Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

ID Analytics Now Has 85% Visibility Into Online Consumer Lending

October 24, 2017 At Money2020, deBanked caught up with Kevin King, Director of Product Marketing and Ken Meiser, VP of Identity Solutions for ID Analytics. The last time I crossed paths with the company was six months ago at the LendIt Conference in New York City. Since then, the company has increased its visibility into the online consumer lending market to 85%.

At Money2020, deBanked caught up with Kevin King, Director of Product Marketing and Ken Meiser, VP of Identity Solutions for ID Analytics. The last time I crossed paths with the company was six months ago at the LendIt Conference in New York City. Since then, the company has increased its visibility into the online consumer lending market to 85%.

Because so many lenders, including credit card issuers, are plugged into their system, ID Analytics can view where consumers are applying for credit across the spectrum. That’s bolstered by their visibility into where applicants are in the process with getting approved. “We’re seeing the lifecycle of that application,” said King, who added that it’s possible using their tool that a lender can know where in the process a borrower is with another lender, though without the ability to see who that lender is.

ID Analytics is not a credit bureau, but they can help lenders root out fraud by analyzing among many other factors, the “velocity” of a consumer’s credit applications. An example is the number of credit applications submitted in a short amount of time. It’s important to distinguish what kind of credit it is though, King and Meiser explained, because the way people apply for online loans can be different than how they apply for credit cards.

Meiser shared an example of something that might on its face look anomalous but is actually not, such as when someone moves and all of the sudden there are several credit applications tied to a home address never previously seen on record for that borrower. Are we talking about normal stuff like a store credit card at Home Depot to buy a refrigerator for the new house or is it for multiple loans? was the gist of a point he made.

ID Analytics won’t declare a loan application to be fraud, they just provide the lender with an ID Score®, a real-time fluid score that can signal to a lender to carry out more due diligence depending on the extremity of the score. If someone applies for five loans in one day, for example, that score could go up with each application. Their service helps root out fraud by looking at “leading indicators” rather than “trailing indicators,” they said.

“We’ve seen an interesting shift in how fraudsters are attacking,” King stated. The company is now reviewing about 1 million credit applications a day and can continuously scan for new trends. 7 out of the top 10 credit card issuers use their service, as do many online lenders and phone carriers.

Asked if their service would have anything to do with online lenders asking the occasional borrower to submit a utility bill or other document to confirm their identity all while other borrowers are not asked at all.

Lenders use a lot of their own factors, but if they’re suddenly asking for more documents to prove an applicant’s identity, there’s a good chance that could be because of us, they said.

Stacking Lawsuit Could Go to Trial

October 18, 2017 A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

In this case, plaintiff Small Business Financial Solutions, LLC (SBFS AKA RapidAdvance) alleged that Pearl Beta Funding, LLC (AKA Pearl Capital) interfered with a loan agreement it had with a merchant when Pearl “stacked” financial obligations to Pearl on top of the obligations the customer owed to SBFS. Ultimately the merchant defaulted and SBFS wants to hold Pearl responsible for the damages it incurred.

Pearl originally moved to dismiss the suit but was unsuccessful. Later, Pearl filed a motion for summary judgment. On September 29th, that motion was denied, with the judge opining that issues of fact remained that were best left for a jury.

Unless Pearl appeals the decision or the parties settle, the case will go to a jury.

A representative for Pearl Capital declined to comment on the decision, citing ongoing litigation.

Patrick Siegfried, Assistant General Counsel for RapidAdvance, opted to tell deBanked the following:

“The court’s decision from many months ago to reject Pearl’s motion to dismiss and its more recent decision to reject the motion for summary judgment and permit this case to go to trial confirms the anti-stacking position RapidAdvance has consistently taken. The court’s rulings make it clear that when a funding company funds a merchant knowing that doing so is a breach of the customer’s agreement with another funder and the stacker’s funding is a substantial cause of the merchant defaulting with the other funder, its actions constitute tortious interference. As a result, the company that stacked can be held liable for the losses the original funder incurs. While the outcome at trial is impossible to predict as the court will need [to] decide whether there are sufficient facts to satisfy each element, RapidAdvance is pleased that its legal reasoning on stacking has been confirmed in a written opinion and that we now have the roadmap for pursuing others that tortiously interfere with our contracts by stacking.”

Of note, is that RapidAdvance brought this case in The Circuit Court for Montgomery County, Maryland. Few other players in the industry may be able to designate Maryland as the proper venue. The standards for tortious interference may not be the same in other states. There are many circumstances in the case not discussed in this synopsis. Consult an attorney before drawing any conclusions. YOU CAN DOWNLOAD THE FULL DECISION HERE.

The case is Small Business Financial Solutions, LLC v. Pearl Beta Funding, LLC Case No. 411478-V in the Circuit Court for Montgomery County, Maryland.

Mayor Rahm Emanuel Cuts Ribbon for 160% APR Online Lender

October 11, 2017Chicago Mayor Rahm Emanuel cut the ceremonial ribbon at OppLoans’ new headquarters in Chicago this week. The APR of a typical installment loan is 160% APR in many states, according to the OppLoans website. In South Carolina, a typical loan is listed as 199% APR over 9-18 months.

Today we cut the ribbon on @OppLoans' new office in Chicago. pic.twitter.com/SAROJfCTcE

— Mayor Rahm Emanuel (@ChicagosMayor) October 9, 2017

According to a press release, Emanuel said “While for a lot of people outside this room, this may be the first time they’ve heard of OppLoans. There is no doubt in my mind this will not be the last time they’ve heard of OppLoans. I look forward to being back as you scale more mountains, more heights, and continue to grow and to be successful, and to offer financing to a lot of families.”

While OppLoans offers consumer loans, Emanuel has previously attacked small business finance products with lower costs than OppLoans as predatory. Perhaps he has reevaluated his understanding of APR.

Google Restricts Ads for Merchant Cash Advances

October 8, 2017Google’s quest to stamp out payday loan advertisements from its paid search results has caused collateral damage to merchant cash advances. That’s because the two-word term cash advance, often synonymous with payday loan, appears to now have a blanket restriction that blocks ads whenever that term is included in search, regardless of the words that come before it or after it.

Merchant cash advances, however, are commercial factoring transactions with no relation to payday or consumer finance.

A user on the deBanked forum first alerted me on October 5th and deBanked conducted tests from internet connections in two states to see if we could replicate the results. Below is a sample of our results:

| Keyword | Google Adwords Status |

| cash advance | BLOCKED |

| merchant cash advance | BLOCKED |

| business cash advance | BLOCKED |

| business loan | ACCEPTED |

| loans | ACCEPTED |

| get a business loan | ACCEPTED |

| loan for my business | ACCEPTED |

| cash advance for my business | BLOCKED |

| business loan companies | ACCEPTED |

| merchant cash advance companies | BLOCKED |

| factoring or business loans or credit cards | ACCEPTED |

| factoring or business loans or merchant cash advances | BLOCKED |

| loan from ondeck | ACCEPTED |

| cash advance from ondeck | BLOCKED |

| consolidate loans | ACCEPTED |

| consolidate cash advances | BLOCKED |

No such block exists on rival search engine Bing.

Though Google has not said this, the mass removal of payday lending ads, once a massive source of revenue for them, is likely the result of government pressure. Over the last two years, federal regulators have begun targeting lead generation sites that direct users to lenders in a misleading manner.

Unless Google fixes the glitch that caused merchant cash advances to get wrapped up with consumer cash advances, the organic search results will experience a huge boost in value. Last month we reported that companies like OnDeck, Fundera, and Nerdwallet were winning the search engine optimization battle for several keywords including merchant cash advance. Absent any ads, those companies and several others will now benefit from a stream of free traffic and applicants for which their cost of acquisition will be zero dollars.

Perhaps little has been mentioned about this ban within the industry because the end result is FREE leads for those that rank well organically. Long live SEO!

Dear MCA and Business Loan Brokers, It’s Time

October 5, 2017 It’s been two years since the Year of the Broker was published. And it’s been many more than that since the last time I brokered a deal myself. Though I’ve only been writing about merchant cash advances (MCAs) and non-bank business loans for seven years here, my involvement in that industry started more than a decade ago. In all that time I’ve gone to countless trade shows, conferences, networking events, meetups and discussion sessions. To their credit, many of those provided excellent value across the spectrum of finance or payments, but none ever quite fully gripped an industry that is now pumping out approximately $15 billion to small businesses each year.

It’s been two years since the Year of the Broker was published. And it’s been many more than that since the last time I brokered a deal myself. Though I’ve only been writing about merchant cash advances (MCAs) and non-bank business loans for seven years here, my involvement in that industry started more than a decade ago. In all that time I’ve gone to countless trade shows, conferences, networking events, meetups and discussion sessions. To their credit, many of those provided excellent value across the spectrum of finance or payments, but none ever quite fully gripped an industry that is now pumping out approximately $15 billion to small businesses each year.

MCAs and online business loans are still overwhelmingly facilitated by salespeople, whether they’re employed by direct capital providers or independent sales organizations and brokers. Notably, a recent survey of industry CEOs suggested that in the last two years, the industry has come to rely even more on brokers for originations despite the belief that their reliance on them would decrease. An average of 64% of originations are currently coming from external sources/ISOs, the survey revealed.

Even salespeople at direct capital providers can find themselves playing the role of adviser or middleman when the solutions they offer in-house are not the right fit for a prospect. Small businesses need someone to help them navigate the massive universe of options and have that person be able to explain those options correctly. It only makes sense then that there would be an annual gathering of brokers, lenders, and MCA funders where all of those salespeople and their colleagues come together. Much to my disappointment (and I’m not alone in that) I’ve never found such an event.

I expect that will change in 2018. I truly believe dear friends that it’s time…

Update: Meet Broker Fair 2018

ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

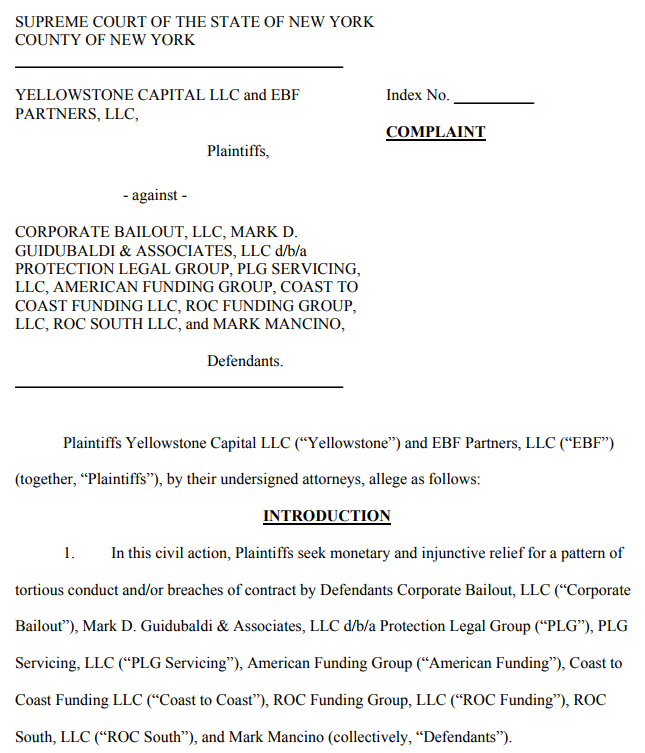

September 28, 2017 ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

The debt settlement companies “mislead the merchants as to the services they will perform and the cost to the merchant, and they also conceal their relationships with the ISO Defendants and the fact that they or their affiliates are introducing these same merchants to merchant cash advance providers like Plaintiffs only to later induce those merchants to breach their agreements with their cash advance providers,” the complaint states.

Among the named defendants are:

- Corporate Bailout, LLC

- Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group

- PLG Servicing LLC

- American Funding Group

- Coast to Coast Funding, LLC

- ROC South, LLC

- Mark Mancino

Several defendants are already best known for running an office “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street,’” according to a salacious story that graced the back cover of the New York Post last month.

One paragraph of the complaint summarizes the allegedly collaborative scheme like this:

American Funding, Coast to Coast, […] (the “ISO Defendants”) are independent sales organizations (“ISOs”), companies that ostensibly support the merchant cash advance industry by brokering merchant agreements for companies like Plaintiffs. The ISO Defendants are anything but the proverbial “honest brokers.” As alleged below, they have partnered with companies that purport to offer debt relief services to merchants who have agreements with merchant cash advance companies like Plaintiffs. In practice, for these companies, “debt relief” is a code word for deceiving merchants to breach their existing agreements with Plaintiffs and to instead pay fees to these debt relief entities. In short, they scam merchants into believing that they can save them money when, in fact, they leave these merchants in financial shambles, while causing Plaintiffs to suffer millions of dollars in losses and future los[t] profits.

“’DEBT RELIEF’ IS A CODE WORD FOR DECEIVING MERCHANTS TO BREACH THEIR EXISTING AGREEMENTS”

Central to the plaintiffs’ claim is that they have ISO agreements with the defendants and that the defendants’ conduct is a breach of those agreements. The three causes of action alleged are tortious interference with contract, conversion, and breach of contract. Plaintiffs claim that 100 merchants with more than $3 million in outstanding balances are in breach of their contracts because of the defendants’ conduct.

The complaint was prepared and filed by attorneys at Proskauer, a 142-year old law firm founded in New York City.

Debt Relief Under Fire

The small business debt relief industry has been marred by scandal in recent years. In an unrelated criminal matter being handled in the Western District of New York, the owner of Corporate Restructure Inc. (no ties to Corporate Bailout) is currently residing in the Niagara County Jail awaiting trial on charges of conspiracy to commit mail fraud, wire fraud, bank fraud and money laundering for failing to deliver the debt relief services it charged for. In that case, United States vs. Sergiy Bezrukov, Bezrukov advertised that he could reduce a merchant’s short term debt by up to 75%. He is facing up to 30 years in prison. He was also previously a merchant cash advance ISO.

Two other MCA funding companies, Pearl Gamma Funding and Pearl Beta Funding, filed a lawsuit last November against another debt relief company that calls itself Creditors Relief. The complaint in that case also alleges tortious interference with contract and is still pending.

Meanwhile, a lawsuit filed in May by famous TCPA litigant Craig Cunningham against Corporate Bailout and Mark D Guidubaldi & Associates LLC went unanswered, according to court records. Cunningham, who alleged violations of telemarketing laws, filed for a default judgment against Corporate Bailout on September 12th.

Taking Advantage

Both Yellowstone Capital and Everest would not comment on the lawsuit they filed, citing pending litigation. Sources close to them, however, contend that both companies take matters that involve merchants being taken advantage of very seriously.

“When our own ISOs work directly in concert with companies that induce merchants to breach our contracts, that’s a problem,” said one source who did not wish to be named and was speaking generally about the recent introduction of debt relief service companies to the industry. “They’re taking advantage of businesses that can’t afford to be taken advantage of.”

An email sent by deBanked to Mark Mancino early Thursday afternoon, an individually-named defendant alleged to be affiliated with the other defendants, has not yet received a response. This story may be updated if a reply is received.

A COPY OF THE COMPLAINT CAN BE VIEWED HERE.

Funders and Lenders are Relying More on Brokers, Survey Finds

September 27, 2017Business lending and MCA CEOs are not finding it easy to reduce their dependence on brokers, the latest Bryant Park Capital/deBanked survey results suggest. In a past survey conducted in Q4 2015, respondents indicated that an average of 46% of their business came from external sources/ISOs versus internal marketing. 44% of respondents also reported at the time that they expected the percentage of ISO business to decrease while 33% expected it would remain the same.

Nearly two years later, respondents to the latest survey reported that an average of 64% of their business now comes from ISOs/external sources, a significant increase. 62% of those surveyed said they expected that percentage to decrease.

OnDeck, who did not participate in the survey, reported last quarter that 21.1% of their loans were originated through ISOs, brokers and related parties, up from its lowest point in recent years. That accounted for 24.3% of the total dollars loaned for the period.

Confidence in MCA and Online SMB Lending Industry Ticks Up

September 26, 2017The latest industry CEO survey conducted by Bryant Park Capital and deBanked showed that confidence in the continued success of the SMB lending/MCA industry is coming back. Confidence had a hit a low of 73.8% in Q1 of this year, the lowest point since the survey started in 2015. In Q3, the number jumped up to 81.3%.

Confidence in being able to access capital at a reasonable cost to grow ticked up only slightly to 79.9%, up from its lowest point in Q1 this year at 78.7%.

The first quarter of 2016 holds the confidence record since the surveying began. Coincidentally, that period is widely considered to be the peak of the online lending bubble. An April 2016 blog post published during that year’s annual LendIt Conference declared an end to the euphoria.

While respondents to the most recent survey were not asked to explain their confidence level, factors like a steady regulatory climate and some recent competition-reducing consolidation likely played a role in the boost.