Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

15,000 exempt from the debit card interchange fee standards

August 23, 2011Originally Published on July 14, 2011.

Why is the number ‘15,000’ significant? That’s approximately the number of banks that are EXEMPT from the debit fee interchange cap. Download List

From the Federal Reserve:

The Federal Reserve Board on Tuesday published lists of institutions that are subject to, and exempt from, the debit card interchange fee standards in Regulation II, which implements provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act. These lists, available at http://www.federalreserve.gov/paymentsystems/debitfees.htm, are intended to help payment card networks and others determine which issuers qualify for the statutory exemption from interchange fee standards. The statute exempts any debit card issuer that, together with its affiliates, has assets of less than $10 billion.

To facilitate compliance with the debit card interchange fee standards in the Board’s Regulation II, 12 CFR part 235 (which implements section 920 of the Electronic Fund Transfer Act), the Board is publishing two lists of institutions using data available to the Board. These lists are intended to help payment card networks and others determine which issuers qualify for the statutory exemption from interchange fee standards.1 The statute exempts any debit card issuer that, together with its affiliates, has assets of less than $10 billion. The lists have been generated from the set of institutions in existence on December 31, 2010, according to the available data.2 Institutions have been grouped into two categories: Exempt and Not Exempt. Institutions in the Exempt category have been determined to have, together with their affiliates, reported assets of less than $10 billion, and therefore are exempt from the interchange fee standards under the statute. Institutions in the Not Exempt category have been determined to have, either individually or together with their affiliates, reported assets of $10 billion or more, and therefore are not exempt from the interchange fee standards under the statute.

In addition, a small number of debit card issuers may not appear on either of these lists, such as institutions for which the Board has incomplete affiliate data, de novo institutions for which the Board did not have financial data as of December 31, 2010, and issuers without federal deposit insurance. If an issuer does not appear on either of these lists and is exempt from the interchange fee standards, it should so certify to its participating payment card networks.

The interchange fee standards become effective on October 1, 2011. The Board plans to update the lists annually.

For media inquiries, call 202-452-2955.

Read the report and find the list here:

http://www.federalreserve.gov/newsevents/press/bcreg/20110712a.htm

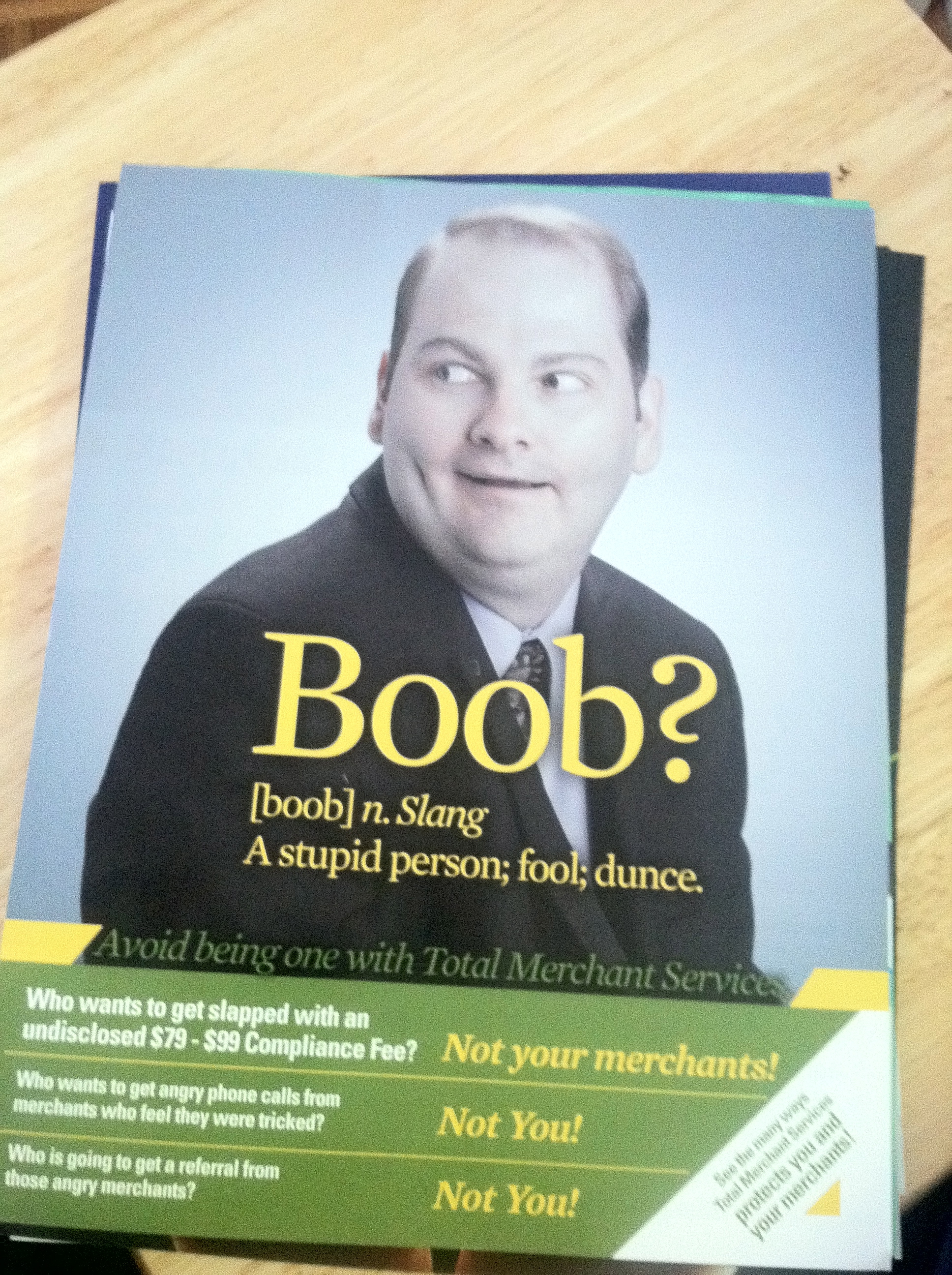

Sales Agents Are You A Doofus?

August 23, 2011

Update 1/16/2012: are you a boob?

The attached advertisement came tucked inside our latest issue of the Green Sheet. By now, this must mean that these ads are working for them. LOL.

————————–

Are you a doofus? A few folks in Basalt, CO are challenging resellers of merchant processing services to find out. Total Merchant Services recently launched an ad campaign touting their ability to maximize both customer and reseller satisfaction. But their target market is having mixed reactions, leading some to claim they have completely missed the mark.

And unlike many controversial ads, this one leaves no wiggle room for interpretation:

Avoid being inept in your career and work with Total Merchant Services!

Of course this may appeal to the younger resellers who are drawn in by flashy, satirical marketing. But for seasoned agents who’ve been in the business 5, 10, 20, and 30 years, they’re unlikely to be anything less than highly proficient. There’s a learning curve in the industry and the ones that turn it into a steady career have already figured out how to balance a good processing deal for both themselves and their customers.

If you click through to the actual full advertisement, it boasts that agents need not worry any longer about tricking their customers. “Who wants to get angry calls from merchants that feel they were tricked? Not you!” It says a lot about who they’re targeting.

Of course on the other hand, it may all just be a ploy to get their company some press. “Did you hear what Total Merchant Services did?!” Maybe you wouldn’t have if they ran the same plain vanilla ads that everyone else does.

Avoid being a dumb bastard and learn a few things at the Merchant Processing Resource!

What do you think?

– deBanked

“Don’t Make Us Pay” Goes Quiet

August 22, 2011Originally published on August 7, 2011.

As the Federal Reserve wound down the debit card debate on Capitol Hill, the “consumer rally” to fight against the reform followed suit. http://www.dontmakeuspay.org was/is a portal for individuals to lodge complaints with their local politican over a regulation that may potentially lead to higher debt card fees.For the most part, we championed this consumer movement since it was our belief that the Durbin Amendment would have unintended negative consequences.According to their site:

In December, the Fed issued a draconian regulation that reduces fees paid by retailers by 70 to 90 percent. As a result, the nation’s largest 2 percent of retailers will receive a $12 billion windfall – and debit card users like you will have to pay the tab.What does this mean for you? YOU could see higher fees, reduced rewards, and new debit card restrictions, unless Congress acts now to stop the rule.You shouldn’t have to pay more to use your debit card. TELL CONGRESS: DON’T MAKE US PAY.

Sounds logical enough right? We lodged our complaint with a few members of Congress and were immediately accused of astroturfing by politicians, bloggers, and retail chains. They got quite nasty too! Our advocacy for this movement led many to believe that our blog was secretly controlled by the big banks in order to create the illusion of a grass roots campaign by consumers. That was hurtful, especially since our site’s purpose is to provide businesses with free help to lower their fees, understand their statements, and make the best decision for themselves. It sure did wonders for our site traffic though, which experienced an 800% spike to all of our pages discussing debit card reform.

Although the debate pretty much ended with the final passage of the law on June 30th, 2011, the consumer movement to combat it died altogether. We have to admit that we’re a little surprised. dontmakeuspay.org has not updated their site since june 2nd, a full four weeks before the ruling. The silence is deafening, considering they used to post news several times a week. From what we’ve seen, the passage of a law never stopped the masses from voicing their discontent, especially if it was over something wildly unpopular.

But these consumers seemed to have vanished going into the homestretch and haven’t been heard from since. The banks themselves have acknowledged that the damage may not be as bad as anticipated and the retailers are claiming a mild victory. That was to be expected, especially since the final law called for an interchange cap that is nearly double than what was originally proposed. Regardless of who “won”, the opinions by both sides of the outcome have been published, politicized, criticized, or celebrated. But there seems to be no spokesman for the consumers who supposedly had been leading a crusade of their own. Are they happy with the outcome of the debit card law? Do they still believe that fees will still be passed down to them? We can’t answer their questions because the movement is seemingly MIA.

- A Retailer Celebrates: http://www.businessweek.com/magazine/sniping-at-charges-for-swiping-debt-cards-07072011.html

- A Card Issuer Tries to Stay Positive: https://debanked.com/apps/forums/topics/show/5593452-mastercard-sees-durbin-opportunity

- A Consumer Shares How They Feel: Nothing found…

Which brings us back to dontmakeuspay.org, the home base for the average Americans who believed they were about to get screwed. Even if the site was no longer being updated, surely we would find a band of angry consumers still discussing the issue on social networks like Facebook.

- Don’t Make Us Pay’s official FB Group: http://www.facebook.com/#!/group.php?gid=106108824431

Only 104 Members and the last wall post was on April 17th. Coincidentally it’s a link to an article we wrote on the topic (No wonder people thought we were directly involved). A Twitter search comes up with even less.

And so we come back to our readers with our tail between our legs. Dontmakeuspay.org was likely (just as many people accused) an astroturf campaign for the big banks. There was no national, cohesive consumer movement to fight the Durbin Amendment. Bummer.

But that doesn’t change our opinion of the legislation, nor the big banks. Increased fees were legitimately on the table but nobody was paying attention. It wasn’t until dontmakeuspay.org started slapping people in the face with mass transit posters, billboards, and internet advertisements, that the country began to realize how monumental the issue being debated was. Bringing a mass awareness to the public was a good thing and it may have ultimately achieved its goal. The proposed interchange cap went from 12 cents to 21 cents and 5 basis points, just high enough to save consumers from a world of hurt.

But that outcome should be overshadowed by the complete irony of it all. It is our opinion that both the retailers and the big banks got screwed together as a result of the reform. The only group that achieved victory, is the one that we know now didn’t even exist to begin with.

- Retailers will not see a decrease in their debit card fees. See: ‘And the Misinformation Continues‘

- Card Issuing Banks went from a limitless market rate to a strict profit killing cap

- Consumers see no rise in fees or elimination of reward programs in near future

Dontmakeuspay.org may have gone quiet, but while it was active, it helped the one group it claimed to represent. Call it deceptive, call it a decoy, call it misleading, or call it whatever you want. The big banks stuck their neck out for the little guy and the little guy won. It’s hard to hate on that…

– deBanked

https://debanked.com

Starting a Business – Read First

August 22, 2011Jerry had a business plan and some money set aside for startup capital. He assumed that’s all he needed, but six weeks later he was already out of business. What went wrong?

Starting a business is exciting and some entrepreneurs even describe getting an adrenaline rush as they approach opening day. But this impulsivity forward can lead to major mistakes, careless decisions, and ultimately put you on the path to failure. If you’ve got a lease on a storefront that opens May 1st, you should aim to open the business on May 1st. But if you are not prepared to handle the demands of your customers or conduct operations most efficiently, then you shouldn’t open just for the sake of opening.

- What can go wrong the week before opening – April 24th

1. Choosing vendors out of convenience or because they can meet an arbitrary deadline

Example: You’ve spoken to two advertising agencies about your startup. Both have quoted the same price. Company A can put together a promotional campaign by May 1st, your opening day. Company B can put together a promotional Campaign by May 18th, but it will be much more effective and reach a larger audience. Company B’s campaign is far more likely to bring in customers for the same price.

Believe it or not, with all the stress and time against their side, many entrepreneurs would rather pick Company A just for the immediate relief. It coincides with their opening day and it would feel great to have one less thing to worry about. But Company B would generate more revenue for them and thus would probably be the smarter decision.

2. Looking at the process like a checklist

Let’s say you’ve created a series of basic steps that must be completed before May 1st. In the last week, you go back to check and make sure they’re all done or to find out what you have left.

Example:

1. Create business plan

2. Raise capital

3. Lease store space or office space

4. Choose vendors for inventory, supplies, and equipment

5. Advertise

If your list is as basic as this, you’ve already failed. Each step should have a series of substeps.

Example:

1. Create business plan

– Survey prospects to determine if there is demand for this product (Don’t ask your family. They don’t count)

– Obtain a 2nd opinion from a qualified business advisor on your business plan

– Locate 10 weaknesses or shortcomings of your business plan (if you can’t find 10, you’re giving yourself too much credit)

– Find proof that a similar business model has worked before and dissect their plan

2. Raise capital

– Determine how much equity you are willing to sacrifice

– Set realistic goals for when your business will be able to start making payments, how often you can make payments, and how much you can afford in each payment

3. Lease store space or office space

– Determine several locations that would be ideal to reach your target market, whether or not there is space available there

– Determine if there is a way to obtain space in that area (sublease, a landlord looking to replace a tenant etc.)

– Determine which locations are actually available to lease

– Determine if any of them are suitable for your business (if none, DON’T open!)

– Determine if the costs justify the level of success you can achieve in that location

4. Choose vendors for inventory, supplies, and equipment

– Seek out terms on inventory as opposed to COD (very difficult for a startup to attain but it would be a huge difference in cash flow)

– Choose reputable vendors (don’t pick the cheapest just because cash is tight in the beginning. Low quality goods may turn your customers away)

– Choose how you will pay for supplies and equipment (lease or purchase. Leasing may be less expensive now but far more costly in the long run)

5. Advertise

– Shop around and learn about all the different ways these firms intend to help you reach your target audience

– Choose the company that will produce the most bang for your buck

– Use common sense (A 3 AM TV commercial is probably not suitable for a toy store etc.)

If you didn’t go through this whole list, there’s a good chance you’ll fail. And just when you think you’re sure you’ve got a handle on everything, buy a few books by people who have been in your shoes. Find out what they did, what challenges they faced, and how they succeeded or failed. We’re not talking about a short article like ours, but rather a full story that shares every detail, thought, and emotional feeling that you can expect to go through. There’s nothing like being prepared and it may even inspire you to modify your business plan as it currently stands. Don’t end up like Jerry. Doing things right is much better than doing things quickly.