Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Commercial Finance Coalition Tells MCA Industry Story on Capitol Hill

September 23, 2016

Earlier this week, executives and representatives from the merchant cash advance industry met with dozens of policymakers on Capitol Hill. The Fly-In was hosted by the Commercial Finance Coalition, whose members make up a sizable chunk of the industry’s overall transaction volume. It was their second such event this year.

The opportunity allowed industry representatives to get face time with Republicans and Democrats from both the House and the Senate. One message of great importance was in communicating the challenges that small businesses face in trying to access less than $250,000 in working capital. Another was in distinguishing purchase transactions from loans.

“Our members are engaged and committed to educating and advocating the interests of the merchant cash advance industry in Washington DC and state capitals around the country,” said Isaac Stern, President of the CFC and Fundry. “I would strongly encourage my industry colleagues and competitors to get involved in the organization and help us grow the CFC.”

While banks have been accused of being too big to fail, the CFC noted that many businesses have become too small to survive as a consequence of banks moving upstream. Regulations have made it too burdensome and expensive for a bank to underwrite a $25,000 loan, plus they may not be able to stomach the risk or be properly incentivized to approve or decline a loan in the first place. The CFC’s members do not securitize their transactions or sell them off, lending credence to the position that their livelihood depends on small businesses succeeding and performing.

“In less than 9 months the CFC has become the gold standard of alternative small business finance trade groups in Washington,” said Dan Gans, Executive Director of the CFC. “In a short time we have been able to conduct over 50 meetings with key policymakers and assemble a world class regulatory and lobbying team. I would encourage anyone involved in the merchant cash advance or alternative small business finance space to join the CFC and help us advocate for the thousands of small businesses across the country who benefit from the access to needed capital provided by the industry.”

The CFC has not been the only coalition from the broad genre of fintech to host a Fly-In, making it all the more imperative for the MCA industry to educate policymakers on the specifics of what they do and how they do it. For instance, a lot of the regulatory discussion as of late has focused on the partnerships between online lenders and chartered banks, the legitimacy of those partnerships and the sustainability of the algorithms being employed to make quick decisions. While there are several MCA-like products that rely on that model, there is also an entirely different methodology that relies on helping small businesses by purchasing their future receivables. The CFC is one major coalition communicating that distinction.

The CFC is also currently accepting new members to join their cause and participate in future events.

Annual Percentage Rates Fail Business Owners, Again

September 16, 2016 A survey of small businesses once again revealed that Total Cost of Capital (TCC) was a better metric than Annual Percentage Rate (APR) when choosing a small business loan. This study, conducted by Edelman Intelligence on behalf of the Electronic Transactions Association (ETA), found that a majority of respondents stated that they would look to minimize TCC, rather than APR, when considering loan options in the face of a short-term ROI opportunity.

A survey of small businesses once again revealed that Total Cost of Capital (TCC) was a better metric than Annual Percentage Rate (APR) when choosing a small business loan. This study, conducted by Edelman Intelligence on behalf of the Electronic Transactions Association (ETA), found that a majority of respondents stated that they would look to minimize TCC, rather than APR, when considering loan options in the face of a short-term ROI opportunity.

The ETA explained this in the report as follows:

Generally, when consumers take out a loan, they are not making an income-generating investment that would increase the funds available to pay the loan back. Therefore, in most situations, the more “affordable” loan for a consumer is one with a longer term and lower monthly payments, even if it results in paying more over the long term. Consumers, therefore, look at APR, which describes the interest and all fees that are a condition of the loan as an annual rate paid by a borrower each year on the outstanding principal during the loan term. APR takes into account differences in interest rates and fixed finance charges that may otherwise confuse a consumer borrower and is most useful in comparing similarly long-term loans, such as 30-year mortgages or multi-year auto loans. Likewise, APR is useful for comparing revolving lines of consumer credit, like credit cards, where the amount borrowed each month changes. APR allows consumers to compare the rate at which an outstanding balance would increase under different credit cards.

While APR describes the cost of the loan as an annualized percentage, TCC represents the sum of all interest and fees paid to the lender. As the Cleveland Federal Reserve recently noted, TCC enables a small business to determine the “affordability” of a product – a key driver for most small business borrowers. Unlike consumer loans, commercial loans are normally used to generate revenue by helping a business purchase equipment or inventory or hire additional employees. Thus, “affordability” for small business borrowers means assessing the cash flow impact of the loan and comparing the TCC of the loan and the return they expect to earn from investing the loan proceeds. To reduce TCC, many small business borrowers prefer short-term financing they can quickly pay back with the return on their investment (ROI).

The ETA’s full report can be VIEWED HERE.

The findings are consistent with other studies:

Fed study on small business borrowing

A debate with anecdotal evidence, demonstrating people’s inability to calculate an APR

Consumers also struggle to make sense of APR, according to a 2008 Fed study

Barney Frank, Now a Banker, Sounds Like a Champion for Private Lending

September 16, 2016 Barney Frank, the infamous former Congressman whose name still haunts the financial industry through the Dodd-Frank Act, has taken on a surprising role in his retirement from public service. These days he’s on the board of directors of Signature Bank, a Wall Street staple with $33 billion in assets that is ironically becoming known as one of the nation’s fastest growing lenders to private businesses. In fact, it’s the preferred bank of Murder Inc. record label founder Irv Gotti, according to a WSJ story that explained how the bank stood by him even as he was facing federal money-laundering charges. Frank was mentioned alongside Gotti and is reported to have said that he likes the bank’s focus on lending.

Barney Frank, the infamous former Congressman whose name still haunts the financial industry through the Dodd-Frank Act, has taken on a surprising role in his retirement from public service. These days he’s on the board of directors of Signature Bank, a Wall Street staple with $33 billion in assets that is ironically becoming known as one of the nation’s fastest growing lenders to private businesses. In fact, it’s the preferred bank of Murder Inc. record label founder Irv Gotti, according to a WSJ story that explained how the bank stood by him even as he was facing federal money-laundering charges. Frank was mentioned alongside Gotti and is reported to have said that he likes the bank’s focus on lending.

Say what?!

I got to interview Frank personally very briefly two years ago in New York City and got a quick sense of his views on business-to-business transactions; That is that he doesn’t believe small businesses should get the same protection as consumers. In addition to restating his opposition to the Durbin Amendment in his own law, which regulated debit card interchange fees, he was also surprised by my suggestion that some people had floated the concept of federal interest rate caps on business loans. He offered a hard no when I asked him if he would be in favor of that idea. Above all however, he was in favor of transparency.

Frank more recently shared additional thoughts on finance in an interview with the Commercial Observer. “From the standpoint of the economy, the goal is to make sure enough loans are being made and that they’re not too risky. Who makes them is less important,” Frank said. These comments were offered in response to a question about capital constraints interfering with bank lending, to which he explained didn’t matter because the private sector was picking up the slack.

“First of all, the government is not in the business of favoring one sector over another. From the standpoint of public policy, is the demand for loans necessary to fuel economic activity being accommodated? I think it is. […] Although [Dodd-Frank] does give [the nonbank sector] power, there may be some further looking into them. Some people worry about peer-to-peer lending, for example, but this is helping one sector versus another.”

A lot of the complaints people have about his famous law, according to Frank, weren’t even written into the law. They are instead rules created by regulators all on their own. “There’s nothing in the statute that cracks down on commercial regulation,” he said.

Frank, sometimes viewed as one of the most liberal anti-Wall Street politicians of his time says his own bank has been criticized for too much lending, but that he is not deterred because he believe it’s not the irresponsible kind that got wrapped up in the financial crisis that necessitated Dodd-Frank to begin with.

Barney Frank, the man, the myth, the director of the bank. Read the full interview with the Commercial Observer HERE.

A Day of Remembrance for Aviv Henry Boaz

September 13, 2016

On a day that America salutes its first responders, family and friends gathered in Hillside, NJ this past Sunday to raise funds for Hatzalah of Union County while honoring the memory of Aviv Henry Boaz, a former associate of Yellowstone Capital that recently passed away.

Hatzalah is an all-volunteer ambulance squad with many chapters around the country. According to Chief Yudi Abraham, the Union County chapter is actually the largest with 23 EMT responders, 13 dispatchers and 3 ambulances. Funds raised from the event enabled the chapter to replace an ambulance that was very old with a brand new one.

Emblazoned on the side is a dedication to Boaz. His father actually flew in from Israel to bear witness to it. Chief Abraham said the day was about “the tribute to Aviv Henry Boaz.”

Isaac Stern along with Yellowstone Capital’s family and friends made the day possible. “Yellowstone Capital is our largest supporter financially,” said Abraham. And what better way to honor Boaz than to make him a part of something that will help save lives, he added.

More than $80,000 was raised on Sunday.

Marketplace Lending Performance In The Eye of The Beholder?

September 12, 2016A user took to the LendAcademy forum to vent about the high charge-off rate that his Lending Club portfolio was experiencing. He also indicated that the seemingly poor performance has affected his investment strategy and feelings about the platform for quite some time.

Other users commented and soon discovered that he was incorrectly calculating his charge-off rate, so the original user went back and redid his math. The end result? His charge-off percentage was actually lower than he originally hoped to achieve, and much lower than the percentages that he thought he was experiencing.

The original user went from angry to happy even though the actual dollars being earned never changed, only the perception of the performance.

Is performance then in the eye of the beholder?

Why The Quiet Summer Was a Good Thing for ‘Marketplace Lending’

September 11, 2016 A lackluster April turned into an explosive May. And then… well it got kind of quiet there for a bit as loan origination volumes for some lenders dropped.

A lackluster April turned into an explosive May. And then… well it got kind of quiet there for a bit as loan origination volumes for some lenders dropped.

A lot of theories have been challenged, a lot of absolutes shaken. Like given the choice between a short term loan at a high interest rate and a long term loan at a low interest rate, which one would a small business choose? A lot of lenders raised money on the belief that businesses would choose the latter, bolstered by a compelling argument that it is “better” for their well-being. But businesses are not neatly packaged entities with uniform interests, strategies and situations. It’s not uncommon for small businesses to choose both options. Simultaneously. Two loans. To serve different purposes.

And so what then? I believe to some extent the concept of algorithms with thousands of data points, yelp reviews and the rest of it are being challenged by basic scenarios such as what happens to performance models if the customer takes on more debt after the initial loan?

Why do many consumer borrowers that claim to be consolidating their debt end up more in debt? Maybe the lenders themselves expected this but it conflicts with the message that was being told to the outside world for a long time about what made these products so special, that borrowers were consolidating their high interest debt to lower rate loans that was all made possible thanks to the low cost required to operate an online lender fueled by revolutionary new algorithms.

Even the underlying low cost premise to operate is being challenged. Why are low cost lenders often wildly unprofitable if their secret sauce is supposedly the low cost of being a nonbank online lender?

The problem is that some stories sound great on paper but don’t work out exactly as planned in the real world.

Even the concept of peer-to-peer lending and to some degree the marketplace has transformed or been phased out. Marketplace lending as the term is survived by today is typically Wall Street institutions providing capital to nonbank lenders. There is no real marketplace, at least not for the little guy anymore.

All of these discoveries and evolutions are a good thing. Too many experiments being conducted in the market at the same time created chaos. Failures, slowdowns, and adjustments are a positive step toward a sustainable future. How could a lender reasonably rely on its performance models when every day some new company was opening up and pulverizing the market with billions of dollars of marketing and loans based on some untested unprofitable system?

It’s no wonder that like twenty trade groups formed this year alone. Regulators and legislators looking out into the world of fintech probably saw and still on some levels see a tornado of disruptive confusion.

“Are you guys one of those crowdfunding marketplace bitcoin cash advance peer-to-peer lending companies I’ve been reading about? We need to regulate you.”

They need help to sort through it all and fast.

The FDIC, for example, humorously defined marketplace lending as basically every kind of lending there is, from auto loans to merchant cash advance to medical patient financing to real estate lending. The industry became everything and as everything it’s essentially nothing.

And so the quiet summer months, though not totally dead, were much needed. Hopefully everybody has gotten a chance to breathe and can now continue the work they set out to do and truly provide sustainable value to the economic system.

Bring on Fall!

The Empty Loan Marketplace – Lending Club Zero?

September 2, 2016Update: 9/2/16 – At 1 PM, Lending Club uploaded a batch of 600+ loans on to the platform.

Update: 9/3/16 – The only notes available on the platform today are C-grade notes. No A,B,D,E,F,G…

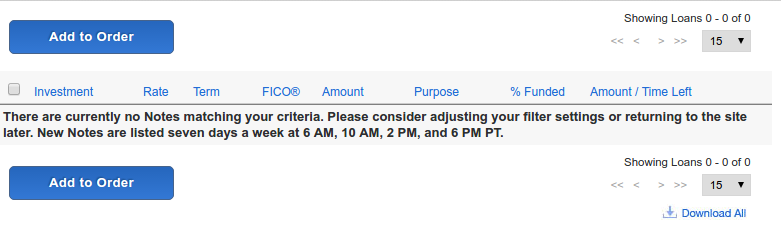

The leader in marketplace lending is showing ZERO available notes in its retail marketplace, according to a screenshot captured of Lending Club this morning. This indicates that Lending Club either hasn’t uploaded its latest batch or that no loans are currently being allocated to retail investors. It doesn’t mean that the company isn’t lending.

PeerCube, which tracks the amount of new and total loans on the Lending Club platform, also shows zero availability over the span of several hours.

Even if it’s a technical issue, Lending Club’s purported 135,000 self-managed active individual investors will be sure to notice that the marketplace is currently out of stock.

PeerCube also shows that there were 27% fewer loans listed on the retail marketplace in August than in July.

Meanwhile, a thread started on the LendAcademy forum where many Lending Club retail investors hang out, shows users discussing a dearth of new loans going back to July 22nd. Anil Gupta, who runs PeerCube, said in the thread that Lending Club had recently stopped releasing new loans to the retail platform on weekends.

Lending Club has not yet responded to an email sent to them inquiring about the zero note availability, but recently company CEO Scott Sanborn reassured investors that they were committed to the marketplace.

Some of our investors have observed the funding environment and asked: “Are you going to become a balance sheet lender, just like a regular bank? Has Lending Club’s business model changed?”

Let me be very clear: Lending Club is committed to the marketplace model and we do not plan to become a balance sheet or “hybrid” lender. Our mission of connecting borrowers and investors has not changed.

– Scott Sanborn, in an email on 7/28/16

On August 4th, Bloomberg reported that Lending Club was in talks with Western Asset Management Co. to set up a fund that would purchase as much as $1.5 billion of loans over time. Institutions like these may be responsible for the periodic lack of notes made available to the retail market.

Letter From The Editor – Sept/Oct 2016

September 1, 2016What is marketplace lending? Lately it’s been looking more and more like Wall Street and banking. Goldman Sachs is now playing a more prominent role in the space while the Office of the Comptroller of the Currency is considering a limited-charter framework, which would make the non-bank lenders more bank-like. Not to mention that things like securitizations, bond ratings and vintage performance are dominating news headlines. It all sounds very Wall Street indeed.

But while a segment of the industry looks to effectively merge back into the traditional banking system [ I suppose they are becoming “reBanked” 😉 ], there’s another segment chugging along just fine without the banks and we write with you in mind.

To that end, we asked, what are the challenges with funding merchants in Puerto Rico? Is it okay to fund marijuana-based businesses in states where it’s legal? And what’s the latest challenge to affect telemarketing efforts?

Maybe you are surprised to hear that telemarketing even has a place in the world of fintech especially since the media hype over the last few years has imagined an online-only Internet utopia where all lending happens in the cloud. Meanwhile, millions upon millions of dollars of transactions start with a guy or gal and a cold call.

There are rules, of course. You can’t just call anybody using whatever means you want and some people on the receiving end of those phone calls know that. Woe betide you who calls the wrong person the wrong way, our research discovered. The TCPA (Telephone Consumer Protection Act) is creating another burdensome layer of cost and some of the tactics being employed to extract penalties warrant close attention. It might not be future regulations that cause problems but existing ones. In this issue, we’ll show you why smiling and dialing do not always go hand in hand.