Articles by deBanked Staff

Is OnDeck Back On Deck? – Industry Veterans Weigh In

March 8, 2016 After an unpleasant seesaw ride, Ondeck’s stock bounced back to its pre-earnings levels hovering around $8. The lender’s stock crashed 20 percent following its financial earnings on February 22nd due to a soft forward guidance.

After an unpleasant seesaw ride, Ondeck’s stock bounced back to its pre-earnings levels hovering around $8. The lender’s stock crashed 20 percent following its financial earnings on February 22nd due to a soft forward guidance.

The online lender funded a record $557 million in loans in Q4 2015 and generated $68 million in revenue but it wasn’t enough to make up for the $4.6 million in loss. As deBanked commented earlier, the markets can be unforgiving and irrational in its speculation of a downturn. And while OnDeck prides itself for being a company built for downturns because of its short-term repayment cycle, its stock has slumped over 65 percent since its December 2014 debut.

deBanked spoke to experts to ask how reflective this was of the industry and if this portends a larger economic gloom. Here’s what they had to say:

Downturn Survival? Not So Sure

David Obstfeld and Eric Cavalli of merchant cash advance provider S.O.S Capital, think that the market reaction to OnDeck is too strong, even unwarranted. “This is a fairly new industry and many don’t understand it yet,” said Cavalli. “Everybody is expecting an economic downturn and since this is an unproven business, one cannot really comment on whether MCA and the small business lending industry will actually survive.”

While OnDeck’s big data-led algorithmic lending has brought about a major shift in the industry, Obstfeld and Cavalli suspected that it might be why the company lost touch with the ISO base they relied on when it started.

OnDeck, Not On Deck

OnDeck, Not On Deck

Heather Francis of Elevate Funding does not consider OnDeck a part of the alternative finance industry given its business model and its fintech brand identity. “OnDeck has a brand issue, they want to be a software company on one hand and an alternative bank on the other,” Francis said. “The marketplace does not know what to do with them and no one sees what OnDeck sees in the mirror.”

Francis also commented that the hype around algorithmic lending is driven less by success and more for investor appeal in fintech. “OnDeck and Lending Club have a lot of capital behind them but there will be a lot of segregation between these companies and the traditional alternative finance companies. OnDeck cannot handle any kind of downturn.”

Just Process, Not Alarm

Corey Cicero at Platinum Rapid Funding considered the market reaction to be harsh and said that this is a normal trajectory for any company. “They are a market leader as far as brand names go. They have a lot to validate their leadership and they are on everybody’s bank statement who has a merchant cash advance,” Cicero said. “I don’t think the stock will be affected further. Congress is figuring out what to do with the industry, everyone else is figuring it out. This is a process.”

Industry Trends

Obstfeld at S.O.S Capital expects a major shakeout in the lending industry. “The market is saturated and in the next six months, the reputable companies will slash rates and when rates cannot be lowered further, companies will get creative with products and pricing.”

And Francis thinks that shakeout could come in the form of consolidation. “The market will shrink and people will spend more to get more origination and the most eye-catching product appealing to millennial entrepreneurs will take off.”

Meanwhile, Cicero at Platinum Rapid Funding said he thinks that there will be a purge of people writing bad loans. “This industry has a low barrier to entry leading to too much competition. People who write bad loans will be weeded out and the industry will correct itself.”

Wedding Financier Lends $1 million Each Month

March 5, 2016 Wedding financier, Promise Financial, announced that it crossed $5 million in loan originations and is now lending more than $1 million each month.

Wedding financier, Promise Financial, announced that it crossed $5 million in loan originations and is now lending more than $1 million each month.

There are over 2,000,000 weddings annually with an average cost of $30,000. And Promise’s loans range from $3,000 to $35,000.

The Hoboken, New Jersey-based wedding financier also has tie ups with over 50 wedding venues, planners, and photographers. “As we grow, we’ll continue to focus on technological innovation and excellent customer service to help our customers proactively plan their financial future,” said Bradley Vanderstarren, President of Promise Financial. The company uses big data to underwrite.

Promise is not the first online lender to hone in on the wedding market. Prosper Marketplace, another online lender, targets couples one step earlier by offering engagement ring financing. “While we at Prosper may not be experts at finding the right engagement ring, we can help you apply for a great rate on a jewelry loan to purchase it,” their website says.

Promise also does engagement ring loans and honeymoon loans. Prosper Marketplace goes even further by offering baby and adoption loans.

Big Banks Will Buy Small Lenders, Says Deloitte

March 4, 2016The marketplace lending industry is likely to see more consolidation. It will be driven by normal credit changes, interest rate changes, and technological improvements such as artificial intelligence, the blockchain and machine learning.

In a study, Deloitte reported that the financial industry is ready for a shakeout and over the next five years, blockchain technology, collaborative ecosystems and cryptocurrencies will become ubiquitous.

For marketplace lending specifically, Deloitte predicts that big banks will start to acquire these lenders or partner with them.

“First, a few marketplace lenders with scale will survive, acquiring smaller rivals and securing joint ventures with big banks and partnerships with small banks; second, big banks will acquire marketplace lenders and other technology/data ecosystem players, replacing or strengthening many aspects of their banking operations; and third, some MPLs will choose to provide white-label services to banks,” said Deloitte in the report.

It also predicts machines to take over most processes of the security trade cycle. But however it added that the role of “human insight will become even more important in serving clients.”

“Bitcoin Lending As a Concept Has Problems”

March 4, 2016 As the trillion dollar alternative lending market expands, it is bringing into its fold newfangled and unproven investing practices like bitcoin lending. While bitcoin lending upstarts like LoanBase, BTCJam, Bitbond woo investors with attractive returns and push its cause for a diversified portfolio, researcher Brett Scott who studies economic systems is less convinced that bitcoin as an alternative currency will save the day. In his paper for the United Nations, Scott argues that it will still be a while until it brings about actual change in terms of financial inclusion and development.

As the trillion dollar alternative lending market expands, it is bringing into its fold newfangled and unproven investing practices like bitcoin lending. While bitcoin lending upstarts like LoanBase, BTCJam, Bitbond woo investors with attractive returns and push its cause for a diversified portfolio, researcher Brett Scott who studies economic systems is less convinced that bitcoin as an alternative currency will save the day. In his paper for the United Nations, Scott argues that it will still be a while until it brings about actual change in terms of financial inclusion and development.

deBanked spoke to Scott about bitcoin lending and its deficiencies as a loan product. Here are the excerpts from the email interview.

On Bitcoin lending

Bitcoin lending could be very positive in principle but in practice, though, the concept still has many problems. Firstly, Bitcoin is not anchored into any national economy. A currency like the Pound is legal tender in a particular geographical area and is widely accepted by everyone within that geographical area. Indeed, if a person in Britain wants to take part in the economy they pretty much have to use the Pound, and if they don’t they will face exclusion. Bitcoin is not like this. It might be accepted but it is not required to be accepted, and a person who doesn’t accept it doesn’t face exclusion from the economy. Thus, while I can buy certain types of goods with Bitcoin – like Pizza at the Pembury Tavern in London – it is not guaranteed to command goods and services anywhere.

On Bitcoin for business needs

This is a problem if you’re borrowing Bitcoin to start a business. If you’re borrowing money, you ideally want the money to be useful for buying a wide range of goods and services that will then enable you to start the business, and you then use your business to earn money with which to pay the loan back. If I get a Bitcoin loan, I’m probably going to struggle to use it to buy all the things I need to start a business – can I buy a computer, for example, or a scooter for delivering goods?

On unstable purchasing power

Also, Bitcoin is unstable in its purchasing power. If you are borrowing money, you want to have some degree of certainty as to what amount of goods and services that money will be able to purchase. I don’t want to get the loan thinking it will be enough to cover three months of business operations, and then discover than it can only cover two months of operations.

On Bitcoin and currency conversion

While businesses might borrow in Bitcoin, it will normally be earning income in a normal national currency. This poses a currency conversion risk in which your assets produce income that is in a different currency to the one required to pay off your liabilities. One response to this is just to accept the risk that the value of the currency your income is in doesn’t depreciate relative to Bitcoin. This basically means that you’re doing currency trading in addition to trying to focus on your core business though. Your business success really should be based on how well you run your operations, rather than how lucky you are about changes in currency values.

Big corporations that operate in multiple countries using multiple currencies deal with this by entering into currency derivative contracts with big investment banks, in which they hedge their currency risk, but right now there is not a well-developed market in Bitcoin currency derivatives. This doesn’t mean such a market won’t develop, but it will take some time still.

One alternative to this is to structure the Bitcoin loan in such a way that it is tied or pegged to a national currency, such that the amount of Bitcoin you have to pay back adjusts depending on how the value of Bitcoin changes. You’re going to have to convince the person that is giving the loan that this is a good arrangement though.

On pegging bitcoin to another currency

Both the lender and the borrower might think of the Bitcoin system as more of payments system instead of a currency in itself. Thus, someone in Britain might want to lend £10 000 to someone in India, so they take £10 000 and use it to buy Bitcoin on a Bitcoin exchange, then they send that Bitcoin to the person in India, who immediately sells it on an exchange for 945000 Rupees.

Furthermore, the person who is lending prices the loan in Pounds rather than Bitcoin. What has essentially happened here is that the loan is really in Pounds but the Bitcoin system was used as a way to transfer it into Rupees, rather than using the normal bank payments system to do that. Then, when the person wants to send interest payments back, they use Rupees to buy Bitcoin and send the Bitcoin to the UK person, who immediately uses it to buy Pounds. It’s possible that this – somewhat elaborate – process might end up being cheaper than using the normal international payments system, but you’d need to investigate that further.

Here’s Why Small Businesses Like Small Banks

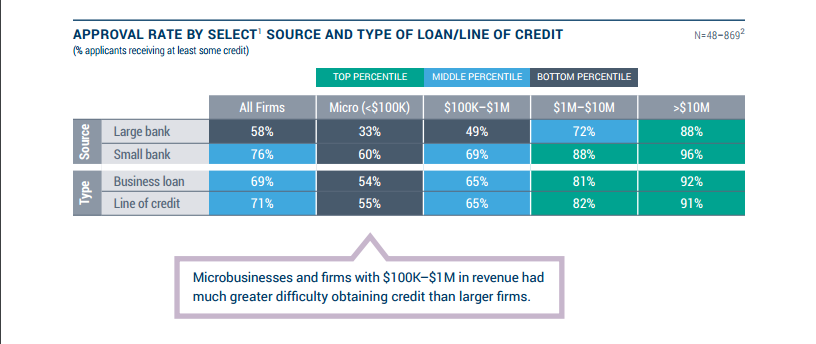

March 3, 2016Small businesses like small banks.

The Small Business Credit Survey released by the Federal Reserve revealed that small businesses like doing business with smaller banks mostly with rate of approval and customer satisfaction.

Small banks approved at least some of the amount requested for 76 percent of applicants, while large banks approved 58 percent of the applicants. And when it came to customer relations, small banks scored a satisfaction score (percent of firms satisfied with the experience) of 75 while the big banks earned a score of 51.

And while banks still dominate as an advisory and credit channel, the survey suggested that 30 percent of microbusiness applicants and 22 percent of small firms ($100K–$1M in annual revenues) applied to an online lender, presumably because these applicants consider online lenders to be as credible as the big banks and despite the lower interest rates, the loan difficulty process and the wait for approval has the small businesses seek alternatives to the traditional bank credit system.

Bizfi Woos Restaurants With Lending Products

March 3, 2016The New York State Restaurant Association signed Bizfi to provide business financing for its 2,000 members.

The New York-based financial platform will be the designated funder of equipment financing, invoice financing, lines of credit, medium term financing, short-term financing, franchise financing and long-term loans from more than 45 partners.

“Restaurants have unique funding needs and owners often do not have time to spare in order to complete the long application process at traditional lenders,” said Stephen Sheinbaum, founder of Bizfi.

Bizfi’s lending partners include all the major lenders in the industry including OnDeck, Funding Circle, Kabbage, IMCA Capital, Bluevine, and SmartBiz and the company has funded over $1.4 to over 27,000 small businesses since 2005.

![]()

Prosper Hires New CFO Amid Rate Hikes, Downgrade

March 2, 2016Online lender Prosper Marketplace has hired David Kimball as its chief financial officer.

Kimball joins the San-Francisco based lender from USAA where he was a senior financial officer in charge of capital markets, treasury and accounting.

“Marketplace lending is an industry that I have watched with interest for some time, and I’m thrilled to be returning to the west coast to join Prosper Marketplace,” said David Kimball.

The company recently raised interest rates among what it called a “turbulent market environment” by an average of 1.4 points to 14.9 percent. Separately, Moody’s downgraded three bonds backed by Prosper citing concerns over slow repayment and loss projections.

Avant Crosses $3 Billion in Personal Loans

March 2, 2016 The naysayers of automated underwriting will have to be silenced again.

The naysayers of automated underwriting will have to be silenced again.

Chicago-based marketplace lender Avant, which uses big data and machine learning to underwrite loans announced that it has beat its online rivals as the first lender to cross $3 billion in personal loans in three years.

The four year old company has 440,000 customers and has issued 480,000 loans so far. It goes after the middle class consumers who take personal loans for an average of $8,000.

“This is a huge accomplishment and speaks to the market demand for affordable and accessible personal loans,” said CEO, Al Goldstein.

Much of its success came from the beefed up presence in the UK, a world leader in P2P lending — where the average loan size is 72 percent higher than the US on a per capita basis. The company hired key executives from MasterCard and HSBC after closing a Series E round from General Atlantic for $325 million last year. With that, it has so far raised $1.7 billion in total.