Banking

Zoom CEO and Big Banks Rolling Back Remote Work

May 5, 2021 It’s not just you: Zoom CEO Eric Yuan admitted to suffering from video meeting fatigue at the Wall Street Journal’s CEO Council Summit. During a video conference panel called “The Future of Work,” Yuan said he is done with it after sitting through 19 video calls in one day last month.

It’s not just you: Zoom CEO Eric Yuan admitted to suffering from video meeting fatigue at the Wall Street Journal’s CEO Council Summit. During a video conference panel called “The Future of Work,” Yuan said he is done with it after sitting through 19 video calls in one day last month.

“I’m so tired of that,” Mr. Yuan said, “I do have meeting fatigue.”

Yuan said he would begin requiring employees to return to the office at least two days a week. Many WSJ guests at the May 4th conference shared the same sentiment, like JPMorgan CEO Jamie Dimon, who said the firm would begin to bring people back by July.

For creating new ideas, and “for those who want to hustle,” Mr. Dimon said, remote work doesn’t match in person. “I’m about to cancel all my Zoom meetings,” Dimon said. “I’m done with it.”

Along with the announcement from Gov. Cuomo that New Jersey, New York, and Connecticut would begin relaxing all restrictions on May 19th, FIDI hot dog vendors must be excited this week. Goldman Sachs also announced this week through a memo to employees that they should “make plans to be in a position to return to the office” in June.

Can’t Wait to Become a Bank? Buy One

March 15, 2021 Major fintech companies can’t wait to become chartered banks, and some don’t have the patience to wait for the paperwork to go through.

Major fintech companies can’t wait to become chartered banks, and some don’t have the patience to wait for the paperwork to go through.

Last week, SoFi bought California-based Golden Pacific Bank (GPB) for $22.3 million to speed up its mission to become a nationally chartered bank. SoFi paid for the cash purchase and will apply to take ownership of the bank’s OCC charter- swapping out their pending application to become a bank outright.

“By pursuing a national bank charter, we will be able to help even more people get their money right,” CEO Anthony Noto said. “We are thrilled to have found a partner in Golden Pacific Bank to both accelerate our pursuit to establish a national bank subsidiary, as well as begin to expand our offerings in SoFi’s financial products.”

SoFi, once an anti-bank fintech was preliminarily approved by the OCC for a charter earlier this year.

A year ago Varo started the buy/apply banking trend after receiving approval for an FDIC Bank Charter. LendingClub, a former Peer-to-Peer lender, soon after joined the club by picking up Radius Bank. Square just two weeks ago became a bank, announcing it received an industrial banking license.

Other lesser-known fintechs have been moving toward chartered banking as well. In February, Brex, an online banking fintech, began the process of opening a Utah Based industrial bank as well. Jiko, a small online banking and payments firm, bought Mid-Central National Bank in Minnesota.

There are other up-and-coming fintech banks, like Chime and even blockchain banking contenders, like Figure Technologies. Figure is a home equity lender that is currently applying for a banking charter without the normal FDIC-insured deposits but instead deposits over $250,000 that would act as uninsured high yield loans.

If Sofi’s plan works, the firm aims to contribute $750 million toward digital lending while maintaining GPB’s community banks’ business and branches. The deal should be completed before the end of 2021, and GPB will operate as a division of SoFi Bank.

LendingClub Talks Earnings Post Radius-Bank Acquisition

March 11, 2021 “It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

“It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

The company reported a Q4 net loss of $26.7M on $75.9M in revenue and originated $912M in loans. Their status of being a bank, however, is only just beginning. CFO Tom Casey explained the following:

In addition to lowering our funding cost of deposits, our new marketplace bank will capture significant financial benefits from being a bank and having a marketplace. [….]For every $100 million of loans we originate, we generate about $4 million through an origination and servicing fee when we sell the loans in the marketplace. The vast majority of this fee-based revenue is realized immediately and without requiring a significant amount of capital. However, it is highly dependent on origination volume.

[…]

We can now bolster this revenue stream with bank revenue generated by loans held for investment on our balance sheet. As you can see on the left side of the page, every $100 million of loans we hold on the balance sheet should generate additional marginal profitability of approximately $12 million. And when you compare that to the $4 million in the marketplace, that’s 3 times more. And this recurring revenue is not dependent on originations in any given quarter.

LendingClub experienced unique success during the pandemic, stating that loan performance exceeded their expectations.

“Coming out of the pandemic,” Sanborn said, “the strength of our underwriting has now also been cycle-tested. Losses on loans issued pre-COVID are in line with our pre-pandemic expectations, and loans issued since the pandemic are some of our best-performing loans in recent years.”

Square Officially Becomes a Bank

March 2, 2021 Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

“Bringing banking capability in-house enables us to operate more nimbly,” CFO and Chair of the new bank Amrita Ahuja said, “which will serve Square and our customers as we continue the work to create financial tools that serve the underserved.”

Square had previously offered credit products through a partnership with Utah-based Celtic bank. The move answers the questions “buy or build” when it comes to fintech banking. Many fintech firms, some of who even claimed to be anti-bank alternatives, have made the switch to either partnering with a nationally chartered bank or outright becoming a bank themselves.

“We thank the FDIC and Utah DFI for their partnership enabling us to reach this milestone, and look forward to continuing to expand access to financial services at this critical time for small businesses,” Ahuja said.

Linear CEO on New Merger

March 1, 2021 Fundation and ODX were in talks to merge for over a year, Linear and past Fundation CEO Sam Graziano said. Then covid changed plans, but by mid-summer talks were back on.

Fundation and ODX were in talks to merge for over a year, Linear and past Fundation CEO Sam Graziano said. Then covid changed plans, but by mid-summer talks were back on.

There was recognition by the leadership team at Fundation and CEO of OnDeck Noah Breslow that ODX and Fundation were competitors in the same banking-as-a-service space and could merge to serve the entire market, Graziano said.

Launching with the press release last week, Linear is majority-owned by Fundation, but Graziano said it was looked at as a “cashless transaction” and merger between two companies. This upcoming year, Linear plans “To merge the two businesses more structurally,” Graziano said, “continue to merge the two businesses, deepen industry relationships, and continue to expand the scope of clients.”

Fundation’s minor business funding branch will continue under the Fundation brand, Graziano said.

ODX Merges with Fundation

February 25, 2021 The ODX brand from OnDeck is splitting off to combine with Fundation, forming a new SMB digital banking company called Linear Financial Technologies.

The ODX brand from OnDeck is splitting off to combine with Fundation, forming a new SMB digital banking company called Linear Financial Technologies.

The news follows the recent disclosure from Enova that it was looking to divest ODX in addition to OnDeck Canada and OnDeck Australia.

The new firm, headed by the current CEO of Fundation, Sam Graziano, will be an online banking service provider. Linear will take on Fundation’s service of processing loans for big and small banks, reportedly processing a total of $13 billion.

“Over the years, our combined platforms have served hundreds of thousands of business customers through many of the leading business banking providers in the market, deploying modern banking experiences that their customers and front-line colleagues expect in the digital era,” said Graziano in the published announcement. “Together as Linear, we’ll have the resources to more rapidly expand the breadth of our solutions to bring more value to our clients.”

Enova will retain a minority stake in the new firm.

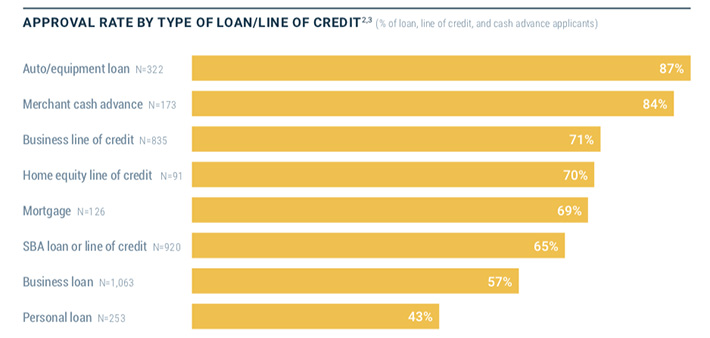

Merchant Cash Advance Approval Rate Was 84% in 2020, Federal Reserve Finds

February 3, 2021Eighty-four percent of applicants that applied for a merchant cash advance in 2020 were approved, according to the latest study published by the Federal Reserve. However, that figure includes the pre-March 2020 covid era.

When MCAs and online loans were blended, for example, the approval rate shrank from 81% pre-March 1st to 70% after March 1st.

Eight percent of all small businesses sought a merchant cash advance in 2020, down slightly from 9% in 2019. Leasing dropped from 9% to 7% and factoring dropped from 4% to 3%. Pursuit of credit cards even dropped, down from 29% to 21%.

There were some downsides for the online lending industry reported.

Only 9% of PPP applicants used an online lender.

Online lenders had the lowest satisfaction rate (43%) for small business credit needs. Credit unions scored the highest (87%).

Net satisfaction with online lenders dropped to its lowest level since 2016.

Small businesses satisfaction with big banks actually grew from 2019 to 2020.

Small businesses were less likely to apply for a business loan or MCA from an online lender in 2020 and more likely to apply for them at a bank in 2020 than they were in 2019.

Eighty-two percent of businesses applied for a PPP loan. Forty-seven percent applied for an EIDL loan.

Banks, perhaps counterintuitively, were the big winners in 2020. That trend could increase as banks and online lenders become the same thing.

SoFi, The “Don’t Bank” Non-Bank, Has Been Approved to Become a Bank

October 29, 2020It’s a little ironic. SoFi, one of the pioneers of the bank disruptor market, is embracing everything it preached against. The company founded in 2011 as an online student lender was just granted a preliminary approval for a national bank charter by the OCC.

When the company launched, SoFi’s message to the masses was not only that they were better than a bank but that customers shouldn’t use banks in general. They took this message to the extreme:

Just, don't do it. #DontBank pic.twitter.com/lnxKJHH3QJ

— SoFi (@SoFi) February 11, 2016

Banks send you statements. Our statement is we don’t like banks. Check us out at https://t.co/B5YXtHWKL0. #DontBank pic.twitter.com/RshfsAhdYR

— SoFi (@SoFi) January 26, 2016

Happily not a bank. http://t.co/bDN6i1Fd5W #SoFiSoFun

— SoFi (@SoFi) August 25, 2015

To be fair, a lot has changed at SoFi since. Anthony Noto, a former Goldman Sachs banker, took over as CEO in February 2018. And SoFi has grown well beyond just student loans to personal loans, home loans, insurance, small business financing, credit cards, and investing.

The company has also expanded its visibility, including by securing the name rights to the Los Angeles football stadium that serves as the home to the Rams and Chargers. When the deal was announced, it all sounded something very much like what a… bank… would do.

SoFi has technically been mulling the idea of becoming a bank for a long time. They applied for a state industrial bank charter in 2017 but withdrew it amid some internal issues as well as external criticism over the choice of charter.

According to Reuters, Noto said of the latest approval news:

“SoFi is on a mission to help consumers get their money right all in one app. This preliminary conditional approval from the OCC is a testament to the mission-driven company we have built, the employees who help it grow, and the over 1.5 million members we currently serve.”