ACH Advances

Why You Need FundersCloud – An Independent Review

August 29, 2012Picture this:

You get up in the morning, take a shower, brush your teeth, and hop on to your computer. 73 new e-mails are waiting in your inbox. Ugh! Some of them are saying “Hey buddy, I got this deal that I think you might want to co-fund. Give me a call later and I’ll try to give you a breakdown.” Half of the time when you call these guys back, they’re busy, have already found a participant, or the deal is way too risky for you to be interested in. Fortunately, you don’t really have to deal with this hassle ever since you joined FundersCloud. You close Outlook, log in to the Cloud and check out the menu of fresh deals that have been posted to the site. You read them aloud to yourself as you scroll down the list. “15k in monthly credit card sales, 40k gross, 720 credit, in business 3 years, ooo.. and it’s a restaurant! $10,000 advance for $13,700… I like… I like… oh and $7,000 has already been raised.” You click ‘Bid’, type in $3,000, and click ‘Bid’ again to finalize. That’s it. You’re done. Once the agent closes the deal, your $3,000 is automatically withdrawn, along with the amounts from the other participants to fund the merchant the $10,000. Satisfied, you walk into the kitchen to make toast…

And that’s what FundersCloud has done. Whether you are an independent agent, an ISO, or a funder, deal syndication is now as easy as:

FundersCloud is not the competition. They’re the turbo boost button to the marketplace that already exists. This Cloud doesn’t threaten or replace your existing cloud, system, database, or CRM but rather complements it, integrates with it, and adds even more value to what you already have.

FundersCloud makes funding quicker, smarter, more efficient, and incredibly transparent. This isn’t a paid advertisement. In fact we spent a few weeks on the phone with the FundersCloud team to come up with our own independent assessment. “How does this work? Who reviews this data? How can people trust you?” and so on… We’re actually thankful their team is still accepting our phone calls after our barrage of questioning and requests for details.

FundersCloud makes funding quicker, smarter, more efficient, and incredibly transparent. This isn’t a paid advertisement. In fact we spent a few weeks on the phone with the FundersCloud team to come up with our own independent assessment. “How does this work? Who reviews this data? How can people trust you?” and so on… We’re actually thankful their team is still accepting our phone calls after our barrage of questioning and requests for details.

The reason we believe FundersCloud is the future of syndication is because it allows people to continue syndicating with funders and people they already trust.

Huh?!

Allow us to explain using a fictional example:

Funder 123 encourages friends, agents, and funders to participate in funding certain deals. ISO ABC likes to syndicate some of those deals but not all of them. So the owners of ISO ABC wait and hope that Funder 123 will call them sometimes with a deal that they like. Sometimes they hate the deal. Sometimes they like it. Other times, they play so much phone tag that they miss out on the opportunity. The process takes phone calls, emails, and time, time, time. Not to mention that Funder 123 may make several of these calls to other people to join in on the participation as well.

In a perfect world, ISO ABC would automatically be notified that Funder 123 has approved a deal and is seeking participants. The key factors like credit score, processing volume, batch frequency, gross sales, and other pertinent information would be immediately available. The ISO could then click a button if they wanted to participate and the rest of the process would all be automated. This perfect world exists because this is the FundersCloud model.

Ohhh yea! And it gets better

An agent is tired of submitting his/her deals to 5 funders at once, hoping that one of them will approve it. The funders are tired of the agent doing that too. Because the agent is forced to maximize the odds of approval, there is really no alternative solution than to continue operating this way. FundersCloud resolves the mess.

Hypothetical Agent DEF uploads their deal to the Cloud and selects one company from the vast array of Deal Controllers to verify and underwrite the file. Deal Controllers are typically existing funding providers, companies that have the ability to pay commissions, collect funds back from the merchants, and track the activity. Perhaps Agent DEF’s deal does not accept credit cards but does more than $10,000 a month in gross revenue, something that a lot of companies like to look at now. So Agent DEF selects a funder as the Deal Controller in the Cloud. The underwriters at that funder are then able to access the deal through the Cloud and underwrite it. If the file meets their standards, they Verify it. The funder can then choose to fund 100% of the deal themselves or pledge to fund anywhere from 1% to 99% of it and put the remaining percentage of the approved funding terms up for auction on the Cloud.

The key details of the deal are then immediately posted and viewable to all members of the Cloud. Thousands of people will now see that a funder has verified this deal and is willing to fund part of it. If you trust that funder’s judgment, have participated with them before, or just love funding anything you can get your hands on, you can opt to participate in the deal with them. You’re not flying blind because the credit score, processing volume, gross sales volume, time in business, type of business, and batch count are all there for you to see. Cloud members can’t steal deals because any information that could be used to identify the merchant is not visible.

So why is this better? You’re only submitting your deal to one Deal Controller (funder) through the Cloud, which then allows thousands of agents, ISOs, and funders to participate if the Deal Controller chooses to fund none of it or less than 100% of it. With this kind of system, why the hell would any agent continue to send out their deal to multiple funders and then wait a week to hear back from all of them? The merchant’s credit would get hit 5 times, one of those funders might steal the deal for themselves, and at the end of the day, only 5 people are looking at it. Wouldn’t you rather let one funder Verify your deal and then give thousands of companies and agents the chance to fund it? Seriously…

If the Deal Controller is verifying the deal and can see the full file, what’s to stop them from stealing it?

A contract, a zero-tolerance policy, and a reminder that it’s up to you to choose your Deal Controller. If there are two choices in the Cloud to Verify your deal and one is XYZ Funder and the other is someone you know very well, you can pick the company you like. Many other people may trust XYZ Funder but if you don’t know who they are, then you need not select them. Besides, if a Deal Controller is caught stealing a deal from the agent through the Cloud, they will be banned. The industry is competitive and even though there are many safeguards already in place, FundersCloud will not tolerate anyone who tries to pervert the system.

Is this process difficult for the agents?

We must admit that when it was all first explained to us, some of the terms went over our head. That’s mainly due to the fact that for all the evolution within the Merchant Cash Advance industry, many things are still kind of old-fashioned. For all the systems, databases, and clouds floating around out there now, too much time is spent e-mailing, calling, and meeting up for lunch to discuss the details that we must then go back and enter into these systems, databases, and clouds. Once you sit down and play around in FundersCloud for yourself, you’ll kick yourself for not developing this on your own or curse the Merchant Cash Advance gods for not having introduced this into your life years ago. This process is just as easy for the agent as it is for the other roles.

Agent uploads deal -> Agent chooses Deal Controller -> Deal Controller Verifies Deal -> Cloud members pledge money by placing bids -> funding contract is automatically generated and made available for download to the agent -> Agent closes the deal and uploads signed contract to the

Cloud -> The Cloud automatically pulls the funds from the pledged participants and transfers them to the Deal Controller -> Deal Controller funds the merchant and is responsible for managing the account -> Agent gets paid the commission by the Deal Controller -> Agent makes toast

The deal’s performance is then made available to the involved parties through the Cloud in real time. And since the Deal Controller is obligated to manage the deal on the Agent’s behalf, the Agent retains full control of the deal on renewals. Similarly, participants are given the option to join in on renewals or new participants can be brought in altogether. Many things can happen, but all of them lead to more funding, faster funding, and a system that’s more transparent for all the parties involved.

Your own internal cloud, system, database, or CRM is probably doing wonders for data management within your company. So why resist technology in other areas? FundersCloud isn’t a concept, it’s live. Deals are already being posted, funded, and tracked. Which means, even if you’re skeptical or have a thousand more questions, you need to sign up (it’s FREE) and see this for yourself. We’ve kept tabs on a lot of events in the Merchant Cash Advance industry, and this is one of those moments where we need to pause, join the Cloud, and make toast. Because the toughest part of getting a deal funded in the future, will be deciding if you want White, Rye, or Whole Wheat afterwards.

The FundersCloud Website

– deBanked

https://debanked.com

Note: This article was originally drafted in late April but was on hold while FundersCloud made some key upgrades. We apologize if we left out any of the new cool features.

This Week in MCA

August 23, 2012Days after our founder shared his personal tale of evolution in the Merchant Cash Advance (MCA) business, one of the industry’s largest players secured a financing round that is sure to turn some heads. It’s not every day that someone lands $100 million. New York based, On Deck Capital (ODC) has linked up with some big names, most notably Goldman Sachs. ODC has accomplished a lot and has evidently managed to deliver that same magic number of $100 million in loans to small businesses in the last 10 months alone. Seconds after this post gets published, we anticipate that ODC will let out a giant sigh from their headquarters in NYC. “Why oh why are we featured in an article about Merchant Cash Advance? We’re not a Merchant Cash Advance company,” they’ll remind themselves.

Some people would say that their micro loan program is indeed not an MCA. ODC leaves little room for confusion in their advertising message:

![]()

But in 2012, MCA is not necessarily just the purchase of future credit card sales or even the purchase of any sales. Today, MCA is synonymous with micro financing. Not to mention that ODC got its start by soliciting business from within the MCA industry. Regardless, they’ve created quite a niche for themselves and have earned the praises they receive.

Another fact worth mentioning is that Lighthouse Capital Partners (LCP) is one of the companies involved in the $100 million deal. Didn’t we just finish predicting that California VCs with an affinity for social media were about to dive head first into the world of MCA? Fresh off the wire and just hours after the ODC announcement, a social networking company called Tagged released news of a $15 million deal inked with…LCP. Expect us to cover this Silicon Valley invasion even more as it develops.

———————–

The MCA Forums… let’s talk about it. We all know that certain message board exists out there on the Internet where a handful of industry veterans occasionally visit to chat about deals. But who’s running the forum exactly and how is it really helping us all communicate better? We’ve asked around a bit and no one seems to know who the owner of it is or if he has any affiliation to Merchant Cash Advance at all. Forum fail… but it’s a cycle repeated a lot in this business. Every time there’s a payment processing expo, the MCA guys show up but they’re never the ones hosting the show. It’s much like that with the MCA Forums, where everyone’s visiting it but none of us are at the helm. The MCA Forums have helped the community over the years but there are many that would agree it’s time to take the next step. Capital Stack and Merchant Processing Resource have been working together to create what we hope will be the next phase in MCA industry communication. We want all the big players to play a part in it and to also invite our brothers and sisters in micro finance (micro lenders, asset based lenders, equipment financiers, leasing companies, etc.) to join in with us. We’re calling it ‘The Daily Funder’ and it should be ready to go in a few weeks. We’ve put this video together to reiterate what we just said. 🙂

Want to know more, share an idea, or become a key player in it? E-mail David Rubin at ceo@capitalstackllc.com OR sean@merchantprocessingresource.com.

———————–

The Merchant Cash Advance Warriors fantasy football league is now open. Co-commissioned by Merchant Cash Group and Merchant Processing Resource, we’re aiming to pick up representatives from ISOs and funders around the country for some good old fashioned competition, the friendly kind, but with smack talk allowed. Want to join? Signup is free. Please contact sean@merchantprocessingresource.com or heather@merchantcashgroup.com for a formal invite.

The Merchant Cash Advance Warriors fantasy football league is now open. Co-commissioned by Merchant Cash Group and Merchant Processing Resource, we’re aiming to pick up representatives from ISOs and funders around the country for some good old fashioned competition, the friendly kind, but with smack talk allowed. Want to join? Signup is free. Please contact sean@merchantprocessingresource.com or heather@merchantcashgroup.com for a formal invite.

———————–

Is anyone using Funders Cloud? We’re friendly with one of the owners but haven’t caught up with them in awhile. The platform was designed to be pretty awesome:

– Merchant Processing Resource

https://debanked.com

The Bubble That Wasn’t

August 17, 2012“The smaller the loan, the more likely a lender will deny it. The denial rate for applications for small loans (less than $100,000) was more than twice as high as it was for bigger loans.”

– CNNMoney 8/16/12

In early 2009, a very wise friend of mine gave me a bit of advice. As an ex-stock broker who made his fortune in the 80s, he’d seen his fair share of bubbles. And so he bestowed upon me his wisdom that the Merchant Cash Advance (MCA) industry’s days were numbered. “It’s got 6-8 months left of life in it and then it’ll go away. Everyone’s in freakout mode right now but things will go right back to the way they were and banks will push you right out of a job,” he lectured me. My expression didn’t change, for he wasn’t the first one to sing me this cautionary tale. He continued on, “You’re a nice guy so I suggest in the next few months, you go out and get into another line of work. You can always look at this experience as a wild ride but MCA is a fringe industry borne out of the financial crisis.” I thanked him for looking out for me and went home that night to mull over what he and a few others had been saying.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

I am reminded of the time when a Craigslist Ad was answered by over 500 recently laid off mortgage brokers and underwriters. Some had literally been hired to underwrite mortgages, only to be told days later that their division was closing down. Similarly, there were hot shots from the payday loan industry who stopped by to learn what our business was all about. These people looked like they had been punched in the gut and told stories of major success followed by unforeseen ruin as states legislated them out of business overnight. And still others had the mentality that MCA was a get rich quick scheme and went on to run their own funding companies or brokerage offices into the ground within a matter of months. They cursed the MCA gods and the bubble they believed they were a victim of, ignoring the reality that they had poorly managed themselves into oblivion.

As the 6 to 8 month timeline for destruction expired and the light shone on those still standing, I realized I had made the right choice by sticking it out. MCA was not a progeny of the financial meltdown. Heck, the product itself had already been around since the late 1990s and had gained significant popularity around 2005 when other players began entering the market. It also had none of the trademark signs of a bubble. If financing businesses was a bubble, there would be no such thing as banks today. Business financing has been around for literally thousands of years. MCA firms just catered to the ones that banks ignored and by 2008 that included nearly every small business in the country. One could argue that the growth rate of MCA would eventually slow down, supporting the claim with the same wisdom I had heard nearly a year before, that everything would return to “normal.”

Today’s world is anything but the world of yesterday. The unemployment rate in July was 8.3% and according to a survey reported by CNN, “[Today], the option most often sought by businesses — opening a new credit line — face[s] the lowest approval rate at 13%” Banks never did return to their old ways, nor does it seem likely that they will any time soon. Those that doubted MCA’s longevity in 2009, including those who left the industry altogether back then in fear, did not foresee the many roads of evolution that would allow it to thrive.

Years ago, an MCA was easily defined as a purchase of future sales that would ideally be completed in 6 to 9 months. Virtually every provider offered identical terms and costs, which stymied competition and eventually created stereotypes that would come to haunt the image of MCA for quite some time. For a while, America had a hard time envisioning MCA as anything but a 1.38 factor rate that was available to those that fit a certain credit criteria and processed a minimum amount of credit card sales monthly. So imagine the shock some small business owners felt when approved by RapidAdvance, a veteran MCA firm, for a ::gasp:: small business loan. A loan?! could it be? Yes, MCA has been semantically broadened to include many forms of short term lending. And then there’s Florida based Merchant Cash Group that became famous with their Fast Funding program, a financing option for businesses that fell outside the box for traditional MCAs. Some companies don’t even require businesses to accept credit cards as a form of payment. “Credit card sales? Who cares how much they’re doing in credit card sales?!” Would you ever imagine an MCA rep making such a statement in 2009?

MCA is still widely considered to be tied to credit card processing and it doesn’t ever need to officially evolve away from that. Withholding a percentage of sales directly from a payment processor is what initially allowed the many business owners that were horrible at making monthly payments suddenly eligible to receive capital. But for all the changes that have been applied to the financing product itself, something has changed with the companies offering it as well.

Competitors used to be ultra secretive about their practices. An MCA firm could be underwriting an application that another MCA firm funded the day before. Sure, the merchant wasn’t supposed to hop around and do this with more than one company at a time, but the other firm wouldn’t even confirm if they funded them if you asked. One of the great failures of the past was the lack of cooperation amongst the players in the industry. An ‘every man for himself’ mentality hurt more than it helped in a business that was struggling to create its identity in the mainstream world of finance. The North American Merchant Advance Association (NAMAA) sought to correct that through data sharing and the promotion of common standards. Some of the major members have years of experience under their belt including Merchant Cash and Capital, Strategic Funding Source, RapidAdvance, and Merchant Cash Group. These firms have been around the block and back. “MCA bubble? What bubble?,” they’ll say with 100% confidence in their tone.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

The only things bubbly in MCA these days are the excited account reps, underwriters, and support staff that are working to get America’s small businesses humming again. Some have taken to wearing their FUNDED pants 7 days a week. I know I have practically worn mine out.

I’m always struck now by the college grads that ask me if this business is sustainable. Their anxious parents are worried sick that their babies are going to be caught up in some bubble and be out of a job 6 to 8 months from now. To this I offer a few words of wisdom. “Providing small businesses with capital isn’t going away anytime soon. Sure, the product might evolve and the economy will change, but the fundamental demand for short term financing is here to stay. You seem like nice parents so I’d hate to see your kid get involved in some other industry at the end of its life cycle. He or She is getting in early on something big, something long lasting, something that has become a permanent staple of the American financial system.” Good advice for sure.

By: Sean Murray

Founder of Merchant Processing Resource (https://debanked.com)

Began career in the MCA industry in August, 2006

P.S.

The FUNDED pants do exist and were created by Next Level Funding in early 2010.

It Might Be You

August 8, 2012You are innocently eating your bologna sandwich in the lunchroom when some of your fellow elementary school friends start to giggle. You giggle a little too just because you usually all laugh at things together, even though you’re not exactly sure what the joke was. “Damn,” you think to yourself. “I got all caught up in my bologna sandwich and I missed something.” Soon others begin to laugh. You laugh nervously with them, but take a couple quick glances around the room to try and locate the source of the humor. You spot nothing, but realize the chuckles are spreading like wildfire. Some people are looking at you as if they are suspicious that you might be the only one that doesn’t GET it. So instead you double down on your laughter as if to prove you’re enjoying the joke more than they are. “I’m enjoying whatever it is we’re all laughing at more than you are!,” you say under your breath. This only makes the crowd more raucous and by now everyone is starting to point in your direction.

“Ohhhhh crapppp…”

And then you find out it is you. There you are, sitting in the cafeteria, munching on a bologna sandwich with a grade school level obscenity drawn on the back of your shirt. You don’t know who drew it or when it happened, but you quickly learn it was done in red marker, particularly the kind from the 1980s that smelled like cherry, caused dizziness, and made your nose bleed after 15 seconds. There’s always somebody getting picked on, you just never thought it would be you.

Smells Sooooo Gooddddd

“Ohhhhh crapppp…”

It might be you. Every year or so, the MCA industry welcomes in a couple new big players. There’s always one that funds more, pays more, bends more, and brags more as they quickly cut into the marketshare that established funders have had for years. Suddenly they’re the hottest thing in town, that is until about 6 months later when they start telling their “loyal” broker shops to stop sending in new deals for a while. As the newbie’s joyride comes to an end, the established funders roll their eyes and continue on the way they always have, responsibly.

It might be you. Every year or so, the MCA industry welcomes in a couple new big players. There’s always one that funds more, pays more, bends more, and brags more as they quickly cut into the marketshare that established funders have had for years. Suddenly they’re the hottest thing in town, that is until about 6 months later when they start telling their “loyal” broker shops to stop sending in new deals for a while. As the newbie’s joyride comes to an end, the established funders roll their eyes and continue on the way they always have, responsibly.

We’re not here to point anyone out or to suggest that brokers purposely send bad paper to an inexperienced funder. It’s just easy to spot the amateurs. Sadly, most people laugh at them behind the scenes until the funder calls it quits, completely unaware that they’ve been wearing a “kick me” sign on their back for months.

This could be an uncomfortable topic for some, but this rapid rise and fall scenario plays out across many industries. If your business is less than two years old, ask yourself this: Is your success a result of awesomeness or do you smell a tinge of red cherry marker?

—————

Does anyone know what the truth is anymore? These contradictory articles were both published yesterday by reputable news media outlets:

Banks Keep Lending Standards Tight For Small Firms

Fed Says Banks Ease Standards On Business, Consumer Loans

Is affirmative action coming to a funder near you?

Dodd-Frank’s small business lending time bomb

Growth in the usage of MCAs (selling future sales for cash upfront) is taking a huge chunk of market share away from traditional lenders.

Some crusty old reporters remain clueless as to why fewer and fewer businesses are turning to their banks for loans. Professor Scott Shane in BusinessWeek fumbled through his recent 700 word article in which he makes several unconvincing arguments for credit cards as being the new holy grail for business owners. Ultimately, he concedes that the decrease in small loans to businesses might simply be a benign statistical anomaly. This guy is a professor??!! Borrow, Borrow, Loan, Loan, Loan. Some people still can’t imagine a world where leveraging can happen without a borrower and a lender.

—————

Have you ever tried to peg down what exactly is happening in the credit markets? The National Federation of Independent Business has already done a lot of the work for you. A few clues:

- Small-business owners are increasingly employing personal rather than business cards for business purposes

- Fifty-seven (57) percent of small employers attempted to obtain credit from a financial institution in the last 12 months, a nine percentage point increase from 2010 with the demand for lines and cards each rising more than one-third. The demand for line renewals and loans were flat. More attempts resulted in more rejections rather than more small-business owners obtaining credit

- Poorer credit risks were more likely to try to borrow in 2011 than better credit risks, other factors equal. A number of financial factors, such as credit score, differentiate the two groups. Men and owners of larger small businesses were also more likely than their counter-parts to try to borrow

Download the full 76 page NFIB January 2012 report

—————

Some MCA underwriters hate when merchants state they aim to use the funding proceeds for “cash flow” as if its unspecific nature was code for betting on the horses. In the traditional lending world, businesses have been offering that up as a purpose for decades. From the NFIB Report:

– Merchant Processing Resource

https://debanked.com

The Funders of Summer

August 2, 2012What’s new? Who funded? What happened? Merchant Processing Resource will try to give you a glimpse into the Merchant Cash Advance (MCA) universe:

We all know salespeople love to fund, but underwriters?!! This banner hangs on the wall of the underwriting department at mid-sized MCA firm, Rapid Capital Funding:

Holy Moses Batman! $10 Million in a month?! Yellowstone Capital is reporting a new personal monthly funding record of $10,245,000.

There has been an influx of really creative instructional/promotional videos about MCA lately. Cartoons are really “in” right now:

PayPal white labeled a Merchant Cash Advance program in the U.K.

Will the mega banks be next?

It feels like 2006 all over again says First Annapolis Consulting in a recent article:

This seems to be the same bullish sentiment that surrounded the industry in 2006, when there was a constant influx of new MCA providers into the industry and what appeared to be unlimited financial sources. What might be different now is the experience accumulated in the industry during the recession. In the last few years, and as a result of the mounting losses that the industry suffered during the economic crisis, MCA players have implemented more conservative risk management practices and procedures.

Underwriters industrywide are also reporting that stacking, splitting, double funding, and fake statements are on the rise. It certainly brings back some nostalgia for veterans and not the good kind. A screenshot of a current ad on craigslist that is directed at bad apple merchants:

A new chapter opened for Merchant Cash Advance (This is soooo last month but a great read if you missed it).

http://greensheet.com/emagazine.php?issue_number=120602&story_id=3088

Is the loan shortage a banking problem or a merchant problem? Ami Kassar makes the case in his New York Times column.

“Where are the leads? I need the leads. Can you tell me where the leads are?” We literally get asked daily where to get leads from. We recommend:

http://SmallBusinessLoanRates.com

http://meridianleads.com

By the way… for every company that says cold calling doesn’t work, there’s a company getting rich doing just that. Same goes for SEO, mailers, e-mail blasts, PPC, and so. Marketing is an art form. Just because it doesn’t work for you, doesn’t mean it doesn’t work period. Keep doing what you’re doing. Too many ISOs/agents/marketing directors abandon campaigns after 30-60 days. Practice makes perfect!

Have you abandoned social media? We ask this question: What looks worse to a prospect?

Not having a business twitter account or having one but failing to tweet at all in the last 8 months?

Not having a business blog or having one but failing to add any new blog posts in over a year?

We didn’t spend much time researching hard data but we would surmise that freshness is a psychological component to a prospect’s shopping experience. If a business blogged regularly on their site up until May, 2011 and then stopped, might a merchant think the entire business itself is abandoned or gone? Is a facebook fan page with 1 post from 8 months ago a positive or negative selling point? WE SAY: If you build it, maintain it. Nothing brings down your presence on the Internet like abandonment. We understand that smaller companies might not have the manpower, time, or creative energy to write informative articles or engage people through social networking, especially when it’s hard to measure the results and value it creates. Consider the value you might actually be losing by projecting to the world that you have given up. It’s like operating a store with a sign out front that says “THIS BUILDING HAS BEEN CONDEMNED” even though you are actually open for business. If WE stopped posting articles for a year, would you still come back several times a month?

Here are two examples of MCA firms that keep it FRESH!:

http://unitedcapitalsource.com/blog/

http://takechargecapital.com/category/blog/

Don’t you just love MCA? We do! Visit our site again soon.

– Merchant Processing Resource

https://debanked.com

The Other 93%

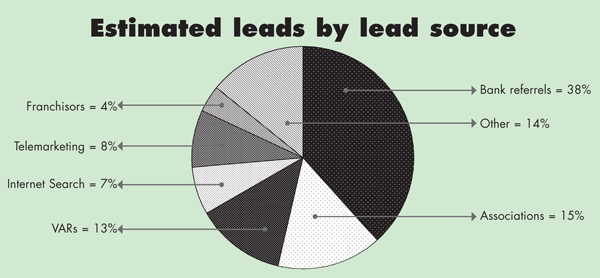

July 13, 2012The SEO war rages on for Merchant Cash Advance providers, ISOs, micro lenders, and other financing firms, but just how much real estate is everyone really fighting over? According to data recently provided in The Green Sheet by First Annapolis Consulting, only 7% of all merchant account leads are generated via the Internet. So if your business plan’s success hinges on getting to page 1 of Google search, you might be shutting yourself out from nearly the entire marketplace. Don’t get us wrong, there’s a lot of money to be made and business to be acquired via the Internet, but even the big firms get roughed up from time to time by competition, new algorithms, and SEO companies that promise the world but deliver few results.

So if not the Internet, then what else is there besides cold calling? That’s a question that tons of small ISOs ask themselves when they realize that competing online isn’t easy. It just so happens that the “what else” comprises of 85% of all generated leads in the payments industry. More than 50% are derived from bank referrals and associations alone.

Has anyone ever wondered why companies like AdvanceMe (Capital Access Network) are still number one in the Merchant Cash Advance arena? They’ve managed to defy Darwin’s theory of evolution. In every industry, there is a pioneer that leads the way, gets too comfortable, stops innovating, and is systematically made irrelevant by fresh thinking competition. There was MySpace until there was Facebook. There was Yahoo until there was Google. There was AOL until…there was just everything else.

So one would expect that in 2012, the mere mention of AdvanceMe would be part of a requiem for the founding fathers of the Merchant Cash Advance industry. That isn’t the case and is quite the opposite considering they are on pace to fund at least $700 million this year. So they must be #1 on Google, right? Nope. For all of the main keywords that people are fighting over, they rarely if ever, even show up on the first page of the results.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

All the sales pitches in the world about lower rates and free POS systems aren’t going to compete with a merchant who has just been given a referral by a company they already have a relationship with. Hell, even you have probably enlisted an insurance company, wedding vendor, or mortgage broker because someone you trusted said they were great.

This isn’t another lecture about how referrals are crazy good and that cold calling is wicked bad, especially since we don’t even necessarily feel that way. The point is really to highlight just how much more potential there is out there for small funders and ISOs. You can actually be successful with a sucky website and no SEO if you can just solidify some key relationships.

If you want to be around 14 years later, you can’t ignore the other 93% of the market. The volume of Internet leads will probably increase in the future as more computer savvy people become small business owners. But it’s way too easy to set up a website, hire an SEO guy, and throw money at Pay-Per-Click. Anyone can do it and everyone is doing it. That means most companies are losing the battle and tons of you are saying “what else is there?” Fortunately, the lead generation pie chart offers unlimited hope. You just need to think bigger and try harder.

If the other categories seem too ambitious, well then you’ll never make it in this biz kid…

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource