by the pandemic. And the transaction that we were supposed to be closing in March 2020, our investor said, ‘you guys are fantastic, but there are too many unknowns.'”

But due to Aspiria’s resilience and the fact that they went into 2020 with a rock-solid business, Hernandez said Oikocredit decided to complete the investment deal. Aspiria was growing and profitable, and though it was unclear if the markets were going to fall apart, Hernandez said he and his team put the nose to the grindstone and worked through it.

Oikocredit is a worldwide cooperative that provides loans and investments to promote financial inclusion while empowering people by improving livelihoods. That vision is what Aspiria aims to accomplish as an SME lender, Hernandez said, helping businesses access funds to grow.

The Mexican financial space has ample room for growth, and Hernandez said Aspiria is one of the first alternative business lending firms to capture the market.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

“The whole financial services industry, I mean it’s light-years behind the US,” Hernandez said. “I saw that the way that people would do the underwriting, the way that people provided financing for small businesses was just so outdated; it was more of an old school market here. I decided there was this huge opportunity for the market.”

For example, Mexico has a third of the US population, but only 30 banks to the 7,000-10,000 the US has. That population is also a younger demographic than up north. In Mexico, the average age is 27 (It’s 38 in the US); Hernandez said: the Average Mexican is trying to establish themselves and reach the middle class, young, educated, and ready to start a business.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

“It was my first exposure to technology, and I was completely amazed. I fell in love with it,” Hernandez said. “At that moment, I was actually thinking about changing careers. I was completely fed up with financial services because it’s boring sometimes. I thought it was not sexy anymore.”

Co-founding Aspiria, Hernandez went on to become the major funder in the space. He said there is so much demand for capital in a standard year that his firm can see 100% year-over-year growth. Even in a pandemic, his firm received a confident investment that will go directly toward building the shop, scaling up funding, hiring, and aiming toward a firm that will one day put it on par with the rest of North America’s leading alternative finance firms.

Why The PPP and EIDL Data Got Dumped

December 3, 2020 The SBA’s time has run out: on Tuesday night, the organization released the loan data for all Paycheck Protection Program (PPP) recipients. The name, address, and how much each recipient received was posted in a series of excel spreadsheets in compliance with a D.C. District Court order, decided November 24.

The SBA’s time has run out: on Tuesday night, the organization released the loan data for all Paycheck Protection Program (PPP) recipients. The name, address, and how much each recipient received was posted in a series of excel spreadsheets in compliance with a D.C. District Court order, decided November 24.

The results do not inspire confidence. Despite knowing this data would be scrutinized by the public, records show that nearly $10 million went to businesses for which the business name field was not entered correctly. Some of these were blank while others contained phone numbers or random dates.

Is it fraud? Maybe, maybe not. It certainly suggests, however, that the official books on $525 billion in individual PPP loans aren’t exactly up to snuff.

The legal struggle to release the data began with filing a Freedom of Information Act (FOIA) in May by a coalition of news companies, including the New York Times, representatives for the Wall Street Journal, ProPublica, and 11 other newsrooms. They hoped to uncover where billions of CARES Act loans went but received privacy concern pushback from the SBA.

In June, the SBA released limited info on the top bracket of loans, from $150,000 upward. United States District Court Judge James Boasberg ruled that there was no reason not to release the information after the SBA refused to open the files up on the bottom 4 million loans at the beginning of November. The SBA pushed for a stay of the order, which was shot down by Boasberg, and finally, the SBA released the data.

As of early November, the agency had processed and approved more than 5.2 million individual PPP loans, along with an additional $192 billion in EIDL loans. PPP funds had the unique distinction of being forgivable so long as they were used for expenses like payroll.

A PPP & EIDL search tool is available on the Small Business Forum where anyone can query the released data.

EIDL Loans Searchable

December 3, 2020The Small Business Forum has added additional functionality to its PPP loan querying tool. The tool now enables users to query every single EIDL borrower as well.