Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Fintech Déjà Vu: Wait, Has This All Happened Before?

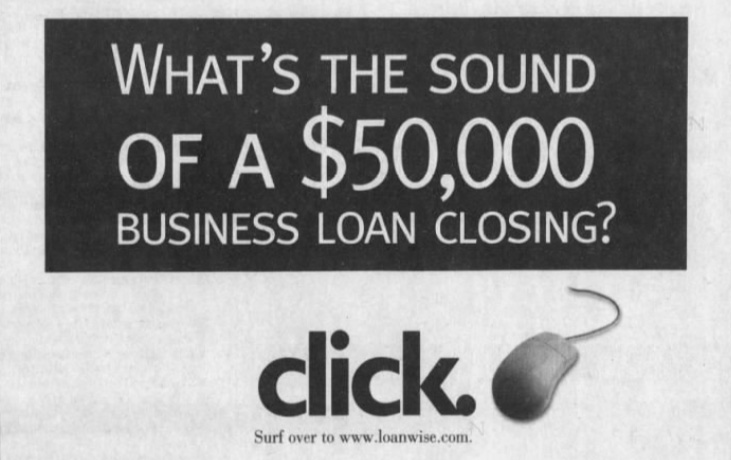

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

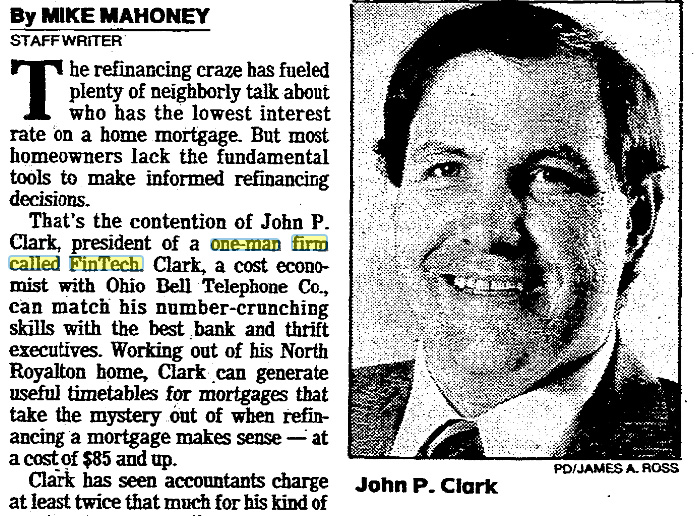

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

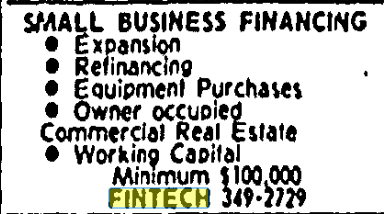

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

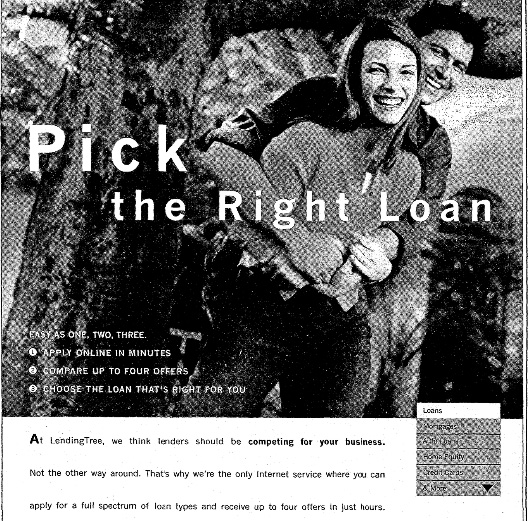

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

How to Comment on New York’s Commercial Finance Disclosure Law

October 4, 2021With New York’s commercial financing disclosure law on the horizon for Jan 1, the state’s Department of Financial Services is seeking input on how the law should officially be rolled out. Their draft was published on September 21st. Directions for how to submit a comment were said to be forthcoming, but the when and how to do that, were not easily discernible.

The DFS website says that comments should be submitted via email to George Bogdan, but that the time to do that has already expired, the deadline having been October 1st.

A spokesperson for DFS on social media, however, said that comments on the law can be sent to: Comments@dfs.ny.gov.

This process of emailing comments contrasts with processes at the federal level which typically employ formal portals. While it may apparently be too late, anyone that had hoped to contribute their feedback but didn’t get to, could try the above contacts.

Fake Press Release Announced That SEC Had Dropped Case Against Ripple

October 1, 2021 XRP, the digital assets tied to Ripple, surged this morning from a price of $0.95 to $1.04 on the supposed announcement that the SEC had dropped its lawsuit against Ripple.

XRP, the digital assets tied to Ripple, surged this morning from a price of $0.95 to $1.04 on the supposed announcement that the SEC had dropped its lawsuit against Ripple.

The news came via press release service Accesswire in the headline “SEC vs Ripple Legal Fight is Over.” Other news outlets immediately picked it up, including Yahoo, and it made its way to the top of Google’s search results.

The problem is that the entire press release was fake.

“Ripple, the leading provider of enterprise blockchain and cryptocurrency solutions for global payments, is pleased to announce that the SEC vs RIPPLE legal battle is finally over,” it began. “The lawsuit that lasted over ten months has finally been settled between the Securities and Exchange Commission (SEC) and the cryptocurrency company Ripple. The SEC has announced it would drop its charges.”

Accesswire deleted it as did Yahoo. deBanked obtained it via archive.org. Merely googling: ripple sec, however still shows the fake headline as the top result.

The public may not be fully aware that the news is false yet, if the price is any indication. It’s still trading at $1.04 as of the time this story is being written.

Two weeks ago, GlobeNewsWire fell victim to a similar scheme, when it distributed a fake announcement that Walmart would begin accepting Litecoin.

MJ Capital Funding’s Website Has Been Shut Down, Company’s Assets Being Auctioned Off

September 24, 2021 MJ Capital Funding investors holding out hope that a return to business as usual could be in the cards for the company accused of being a ponzi scheme, might find that outcome a little less likely.

MJ Capital Funding investors holding out hope that a return to business as usual could be in the cards for the company accused of being a ponzi scheme, might find that outcome a little less likely.

The Receiver has agreed to auction off all of the assets at the company’s Pompano Beach offices on September 28, and everything must go, from the 60″ TV to the garbage cans to the houseplant.

Such powers afforded to the Receiver, a law firm partner named Corali Lopez-Castro, also gives her the ability to enter into binding legal agreements on behalf of the company, the latest ones being Consent Agreements with the SEC. In doing this, the two MJ companies (MJ Capital Funding, LLC and MJ Taxes and More Inc.), have agreed to disgorge of “ill-gotten gains,” accept a civil penalty, and be permanently restrained from continuing its former business. Such an arrangement is standard fare when companies are thrust into forced Receiverships like this one. The Receiver’s job will be to collect as much money as possible so that it can be distributed to afflicted investors.

The MJ Capital Funding Website has also been shut down. It now forwards to law firm Kozyak, Tropin, Throckmorton. Regular updates on the case are available for free at: https://kttlaw.com/mjcapital/.

The consent orders do not apply to former CEO Johanna M. Garcia individually, who lost control of the company and ability to act on the company’s behalf when it was placed into Receivership.

An astounding 3,160 people have signaled their support for Garcia in this case. That’s the number of signatures on the online petition for her located on change.org.

“Our goal with this petition is to get those funds unfrozen as soon as possible,” it says. “This is Johanna’s desire as well proving once again Johanna’s unwavering support for us and in building a strong team and community. Johanna has helped countless amounts of people and charities with the work she does local and worldwide.”

Brokers Say “Yes” to Commissions in Crypto

September 12, 2021 One month after Velocity Capital Group began offering broker commissions in crypto, CEO Jay Avigdor says it is taking off. It’s completely optional of course, but already seven of VCG’s ISOs have opted to get paid that way.

One month after Velocity Capital Group began offering broker commissions in crypto, CEO Jay Avigdor says it is taking off. It’s completely optional of course, but already seven of VCG’s ISOs have opted to get paid that way.

“The feedback has been fantastic!” Avigdor says.

In a previous interview with deBanked, Avigdor said that the initiative wasn’t about speculating on cryptocurrencies but instead about taking advantage of the transaction speed. Crypto can change hands faster than an ACH or a wire, for example, and VCG will send funds via a stablecoin so that there is no volatile exchange rate risk.

“Our goal since day 1 of VCG, was to give ISOs and merchants the ability to access capital as fast as possible,” Avigdor said. “With VCG’s proprietary technology, we have been able to change that mindset from ‘as fast as possible’ to ‘the FASTEST possible.’”

One broker attested on facebook that he received his commission from VCG within 5 minutes from the moment the deal funded via the DAI stablecoin.

Even a merchant requested that they be funded with crypto, according to Avigdor, which they accommodated. Payments back to VCG are still done via ACH debit, however.

The market cap of the cryptocurrency industry is currently at more than $2 trillion.

Facebook Enters the Invoice Factoring Arena and More

September 11, 2021 Facebook is the latest tech company to enter the small business financing space. Starting October 1st, Facebook will begin offering eligible American businesses the opportunity to sell their invoice receivables for cash upfront. The only cost is a 1% fee of the A/R and invoices can be as small as $1,000.

Facebook is the latest tech company to enter the small business financing space. Starting October 1st, Facebook will begin offering eligible American businesses the opportunity to sell their invoice receivables for cash upfront. The only cost is a 1% fee of the A/R and invoices can be as small as $1,000.

Dubbed Facebook Invoice Fast Track, a promotional video touts it as a solution to cash flow challenges.

The caveat is that it will only be open to businesses owned by minorities, females, veterans, LGBTQ+ or someone with a certified disability. Also, the invoices must be issued to a corporation or government entity with an investment-grade rating. An outstanding invoice from something like “Joe’s corner t-shirt shop” for example, would not be eligible.

Facebook COO Sheryl Sandberg predicts the company will be funding $100 million in invoices on an ongoing basis.

That’s not all, however. The company is also introducing a new small business loan resource through an arrangement with Connect2Capital. Facebook claims that in doing so, it is not “brokering” loans.

The developments may not be all that unsurprising given Facebook’s recent foray into India’s small business loan market.

The Sports World Is Going Nuts for Crypto

September 9, 2021 Miami Mayor Francis Suarez wants NFL Quarterback Tom Brady to know that he’s totally in to crypto.

Miami Mayor Francis Suarez wants NFL Quarterback Tom Brady to know that he’s totally in to crypto.

Strange times as it may be, and stranger yet with a new TV commercial that has Brady communicating agreeably with New York Jets super fan Fireman Ed, the cool place to be is “in crypto.” That’s the substance of a commercial for FTX, an international cryptocurrency exchange with a US operation known as FTX US.

Hey @GiseleOfficial @StephenCurry30 @Trevorlawrencee @mlb @kevinolearytv @LCSOfficial @MiamiHEAT @riotgames @TSM @stoolpresidente, you in? @ftx_official #FTXyouin pic.twitter.com/tGsQzgFJvs

— Tom Brady (@TomBrady) September 8, 2021

FTX already has the naming rights to Miami’s major sporting arena that is home base for the NBA’s Miami Heat. That arrangement excited the likes of Mayor Suarez, who has jumped on the crypto bandwagon so heavily that he actually launched his own crypto conference back in June.

On the other side of the country, Golden State Warrior powerhouse Steph Curry, announced he had signed on as an FTX partner/spokesperson.

“I’m excited to partner with a company that demystifies the crypto space and eliminates the intimidation factor for first-time users,” Curry said in a release.

Curry was one of several celebrities (including Brady’s supermodel wife Gisele Bundchen who also stars in it) that Tom Brady tagged in a tweet promoting his commercial.

“Whatever you do… don’t laser eyes!” Brady separately tweeted to Curry, a joke at the fact that crypto’s twitterverse has adopted “laser eye” profile pics to signal to others that “they’re in.” Brady is no different. Though his account profile description is short and to the point, “Family and Football,” his red laser-eyed pic is a signal that FTX and crypto are not just another random endorsement deal.

Brady is also a co-founder & co-chairman of the Board at Autograph, for example, a blockchain-based NFT autograph site that is currently selling digitally signed Derek Jeter autographs at high prices.

“NFTs bring an entirely new dimension to the collector experience, and I cannot wait for people to discover and engage with this first ever drop of Autograph’s official digital collectibles,” Brady said in a public statement about the company. “We created Autograph as a way for fans and collectors to own a piece of iconic moments in sports and entertainment through authenticated and official digital collectibles and we are just getting started!”

CFPB Publishes Long Awaited Proposed Rule on Small Business Loan Data Collection

September 1, 2021 A 918-page proposed rule published by the Consumer Financial Protection Bureau (if you don’t know what this bureau is, now is a good time to read up), is finally out.

A 918-page proposed rule published by the Consumer Financial Protection Bureau (if you don’t know what this bureau is, now is a good time to read up), is finally out.

Its application is broad, extending to “loans, lines of credit, credit cards, and merchant cash advances,” the CFPB said today. Initially, the Bureau’s intent was to exclude merchant cash advances, but that has apparently changed. (side note: I predicted this could happen as early as 2014.) Meanwhile, “factoring, leases, consumer-designated credit used for business purposes, and credit secured by certain investment properties” are exempt from the rule.

The rule is designed to assess whether there are disparities in sex, race, and ethnicity, when it comes to small businesses being able to access credit.

Covered financing providers would have to request that applicants disclose these things, which applicants can refuse to answer if they so choose. It could get a bit awkward from there because “if an applicant does not provide any ethnicity, race, or sex information for at least one principal owner, the Bureau is proposing that the financial institution must collect at least one principal owner’s race and ethnicity (but not sex) via visual observation and/or surname if the financial institution meets in person with any principal owners (including meeting via electronic media with an enabled video component).

BUT “minority-owned business status and women-owned business status would only be reported on the basis of information the applicant provides specifically for Section 1071 purposes, and financial institutions would not be permitted or required to report these data points based on visual observation, surname, or any other basis.”

Further, no one involved in the underwriting of the loan or advance would be allowed to know or access the ethnicity, race, or sex of the applicant. However, this would not apply if it isn’t “feasible” to do so.

All of the nuances, which seem to contradict themselves on the surface level, are specified in greater detail in the 918 page document.

When the proposed rule becomes final, lenders and MCA providers would have 18 months before they would be required by law to not only collect this data in the properly established manner, but also be prepared to submit it annually to the CFPB.

This rule will become a standard operating part of the business for companies both large and small whether one agrees with it or not. This law was passed in 2010 and it has taken this long to get to this point. This is a link to the CFPB’s official summary.