Brokers

Broker Fair’s 2026 Conference Beats All Previous Shows in New York City

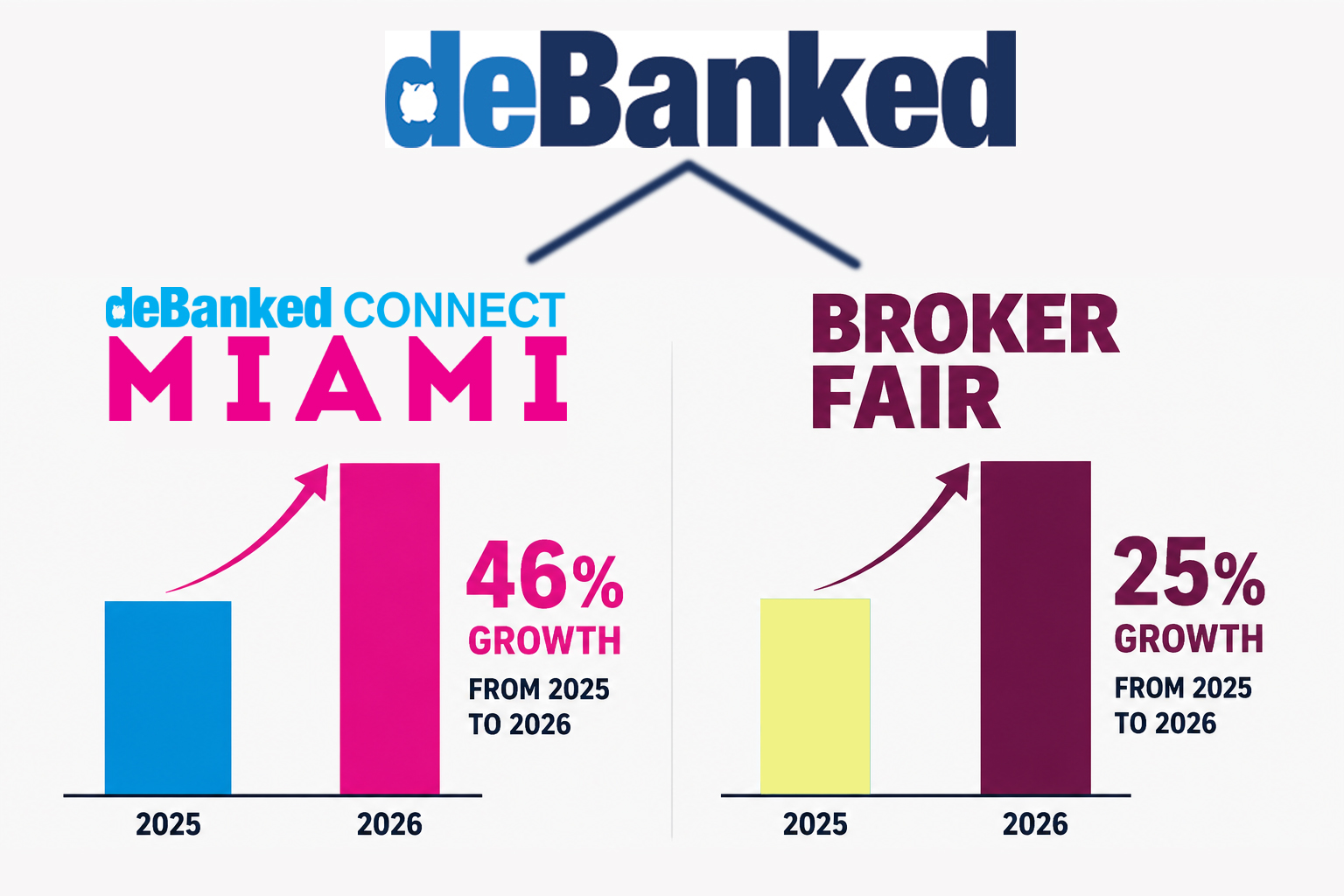

June 2, 2026The industry is full of life! deBanked’s first two conferences of 2026 have set all-time records for tickets. deBanked CONNECT MIAMI grew by 46% year-over-year while Broker Fair in New York City grew by 25%. More than 50% of attendees to this year’s Broker Fair had never attended Broker Fair before in the past despite the annual event having already run for 9 straight years.

The next deBanked affiliated conference, B2B Finance Expo, takes place October 19-21 at the Cosmopolitan of Las Vegas in collaboration with the Small Business Finance Association.

Speed to Lead, Closing the Deal, and Running an ISO Shop

April 15, 2026 I sat down with Nicole Cruz, CEO of Redline Capital Inc, a brokerage based in in Secaucus, New Jersey. Cruz spilled some of the secret sauce, including what happened when she tried lead sources that her peers and competitors adamantly claimed weren’t good. Cruz started in the industry in 2018 and worked as a sales rep and ISO rep before trying her hand at starting her own company. One of the signature elements of their sales culture is the daily “power hours” they have. When I arrived on site, they were in the middle of one. She explains it all and more in our talk.

I sat down with Nicole Cruz, CEO of Redline Capital Inc, a brokerage based in in Secaucus, New Jersey. Cruz spilled some of the secret sauce, including what happened when she tried lead sources that her peers and competitors adamantly claimed weren’t good. Cruz started in the industry in 2018 and worked as a sales rep and ISO rep before trying her hand at starting her own company. One of the signature elements of their sales culture is the daily “power hours” they have. When I arrived on site, they were in the middle of one. She explains it all and more in our talk.

You can follow Cruz on her Instagram here.

While we’re posting some short video snippets across social media, you can listen to the full thing on Spotify while you’re on your commute.

Also, make sure you’re registered for Broker Fair, coming up on June 1 in New York City! Brokerfair.org.

Eddie DeAngelis to Speak at Broker Fair 2026

March 31, 2026

Eddie DeAngelis will be speaking at Broker Fair 2026 in New York City on June 1. DeAngelis owns a high-performing small business finance brokerage.

About QualiFi

QualiFi’s journey is just getting underway and will be extraordinary. We get to push the reset button one more time and apply what we’ve learned from our many successes and failures. Our current mission with QualiFi is two-fold, and we’re inspired to make it happen. We’re determined to take the hassle out of small business financing by building an accessible, affordable #1 client experience for business financing, one client at a time.

Success and Lessons Learned From Small Business Finance Industry Vets

December 11, 2025 “In October, the company did $23 million+ and it was our best month ever,” says Eddie DeAngelis, founder and CEO of QualiFi, a full-service business loan brokerage.

“In October, the company did $23 million+ and it was our best month ever,” says Eddie DeAngelis, founder and CEO of QualiFi, a full-service business loan brokerage.

Talk to anyone in the industry and it always seems to be their best month, quarter, or year, but that’s just happenstance since those same people will also tell you—if they’ve been in it long enough—that success is not a straight shot up. They’ll also say that success is defined on their own terms, not by other people’s measures.

In DeAngelis’ case, for example, the origination figure, which comprised a mixture of LOCs, term loans, HELOCs, SBAs, and equipment financing, is all the more celebratory because the company accomplished it with just 13 funding reps at the time.

“It just shows how efficient our business model is,” DeAngelis says, “so that’s the number that I’m really proud of, which is 13 reps.”

Jared Weitz, CEO of United Capital Source, a small business finance marketplace, had a similar perspective, sharing that at one point he had 27 employees and now operates with 17—but the 17 are producing the same output as the 27.

“Ten less people, less expenses, same numbers, higher net margin and profit,” Weitz says. He explained that he spent time dissecting his P&L, structures, and systems to maximize efficiencies to get where he wants to be.

“I’ve always viewed it as ‘am I profitable every year?’” Weitz says. “‘Do I have concentration where, if 3,4, 5, [lenders] in my portfolio go out, am I screwed? Can I grow without body count? Can I create more efficiencies in my business through automations, technologies, different marketing and grow without body count?’ I’ve done that very well.”

Zach Ramirez, CEO of Calldrive, a pay-per-call marketing and consulting company, also has experience running brokerage shops.

“I found that my skillset, I was great at sales. I still am good at sales, but I think my real skill is building operations. I’ll be honest, one of my weaknesses is I’m not really that great at managing big groups of people,” Ramirez says.

In this regard, Ramirez also thought deeply about maximizing efficiencies rather than maximizing headcount, and says that “I found that what I do enjoy doing is building the infrastructure, the marketing, the sales processes, all the metrics and KPIs, and building the CRM and all the automations.”

Between that and his mountain of firsthand experience working at and operating brokerages, Ramirez is often called upon these days as a consultant for ISOs to help fix or improve all of those things.

Chad Otar, CEO of Lending Valley, a revenue-based financing provider, shrugs at the milestone benchmarks some of his competitors tout and explains that it’s not a race for publicity but rather a marathon of good economics. Otar, for example, says his company funds from its own self-funded balance sheet and has no incentive to be anything less than prudent.

“I’m not looking for market share,” Otar says. “I’m just looking for, you know, a calm, collected life at the end of the day.”

Through all the years Otar has been working in the industry, he says he’s seen the cycle of jaw-dropping deals that, while they may still be more expensive than a bank loan, are unlikely to yield a financial incentive for him to risk participating in.

“And I’m like, no, no. I’ll just stick to what I know, stick to what I like,” he says.

All four executives have the benefit of experience under their belts. Otar has worked in the industry for 19 years, Weitz for 20, Ramirez for 16, and DeAngelis for 12.

What they all have in common is a deep love for the game.

“It’s a delight, I love this #$@&*!-ing industry,” Ramirez says.

“I wouldn’t trade it for the world. I love this industry a lot,” echoes DeAngelis.

Weitz and Otar expressed similar sentiments.

DeAngelis, who had a couple of decades’ worth of experience as a traditional business owner in screenprinting and designer fragrance wholesaling, says that he loves talking to business owners, overseeing operations, and building relationships with partners.

Weitz says it’s been a joy to watch long-term members of his team go through their own life milestones, like going from an apartment to marriage to a home to kids.

“They’ve seen growth also, which really also means we’ve shown growth to not just our clients but our staff,” Weitz says. “These are really good recognition signs that we’re doing pretty good, which is also how I define success.”

If you’re earlier on in your career or entrepreneurial journey, know that there are going to be rough times—especially in this industry.

“My very first job selling finance was for [a mentor],” says Ramirez. “I was probably 19 or something, or 20, and he always said, ‘when you build your business, put your blinders on and only focus on your business and you’ll be instantly rich in 20 years.’”

Ramirez says that the march toward success is kind of like going to the gym. There are people who give up on a routine after three months because they think they’ve put in enough time to judge the final outcome and never truly follow through. And then there are those who stick with a routine, realize that they’re incrementally moving toward their goal, and eventually get there. Ramirez says he has been guilty of surrendering too soon in the past and has also fallen victim to shiny object syndrome. In one example of the latter, he said his previous ISO became overly caught up with selling Employee Retention Tax Credits (ERTC/ERC) during COVID, to the point where it overwhelmed and negatively impacted what had been a well-run business.

“It was a waste of time and energy more than anything, but also cash, because I didn’t remain true and focused to my major core expertise or my core area of competency,” Ramirez says. “I think we lost probably over a full year. We went the wrong direction.”

Otar, meanwhile, says he has felt the pressure as a funder in an increasingly competitive environment with demanding brokers. In one example, he says that while he normally sticks to his principles about not doing same-day fundings, he became convinced to make an exception—and it came back to bite him.

“I did a same-day funding and the next morning on the first Decision Logic, there’s four different positions in there already.”

In his view, that completely changed the risk profile of the deal and produced immediate regret. “That’s why I’m not advocating for same-day funding. I am not advocating for [online] checkouts,” he says. “I’m not doing any of that. I’m still sticking to what I know best, and it’s the reason why I have longevity in this industry.”

Otar adds that he is still employing automation, tools, and systems, and running a modern operation, but he thinks very carefully about each decision.

For Weitz, one of the big defining moments in his business was realizing that concentration risk can be existential. In an industry that prides itself on strong relationships, putting too many eggs in one basket can produce unforeseen consequences if a lender or funder disappears. And what are the odds? High enough that it happened to him. In the early days of United Capital Source, two large funding partners ceased operations at the same time, one of which comprised nearly half of his company’s entire portfolio. That not only jeopardized renewals but also the valuable volume bonus relationships he had with both.

“I know plenty of large brokers who make their profits solely from volume bonuses,” Weitz says. Fortunately, he recovered—and it gave him the chance to refactor his strategy to mitigate future fallout.

DeAngelis says that things can go from great to not good at all in a very short time. In one example, he said that six months after being featured positively in a deBanked story in early 2023, his company QualiFi hit such a snag that he had to temporarily take himself off payroll.

“We just ran into this down spurt where we had a really bad month,” DeAngelis says. “We’ve been there before, right? Another month, another really bad month. ‘Okay, so now back-to-back months. What’s going on? June, July, another bad month. Now it’s a bad quarter,’ and we just were spiraling down, like revenues dropping 30%, we’re starting to stress with the bills, like, ‘what the hell’s going on?’”

They knew they didn’t forget how to execute, but they made tweaks where they could. Like Ramirez’s gym analogy, DeAngelis said they didn’t completely change what they were doing—they stayed the course.

“Our answer was to just keep our heads down, just keep pushing, make some changes and start watching what we’re spending and just barrel through and push through,” DeAngelis says. “And then when we got to October [2023], is when things started to turn for us.”

Two years later, that recent $23 million funding month is a milestone that arose from going through the bad to get to the good. The last several months have also come in at over $15 million.

Some founders try to leverage milestones into additional growth before they’re ready, but DeAngelis—who has been down this road before, including with a previous company he started that was acquired by Nav—says it’s become important to look at each portion of the business as its own business. Hiring and onboarding, for example, has become its own structured operation.

“Before when we lost a rep or we needed to hire someone, we’d hire like the first two to come through the door and just put them on the phones, right?” DeAngelis says. “Those days are done. So the hiring process, we’re super selective. We want to make sure it’s a really good fit for the candidate, as much as this is for us, for long-term sustainability.”

DeAngelis has added a few more reps since the earlier-mentioned 13 and is being cautious about how they approach growth from here.

Ramirez, meanwhile, says that sometimes it helps to look at a problem in reverse. A common gripe these days is that the small business finance market is getting too crowded and squeezing margins (and ethics).

“If I look at everything from the perspective of, ‘I’m an ISO, and there’s more ISOs coming in,’ I understand why they would feel threatened,” Ramirez says. “Because… we’re all fighting for the same pool of merchants, essentially. I would respond with, ‘well, why don’t you help them?’ Instead of being fearful, then why don’t you help them? Why don’t you find these other smaller ISOs and help them do business the right way. Consult with them, charge them for that.”

Ramirez’s outlook embraces the spirit that success in the industry is not limited to being the best broker or the best lender, but about spotting opportunities and being brave enough to capitalize on them.

For Weitz, that meant diversifying early on beyond just one product. United Capital Source offers LOCs, HELOCs, SBA loans, term loans, revenue-based financing, equipment financing, and more. The result is long-term client relationships that shift between products as needs evolve—some going back to the company’s inception 15 years ago. Weitz also notes that not all new competition is real competition: his team conducts themselves with a level of expertise and best practices that they believe clearly distinguishes them.

For Otar, seeing a crowd rush into something doesn’t necessarily indicate a real opportunity, at least not economically. Unless the play is for market share or another specific objective, he considers patience and vigilance his advantages.

“I’ve been through the ringer,” Otar says. “I started this a long time ago. I was an opener, I was an originator, I was a collection guy, I was an underwriter, I’ve seen it all. I don’t think there’s one area in this industry that I haven’t been able to cover yet.”

“I’m here for the long run, not overnight,” Otar adds. As part of that, he prides himself on relationships not only with brokers but with every merchant he funds.

“My mom, when I first started, she had said this, ‘there’s three things that you don’t mess around with in people’s lives: their money, their spouse, and their car.’”

Realizing that his business involves one of those three, he has made it his mission to manage it with care.

“If you look at Lending Valley’s reviews, we’re at 5.0 right now, every single one of them. You could give them a call and they’ll be like, ‘Chad is amazing,’ because I try to keep them on with me.”

For DeAngelis, part of success is giving back. For example, they recently started a charity drive in the office where each month a different employee selects a charity and the company donates to it.

“We started with a small donation of like $500 a month,” DeAngelis says. “And it started really catching on, and I loved it, and got everybody involved. And we talk about it every month. Somebody picks a charity, tells us why it’s special to them, and then they give us some updates on it.”

“I just want to say that ever since we started doing that, even when we were struggling, our business just literally made a skyrocket transformation,” DeAngelis adds. “Over the last year, we’ve doubled and tripled and almost quadrupled our fundings and our revenues.”

For Ramirez, he says that “Last year was one of the best financial years of my life.” He used some of the earnings from it to acquire a small telecom company, which has become another valuable component of his overarching strategy. For younger people entering the space, he’s certain that this business is here to stay.

“The industry is not going anywhere,” he says. “Is it going to fluctuate? Is it going to change? Absolutely.”

Weitz, now two decades in, also concludes that by any rational measure, this business will continue to provide opportunities—as long as one evolves with the times.

“People are always going to need homes,” Weitz explains. “People are always going to borrow against assets. Businesses will never go away, ever, ever, ever, and they will also never, ever, ever have enough capital to grow themselves. They’re always going to need an outside source. This is the way the world has worked for a thousand years. So that won’t change. How people access it will change. The cost will change. The products will change. The need will not. So as long as you’re shifting with that, you’re in an industry where that need is still abundant.”

Otar says, “At the end of the day, I’m very happy with what I do every day. It makes me excited to wake up and actually want to go to work. It’s like I don’t have a job per se. They say, ‘if you have something that you love to do every day, it’s not a job.’ It just becomes a habit at this point. And I enjoy my habit.”

On The Ground at the Lexington Capital Grand Opening Ceremony

November 18, 2025 “Today, I would like to share three stories from my life and the journey of what it took to get here today. The first story is about love and loss. I was lucky. I found what I love to do early in life. That was being an entrepreneur.”

“Today, I would like to share three stories from my life and the journey of what it took to get here today. The first story is about love and loss. I was lucky. I found what I love to do early in life. That was being an entrepreneur.”

So began the speech made by Frankie DiAntonio, the Founder and CEO of Lexington Capital Holdings & Lexington Estates, at the ribbon cutting ceremony for the company’s new commercial property and headquarters in Port Jefferson Station, Long Island.

On the three acre plot with private parking and 16,000 square feet of office space, hundreds of people including 85 employees, their friends, families, and even funding partners, gathered to celebrate the next chapter of Lexington.

“I started my first company when I was 19 years old,” DiAntonio continued. “It was an auto repair shop. I was so excited about it, I told friends, family and the whole entire community. I did not know how to market or generate leads or even how to acquire customers back then.”

Between the live outdoor DJ, a busy food truck operator, and the cacophony of brokers trying to make or close a deal from their cell phone in the parking lot, the activity caught the attention of locals, including a representative from the town’s chamber of commerce who was eager to welcome them.

Between the live outdoor DJ, a busy food truck operator, and the cacophony of brokers trying to make or close a deal from their cell phone in the parking lot, the activity caught the attention of locals, including a representative from the town’s chamber of commerce who was eager to welcome them.

DiAntonio, who actually began the proceedings outside by playing the National Anthem, walked the crowd through his trials and tribulations of entrepreneurship, much of which had humbled him. Lexington Capital Holdings, however, a small business finance marketplace, has been a huge success four years after it started thanks to the people around him.

“Lexington did not get built by me. It got built by us,” DiAntonio said in his speech, “by every person who walked into my life at exactly the right moment, and standing here today opening the doors to this new home, I’m reminded of the biggest lesson the story teaches, the dots always connect, just not always in the moment. They connect when you look back, when you stand somewhere you once dreamed of, you realize every twist, every friendship, every failure, every blessing in disguise brought you exactly where you needed to be.”

DiAntonio attributed much to his sister Nicollete and old friends who are now key operators at the business. Several of them gave speeches.

DiAntonio attributed much to his sister Nicollete and old friends who are now key operators at the business. Several of them gave speeches.

“Working side by side with Frankie truly is a pleasure and an honor, something I look forward to on a daily basis,” said Lexington COO Frank Lewando during his speech. “He’s my best friend, my mentor and my brother, and I’m proud of him for making this big jump and pushing our company to the next level. I patiently wait to see what’s going on next for us. With the opening up of our first commercial property today, we find a new life and direction for the company.”

Inside the building, Lexington is split into different departments. Among others there are separate sales rooms for SBA lending and its new real estate business, Lexington Estates. Purely by observation, the average age of a “Lexonite” appears to be mid-20s. A few of them said off the cuff to deBanked that working at Lexington is the best thing that ever happened to them.

Inside the building, Lexington is split into different departments. Among others there are separate sales rooms for SBA lending and its new real estate business, Lexington Estates. Purely by observation, the average age of a “Lexonite” appears to be mid-20s. A few of them said off the cuff to deBanked that working at Lexington is the best thing that ever happened to them.

When the big moment was coming to an end, DiAntonio cut the ribbon and was presented with a giant gold key and certificate.

“We knew if we worked hard and we stayed true to each other that we would make it,” DiAntonio said in the lead up to the finale. “The first two years were really tough, and we had some really rough days together. Each day was a dog fight to stay in business. I wasn’t concerned about next year, next month or even next week. I just wanted to survive and advance to the next day. By the grace of God and our hard work and efforts, we ended up funding our first deal in our second month, just a domino effect after that. Our second month we funded $71,000. Our third month we funded $193,000. Our fourth month, $400,000 and modern day, we fund nothing less than $15 million every single month for small to medium sized businesses all across the United States.”

Why Lexington Capital Holdings is Expanding Into the Real Estate Business

September 24, 2025Lexington Capital Holdings is expanding beyond small business lending and into real estate, the company recently revealed. Lexington, a Long Island-based financial marketplace and brokerage led by CEO Frankie DiAntonio, is launching Lexington Estates to buy, sell, rehab, and hold properties long term.

According to DiAntonio, deals involving real estate have already been a part of their regular broker product mix for a long time, but when deciding whether or not they wanted to lend against real estate on their own or become the actual buyers and builders, they felt the latter would be more impactful. A syndication fund for these real estate deals, for example, will be open to employees of the firm to participate in. Lexington’s existing operation already has about 50 sales reps. Two from that group will move over to the real estate side to join a number of new hires they’re bringing on board to carry this plan out.

“Business is a team sport and I wouldn’t have been able to do any of this without the amazing Lexington team behind me,” DiAntonio said of the company’s success to-date.

Lexington Estates is already closing on its first property on Long Island. While they will make their focus local right out of the gate, they plan to work on deals both residential and commercial throughout the United States within 12 months. DiAntonio cut his teeth on real estate deals by participating in them personally outside of his business and now he’s making it a corporate endeavor. Whether it’s residential, retail, office space, industrial space, or anything else, they plan to evaluate it on the merits of the potential profits.

“I’m looking for deals,” DiAntonio said. “I’m looking for what’s the best bang for our buck.”

DiAntonio views this ambitious plan as one of absolute necessity given the challenges that the younger generation faces with the cost of living going up.

“I strive so hard to put my people in a position where they can make more money than the average American because you can’t even live the average American life and be average anymore,” DiAntonio said. “You actually have to be great just to live an average American life.”

Lexington Estates plans to officially launch on October 12th.

James Webster to Speak at Broker Fair 2025

March 31, 2025

James Webster, Founder and Executive Chairman of ROK Financial, will be a guest speaker at Broker Fair in New York City on May 19th.

James brings a passionate and innovative mindset to the businesses he and his company help grow on a daily basis. Since the age of 18, James has managed multiple sales floors, which allowed him to develop a strong business understanding and a passion for small business.

With nearly two decades of experience in financing and commercial lending, James and his team have helped thousands of business owners secure nearly $2 Billion in business financing, created thousands of new relationships with partners and strengthened their lender relationships, making them a true leader within the landscape. James and the team pride themselves on helping businesses identify their strengths and weaknesses, as well as educate them on the ways they can build on their successes by creating perpetual opportunities with business financing.

In addition to his role at ROK, James sits as the co-chairman of the Small Business Financing Association Broker Council, a non-profit advocacy organization dedicated to ensuring that small businesses can access financing solutions that are clear, secure, and fair. In this role, James establishes responsible and transparent practices for alternative lending brokers while also educating policymakers and regulators about the technology-driven platforms that have emerged in the small business lending market.

James was born and raised on Long Island where he currently lives with his wife, Melissa, and their two children, Lilyanna and Jameson. He is an active member of the Long Island community and feels a special connection to local businesses. Philanthropy plays a big role in James’ personal and business life. ROK’s main philanthropic initiative includes donating 50 meals for every deal that funds with ROK Financial, with the hope of helping end hunger in America.

When not at the office, You will either find James on a golf course or enjoying his other interests such as skiing, fishing, boating, traveling, live sporting & music events but, most of all, spending time with his family!

Role-playing and The Value of Practicing Sales Calls

March 31, 2025deBanked asked several brokers over the past month about the value of role-playing with colleagues to prepare for real life sales engagements. Below are some excerpts of what they said.

Cheryl Tibbs, Commercial Capital Connect: “Before my broker life, I was a call center supervisor, so just really familiar with call centers making cold calls and that type of thing. So it’s very important [to role play], I think you have to practice. You don’t want to read a script, you don’t want to sound robotic, but you want to be engaged enough where you can have a good conversation with people without having to really think about it.”

Cheryl Tibbs, Commercial Capital Connect: “Before my broker life, I was a call center supervisor, so just really familiar with call centers making cold calls and that type of thing. So it’s very important [to role play], I think you have to practice. You don’t want to read a script, you don’t want to sound robotic, but you want to be engaged enough where you can have a good conversation with people without having to really think about it.”

Is there a point where practice is no longer necessary?

“Our industry changes day-to-day, little by little, things are changing. So I think it’s just always incumbent upon us to sharpen our skills. That means practicing at least once a week.”

Josh Feinberg, Everlasting Capital: “Role-playing is like stretching before going for a run. It makes it possible for you to be fast on your feet and really be able to have the answers when you’re talking to a, let’s just say, a construction company that does equipment financing, and they’ve financed all of their equipment. A lot of times they’re going to be more knowledgeable about the equipment financing and leasing product than a lot of the brokers that are going to be talking to them in regards to it.”

Josh Feinberg, Everlasting Capital: “Role-playing is like stretching before going for a run. It makes it possible for you to be fast on your feet and really be able to have the answers when you’re talking to a, let’s just say, a construction company that does equipment financing, and they’ve financed all of their equipment. A lot of times they’re going to be more knowledgeable about the equipment financing and leasing product than a lot of the brokers that are going to be talking to them in regards to it.”

Is this something you do with your own reps?

“Yes, especially when someone is newer or starting out, role playing is essential to even a point just like on Equipping The Dream, we need to make sure that we’re call-coaching too. While we’re listening to them on the phone we’re in their ear telling them what to say, just to have them get used to it. And then we do a bunch of different role playing…we’ve done it hundreds and thousands of times over the years”

Adam Oster, Canyongate Financial: “We have a set list of questions: understanding the merchants needs and building that relationship. And if I know somebody’s really good but they’re not doing well, then we’ll go back and say, ‘Hey, let’s role play. Because there’s something—you’re too complacent, you’re missing something, or you’re not listening to the customer.’ So role play is very important.”

Adam Oster, Canyongate Financial: “We have a set list of questions: understanding the merchants needs and building that relationship. And if I know somebody’s really good but they’re not doing well, then we’ll go back and say, ‘Hey, let’s role play. Because there’s something—you’re too complacent, you’re missing something, or you’re not listening to the customer.’ So role play is very important.”

How does this take place?

“If they’re here locally, we’ll do it in-house a lot of times. I’ve got a couple people—one in California, one in Austin, Texas, so we have to do it over the phone. And if somebody’s thriving, I’ll ask them, ‘What are you doing? What are you saying to your dealerships or your customers that are helping you get deals?'”