Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

“Don’t Make Us Pay” Goes Quiet

August 22, 2011Originally published on August 7, 2011.

As the Federal Reserve wound down the debit card debate on Capitol Hill, the “consumer rally” to fight against the reform followed suit. http://www.dontmakeuspay.org was/is a portal for individuals to lodge complaints with their local politican over a regulation that may potentially lead to higher debt card fees.For the most part, we championed this consumer movement since it was our belief that the Durbin Amendment would have unintended negative consequences.According to their site:

In December, the Fed issued a draconian regulation that reduces fees paid by retailers by 70 to 90 percent. As a result, the nation’s largest 2 percent of retailers will receive a $12 billion windfall – and debit card users like you will have to pay the tab.What does this mean for you? YOU could see higher fees, reduced rewards, and new debit card restrictions, unless Congress acts now to stop the rule.You shouldn’t have to pay more to use your debit card. TELL CONGRESS: DON’T MAKE US PAY.

Sounds logical enough right? We lodged our complaint with a few members of Congress and were immediately accused of astroturfing by politicians, bloggers, and retail chains. They got quite nasty too! Our advocacy for this movement led many to believe that our blog was secretly controlled by the big banks in order to create the illusion of a grass roots campaign by consumers. That was hurtful, especially since our site’s purpose is to provide businesses with free help to lower their fees, understand their statements, and make the best decision for themselves. It sure did wonders for our site traffic though, which experienced an 800% spike to all of our pages discussing debit card reform.

Although the debate pretty much ended with the final passage of the law on June 30th, 2011, the consumer movement to combat it died altogether. We have to admit that we’re a little surprised. dontmakeuspay.org has not updated their site since june 2nd, a full four weeks before the ruling. The silence is deafening, considering they used to post news several times a week. From what we’ve seen, the passage of a law never stopped the masses from voicing their discontent, especially if it was over something wildly unpopular.

But these consumers seemed to have vanished going into the homestretch and haven’t been heard from since. The banks themselves have acknowledged that the damage may not be as bad as anticipated and the retailers are claiming a mild victory. That was to be expected, especially since the final law called for an interchange cap that is nearly double than what was originally proposed. Regardless of who “won”, the opinions by both sides of the outcome have been published, politicized, criticized, or celebrated. But there seems to be no spokesman for the consumers who supposedly had been leading a crusade of their own. Are they happy with the outcome of the debit card law? Do they still believe that fees will still be passed down to them? We can’t answer their questions because the movement is seemingly MIA.

- A Retailer Celebrates: http://www.businessweek.com/magazine/sniping-at-charges-for-swiping-debt-cards-07072011.html

- A Card Issuer Tries to Stay Positive: https://debanked.com/apps/forums/topics/show/5593452-mastercard-sees-durbin-opportunity

- A Consumer Shares How They Feel: Nothing found…

Which brings us back to dontmakeuspay.org, the home base for the average Americans who believed they were about to get screwed. Even if the site was no longer being updated, surely we would find a band of angry consumers still discussing the issue on social networks like Facebook.

- Don’t Make Us Pay’s official FB Group: http://www.facebook.com/#!/group.php?gid=106108824431

Only 104 Members and the last wall post was on April 17th. Coincidentally it’s a link to an article we wrote on the topic (No wonder people thought we were directly involved). A Twitter search comes up with even less.

And so we come back to our readers with our tail between our legs. Dontmakeuspay.org was likely (just as many people accused) an astroturf campaign for the big banks. There was no national, cohesive consumer movement to fight the Durbin Amendment. Bummer.

But that doesn’t change our opinion of the legislation, nor the big banks. Increased fees were legitimately on the table but nobody was paying attention. It wasn’t until dontmakeuspay.org started slapping people in the face with mass transit posters, billboards, and internet advertisements, that the country began to realize how monumental the issue being debated was. Bringing a mass awareness to the public was a good thing and it may have ultimately achieved its goal. The proposed interchange cap went from 12 cents to 21 cents and 5 basis points, just high enough to save consumers from a world of hurt.

But that outcome should be overshadowed by the complete irony of it all. It is our opinion that both the retailers and the big banks got screwed together as a result of the reform. The only group that achieved victory, is the one that we know now didn’t even exist to begin with.

- Retailers will not see a decrease in their debit card fees. See: ‘And the Misinformation Continues‘

- Card Issuing Banks went from a limitless market rate to a strict profit killing cap

- Consumers see no rise in fees or elimination of reward programs in near future

Dontmakeuspay.org may have gone quiet, but while it was active, it helped the one group it claimed to represent. Call it deceptive, call it a decoy, call it misleading, or call it whatever you want. The big banks stuck their neck out for the little guy and the little guy won. It’s hard to hate on that…

– deBanked

https://debanked.com

Starting a Business – Read First

August 22, 2011Jerry had a business plan and some money set aside for startup capital. He assumed that’s all he needed, but six weeks later he was already out of business. What went wrong?

Starting a business is exciting and some entrepreneurs even describe getting an adrenaline rush as they approach opening day. But this impulsivity forward can lead to major mistakes, careless decisions, and ultimately put you on the path to failure. If you’ve got a lease on a storefront that opens May 1st, you should aim to open the business on May 1st. But if you are not prepared to handle the demands of your customers or conduct operations most efficiently, then you shouldn’t open just for the sake of opening.

- What can go wrong the week before opening – April 24th

1. Choosing vendors out of convenience or because they can meet an arbitrary deadline

Example: You’ve spoken to two advertising agencies about your startup. Both have quoted the same price. Company A can put together a promotional campaign by May 1st, your opening day. Company B can put together a promotional Campaign by May 18th, but it will be much more effective and reach a larger audience. Company B’s campaign is far more likely to bring in customers for the same price.

Believe it or not, with all the stress and time against their side, many entrepreneurs would rather pick Company A just for the immediate relief. It coincides with their opening day and it would feel great to have one less thing to worry about. But Company B would generate more revenue for them and thus would probably be the smarter decision.

2. Looking at the process like a checklist

Let’s say you’ve created a series of basic steps that must be completed before May 1st. In the last week, you go back to check and make sure they’re all done or to find out what you have left.

Example:

1. Create business plan

2. Raise capital

3. Lease store space or office space

4. Choose vendors for inventory, supplies, and equipment

5. Advertise

If your list is as basic as this, you’ve already failed. Each step should have a series of substeps.

Example:

1. Create business plan

– Survey prospects to determine if there is demand for this product (Don’t ask your family. They don’t count)

– Obtain a 2nd opinion from a qualified business advisor on your business plan

– Locate 10 weaknesses or shortcomings of your business plan (if you can’t find 10, you’re giving yourself too much credit)

– Find proof that a similar business model has worked before and dissect their plan

2. Raise capital

– Determine how much equity you are willing to sacrifice

– Set realistic goals for when your business will be able to start making payments, how often you can make payments, and how much you can afford in each payment

3. Lease store space or office space

– Determine several locations that would be ideal to reach your target market, whether or not there is space available there

– Determine if there is a way to obtain space in that area (sublease, a landlord looking to replace a tenant etc.)

– Determine which locations are actually available to lease

– Determine if any of them are suitable for your business (if none, DON’T open!)

– Determine if the costs justify the level of success you can achieve in that location

4. Choose vendors for inventory, supplies, and equipment

– Seek out terms on inventory as opposed to COD (very difficult for a startup to attain but it would be a huge difference in cash flow)

– Choose reputable vendors (don’t pick the cheapest just because cash is tight in the beginning. Low quality goods may turn your customers away)

– Choose how you will pay for supplies and equipment (lease or purchase. Leasing may be less expensive now but far more costly in the long run)

5. Advertise

– Shop around and learn about all the different ways these firms intend to help you reach your target audience

– Choose the company that will produce the most bang for your buck

– Use common sense (A 3 AM TV commercial is probably not suitable for a toy store etc.)

If you didn’t go through this whole list, there’s a good chance you’ll fail. And just when you think you’re sure you’ve got a handle on everything, buy a few books by people who have been in your shoes. Find out what they did, what challenges they faced, and how they succeeded or failed. We’re not talking about a short article like ours, but rather a full story that shares every detail, thought, and emotional feeling that you can expect to go through. There’s nothing like being prepared and it may even inspire you to modify your business plan as it currently stands. Don’t end up like Jerry. Doing things right is much better than doing things quickly.

The Merchant Cash Advance “Don’ts”

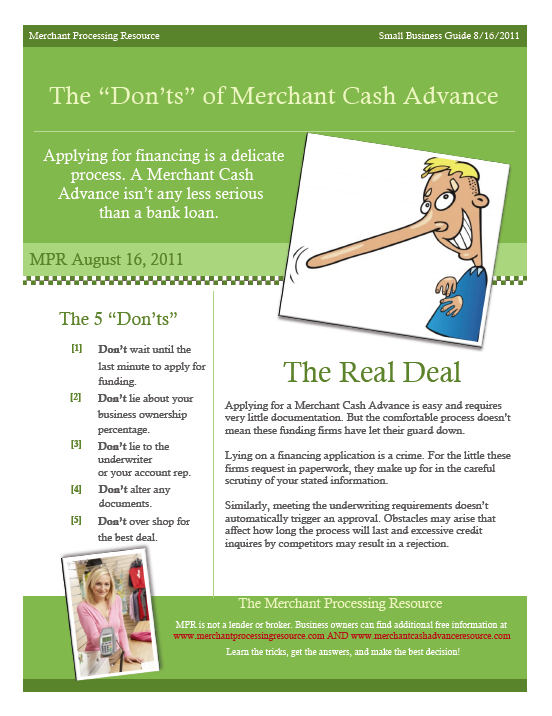

August 22, 2011In sales training, young men and women are taught to negotiate with positive language to close a deal. For example: “We can’t meet the deadline” is replaced with “We can achieve the objective, but we may need to extend the deadline.” Or “We don’t offer that service” is transformed into “We offer many services that can add value to your business but that particular one is a challenge.”We apply a bit of that psychology when developing resources for business owners. People are a lot more open to input when you cast out the negativity. So it’s a bit ironic then that we created a printable reference form, titled The Merchant Cash Advance “Don’ts”. Though it may be perceived as a little condescending, this little banker/business pep talk can protect you from making a major mistake that could cost your business money. So keep it handy even if you don’t plan on applying in the near future.

1. Don’t wait until the last minute to apply for funding.If a firm is advertising funding in 3-5 days, don’t put yourself in a position where you MUST have the funds in 5 days or less. The underwriting process may take longer than you anticipate. The advertised timeframes generally describe a perfect situation. For example: If all documents are received by day 1, all references checked out by day 2, you could potentially receive funds by day 3 assuming the technical setup is already completed. There are situations where business owners have spent 10 days waiting to obtain a copy of their lease from their landlord, which piggybacks onto the 3-5 days. Additionally, supplemental paperwork may be asked for, a trade reference might be unreachable, or your method of card acceptance might require more time to integrate. Anything can happen so don’t wait until the last minute!

2. Don’t lie about your business ownership percentage.This might be seem like silly advice but underwriters report that it’s a growing trend. People with low credit scores tend to assume that they will be declined for their score alone. Therefore they may feel inclined to state that a partner, friend, or family member with excellent credit is the owner of their business and not them. This is bad for several reasons:

- Credit score isn’t the sole determining factor for a Merchant Cash Advance. So why lie?

- Misrepresentation of ownership will be discovered and the application declined.

- Misrepresentation to obtain financing constitutes fraud and is a crime.

3. Don’t lie to the underwriter or your account rep.The liar loans of the mortgage boom ultimately led to the financial crisis and lending shortage. That means the days of declaring whatever you want to obtain the deal you want, are gone. If you state that you generate $100,000 in sales per month, be prepared to show documentation that backs up that claim. Your sales agent or account rep is probably compensated if you close on financing. That doesn’t mean they will help you get there at all cost. They are bound by a certain code of ethics and all applicable laws. If they become aware of any misrepresentation or intended misrepresentation, don’t expect them to be an accomplice to your dishonorable act. If you put them at risk, they will inform the underwriter and terminate your application.

4. Don’t alter any documents.Changing the expiration date on a lease, editing out the embarrassing withdrawals from the bank statements, or any other more or less blatant alteration will result in a rejection. Merchant Cash Advance underwriters are extremely adept in detecting alterations and fraud. Altering documents in an attempt to secure financing is a crime. You are well advised not to try this, no matter how harmless you may perceive the alteration to be.

5. Don’t over shop for a deal.You are entitled to obtain quotes from multiple sources, but don’t press your luck. Too many credit inquiries can spook an underwriter. For one, it tends to drive down the margins that will be earned because competition, thus making the deal less profitable for them and less attractive to put on the books. On the other hand, they may suspect that the other firms declined you and therefore they are being picked as a last resort. When underwriters start to feel this way, your approval may be retracted and it can be a tough battle to convince them to change it back.

We promise next time to provide a guide full of “Do’s”! But for now, we’re making it a point that Merchant Cash Advance is a serious business. The process may be fast and easy, but don’t get too comfortable and make claims you can’t back up. That will lead nowhere good…

– The Merchant Cash Advance Resource

http://www.merchantcashadvanceresource.com

Deja vu? Merchant Cash Advance in Wall Street Journal

August 10, 2011 Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

It was just a couple months ago that we published a scathing editorial on the failure of the Merchant Cash Advance (MCA) industry to reach mainstream acceptance. (See: The Colossal Marketing Failure of the Merchant Cash Advance Product – June 28th, 2011). Most of our readers acknowledged the shortcomings but were at a loss for suggestions to overcome them. ISO&Agent Magazine quickly added their two cents by claiming that MCA was waiting for its big moment (See: Cash Advances: Negotiating a Maturing Market – July 26th, 2011) but completely missed the mark when they identified cost as the obstacle holding it back. It’s not cost, it’s communication.

How often is MCA cited in mainstream news publications? Wall Street Journal? New York Times?

-direct quote from our piece on June 28th

Today we can say that Merchant Cash Advance got its mention in the Wall Street Journal. :::Applause::: Though it’s only in their blog section, most people today get their news online anyway. The article features AdvanceMe, the largest and oldest player of the bunch. So how does the glorification of one company carry over to the industry as a whole? There were a bunch of good messages in there that describe the product itself: The article title implies it’s becoming more popular: “Cash-Advance Demand Rising” A description of how it works: “Merchant cash advances, which first appeared about a decade ago, provide capital in exchange for a share of future debit or credit-card sales. As such, they tend to be used by retailers, restaurants and other small businesses where a large number of customers pay with cards.”The common uses for it: “Business owners use the cash to buy new equipment, restock inventory or pay off debt” Yes, Yes, and Yes. Good for AdvanceMe and good for the MCA industry but this is only the beginning.

Every business owner should be aware of MCA, not just the ones that read the Journal today. It is Un-American (Yeah, that’s right) to withhold information from business owners that may enable them to capitalize on opportunities. With no bank loans available, most projects in this country are on hold. It’s simply not fair. We badly want to take the credit for today’s Journal mention, especially since we delivered our two previous articles on this topic to their editors in July. But the real hero here is AdvanceMe. Their press release the day before clearly caught the attention of the mainstream media. Great job guys. And we’d be remiss if we didn’t point out they forecasted an increase in funding by $1 billion in the next 2 years. That’s about equal to the industry’s entire volume combined. Is Merchant Cash Advance about to hit its growth spurt? AdvanceMe seems to think so. If they’re about to have their ‘moment‘, they’ll likely pull everyone else along with them.

– deBanked

https://debanked.com