Kalamata Capital Merges with Kings Cash Group

June 28, 2018 Kalamata Capital announced today that it has entered into an agreement to merge with Kings Cash Group, effective July 1. The new entity will be called Kalamata Capital Group, or KCG, retaining the Kalamata Capital brand. Together, the new entity and its affiliates will provide approximately $300 million of capital annually to over 5,000 small businesses.

Kalamata Capital announced today that it has entered into an agreement to merge with Kings Cash Group, effective July 1. The new entity will be called Kalamata Capital Group, or KCG, retaining the Kalamata Capital brand. Together, the new entity and its affiliates will provide approximately $300 million of capital annually to over 5,000 small businesses.

Michael Jaffe and Albert Gahfi have been designated the co-Presidents of Kalamata Capital Group LLC, the direct funding and operating entity, and they will run the day-to-day operations. Steven Mandis, Brandon Laks, Carlos Max, and Connor Phillips will be the Chairman, Chief Operating Officer, Chief Financial Officer, and Chief Credit Officer, respectively, of the holding company, Kalamata Holdings LLC. All are members of the Executive Committee of Kalamata Holdings LLC.

“With this partnership we become the preeminent one stop solution for merchants and strategic partners in the industry,” Gahfi said. “Strategic partners can submit one application, and we will quickly develop competitive, actionable solutions.”

Laks, Chief Operating Officer of KCG told deBanked that employees of both companies will be retained and the former Kalamata Capital offices, both in Bethesda and New York, will remain in place. The Manhattan office of Kings Cash Group will also remain and all products that the two companies used to offer separately, will now be offered by KCG, including small business loans, SBA loans, factoring, equipment leasing and merchant cash advance, among others. Kalamata Capital offered all of these products while Kings Cash Group focused on merchant cash advance.

“With no debt, Kalamata Capital has one of the strongest balance sheets in the industry,” Jaffe, co-President of the newly formed KCG said. “Their Chairman Steven Mandis worked at Goldman Sachs, was a Senior Advisor to McKinsey, has a PhD from Columbia University and teaches at Columbia Business School. He has utilized that experience to build a distinctive partnership culture, established brand, and institutional-grade processes and procedures.”

Mandis, Chairman of KCG, said: “We know and value KCG’s technology platform and people, and we believe their talent and capabilities will further strengthen our overall merchant value proposition. The partnership will enable us to better serve more small businesses by enhancing our underwriting capabilities to provide access to affordable business financing solutions to help them and their communities grow and thrive.”

American Express Partners with Amazon on SMB Credit Card

June 28, 2018 American Express announced plans this week to partner with Amazon to introduce a co-branded Amazon credit card for small businesses. Amazon does have a co-branded card with J.P. Morgan Chase for consumers shopping on Amazon’s site, and elsewhere. But this would be Amazon’s first card for small business owners.

American Express announced plans this week to partner with Amazon to introduce a co-branded Amazon credit card for small businesses. Amazon does have a co-branded card with J.P. Morgan Chase for consumers shopping on Amazon’s site, and elsewhere. But this would be Amazon’s first card for small business owners.

“At American Express, we have been helping business owners grow for more than 50 years and we know that millions of them rely on Amazon,” said Glenda McNeal, President of Enterprise Strategic Partnerships at American Express in a statement. “We’re delighted to expand our partnership with Amazon by offering a new cobranded small business card, and by also harnessing the collective insights and expertise of our companies to deliver tangible value to our mutual customers who use Amazon’s services.”

This was quite a win for American Express as J.P. Morgan was competing for this partnership as well, according to CNBC. This deal puts American Express in an enviable position to court more small business customers in its effort to become a leading lender to small and mid-sized companies. Small business cards can be very lucrative for banks. Compared to consumers who might spend a few thousand dollars a month on credit cards, businesses can spend up to hundreds of thousands of dollars in monthly bills, according to CNBC.

“We selected American Express as our partner for the upcoming small business credit card because of our shared commitment to helping small businesses grow,” said Max Bardon, Vice President at Amazon in a statement. “Offering the best of both brands, the cobranded small business credit card program will combine the buying power, convenience and value small businesses have come to know and love from Amazon backed by the world-class service, benefits, access and security of American Express.”

Amazon launched Amazon Lending in 2011 to help small businesses finance and sell more goods on its platform. From the 2011 launch to June 2017, Amazon Lending reported that it issued $3 billion across 20,000 business in the US, Japan, and the UK. And the bulk of the growth has been from small businesses in the US, where the company originated $1 billion in loans in 2017 alone. So small business lending, particularly in the US, is big business for Amazon.

This new co-branded Amazon/American Express card for small businesses is part of a series of new partnerships between the e-commerce behemoth and banks. In February of this year, it was reported that Amazon had partnered with Bank of America Merrill Lynch to provide loans to merchants (on an invitation-only basis) from $1,000 to $750,000.

LendingPoint Gets Increase in Financing

June 28, 2018

LendingPoint announced today that it closed an increase of its mezzanine financing, bringing the total of the facility from Paragon Outcomes Management to $52.5 million. Mezzanine financing is a hybrid of debt and equity financing. Paragon and LendingPoint initiated a relationship with its first credit facility in January 2017 for $20 million. It was then upsized seven months later, and has now been upsized for the second time to $52.5 million.

“We believe this shows a tremendous amount of confidence in the way our portfolio continues to perform,” LendingPoint Chief Marketing Officer Mark Lorimer told deBanked. “It’s a great vote of confidence.”

Among other things, the new credit facility provides an increased advance rate for more efficient equity usage. Today’s announcement comes on the heels of more than a billion dollars worth of senior credit financing that LendingPoint has closed in less than a year. The company secured an up to $500 million senior credit facility in August 2017 and an up to $600 million senior credit facility last month, both arranged by Guggenheim Securities.

“[Paragon’s] support has been critical as we grow our origination volume and balance sheet, and march towards profitability next year,” said Tom Burnside, LendingPoint co-founder and CEO. “We’re proud that LendingPoint’s performance to date means companies like Paragon Outcomes want to be part of our future.”

In March, LendingPoint debuted a point of sale lending platform for merchants that Lorimer said is going well.

“We’re continuing to build it out, add more merchants to the platform and increase the funding levels,” Lorimer said.

Founded in 2014 and based in Kennesaw, GA, LendingPoint and its Merchant Solutions platform have originated more than 70,000 loans totaling more than $500 million.

Facebook Reverses Cryptocurrecy Ad Ban

June 27, 2018 Back in January, Facebook decided to ban all ads for cryptocurrencies. Yesterday, the social media giant changed its mind. In a post on its blog yesterday, the company stated that it will now “allow ads that promote cryptocurrency and related content from pre-approved advertisers. But we’ll continue to prohibit ads that promote binary options and initial coin offerings.”

Back in January, Facebook decided to ban all ads for cryptocurrencies. Yesterday, the social media giant changed its mind. In a post on its blog yesterday, the company stated that it will now “allow ads that promote cryptocurrency and related content from pre-approved advertisers. But we’ll continue to prohibit ads that promote binary options and initial coin offerings.”

The official new policy read: “Ads may not promote cryptocurrency and related products and services without our prior written permission.”

“Advertisers wanting to run ads for cryptocurrency products and services must submit an application to help us assess their eligibility,” Rob Leathern, Facebook’s Product Management Director, wrote in the official blog post. “[This includes] any licenses they have obtained, whether they are traded on a public stock exchange, and other relevant public background on their business. Given these restrictions, not everyone who wants to advertise will be able to do so. But we’ll listen to feedback, look at how well this policy works and continue to study this technology so that, if necessary, we can revise it over time.”

The January ban, also laid out in an official company blog post, said: “Ads must not promote financial products and services that are frequently associated with misleading or deceptive promotional practices, such as binary options, initial coin offerings, or cryptocurrency.”

Facebook acknowledged in yesterday’s company blog post that the wording of its January ban was “intentionally broad” as they continue to work to better detect deceptive and misleading advertising practices.

Funding Circle Expands Partnership with INTRUST Bank to Support More US Small Businesses

June 27, 2018

Yesterday, Funding Circle and INTRUST Bank announced the next phase of their strategic partnership, which helps provide capital to American small businesses. This second phase increases INTRUST’s funding commitment and initiates a targeted, co-branded marketing campaign, giving business owners across Kansas, Missouri, Oklahoma, and Arkansas greater access to fast and flexible financing. To date, over 150 American small businesses have received loans backed by INTRUST through the Funding Circle platform. This new increased commitment is anticipated to bring the number of funded small businesses to more than 500.

“This collaboration is a good example of the ways traditional and innovative financial service providers can work together to help small businesses prosper,” said Chief Financial Officer of INTRUST Bank Brian Heinrichs.

“Not only has INTRUST recognized the investment opportunity available through the Funding Circle platform, but this expansion underscores that Funding Circle’s loans are often the best option on the market for American business owners seeking growth capital,” said Funding Circle’s US managing director, Bernardo Martinez. “We view our partnership with INTRUST as a blueprint for the remaining geographies within the US.”

Funding Circle has been among the top five alternative small business funders in the US over the last several years. And earlier this month, the company released a report that demonstrated the demand for alternative financing among small business owners.

Founded in 2010, Funding Circle is a small business loans platform in the US, UK, Germany and the Netherlands, that matches small businesses that want to borrow with investors who want to lend. Investors include more than 70,000 retail investors, banks, asset management companies, insurance companies, government-backed entities and funds worldwide.

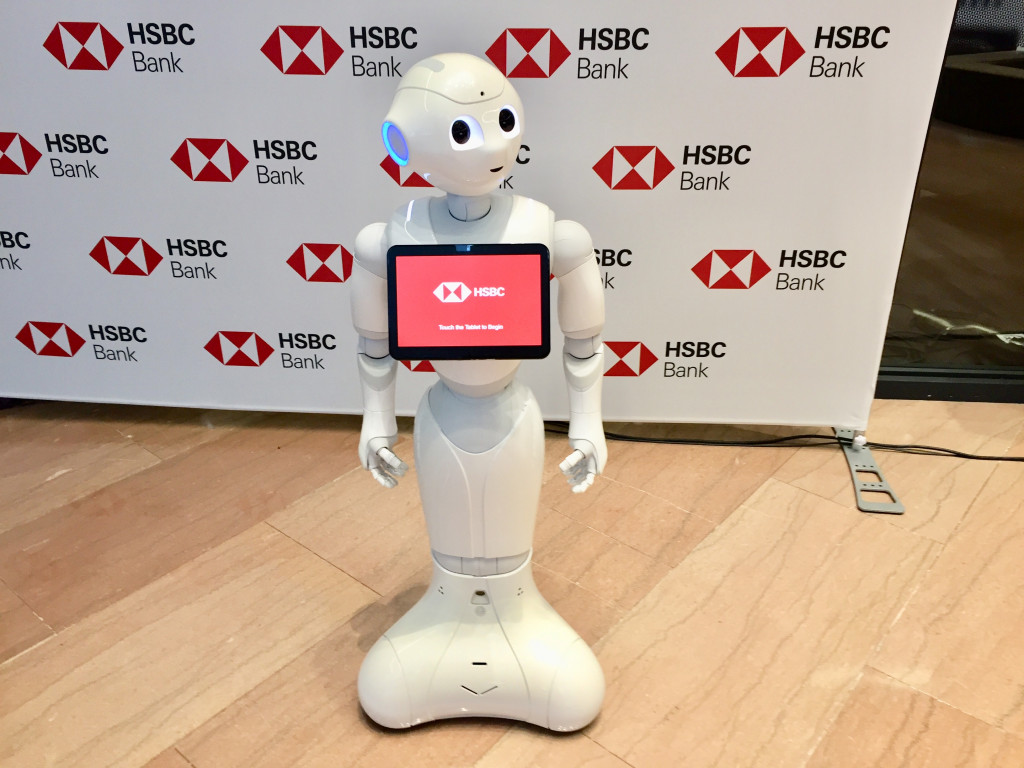

HSBC Bank and SoftBank Robotics America Welcome “Pepper” the Robot

June 26, 2018 A partnership between HSBC Bank and SoftBank Robotics America came to fruition this morning when a robot named Pepper was introduced to media at HSBC’s North American flagship retail branch on Fifth Avenue in midtown Manhattan.

A partnership between HSBC Bank and SoftBank Robotics America came to fruition this morning when a robot named Pepper was introduced to media at HSBC’s North American flagship retail branch on Fifth Avenue in midtown Manhattan.

“Thank you for joining us to make history today,” HSBC Head of Innovation Jeremy Balkin said at the flagship bank.

Pepper is the first robot to operate at a retail bank in North America, according to Julien Seret, VP of Global Product at SoftBank Robotics America. Pepper is four feet tall and can hear, speak and move its head to simulate eye contact. You can interact with Pepper by speaking to it or by tapping the tablet on its chest.

“We’re not replacing people, we’re giving them more time to do what they’re good at,” Seret told deBanked.

Seret said that there are already 15,000 Pepper robots being used in throughout the world, many of them in the hospitality industry. There is a Pepper robot that greets visitors at the Mandarin Hotel in Las Vegas and at least one at the Oakland airport in California. They are helpful to provide any repetitive information and are also used at hospitals.

“Pepper is great for engagement with kids,” Seret said of children at hospitals.

“Pepper is great for engagement with kids,” Seret said of children at hospitals.

Pablo Sanchez, Head of Retail Banking at HSBC, said that HSBC staff brought Pepper outside on the street yesterday for two minutes and 200 people surrounded the robot. Of the onlookers, one came in to learn more about HSBC’s products and then opened multiple accounts. With foot traffic at the Fifth Avenue flagship branch of 18 million people a year, part of Pepper’s appeal is to draw in potential customers.

“But [Pepper] is not just a gimmick,” Sanchez said.

Right now, Pepper mostly serves the role of a knowledgeable greeter, answering questions like “Where can I deposit a check?” Pepper will tell people where to find the ATM machines. But Sanchez said that down the road Pepper could help people open accounts.

While Pepper is capable of facial recognition and collecting and storing other data, Pepper doesn’t that because of privacy laws that SoftBank Robotics and HSBC must abide by and are very respectful of, said Head of Studio at SoftBank Robotics Omar Abdelwahed. But Abdelwahed said that Pepper would be capable of recognizing a regular hotel guest, knowing that the guest is part of a loyalty program and then upgrading the guest’s room.

A Pepper robot is $25,000 to buy, although SoftBank is mostly using a leasing model where users pay about $16,000 for the robot.

Why KeyBank Acquired Small Business Lending Platform from Bolstr

June 25, 2018

KeyBank announced last week the acquisition of a digital lending platform for small businesses created by Bolstr. The lending platform will allow KeyBank to more efficiently serve small businesses for their SBA and traditional lending needs, according to Jamie Warder, Head of KeyBank Business Banking.

“We found Bolstr to have a very flexible capability…and we believe that having the platform will allow us to get to a decision faster,” Warder told deBanked.

Founded in 2010 by Charlie Tribbett and Larry Baker in the Chicago area, Bolstr created a marketplace that connected small business borrowers to institutional and retail accredited investors, or individuals. KeyBank acquired the platform that facilitated this, but not the company. Bolstr no longer operates as it had, but it will continue to work with its current clients, according to Warder.

Warder said that with this acquisition, KeyBank, a regional bank, hopes to attract more small business customers who are looking for speed and ease in obtaining a loan. He thinks that with Bolstr’s platform, KeyBank can be more competitive, although he didn’t say that the bank’s qualifications for obtaining loans would necessarily change.

Warder said that with this acquisition, KeyBank, a regional bank, hopes to attract more small business customers who are looking for speed and ease in obtaining a loan. He thinks that with Bolstr’s platform, KeyBank can be more competitive, although he didn’t say that the bank’s qualifications for obtaining loans would necessarily change.

The Bolstr platform includes features like easy eSignatures, information gathering and digital questionnaires. Already, KeyBank has hundreds of thousands of small business customers, Warder said. The bank, which is headquartered in Cleveland, OH, is more than 100 years old and operates in 15 states.

An ISO Brokers Main Street Deals – on Main Street

June 25, 2018 Envision a giant office filled with rows of commercial finance brokers on the phone, aggressively selling deals to faceless small town merchants. Then step into the office of Horizon Financial Group and meet brothers and business partners James and John Celifarco. The contrast could not be more striking.

Envision a giant office filled with rows of commercial finance brokers on the phone, aggressively selling deals to faceless small town merchants. Then step into the office of Horizon Financial Group and meet brothers and business partners James and John Celifarco. The contrast could not be more striking.

The most dramatic difference between their office and that of almost every other broker, or ISO, is that you enter the office from the sidewalk. There’s no lobby and no elevator. It’s just the two brothers (plus one salesperson and one assistant) working on the other side of a glass storefront window.

The store isn’t on Madison Avenue or Rodeo Drive. It’s on a modest, roughly three-block commercial strip on Avenue S in a working class section of Brooklyn called Marine Park. There’s a deli, a pizzeria, a barbershop, a pet grooming store and a bunch of other stores that you’re likely to find on Main Street, U.S.A. In other words, Horizon Financial Group’s neighbors are the exact kind of small business owners they seek as customers. And since they opened up shop on this quaint stretch at the end of October, many of their store owner neighbors have already become customers.

The store isn’t on Madison Avenue or Rodeo Drive. It’s on a modest, roughly three-block commercial strip on Avenue S in a working class section of Brooklyn called Marine Park. There’s a deli, a pizzeria, a barbershop, a pet grooming store and a bunch of other stores that you’re likely to find on Main Street, U.S.A. In other words, Horizon Financial Group’s neighbors are the exact kind of small business owners they seek as customers. And since they opened up shop on this quaint stretch at the end of October, many of their store owner neighbors have already become customers.

“It’s a different relationship with the customer,” James said of their neighborhood clients. “You’re not on the phone. You’re face to face with these people. You’re meeting them, you’re shaking their hands, you’re getting to know them personally, which helps with the longevity of the relationship itself.”

Sitting at the glass conference table by their storefront window, James, 34, and John, 37, counted up to six clients by simply pointing out the window at other small stores across the street. Horizon Financial Group is an ISO that brokers working capital deals and does credit card processing, equipment leasing, ATM machines and commercial mortgages. (James has his New York real estate license, so he can also help local store owners buy or sell a house.) The brothers said that about 40 percent of their business is facilitating deals brought to them by other ISOs, another 40 percent comes from merchants that they find directly, and about 20 percent comes from these local customers they’ve developed from having a physical presence in the neighborhood.

“Obviously you can’t build an entire business on just these two streets,” John said, “but it’s extra business that we wouldn’t have had if we weren’t here. And when we came here, we stopped thinking ‘Who are we going to buy leads from?’ and started thinking more outside of the box.”

An example of this was their decision to approach the Brooklyn Chamber of Commerce where they are now one of the chamber’s preferred vendors, which brings them business from the entire borough.

James said they’ve made contributions to the local little league and kids football, and whenever a new store opens in the area, they introduce themselves and explain what they do. It also doesn’t hurt that they grew up in Marine Park, so they already know the town pretty well. James recognized someone on the sidewalk and ran outside to say hi. It was someone who used to be a next door neighbor. There is a truly old-fashion sense of community on Avenue S.

“I buy my pizza from [the pizza store owner] and he does his credit card processing with us,” James said. “When the dry cleaner needed equipment, we got them capital, and I actually got to see the piece of equipment I helped finance. That almost never happens.”

Because there is no building guard or front desk person, customers can stop by whenever they like. As if in a sitcom, a man walked into the store saying to the brothers, “Don’t be mad at me.” It was a customer, the owner of a local paint store. “It’s not completely my fault, but I broke the phone swiper on the job.”

Because there is no building guard or front desk person, customers can stop by whenever they like. As if in a sitcom, a man walked into the store saying to the brothers, “Don’t be mad at me.” It was a customer, the owner of a local paint store. “It’s not completely my fault, but I broke the phone swiper on the job.”

Reassuringly, John told him to come to his desk and he helped the customer with a replacement for a piece of credit card processing equipment.

The brothers have each been working in the small business financing industry independently for more than a decade. James established Horizon Financial Group by himself in 2009 while John was working for a different company in the credit card processing and MCA space. John joined James at Horizon Financial Group in September 2017.

John said he prefers co-leading Horizon Financial Group, itself a small business, to running a larger operation in Manhattan.

“Compared to somebody in the city with a huge rent and a huge payroll, I don’t need to do the same numbers he’s doing to end up making the same amount of money.”

John also noted that he doesn’t have to sit on a train for an hour and a half because he lives just six blocks away from the storefront office.

“A lot of people don’t like to say they’re a small company,” John said. “I couldn’t be happier that we’re a small company.”

Running a small business is familiar to the Celifarcos. Horizon Financial Group gets its name from Horizons Dance Center, a successful Brooklyn dance school founded by James and John’s mother. It has been in business for 46 years and is still going strong.

“The name is good luck,” James said.

James lives a short drive away in Rockaway with his wife and daughter. On running a small business like Horizon Financial Group, James said: “It’s also about quality of life. You don’t need to work 7 to 7. I can be on the beach with my daughter. It’s really a different approach.”