SoFi, The “Don’t Bank” Non-Bank, Has Been Approved to Become a Bank

It’s a little ironic. SoFi, one of the pioneers of the bank disruptor market, is embracing everything it preached against. The company founded in 2011 as an online student lender was just granted a preliminary approval for a national bank charter by the OCC.

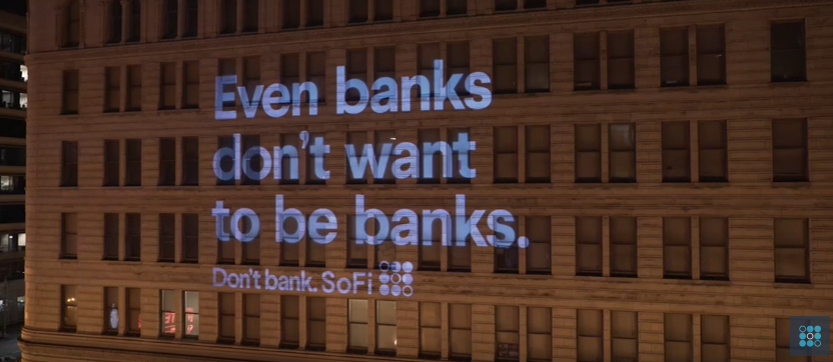

When the company launched, SoFi’s message to the masses was not only that they were better than a bank but that customers shouldn’t use banks in general. They took this message to the extreme:

Just, don't do it. #DontBank pic.twitter.com/lnxKJHH3QJ

— SoFi (@SoFi) February 11, 2016

Banks send you statements. Our statement is we don’t like banks. Check us out at https://t.co/B5YXtHWKL0. #DontBank pic.twitter.com/RshfsAhdYR

— SoFi (@SoFi) January 26, 2016

Happily not a bank. http://t.co/bDN6i1Fd5W #SoFiSoFun

— SoFi (@SoFi) August 25, 2015

To be fair, a lot has changed at SoFi since. Anthony Noto, a former Goldman Sachs banker, took over as CEO in February 2018. And SoFi has grown well beyond just student loans to personal loans, home loans, insurance, small business financing, credit cards, and investing.

The company has also expanded its visibility, including by securing the name rights to the Los Angeles football stadium that serves as the home to the Rams and Chargers. When the deal was announced, it all sounded something very much like what a… bank… would do.

SoFi has technically been mulling the idea of becoming a bank for a long time. They applied for a state industrial bank charter in 2017 but withdrew it amid some internal issues as well as external criticism over the choice of charter.

According to Reuters, Noto said of the latest approval news:

“SoFi is on a mission to help consumers get their money right all in one app. This preliminary conditional approval from the OCC is a testament to the mission-driven company we have built, the employees who help it grow, and the over 1.5 million members we currently serve.”

Last modified: October 29, 2020Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.