Congressman Cleaver’s Findings on Fintech Lending Mixed

August 30, 2018 Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

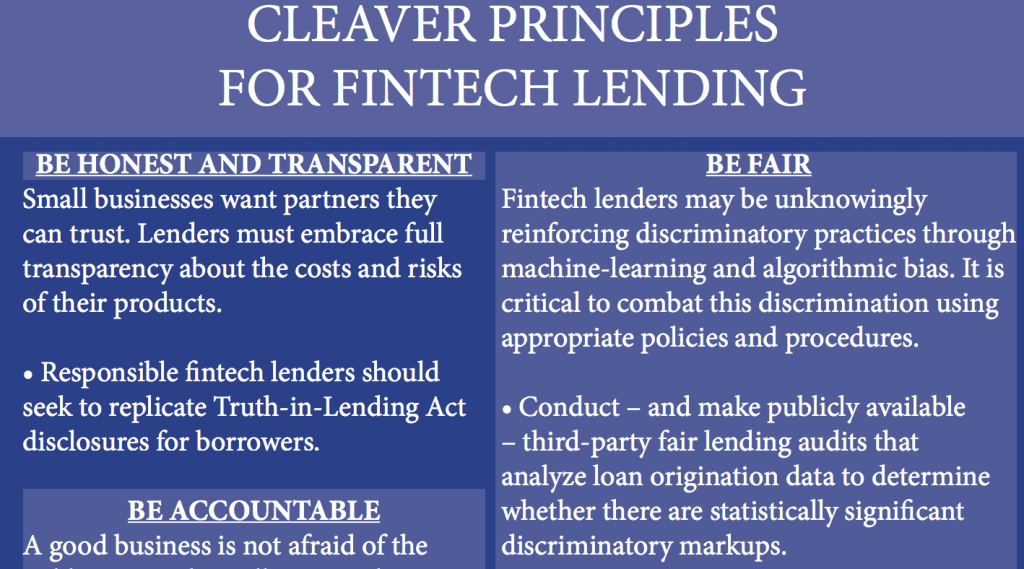

Cleaver concluded that some common practices in non-bank underwriting processes lend themselves to discrimination against minority business owners. One such practice is using a merchant’s personal credit score to determine a business’ credit worthiness, which the report maintains is unfair because “a personal credit score has little bearing on a business model or the owner’s business acumen, and using it unfairly punishes minority business owners who may not have had the same opportunities to build credit.” Another complaint is the common practice of having merchants sign forced arbitration clauses that forbid the borrower to take the lender to court.

The companies that he surveyed included OnDeck, Kabbage, Fora Financial, Lending Club, Biz2Credit and LendUp, even though Lendup only does consumer lending. And OnDeck, Kabbage and Lending Club don’t offer a cash advance product. Still, they make non-bank business loans.

The report also mentioned that algorithms used by some of these companies could inadvertently be discriminatory. That’s because they have the ability to incorporate the number of criminal records and bankruptcies in the merchant applicant’s zip code when making a funding decision. And these numbers tend to be higher in minority neighborhoods.

However, the report also highlighted some good practices, such as including a third party in the lending process to protect from engaging in unintentional discriminatory behavior.

“From the responses gathered,” the report reads, “it has become increasingly clear that a majority of the companies have taken some measure to prevent blatant discrimination. Nevertheless, additional protections are very much needed.”

“The initial findings are clear as day, Congressman Cleaver said in a statement about the report. “We need to further understand how lenders may be intentionally or unintentionally offering higher interest rates to minorities and underserved communities, and work to implement industry-wide best practices.”

Two-Thirds of Daily Crypto Trade Volume May Be Fake

August 27, 2018 Two-thirds of daily trade volume in cryptocurrency is faked, according to research published this month by the Blockchain Transparency Institute (BTI). This translates to $6 billion a day, according to the report. What this likely means is that the exchanges themselves are quickly buying and selling cryptocurrency to give the illusion of high activity on the exchange when, in fact, there may be relatively little.

Two-thirds of daily trade volume in cryptocurrency is faked, according to research published this month by the Blockchain Transparency Institute (BTI). This translates to $6 billion a day, according to the report. What this likely means is that the exchanges themselves are quickly buying and selling cryptocurrency to give the illusion of high activity on the exchange when, in fact, there may be relatively little.

The advantage of creating this illusion is to make it more attractive for actual cryptocurrency investors to buy on a given exchange, which is how the exchange makes money – from taking a percentage of each transaction. This practice of buying and selling to oneself (or to colluding parties) in an effort to mislead others, is called “wash trading,” and is illegal.

The report states that “over 70% of the CMC top 100 is likely engaging in wash trading by at least 3x their stated volume.” Given that most cryptocurrency exchanges are not regulated, this alleged wash trading may not come as a surprise to many. But if this is accurate, the magnitude of this fake trading is significant. Coinbase and Binance were not suspected to be wash trading, according to the report.

The exchanges that are considered to be accurate by the report typically have a volume/user to unique visitor ratio of around between 2% and 5%, whereas suspect exchanges ratio ranged from 10% to over 655,000%.

Sylvain Ribes, a Cryptocurrency investor and writer who is cited in the report, wrote in a March 2018 Medium blog post of his surprise between the differences in trading volume among exchanges.

“Where I had expected mild differences between currencies, I found ridiculously massive discrepancies between exchanges,” Ribes wrote. “Not the kind that can be easily hand-waved away (‘oh well, their users must behave differently’), but the kind that can only be explained by some figures being overstated as much as 95%.”

IOU Financial Profitable, Again

August 23, 2018

IOU Financial originated $29.2 million during Q2 2018, according to the company’s quarterly financial statement released today. This is an increase of 11.6% compared to the same period last year, and an increase of 19.1% over originations of $24.5 million from last quarter. This is also IOU’s third consecutive quarter with positive earnings.

“It’s the contribution from our team, our account executives, broker partners [and] product expansion,” IOU CEO Phil Marleau told deBanked as an explanation for the company’s growth.

Marleau said that over the past year IOU has been originating loans for larger amounts and for longer terms, like longer than 12 months. He also said IOU has been expanding into new industries.

Benjamin Yi, who leads IOU’s Capital Markets & Corporate Development efforts, characterized the company’s results as a “mini version of OnDeck,” alluding to OnDeck’s profitable 2018 Q2 earnings report.

Additionally, provision for loan losses (net of recoveries) decreased by 61.2% to $900,000 for the three month period ending June 30, 2018. Marleau said this is largely because the company has been using a more aggressive litigation strategy against businesses that default on their loan obligations.

And the principal balance of IOU’s servicing portfolio (loans being serviced on behalf of third-parties) amounted to approximately $44.1 million compared to $24.1 million in 2017. Marleau said that servicing loans is part of IOU’s business model and that this near doubling of its servicing portfolio in a single year is simply a reflection of the overall growth of the company.

Most of IOU’s revenue comes from making loans, of up to $300,000, to American small businesses. According to the company website, almost half of IOU’s merchants use the business loans to purchase equipment. Other loans are used for business expansion and temporary cash flow. To date, IOU has originated $563 million in loans.

Despite the focus on the American market, the company’s headquarters is in Montreal and its stock is listed on the Toronto Stock Exchange. While IOU’s footprint in the Canadian market is still very small, Marleau expects that to change and is looking forward to expanding in Canada.

“We’re part Canadian,” Yi said.

Marleau, who is Canadian, met cofounder and IOU President Robert Gloer at a fintech conference in San Francisco, and the company’s first loan was made in 2009. Gloer had ties to Atlanta, which is why IOU’s U.S. office is located there. While the company’s headquarters is in Montreal, the Atlanta office is larger and is where the company’s sales operations take place. The company has about 40 employees, but only about ten work at the Montreal headquarters.

UCS-BizBloom Deal Could Be First of Many

August 21, 2018United Capital Source (UCS) was chosen to service BizBloom’s book of business, according to UCS CEO Jared Weitz. After BizBloom’s president, Thomas Costa, stepped down, the company’s main investor assumed control and arranged for the company’s portfolio of merchants to be serviced by UCS. Weitz told deBanked that he was familiar with the BizBloom investor previously.

“When [they] reached out to me, I knew it was something we would be able to do,” Weitz said. “Between the experience of our account reps, our CRM, our technology that helps us, and our existing relationships, we knew we could take on the additional work, no problem.”

UCS will now control servicing BizBloom’s old portfolio, helping to place renewals. Weitz said he has a confidential financial arrangement with them.

“This type of arrangement is extremely common in finance,” Weitz said. “For instance, when Bizfi went out of business, Credibly was servicing their portfolio.”

While UCS is not known as a servicing company and Weitz said that he is not looking to turn UCS into a servicing company, he said that he is interested in doing more of this.

“It got me thinking that if there are any additional ISOs out there that aren’t growing, aren’t happily performing, or are just looking to get into something else, but have an existing book, UCS would look to service that as well,” Weitz said.

It turns out that BizBloom’s merchants are very similar to the ones that UCS services. And many of the merchants are funded by the same companies that UCS already has relationships with. When UCS opened in 2011, they initially brokered cash advance deals exclusively. But since then, they have added equipment financing, business term loans, business lines of credit and factoring, among other products. They service merchants in a variety of industries, from fitness centers to hotels to gas stations. According to Weitz, 98% of the company’s leads come from its internal marketing team.

Credit Karma Moves Towards Home Mortgages with Acquisition

August 20, 2018 Credit Karma acquired Approved last week, according to a blog post written by Approved CEO and founder Andy Taylor. Approved is a platform that simplifies and facilitates the process of obtaining home mortgage loans.

Credit Karma acquired Approved last week, according to a blog post written by Approved CEO and founder Andy Taylor. Approved is a platform that simplifies and facilitates the process of obtaining home mortgage loans.

“When we left Redfin three years ago to tackle the often painful and tedious process of getting a home loan, nearly everyone in the real estate space was focused on the front end: home search, finding agents and seeing homes,” Taylor wrote. “The industry had lost sight of the fact that a majority of lenders still used fax machines as a regular part of doing business.”

Taylor and co-founder and CTO of Approved, Navtej Sadhal, set out to modernize the process with a number of features including the DocVision Camera which scans documents using the customer’s smartphone.

Both Approved founders had worked at Redfin, a real estate search and brokerage services company, before creating Approved. Taylor and Sadhal will now work for Credit Karma in San Francisco, as Mortgage General Manager and Staff Engineer, respectively.

Founded in 2015, Approved was based in San Diego and originated nearly $5 billion in loans, according to Taylor’s post. It also has reduced document exchange time by 50%, according to the company website.

“Working with Credit Karma gives us the resources and immediate scale to accelerate our mission-driven work, reaching significantly more homebuyers than we could have imagined when we started,” Taylor wrote of Credit Karma’s acquisition of Approved.

Credit Karma, which provides free credit scores and reports, has 80 million members.

The Broker: How Zach Ramirez Makes Deals Happen

August 17, 2018 deBanked interviewed Zachary Ramirez to find out what makes a successful broker like him tick, how he does it, and what kinds of things he’s encountered along the way.

deBanked interviewed Zachary Ramirez to find out what makes a successful broker like him tick, how he does it, and what kinds of things he’s encountered along the way.

Title: Founder and Managing Director of ZR Consulting, LLC, a brokerage of 10 people in Orange County, California.

Years in the industry: 6

Age: 29

Number of brokerage shops he’s started: Three. The first one he created failed after only about three deals, the second one, called Core Financial (that he got in early on with 2 other partners), grew to 27 brokers before it was acquired, and this one is only two months old and has already funded $1 million.

Number of brokerage shops he’s started: Three. The first one he created failed after only about three deals, the second one, called Core Financial (that he got in early on with 2 other partners), grew to 27 brokers before it was acquired, and this one is only two months old and has already funded $1 million.

His morning routine:

I get up at about 5:45.

I have my protein shake – banana, protein, coconut oil and whatever else I can find that seems healthy to me.

I get a cup of coffee.

I sit down at my desk and the first thing I do is look at all the leads that came in that night. Sometimes there’s as many as 80. Sometimes there’s as few as 20 or 25. I then distribute the leads to my sales team, so that as soon as they wake up, they have all their leads. After that, I focus on marketing and closing some of the bigger deals.

Ritual before he closes a deal:

Ritual before he closes a deal:

It’s a funny habit that makes me laugh but before I try to close a deal, I visualize myself closing the deal and I beat my chest. I walk around the office beating my chest like an ape, and it’s just hysterical. I get this big adrenaline rush right before I call the merchant. And when I call them, I’m just on fire. Whatever happens, I’m ready for it. And when I’m in that mode, I can’t lose a deal. It’s like impossible.

His first deal:

It was an auto repair shop that needed $75,000 in order to add three new bays for their repair shop. I think I funded it with OnDeck. It was a very smooth deal. My buddy brought it to me. He said the customer needs the money today. And we ended up funding it the same day. It was great.

I was 23 years old and that was the first time I had seen my business capture any revenue. Finally, after a month or two months of straight working, and not finding a single deal, I finally figured out the marketing a little bit and ended up funding that one. I remember we had 10 points in it, so we had $7,500. I was a single guy renting a room, and for me that was a good chunk of money.

What it taught him:

It helped me learn about expense management because that first broker shop I started failed. I lost everything on that shop. I only funded two or three deals and I ended up spending more money than I made. I was very humbled by this. I realized that being a broker isn’t as easy as people think.

What his best merchants have in common:

My favorite merchants understand why they qualify for what they qualify for. We have a deep rapport. I don’t just talk about business. I’ll talk about their family. I’ll talk about trends I see in their industry. I’ll help them understand their financial situation. And my best merchants are the ones that understand that I’m a source of information for them and I can provide them with valuable insights that they might not be aware of. Things that can help them. I’ll help them with marketing a lot…I say, ‘Look, if you talk to these people, they can do this marketing for you.’ And I do stuff like that because it’s increasing their revenue which helps their business. And that can help me do bigger loans for them.

Largest deal:

Largest deal:

It was a $2 million deal. We had three points in it, so we made $60,000.

Favorite funders:

OnDeck. Also, I really like Fundworks, Quickbridge and Kalamata Capital Group. If someone doesn’t say OnDeck, then they’ve got a problem because OnDeck is amazing.

Why?

Because the consistency of their approvals, their competitive rates, the fast and seamless funding process. And especially, the online checkout. The online checkout is godly.

StreetShares Moves Headquarters

August 16, 2018 StreetShares announced yesterday that it has moved to another location in Reston, Virginia in order to accommodate its growing staff, according to the company’s blog. From January of this year to August, SteetShares says it has doubled the size of its workforce and the new space is 10,300 square feet, more than four times the size of the previous office.

StreetShares announced yesterday that it has moved to another location in Reston, Virginia in order to accommodate its growing staff, according to the company’s blog. From January of this year to August, SteetShares says it has doubled the size of its workforce and the new space is 10,300 square feet, more than four times the size of the previous office.

Established in 2013 in the home basement of CEO Mark Rockefeller, StreetShares offers term loans, lines of credit and a factoring product, with a focus on funding veteran-owned small businesses. Rockefeller is a veteran himself.

According an SEC filing for StreetShares, for the six months ending December 31, 2017, the company generated $1,533,143 in revenue and spent $3,224,131, for a net loss of $2,673,466. The company also received capital at the beginning of 2018, with the completion of a $23 million series B round in January.

StreetShares’ new office has a “tech” aesthetic.

“No cubicles or offices allowed,” Rockefeller said. “Standing desks, teams working together in pods, as well as glass, metal, and exposed concrete reflect a technology startup. And vintage World War II posters and an enormous American flag remind our team of the special members we serve.”

Survey Reveals U.S. Small Business Owner Outlook

August 16, 2018Confidence among small business owners in the U.S. is up, according to a quarterly online survey produced by CNBC and SurveyMonkey. Of more than 2,000 small business owners polled from July 27 to August 5 this year, 58 percent of respondents say business conditions are “good,” up from 53 percent last quarter and up from 39 percent a year ago.

According to the survey, about 33 percent of small business owners anticipate hiring additional full-time employees this year, which is seven percentage points higher than a year ago. Sixteen percent of small business owners said they currently have open positions that they have been unable to fill for at least three months. This CNBC/SurveyMonkey survey polled exactly 2,085 self-identified small business owners 18 and older.