Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Advertising in deBanked’s E-mail Newsletters is Sold Out

November 1, 2015deBanked’s twice-monthly email newsletters have had such tremendous industry reach that advertising space in them is currently sold out.

Thanks to everyone that has made them such a huge success. Our readership continues to get bigger and bigger.

deBanked still has limited availability in its other channels including website sponsorship, print magazines, and email blasts. If you are interested in that, please give us a shout.

Money2020 Photos

November 1, 2015Below are some of the shots we got at the 2015 Money2020 Conference in Las Vegas!

Did you go to money2020? Feel free to send us some of your photos 🙂

Letter From the Editor – November/December 2015

November 1, 2015 Somehow 2015 is already over. It started off as the year of the broker but it ended up as a culmination of many things. It was the year of capital raising and rebrands, the year of regulatory interest and RFIs, the year of unicorns and leaderboards. 2015 solidified alternative lending’s place across multiple continents. Bankers started talking like technologists and technologists like bankers.

Somehow 2015 is already over. It started off as the year of the broker but it ended up as a culmination of many things. It was the year of capital raising and rebrands, the year of regulatory interest and RFIs, the year of unicorns and leaderboards. 2015 solidified alternative lending’s place across multiple continents. Bankers started talking like technologists and technologists like bankers.

In 2015, we introduced William Ramos who went from working at a Lowes Home Improvement store to driving a Maserati after he landed a temporary job as a financial cold caller. We also showed you Jared Weitz, who went from working as a plumber to running a financial company that’s now on pace to originate $100 million in small business funding a year.

As we close out 2015 here, we’ll introduce you to the man whose company is producing billions (that’s billions with a ‘b’) of small business funding. Daniel DeMeo is the CEO of CAN Capital, a company who has weathered both the dot-com bust and the financial crisis and still manages to be one of the industry’s top players. DeMeo shared what he’s all about and the story of CAN you haven’t read anywhere else.

That’s the good stuff, but there’s some bad stuff too. While critics have broadcast some of the not so flattering stories in alternative lending’s rise, there’s a darker side that no one has dared write about, bad borrowers. Perhaps a byproduct of rapid technological change, merchant fraud has become an all too common occurrence. These predatory merchants are causing chaos, damaging margins, exploiting underwriting weaknesses and potentially driving up the cost for the good guys. In this issue, we explore the reality of bad guys and their tactics.

And that’s not all we have of course. In 2015, we compiled the first report on merchant cash advance and small business lending in collaboration with Bryant Park Capital. We measured the industry’s growth, learned of its diversity, and got a numerical sense of the confidence for the future. A sample of that report is included within.

That was 2015 summed up, the year that Marty McFly met us all in the future. 2016 will undoubtedly mean robots, laser beams and interplanetary colonization. Sprinkled in between all that will be online loans, merchant cash advances, bitcoins, and financial disruption. In 2016, the world may become deBanked once and for all.

–Sean Murray

Blurring Small Business: A Troubling Narrative is Gaining Steam

October 30, 2015Almost 18 months ago at LendIt’s 2014 conference, Brendan Carroll, a partner and co-founder of Victory Park Capital said that in regards to business lending, “the government doesn’t have the same scrutiny on this sector as it does in the consumer space.”

This double standard is the crux of American capitalism. In business you can win or lose, be smart or foolish, risk it all or play it safe. Government regulations don’t let the average consumer be subjected to the same stakes. They are viewed to be at a natural disadvantage against businesses and thus there are laws to protect them, and perhaps rightly so.

Since entrepreneurship is a choice, businesses and the people that own businesses are held to a higher standard of acceptable risk taking. In the free market, the pursuit of profit holds the system together.

This economic worldview is part of the reason why entrepreneurial TV shows such as Shark Tank are so popular. In the Tank, contestants can just as easily walk away with a terrible deal as they can a good one. And when bad deals get made, and they do, I’ve yet to see regulators descend on the set to fine or arrest Daymond John, Kevin O’Leary, or Barbara Corcoran.

But Shark Tank features entrepreneurs on a remote stage detached from their daily environment, giving it the look and feel of a game show. If you want to see cold hard dealmaking with mom-and-pop shops on an up close and personal level, just watch CNBC’s The Profit. On the show, small business expert Marcus Lemonis does not sugarcoat what he is. “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother,” he bluntly told one small business owner. It doesn’t matter if it’s a family owned store or a full fledged corporation, Lemonis is looking to make a deal and make some money. When it comes to business, he is well… all business.

Just as the CFPB hasn’t shut down Shark Tank, (which one has to wonder if they’ll be subject to Reg B of Dodd Frank’s Section 1071) none of Lemonis’ deals have been scrutinized by a Federal Reserve study, nor has the Treasury Department issued an RFI to better understand why entrepreneurs go on the show in the first place.

It’s no wonder then at LendIt 2014, Carroll also said that there wasn’t the same sort of moral hurdle when it came to institutional capital investing in business lenders as opposed to consumer lenders.

Moral was a telling word choice because the morality of certain commercial transactions have recently come under fire by groups claiming to represent small businesses. The premise of their argument is that commercial entities are no more sophisticated than consumers, that a corporation and the average joe are equal in their ability to take risks and make decisions for themselves.

Their evidence is that sometimes in business-to-business transactions, particularly in lending, one side accepts terms that would be considered far outside the norm for consumers, terms that violate a moral threshold. One has to wonder where a loan with an infinity percent interest rate ranks on this morality scale, a deal that’s actually been made and accepted several times on a TV show. Referred to as a “Kevin deal” since they are Kevin O’Leary’s favorite, the borrower is obligated to pay a perpetual royalty on top of repaying the loan itself. In simple terms, it’s a loan that can never be paid off.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

The fact that Wicked Good Cupcakes decided what made sense for them and was happy about it, damages the storyline that businesses need to be saved from their own decisions. But there’s another problem, government entities themselves may be inadvertently effectuating this false narrative by inferring incorrect conclusions from their own research.

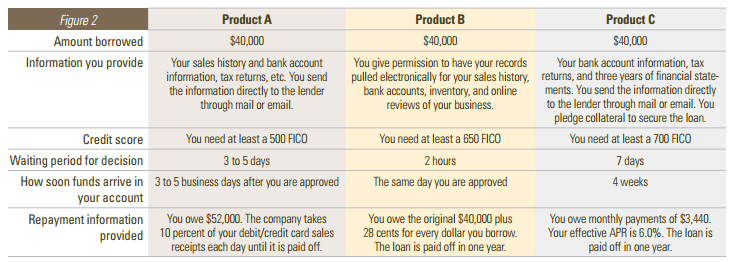

Nowhere is this more evident than in a report recently published by the Federal Reserve Bank of Cleveland that analyzed small businesses and their understanding of “alternative lending.” The report shared the results of two focus groups that had been shown terms for three hypothetical products that supposedly represented actual products in the real world.

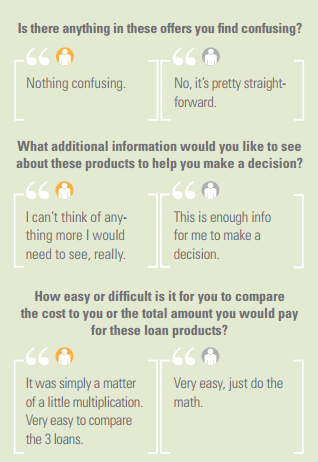

Unsurprisingly, the report concedes “when comparing the products, participants initially reported the three were easy to compare and that they had all the information to make a borrowing decision.” But the researchers pressed on until they got an answer that fit their expectations, that small businesses are confused when it comes to money and finance.

In a hypothetical scenario where a commercial entity sold $52,000 of future receivables for $40,000 today, it stated that the “lender” would withhold 10% of each debit/credit card transaction until satisfied. Participants were then asked to guess the interest rate on this loan if they paid it back in one year. That caused a lot of folks to scratch their heads and that’s because it was a trick question.

The question itself introduced conflicting facts and lacked crucial variables to make an intelligent guess. Nevermind that respondents prior to that question said that there was “nothing confusing” about the products presented as is. The original feedback should’ve been enough. Below are some of the responses offered before they were deliberately tricked.

- “Nothing Confusing.”

- “No, it’s pretty straight-forward.”

- “I can’t think of anything more I would need to see, really.”

- “This is enough info for me to make a decision.”

The researchers concluded however that the answers to their trick question suggested there were “significant gaps in their understanding of the repayment repercussions of some online credit products and the true costs of borrowing.”

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

But even if that was the case, at what point does confusion become unfair in a purely commercial transaction? And what would be an appropriate remedy?

We’ve been down this road before where federal regulators have set mandatory disclosures in order to bring transparency to a lending environment believed to be obscure. And just recently on September 17th, 2015, the House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access pressed community bankers on the impact of such measures dictated by Dodd-Frank.

Congressman Trent Kelly asked if all the added new pages to loan agreements make it easier for their borrowers to understand. “Do they understand what they’re signing?” he asked.

B. Doyle Mitchell Jr., the CEO of Industrial Bank that was speaking on behalf of the Independent Community Bankers of America responded that they do not. “It is not any more clear,” he answered. “In fact it is even more cumbersome for them now.”

If anything, the Federal Reserve study offered compelling evidence that small businesses are happy with the way alternative lenders are currently disclosing their terms. It is only when government researchers tricked them that they became confused. That should say it all.

One consequence of entrepreneurship is that businesses are not created equal in their ability to assess financial transactions and no amount of disclosures or intervention can save them. There must be losers in order for there to be winners.

Case in point, there are lenders out there doing deals so lopsided that they actually turn to each other and say, “I can’t believe she took that.” Such is the case of RuffleButts, a children’s fashion line that appeared on Shark Tank in 2013.

“When they wake up, they’ll realize they messed up,” said Mark Cuban in reference to the deal Lori Greiner proposed and closed. An article on BusinessInsider.com covered the episode and unabashedly concluded, “Shark Tank isn’t a charity. The investors are putting in their own money, so they have every incentive to push to get the best deal possible for themselves.”

Shark Tank has risen in popularity because it is a reflection of a culture that believes dealmaking, both good and bad, is inherent to the endeavor of entrepreneurship. When a bad deal is made, regulators don’t come on the show to urge a do-over.

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

And if the Federal Reserve study indicated anything, it’s that business owners feel there’s nothing confusing about these deals.

So it would seem that everything as Americans know it, watch it and understand it, is business as usual.

Even Brendan Ross, the president of Direct Lending Investments, was quoted by the BanklessTimes as saying, “I want to emphasize there’s absolutely nothing novel about lending money to businesses. This isn’t some phenomenon we are rediscovering. There isn’t going to be increased regulation because this isn’t new.”

Perhaps the only thing that could be considered new is that loan sizes have gotten smaller and the types of products small businesses can access has diversified. Along the way, some of these new startups have decided to offer products in line with a self-professed moral code, which is to deliberately lend money at a loss and lash out at lenders who seek profit.

There’s a term for lending startups that don’t make money. They’re called “failed startups.” By casting small businesses as being no different from unsophisticated consumers, it’s quite possible that shows like Shark Tank and The Profit would become illegal in the process. Disclosures meant to help make things more transparent could actually make things less clear and more cumbersome, just as they have in the past.

I don’t think anybody is in favor of small business failure or an environment where confusion prevails, including the guys making infinity percent interest loans like Kevin O’Leary. But if the goal is to increase transparency, it should be in a way that businesses on both sides are content with.

The Federal Reserve study showed the system is working well as is and that prescribing mandatory changes to fit some universal standard would only serve to usher in an era of confusion that everyone is trying to avoid. Lenders can always do better to serve their clients, but the free market must prevail. As Mitchell, Industrial Bank’s CEO said when he testified in front of the Small Business Committee, “the problem with Dodd-Frank is you cannot outlaw and you cannot regulate a corporation’s motivation to drive profit at all costs so while it has a lot of great intentions in over a thousand pages, it has not helped us serve our customers any better.”

Alternative Lenders Are Waiting for a Shakeout

October 28, 2015 Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Loan terms are getting longer, rates cheaper and the cost to acquire borrowers higher. Somebody has to be feeling the pressure but in a rather benign economic and regulatory environment, it’s clear skies.

Valuations are soaring. SoFi is valued at more than $4 billion and Kabbage at more than $1 billion.

But Robert Greifeld, the CEO of Nasdaq warned attendees about the validity of private market valuations. “A unicorn valuation in private markets could be from just two people,” he said. “whereas public markets could be 200,000 people.” At best he described a private market valuation as being just a rough indicator.

And some wonder if these valuations are based on just scale, rather than the ability to underwrite more intelligently and efficiently than a bank. OnDeck for example, had a Compound Annual Growth Rate (CAGR) in originations of 159% from 2012-2014 when the average originations CAGR for their peers is currently 56%. But OnDeck has the advantage of time. With nearly a decade of data under their belt, they’ve been able to see what works and what doesn’t.

“You have to have enough bad loans to build a good credit model,” said OnDeck CEO Noah Breslow during a Money2020 panel discussion.

For Aaron Vermut, CEO of Prosper, getting their company to the next level was about having access to institutional capital. As a marketplace, and as a company that almost died several years ago, he pointed out, institutional money was the inflection point for them to grow. The peer-to-peer model that actually depended purely on “peers” is what held their company back.

One thing several lenders seemed to agree on was the limited applicability of FICO. FICO is not the thing to use for a small business loan, said Sam Hodges, Managing Director and Co-founder of Funding Circle. His words didn’t come as a surprise since credit scores are generally the domain of consumer lending.

But doubts about FICO’s ability to predict performance didn’t just come from the commercial finance side. Prosper’s Vermut explained that consumers still think their FICO score is the most important factor in the rate they get. So even though they’ve got a system to predict repayment outside of FICO, they’re kind of forced to incorporate it because consumers are being educated to believe that’s what matters most.

The irony was not lost that as Vermut said that on a panel, he was seated next to Kenneth Lin, the CEO and founder of Credit Karma, a company that educates consumers about credit. “A credit score is one of the most important components of a consumer’s financial profile,” says Credit Karma’s website. Such language puts a tech-based lender with their own scoring model perhaps at odds with what their own prospects believe.

For instance if a potential borrower with a 750 FICO score is offered a high interest rate because the lender’s advanced and more in-depth underwriting determined them to be high risk, they’re going to walk away confused.

That of course begs the question, who needs to change? Those educating consumers about credit scores or the lenders who are moving away from them?

Before educational services shift though, it would probably make sense if the lenders can prove that their non-FICO dependent systems will work in the long run. And the sentiment among many lenders is that there are plenty of flawed models out there that will inevitably fail. That makes a shakeout not just a matter of if, but when.

Six months after LendIt, everybody is still standing. Whispers from in and around Money2020’s halls and exhibit floor revealed that the confident lenders wish the correction would happen sooner rather than later but that they are prepared to wait however long it takes.

Right now, confidence about the future on the commercial finance side came in at an 83.7 out of 100, according to the Small Business Financing Report. While there are no other points of reference to compare that to, industry captains are generally very bullish.

That could mean that for those secretly under tremendous pressure already, you could be left waiting for a shakeout for a very long time.

MCA & Small Business Lending’s Compound Annual Growth Rate (CAGR)

October 25, 2015 If you haven’t seen the industry’s first Small Business Financing Report prepared by Bryant Park Capital and deBanked, you can DOWNLOAD IT HERE. These are the only statistics from the survey that are being shared publicly. A more comprehensive report will be privately available about three weeks from now.

If you haven’t seen the industry’s first Small Business Financing Report prepared by Bryant Park Capital and deBanked, you can DOWNLOAD IT HERE. These are the only statistics from the survey that are being shared publicly. A more comprehensive report will be privately available about three weeks from now.

Seven of the respondents in the study were on pace to originate more than $100 million in 2015 and overall the industry was found to have a three-year Compound Annual Growth Rate (CAGR) in originations of 56%. For comparison’s sake, OnDeck had an originations CAGR of 159% from 2012 to 2014 according to their quarterly reports.

The numbers show an explosive industry and evidence as to why OnDeck may have been the first to go public. CAN Capital, by contrast has a five-year originations CAGR of 29% according to Orchard Platform. While perhaps lower than the industry average, it’s an astounding figure considering they’re a 17-year old lender.

According to Morgan Stanley analysts, a broad evaluation of “marketplace lending” originations will continue to grow at a CAGR of 47% through 20%.

There is apparently a lot more room for growth.

The Industry’s First Small Business Financing Report Revealed

October 25, 2015deBanked teamed up with Bryant Park Capital, an investment bank providing M&A and corporate finance advisory services to emerging growth and middle market public and private companies, to conduct the industry’s first comprehensive report.

Our initial findings are drawn from a survey of twenty-seven C-level participants, whose companies primarily offer merchant cash advances and small business loans. Combined, the participants represent more than $1.9 billion in annual origination volume. The survey was sent to over one-hundred eligible respondents, with participation open to all of them equally and included both direct funders and brokers.

- Thirteen respondents reported being on pace to originate $50 million or more in 2015.

- Seven respondents reported being on pace to originate $100 million or more in 2015.

Analyzing the origination volume of participants over a three-year period, the industry was determined to have a:

Compound Annual Growth Rate of 56%.

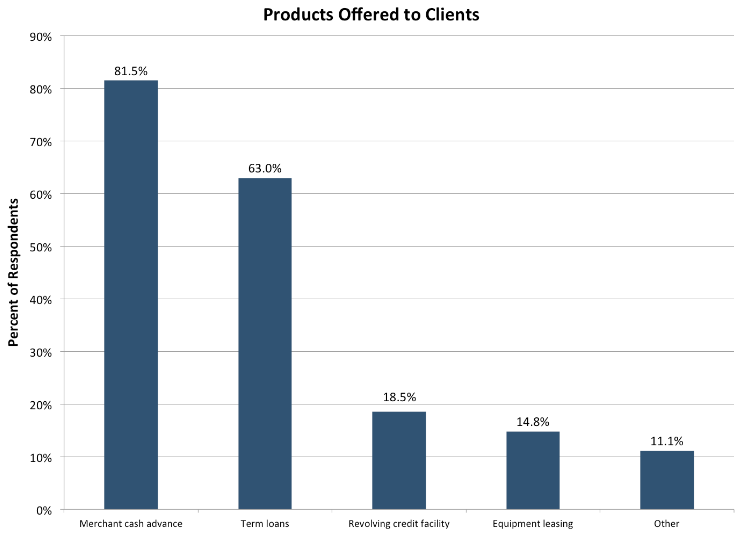

THE INDUSTRY HAS A DIVERSIFIED PRODUCT MIX

Respondents revealed a diversified product mix beyond merchant cash advance. Five participants actually reported originating no merchant cash advances at all and instead offered term loans or other products.

THE INDUSTRY CEOS HAVE A CONFIDENCE INDEX OF 83.7

Based on responses from CEO/participants asked to give their confidence level in the continued success of the small business lending/MCA industry over the next 12 months on a scale of 0–100, with 100 being the highest.

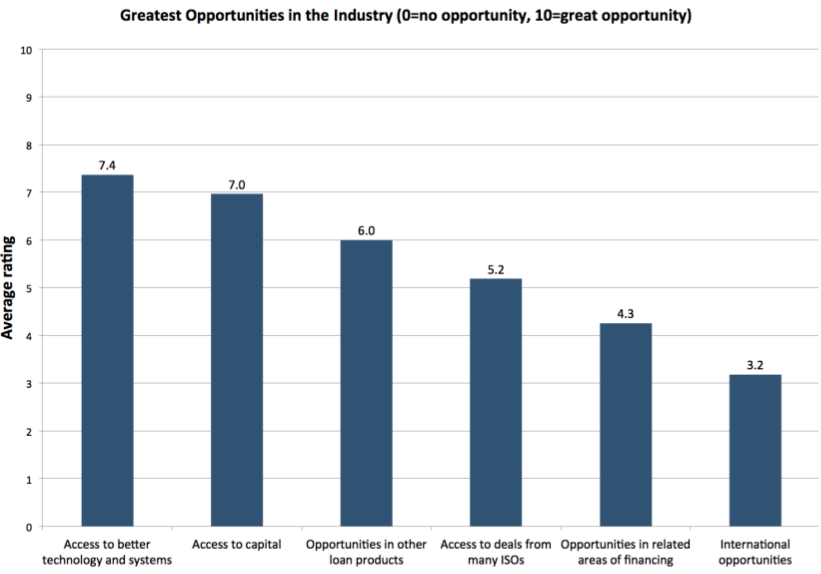

ACCESS TO BETTER TECHNOLOGY AND SYSTEMS IS THE GREATEST OPPORTUNITY IN THE INDUSTRY

Based on responses from participants asked to score the importance of opportunities on a scale of 0–10, with 10 being the highest.

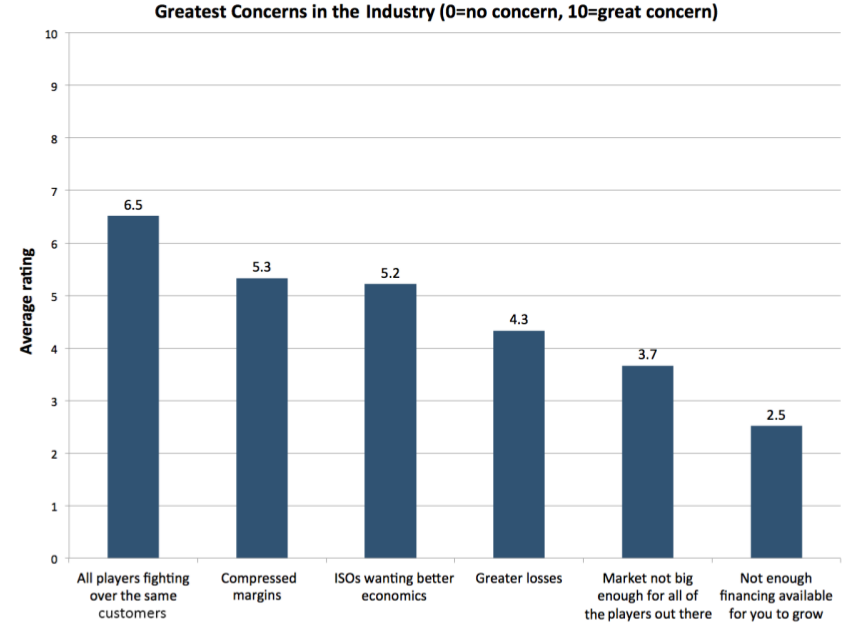

ALL PLAYERS FIGHTING OVER THE SAME CUSTOMERS IS THE GREATEST CONCERN IN THE INDUSTRY

Based on responses from participants asked to score their concerns on a scale of 0–10, with 10 being the highest.

The identities of participants and their individual responses are confidential. Participants were asked a total of 27 questions and had the ability to waive a response to any question, including the disclosure of their identity to the surveyors themselves.

Survey participants are eligible to receive the full anonymized report. Industry players who complete the full survey will automatically receive a full copy of this report. If you are not part of an operating company in the industry and you would like to obtain a copy of the report or participate in the survey, please contact Bryant Park Capital or deBanked.

DOWNLOAD THE PDF VERSION

Talk With us at Money2020

October 24, 2015I will be available at Money2020 in Las Vegas on Monday and Tuesday. If you are involved in marketplace lending, b2b lending, merchant cash advance or a related product, please e-mail me at sean@debanked.com or connect with me on twitter via @financeguy74.

I will be capturing stories for inclusion in both our November/December magazine issue as well as our online blog and newsletters.