Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Fork in the Merchant Cash Advance Road

August 23, 2011Originally Posted on April 25, 2011 at 10:48 PM

The Merchant Cash Advance (MCA) industry is growing, albeit slower than some may have you believe. But it’s moving in two opposing directions, a condition that’s making it tougher to describe the financial product itself in general terms. MCAs are becoming more expensive and a lot cheaper at the same time. HUH? You read that right.

Originally aimed at business owners with poor credit, the risk of default or delinquency was overcome by withholding a percentage of sales revenue directly. As the credit crisis and Great Recession took hold, it attracted businesses of all credit backgrounds and today it’s widely accepted as a lending alternative, rather than a solution to poor credit.

As MCAs pushed forward to compete for customers normally accustomed to bank credit lines, the cost was stiffly resisted. These businesses had a tough time envisioning their financing terms to be anything outside of some percentage over the Prime Rate. Since a MCA is supposed to be structured as a sale, there is no APR equivalent, no timeframe, no amortization, nor any real familiarities of a loan. As the past couple years have passed, the product is more publicly understood, but for it to actually catch on, the costs had to come down. Many funding providers now refer to such high credit, low cost accounts as premium, platinum, preferred, gold, etc.

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

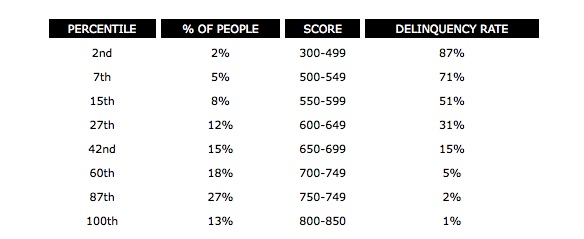

No matter which company ran the figures or how secret these portfolio statistics were, every funding provider came to the same realization. The lower the credit score of the business owner, the greater the chance of a problem. Why this came as any surprise, is a surprise in that of itself. The Fair Isaac Corporation (FICO) will have you know that any individual with a score below 499 has an 87 percent chance of being delinquent on a credit payment within the next 2 years. Delinquent, is defined as a payment of 90 days or more past due.

But wait… if a MCA is not a loan, nor does it depend on the business owner to make payments, then how can there be a risk of delinquency? Intentional manipulation of the revenue flow back to the funding provider can be relatively easy to do. A business owner could use spare POS equipment to accept card payments for which the funding provider is not aware of and therefore prevent the collection of funds. That’s a method known as splitting, and serious consequences can result when discovered. (Read more on what happens in the case of default or deliquency on a MCA in a previous article)

But outside the scope of malice, there’s the traditional reason, the inability to make payments. If the suppliers and wholesales aren’t being paid, then the business isn’t going to have inventory on hand to sell. If the rent isn’t being paid, then there’s not going to be any location to generate these sales. Essentially, the funding provider has a mutual interest in the business being able to satisfy ALL of their obligations, not just the MCA itself.

If there is an 87% chance that suppliers, landlords, or other essential creditors will not be paid on time in the next 2 years, then there’s an excellent probability that the business will be unable to operate at the same level. With no collateral as protection, the MCA industry has adapted to the challenge by raising the cost. Business owners with poor credit can expect funds to be expensive and the terms to be more restrictive. Lower funding amounts, higher withholding percentages, and the sacrifice of any negotiation is the price the MCA industry has set to make funding to the maximum risk group possible. These programs, which are now often referred to as starter advances, don’t work for everyone so the pros and cons should be weighed prior to executing a contract.

Both the premium advances and starter advances have experienced extraordinary growth to the point where they have become niches of their own. There are now starter advance companies and premium advance companies. Funding providers like Strategic Funding Source have taken the product a step further and reportedly did a MCA for an exhibit at the Tropicana Hotel in Las Vegas for $4 Million. Contrast that with deals that are struck for as little as $750. And we can’t fail to mention that some have taken it back to the basics, a loan. ForwardLine in Woodland Hills, CA lends money to businesses which are then repaid in accordance with a predetermined, fixed pace through the card sales. They have reintroduced concepts like APR back to the finance world.

If we continue at the current pace, MCAs will become less expensive, more costly, a lot bigger, and markedly smaller. We’ve come to the fork in the road for what the Merchant Cash Advance industry seeks to brand itself as. Loan alternative? First choice? Backup plan? Is it for smaller businesses or larger ones? Should it go the way of lending or continue to remain a structured purchase of future card sales? Is industry cohesion really necessary or will increased decentralization lead to greater acceptance of this financial product a whole? Will there come a time when America’s big banks swallow the industry up, buy out the existing portfolios, and add this product to their financing arsenals?

These are tough questions. Merchant Cash Advance is evolving, growing, and no longer moving in one direction. While we contemplate our next step, one thing is for certain, there’s no turning back.

– deBanked

www.merchantprocessingresource.com

The Interchange Debate: A Political Mess and a Waste of Time

August 23, 2011

The Huffington Post published a lengthy article today, titled “Swiped: Banks, Merchants And Why Washington Doesn’t Work For You.” While it reiterated the talking points for both sides of the Durbin Amendment debate, it made the case for neither. Rather it highlighted the dirty business of Washington politics. Millions of dollars are being spent on an unrelenting battle, which frankly will result in no winner.

Debit interchange reform was enacted in Australia in 2004 after an exhausting four year debate. The outcome? No savings were passed on to consumers and debit card use declined nationally. We broke down the findings in a previous article: Interchange Regulation and Reduction, Proof it Will Fail.

We will not make our case here again, but instead would like to point out the refreshing perspective by the Huffington Post:

“As swipe fees dominate the Congressional agenda, a handful of other intra-corporate contests consume most of what remains on the Congressional calendar: a squabble over a jet engine, industry tussling over health-care spoils and the never-ending fight over the corporate tax code.

The endless meetings and evenings devoted to arbitrating duels between big businesses destroy time and energy that could otherwise be spent on higher priorities. In America today, over 13 million people are out of work and millions more are underemployed. One out of every seven is living on food stamps. One out of every five American children lives in poverty. Yet the most consuming issue in Washington — according to members of Congress, Hill staffers, lobbyists and Treasury officials — is determining how to slice up the $16 billion debit-card swipe fee pie for corporations.”

We don’t remember debit card fees causing the Great Recession. We do remember the corrupt mortgage brokers, the exotic derivative securities, the overly leveraged investment banks, and the deficit spending at all levels of government. Repeal the Durbin Amendment or support the Debit Interchange Fee Study Act so we can undo the damage already caused and move on to more important matters.

– deBanked

Sony Breach a Result of PCI Compliance Failure

August 23, 2011

As a result of Sony’s network security breach, as many as 2.2 million customers may have had their credit card information compromised. Certain sources allege that this data is now for sale on the black market. In the age of Payment Card Industry Data Security Standards, how could this information have been vulnerable and who is to blame?

The PCI Security Standards Council (https://www.pcisecuritystandards.org) would point the finger at Sony. Businesses have all the guidance and equipment at their disposal to keep customer information safe. if they fail to adhere to the standards or don’t take them seriously, we end up with dreadful situations like this. The Ponemon Institute estimates the average per customer cost of a data breach to be around $200. If indeed 2.2 Million customers have been compromised, then Sony will have about $440 Million at stake. And that’s just the tip of the iceberg. There are over 77 million Playstation Network players, all with varying levels of private information in the network’s files. With all considered, the potential damage could exceed $15 Billion.

And it’s already begun. Playstation gamers recently filed a class action lawsuit in Sacramento, CA. Ira Rothken, the lead attorney handling the case, is quoted in the Green Sheet as saying “I can’t think of a major data breach where the company was PCI compliant,” he said. “I think it is likely Sony was not PCI compliant. There were a lot of red flags that suggest Sony knew or should have known their system was vulnerable.”

It’s a shame Sony didn’t heed our advice earlier. In January we wrote that 60% of merchants are unaware of the costs they would incur for a data breach. Full Compliance involves a lot of things, including an annual self assessment test. Even the corner deli is subject to these mandatory procedures. For information on how to avoid the situation that Sony is in, please refer to the PCI Compliance section of our site.

Seriously. If Sony is vulnerable, you probably are too.

– deBanked

Jack Dorsey Reveals Tweeting Irrelevant with Square

August 23, 2011Posted on May 1, 2011 at 11:33 AM

Twitter co-founder Jack Dorsey built his original company with toothpaste makers in mind. He might even say, “Thanks to Twitter, people in Istanbul can finally get tips on what makes the smiles in Shanghai so white. Tips on scrubbing those molars are transmitted in real time from Rio de Janeiro to Moscow!”

That’s good news for companies like Colgate, but for companies involved in technology, Dorsey reveals that Twitter is basically useless. “No one is following your company’s mundane tweets. No one cares if the Square card reader got a thumbs up from a business owner in Maine.” Of course he hasn’t actually said this in words, but his actions speak volumes.

Dorsey is also the founder and CEO of Square (https://squareup.com/), a credit/debit card reader that can plug right into an iPhone, iPad, or Android. We follow them on Twitter to keep an eye on news that might be worth sharing. But the only news, is no news. What’s up with that?

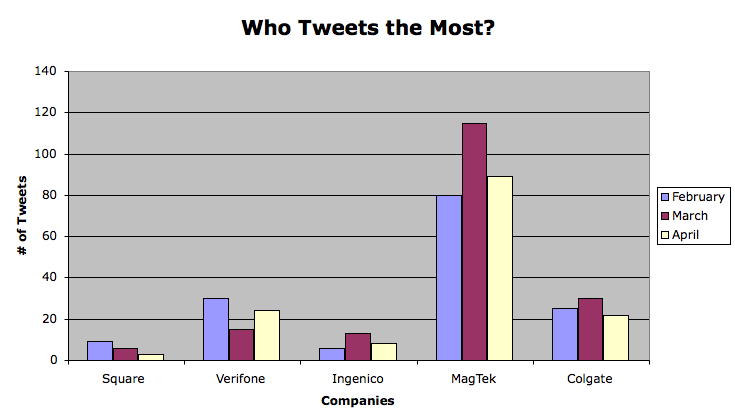

We compared Square’s tweets to three POS hardware companies, Verifone, Ingenico, and Magtek. We threw in Colgate for good measure.

Square, led by Twitter’s Dorsey, ranks last among peers in average monthly tweet volume. As Square seeks a permanent place for itself in the electronic payments world, it has undertaken a massive public relations campaign. None of which includes tweeting. Thank you Mr. Dorsey for revealing what most of the world already suspected, that commercial tweeting is useless.

Verifone just ate a bologna sandwich #yum

Ingenico just donated a credit card machine to a school in Sudan #charity

Magtek was mentioned in a newspaper in Andorra #werule

Colgate just came out with purple toothpaste #purple

Square just stole everyone’s customers while our competitors were tweeting about bologna #winning

Follow:

http://twitter.com/#!/VeriFone

http://twitter.com/#!/ingenico

http://twitter.com/#!/ColgateSmile

– deBanked

Kabbage: The Merchant Cash Advance of the Online Business World

August 23, 2011

Show me the Kabbage! Kabbage offers working capital to Ebay sellers that have difficulty qualifying for a bank loan.  They describe their financial product as an advance and funds are collected back automatically via the seller’s PayPal account. Sound strikingly similiar to something else?

They describe their financial product as an advance and funds are collected back automatically via the seller’s PayPal account. Sound strikingly similiar to something else?

Kathryn Petralia, the COO of Kabbage provided details in an interview with practicalcommerce.com. Funding ranges from $2,000 to $15,000 and approval is based on the following factors:

- Minimum 1 year in business

- Historical Ebay sales volume

- Historical PayPal account activity

- Credit score (although they are flexible)

- Business type

- Chargeback history

Petralia describes the cost as fee based, not rate based. “So it’s a maximum six month period that an advance can be held by a merchant and all of the merchants have to enroll in auto-payback system via PayPal. We automatically take a percentage of the initial advance amount every month. So the idea is in no more than six months, this sum of money will be paid off. A business will not be approved for an amount they cannot payback in that timeframe.”

Take away the fixed timeframe and we have all the signature features of a Merchant Cash Advance (MCA). The term loan, is even for the most part absent from Kabbage’s website. It’s difficult to overlook another feature of Kabbage, the ability to obtain funds in 10 minutes.

It’s easy to see if you qualify for an advance with Kabbage. Do you have about 5 seconds to spend with us? Simply enter your eBay marketplace ID and we will start the process. If you have sufficient activity and a great history of selling on eBay, we will then ask you to complete our application. You can go from eBay ID to cash (in your PayPal account) in as few as 10 minutes!

10 minutes? Traditional MCA funders don’t move THAT fast, nor should they. There’s a few things that alternative funding sources have learned since the financial crisis, and that’s not to go overboard. Funding in 10 minutes is great for the business owner, but doesn’t give the funding company any time to actually underwrite the deal. There’s a few questions we would like Kabbage to answer or consider.

- Do you ask where your applicants store their inventory?

- Is drop shipping an acceptable business model?

- Do you ask applicants if they’re current on their business property or home? If they’re renting a location, this isn’t going to show up on their credit report. If they’re on the verge of eviction, how would you know?

- Do you require contact information for any of their suppliers?

- Do you perform a criminal background check on your applicants?

- If the business conducts sales on a separate website in addition to their Ebay store, what’s to prevent them from discontinuing their Ebay operation while a balance is outstanding?

- What is the recourse in the case of default? What collateral is there?

- What if a business stops using the designated PayPal account and starts using another one. Are there any worthwhile deterrents?

- What if Ebay changes how they conduct business in a way that prevents or decreases the sales capability of their sellers? Are you prepared to adapt?

Though Kabbage is not exactly a Merchant Cash Advance, it’s close enough that we should welcome them to the community. A few tips for these folks though. The more automated the approval process, the higher the default rate. Does a business really need funding in 10 minutes or less? Also, the less grounded a business is, such as a long term lease in a brick and mortar location vs. an Ebay store, the less likely they will survive in the long run.

Good luck!

– The Merchant Cash Advance Resource

Our Favorite Merchant Cash Advance Commercials

August 23, 2011Posted on May 7, 2011 at 1:23 AM

TV has never been a popular venue for Merchant Cash Advance (MCA) providers to advertise. There is a highly specific target market, small business owners that accept credit cards as a form of payment that are looking for funding, that simply reduces the cost effectiveness of mass media. Why pay to reach 100 people when 97 of them may not even fit basic criteria such as owning a business? It doesn’t make sense.

TV has never been a popular venue for Merchant Cash Advance (MCA) providers to advertise. There is a highly specific target market, small business owners that accept credit cards as a form of payment that are looking for funding, that simply reduces the cost effectiveness of mass media. Why pay to reach 100 people when 97 of them may not even fit basic criteria such as owning a business? It doesn’t make sense.

That doesn’t mean that TV or online video commercials for MCA don’t exist, they do. Unfortunately most of them tend to be poorly self-produced webcam miniclips that are so boring, they are more likely to turn someone away from the product, than to help anyone. No offense. But there are some providers that actually took the time, effort, and money to create something worth watching. Here are some of our favorites:

Does anyone else have one they’d like to share? We’ll be happy to show it off!

– The Merchant Cash Advance Resource