Brokers

How Mike Brooks Battled in the Ring and Won Top Broker in Equipment Financing

March 6, 2025

“Equipment Financing is HUGE,” declares Mike Brooks, CEO of New York-based Best Connect Capital and recent winner at Broker Battle 2025 in the equipment finance category at deBanked CONNECT MIAMI. If his name sounds familiar, it’s probably because he appeared on stage as one of six finalists in the previous year’s competition. He refused to give up after his loss and returned this year for round two, leading to him securing a title and prizes along with it. To hear him tell it, it had been a long road to get there.

When Brooks got his start as a 27-year-old broker in 2015, for example, he had technically been battling in a ring for most of his life already.

“I had [boxing] on my mind in high school, without any influence,” says Brooks, “and I walked into a gym one day and the rest was history.” That history includes 60 fights in just amateur-level boxing, resulting in 45 wins and 15 losses. When he followed that at the pro level he went 11-2-1.

“I started fighting at the regular club shows, the Golden Gloves, the metro tournaments, national tournaments, and at one point, I was ranked number seven in the whole country,” Brooks recalls. “I beat some really good fighters, lost to some really good fighters and I made it to the highest levels in the country.”

Some of those fights even aired on live TV. As he bobbed and weaved for years in the ring, he started to think about what a possible career in business might look like afterwards. When that day came, he went to work for a local financial service company on Long Island who taught him about helping small businesses access working capital. Eventually he realized it was a business that he was uniquely suited for and now he runs his own company doing it.

First, there’s the endurance aspect, he explains. There’s a lot of calls, leads that don’t pan out, and heartbreak that hits when deals get declined at the finish line.

“A very small percentage of people can be a successful broker,” Brooks says. “You have to be able to take rejections all day long.”

To that point, Brooks noticed that as the industry grew he was not the only broker offering revenue-based financing to a client. Sometimes there were even as many as four or five other brokers talking to the same client at the same time, which meant that he wasn’t going to win every one and he did not want to bend his ethics just to eke it out. That’s when he started considering another approach and expanded his offerings.

“An equipment financing deal was my first big check during [the covid] lockdowns,” Brooks says. It was a $200,000 deal for a packaging plant. The terms were very attractive and he had the help of an equipment finance veteran who mentored him through it. When it worked out, he knew he had something very big in his arsenal and he’s been offering it ever since to anyone that qualifies for it.

“I said to myself anybody that needs equipment, this is a no brainer right here,” Brooks recalls of it. Now Brooks says when there is competition, he’s almost always the only one asking questions about equipment and the only one prepared to actually move forward with a deal tied to it. Of that experience, Brooks says he’s realized that some brokers have become so accustomed to the mindset of telling customers to take a specific deal, that they don’t stop to consider what they actually want. So his approach is to go in and diagnose what it is they’re trying to do first and then advise them of their options accordingly. And that’s what he does day after day.

“I said to myself anybody that needs equipment, this is a no brainer right here,” Brooks recalls of it. Now Brooks says when there is competition, he’s almost always the only one asking questions about equipment and the only one prepared to actually move forward with a deal tied to it. Of that experience, Brooks says he’s realized that some brokers have become so accustomed to the mindset of telling customers to take a specific deal, that they don’t stop to consider what they actually want. So his approach is to go in and diagnose what it is they’re trying to do first and then advise them of their options accordingly. And that’s what he does day after day.

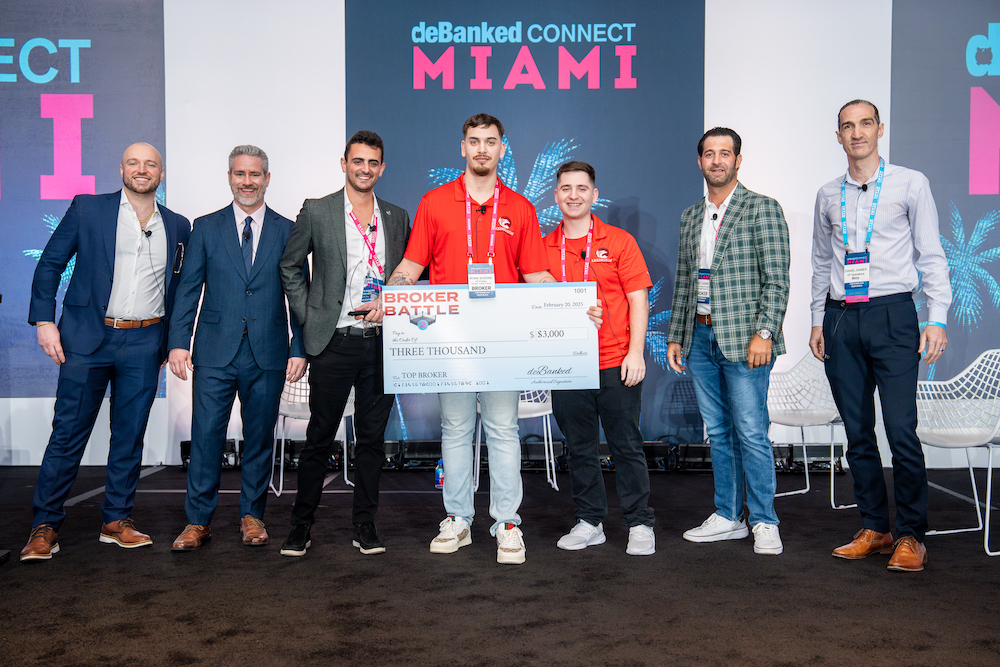

At Broker Battle 2025, it was very much like time spent in the office. He was expected to be his normal self, but on stage in front of a large audience, while three judges played the role of prospective client and asked him questions about what they should do. The end result of it all was that Mike Brooks, former fighter in the ring, walked away as the Broker Battle champion in the equipment finance category in 2025.

“It felt amazing to be able to showcase what I do on a daily basis,” Brooks says, making it a point to say that even the venue took note of his win and offered him a personal congratulations on social media.

In the final photo-op on stage with his prize check, Brooks was the epitome of his dual life—the suit and tie spoke of business, while the cigar and sunglasses hinted at his former life in the ring. “I was a crowd pleaser,” he jokes. “You want to be like ‘bam bam bam’ and the crowd to be like ‘AHHHH!!!’ I want them to do that. I had a great time at deBanked.”

Ryan Showe on Winning This Year’s Broker Battle

March 3, 2025 “What being a broker means to me is servicing your clients in the best way possible, really putting their needs before anyone else’s,” says Ryan Showe, VP of Sales at Long Island-based Lexington Capital Holdings. “Ultimately, at the end of the day, we don’t have a job if our clients aren’t happy, so just constantly doing the right thing, putting your best foot forward, and making sure that you’re doing everything ethically and honest.”

“What being a broker means to me is servicing your clients in the best way possible, really putting their needs before anyone else’s,” says Ryan Showe, VP of Sales at Long Island-based Lexington Capital Holdings. “Ultimately, at the end of the day, we don’t have a job if our clients aren’t happy, so just constantly doing the right thing, putting your best foot forward, and making sure that you’re doing everything ethically and honest.”

Showe was the winner of the 2025 Broker Battle at deBanked CONNECT Miami for the revenue-based financing category, earning him the recognition of Top Broker and the recipient of some prizes along with it. Showe has been in the business for just a little over three years, starting at Lexington during its beginnings. Back then, learning the ropes while doing the work meant putting in 70-80 hour weeks on a regular basis. That included not only seeking out advice from the experts but also watching videos and reading books to fully immerse himself in the mindset of what it would take to become successful.

That effort is paying off and today Showe specializes in the most delicate part of the process at Lexington, helping clients who have applied get to the finish line with a deal while managing lender-side negotiations and communications. On the latter side, that means being highly familiar with the guidelines of more than 60 financial service companies at any given time.

“Anybody can get someone to apply and just fill out a quick one-page application, send over a couple bank statements, but really selling the deal, there’s a specific art to it,” says Showe. “It’s really important to be an expert in your industry and know all the lender guidelines, know what the backend process looks like, because every lender is going to have a different process, whether there’s certain steps that some lenders want, whether it’s a manual-login or DecisionLogic. There’s so many ins and outs to every different lender. And just being able to know all that off the top of your head and just really sound like an expert.”

At Lexington, one of the recent educational team-building strategies was to host an internal Broker Battle in which 30 employees participated in a double-elimination competition. The company’s CEO, Frankie DiAntonio, devised the format and questions—not only role‑playing scenarios but also testing general industry knowledge with trivia. Showe says it’s good practice to be put on the spot in front of a crowd, because a key part of sales is thinking on your feet and executing when it counts. Doing it together with colleagues made for a fun experience in a company that prides itself on a family‑like atmosphere, while also mirroring the competitive nature of the industry where many brokers vie to serve the same customers. It’s game time all the time.

“I even tell my clients, ‘competition is always going to breed the best results,'” Showe says. “If you want the best of the best, you have to make people compete. And it goes down to even selling a deal, right? So if I have a deal and another company has a deal, compare my numbers against their numbers. I’m going to do anything I can to win that business.”

By happenstance, Lexington’s Corey Digiantomasso was one of the six finalists selected to compete in deBanked’s inaugural Broker Battle in 2024, where he put up a very impressive performance. This year was Showe’s turn where contestants weren’t given much background on the format other than that it would be roleplay-based. Showe kind of liked the mysteriousness of it.

“I’m best at showing up and just getting the job done,” Showe says. “So just doing what I do every single day made it easier for me at least.”

On his victory, Showe described the feeling as awesome while also recognizing that his opponent in the Battle, Joe Sasson, was a very worthy competitor. A large crowed showed up to support both of them during the championship.

“It was great to just see all the hard work that I’ve been putting in over the last three years pay off and be crowned #1 in the industry. It goes a long way for not only myself, but for the company as well.”

Broker Battle 2025 Champions

February 24, 2025Broker Battle 2025 took place at the Fontainebleau on February 20th during deBanked CONNECT MIAMI. Video highlights and more will be available soon. In the meantime, here are the results and the top brokers:

Revenue Based Financing

Top Broker: Ryan Showe, Lexington Capital Holdings

Runner-up: Joe Sasson, Advance Funds Network

Equipment Financing

Top Broker: Mike Brooks, Best Connect Capital

Runner-up: Yaro Yarema, Capital MBS

Two Broker Battle Judges Starred in This Show

January 31, 2025 Josh Feinberg and Will Murphy, both judges for the equipment finance category at the upcoming Broker Battle at deBanked CONNECT MIAMI, previously starred in the sales reality show Equipping the Dream. The six-episode show series debuted in February 2022 where they helped train new reps at their equipment finance brokerage Everlasting Capital in New Hampshire and awarded the best of the group. The unscripted series is the most watched show in history of its kind. All the episodes are here.

Josh Feinberg and Will Murphy, both judges for the equipment finance category at the upcoming Broker Battle at deBanked CONNECT MIAMI, previously starred in the sales reality show Equipping the Dream. The six-episode show series debuted in February 2022 where they helped train new reps at their equipment finance brokerage Everlasting Capital in New Hampshire and awarded the best of the group. The unscripted series is the most watched show in history of its kind. All the episodes are here.

Any broker or sales rep that is knowledgeable about equipment financing can enter to compete in the short Broker Battle competition on February 20th at the Fontainebleau by submitting their name here and registering for the event here. The prize is $3,000, a trophy, the title of top broker, and the opportunity to be interviewed for a feature story. The two other categories, revenue based financing and SBA lending, also offer the same prizes and can be entered into using the same links.

Compete to Be The Top Broker in Person and Win Cash, Trophy, and the Title

January 23, 2025

If you sell revenue based financing, SBA lending, or equipment financing, deBanked MIAMI invites YOU to compete in Broker Battle 2 in Miami Beach at the Fontainebleau on February 20th. It’s simple, just register to enter it here if you’re already attending the event, and be judged in a short qualifying round in person during deBanked MIAMI. The two highest scored contenders for each of the 3 aforementioned categories will compete on stage at the conclusion of the event for a short championship.

THE WINNER OF EACH CATEGORY GETS:

- $3,000

- TROPHY

- TITLE OF BEING TOP BROKER

- INTERVIEW WITH DEBANKED (AT YOUR DISCRETION)

This year, Anthony Truglia, the winner of Broker Battle 1, will return as an MC! The judges are a mix of previous participants and industry veterans who are ready to make the competition one you won’t want to miss participating in. All attendees of deBanked MIAMI will get to watch the battle as part of the day’s normal course of activity. See the photos from last year’s inaugural battle here or watch the full video to see what it was all about below!

BROKER FAIR IS BACK! – NYC

May 2, 2022 Broker Fair is coming back to New York City on October 24th at the New York Marriott Marquis in Times Square. Anticipated to be the biggest Broker Fair ever, brokers from the small business lending, commercial financing, revenue-based financing, leasing, factoring, and MCA industries, will come together in the heart of New York.

Broker Fair is coming back to New York City on October 24th at the New York Marriott Marquis in Times Square. Anticipated to be the biggest Broker Fair ever, brokers from the small business lending, commercial financing, revenue-based financing, leasing, factoring, and MCA industries, will come together in the heart of New York.

“It’s amazing to have participated in the industry’s growth over the last four years,” said Broker Fair founder Sean Murray. “Our first event launched in Brooklyn in 2018 and now the demand has brought us into a massive newly-renovated venue in the middle of Times Square.”

Brokers, lenders, funders, factors, equipment financiers, fintechs, and the whole small business finance ecosystem can expect a full day of education, inspiration, and high quality networking opportunities.

Register here. For inquiries or questions, email events@debanked.com.

See last year’s sizzle reel:

Meet The Aspiring Brokers Who Competed on Camera

March 10, 2022

The full cast of Equipping The Dream, the first b2b sales reality show, will reunite at deBanked CONNECT Miami on March 24th.

RJ Rochelle, Juan Carlos Marcano, Thomas Long, and Angela Thompson (above in order), all participated in a week long sales training last November that was captured on camera. They competed for a grand prize that was won in the season finale that aired just recently on March 3rd. Equipping The Dream is the defining b2b sales reality show. Now you can meet the brokers and the trainers that helped them in person!

Only a limited number of tickets to deBanked CONNECT Miami are left and sponsorships have already sold out. This will be deBanked’s 4th event in Miami since 2018.

All six episodes of Equipping the Dream are available on deBanked TV FREE.

Latin Financial Launches First Lending Podcast in ‘Spanglish’

February 4, 2022 In an inaugural move for small business financing this week, Latin Financial launched the first ‘Spanglish’ podcast for funders, lenders, merchants, and brokers titled the Latin Financial Podcast. Hosted by the company’s CEO Sonia Alvelo and co-hosted by Underwriter Ruth Alustiza, Latin Financial hopes to create an open forum of discussion and education about how Latino-owned businesses can get access to different types of financial products; all in two different languages.

In an inaugural move for small business financing this week, Latin Financial launched the first ‘Spanglish’ podcast for funders, lenders, merchants, and brokers titled the Latin Financial Podcast. Hosted by the company’s CEO Sonia Alvelo and co-hosted by Underwriter Ruth Alustiza, Latin Financial hopes to create an open forum of discussion and education about how Latino-owned businesses can get access to different types of financial products; all in two different languages.

“It was so much fun, but so scary,” said Alvelo, when asked about her experience recording on her first episode. “[I’m doing this] to make sure the merchants and clients have and will have the right information, I know I’m breaking barriers of languages, it’s the right thing to do.”

While still in its infancy, Alvelo is expecting the show to take off. Her target audience among merchants is a growing group of Latino-owned small businesses who have been historically underbanked. Offering episodes in both English and Spanish, the podcast hopes to not only educate the show’s listeners on how small business lending works, but also hopes to serve as a crash course in either Spanish or English for those who are already members of the non-bank finance world.

The show will have funders, lenders, merchants, and staff of Latin Financial on as guests, according to Alvelo. The show has begun a stream of content that will be released on a regular basis that is being uploaded on platforms like Apple Podcasts, Google Podcasts, and Spotify.

“We are doing one episode per week, said Alvelo. “We’re going to add guests, they are already asking me to attend, and lenders. I’ll be doing back and forth, Spanish and English for sure.”

Alvelo seems confident that the show can separate itself from the countless other finance podcasts that exist. With a dynamic of two languages, two cultures, complex financial products, and revolving guests, it seems as if Latin Financial has discovered a niche in the business media space. “The audience can listen in Spanglish about what we do to help business owners in the United States and Puerto Rico. It’s a new way to stay informed, get educated on updated programs in the financing Industry, all in two languages,” Alvelo said. “It’s Spanish and English, equals Spanglish!”

A weblink to the show can be found here.