Articles by deBanked Staff

Shopify Launches Merchant Cash Advance Program

April 27, 2016

Shopify (NYSE:SHOP), the online storefront software company that went public a year ago, announced today that it has formally launched a merchant cash advance product.

“For many merchants, securing capital is a frustrating and time-consuming process,” said Saad Atieque, Product Manager at Shopify. “With Shopify Capital, we’re giving entrepreneurs a simple, fast, and convenient way to secure financing to invest in their business. Similar to our payments and shipping solutions, Shopify Capital represents one more way Shopify can help entrepreneurs strengthen their business operations.”

The company’s release referred to it specifically as a merchant cash advance. “During the pilot program, merchants used Shopify Capital merchant cash advances to buy equipment and inventory, launch new products, hire more employees, and add new channels and products.”

Although Shopify is headquartered in Canada, the program will initially only be available to small businesses in the US.

The company closed yesterday at $31.47, nearly twice its $17 initial public offering.

Shark Tank’s Kevin O’Leary Has a Man-to-Man Talk About Alternative Lending

April 26, 2016Yes, it’s an IOU Financial commercial, but given Kevin O’Leary’s business celebrity persona, roles on Shark Tank and Dragons’ Den, authored books, and regular contributions on CNBC, he’s certainly qualified to sympathize with small business owners on the difficulties of obtaining a loan.

Kevin O’Leary is not the only shark to support alternative lenders. His co-hosts have served as spokespeople for IOU’s competitors:

- Barbara Corcoran – OnDeck

- Lori Greiner – Kabbage

- Kevin Harrington – Ventury Capital (actually as a co-founder of this company)

And don’t forget of course the merchant cash advance guys who actually were contestants on Shark Tank themselves:

Lending Club Looks to Do First Major Securitization Deal

April 26, 2016

As marketplace lenders look to reduce their dependence on traditional capital sources, Lending Club appears to be ready to finally give in and do a securitization.

Lending Club is reportedly in talks with Goldman Sachs and Jefferies Group to put together its first big bond offering, according to the WSJ. The news is significant because the company has previously shunned them.

Earlier this year, Lending Club CEO Renaud Laplanche told the Financial Times, “We are showing that we can scale without the securitization market.” That was after saying they weren’t “willing to take more risk to do a securitization than we would through the normal operation of the platform.”

Since then, the market and the mood has changed. Citigroup for example, announced that they would stop securitizing loans for Lending Club rival Prosper Marketplace only two weeks ago due to looming fears of increasing losses. Prosper is also reported to be talking to Goldman Sachs about future securitizations.

Alternative Small Business Financing Company Secures $70 Million

April 22, 2016Brean Capital has successfully helped an alternative small business financing company secure $70 million. While the name was purposely undisclosed, sources say it was a Delaware-based company.

According to the announcement, “the financing round consists of a $50 million senior credit facility provided by a multi-billion dollar credit fund, and a $20 million equity investment from a middle-market private equity sponsor.” Proceeds from the transaction will be used by the Company to execute its strategic growth plan.

Brean Capital served as exclusive financial advisor to the Company.

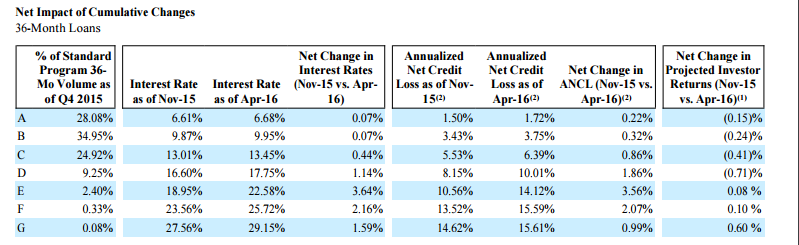

Signs of Slowdown? Lending Club Increases Rates, Adjusts Forecast

April 21, 2016 Should online lenders prepare for a downturn already? Lending Club has a cue.

Should online lenders prepare for a downturn already? Lending Club has a cue.

In a SEC filing on Thursday (April 21) the marketplace lender notified the bureau that it will increase interest rates by 23 basis points and also updated its loss projections.

The hike in rates were concentrated in Grades D – G, identified by the company as underperforming pockets of loans representing 5 percent of the loan volume.

“The population eliminated from the credit policy was mainly characterized by high indebtedness, an increased propensity to accumulate debt and lower credit scores,” the filing said.

The rate hike comes as online lenders look to securitize debt and continue to pursue permanent sources of capital. The industry’s meteoric rise can be attributed to its lenient lending standards but as competition increases the lenders still look to bring more borrowers into the fold. Publicly listed companies like Lending Club have to walk the tightrope between growth and risk.

“Over the past few months the Lending Club marketplace has made a number of proactive changes to reflect the general evolution of interest rates and prepare for a potential slowdown in the economy,” Lending Club said in its filing.

And as alternative lending companies look to disrupt traditional models of lending, several of them are hiring top banking talent for the task.

Lending Club also announced that it hired former McKinsey chief of digital banking, Sameer Gulati as its chief operating officer and promoted chief marketing officer Scott Sanborn to president.

In their new roles, Gulati will head operations and corporate strategy and Sanborn will oversee the company’s product lines (personal loans, small business and patient and education financing) as well as marketing and product development.

From Small to Big: Why Funding Circle is Building its Intermediary Channel

April 21, 2016 If online lenders want to disrupt banking, they need bankers.

If online lenders want to disrupt banking, they need bankers.

Small business marketplace lender Funding Circle hired an intermediary finance veteran Neil Mullane to expand the company’s reach among small merchants. Mullane comes with eight years of experience in commercial finance at Barclays, where he oversaw business and corporate banking working with small businesses with a £250,000 to £25 million turnover.

The London-based P2P lender has channeled more than $2 billion of loans from individual and institutional investors to businesses in the U.S., U.K. and Europe since 2010 and has said that it remains dedicated to two principles, “marketplace and small business.”

And its gaze is set on Europe. Last year, it acquired German marketplace lender Zencap for an immediate footprint in Germany, Spain and Netherlands. Additionally, its SME Income Fund that was listed on the London Stock Exchange in November 2015, raised £150 million from shareholders and started lending to small businesses in those markets last month.

Last week (April 14), the company also launched UK’s first P2P securitized ABS backed by loans worth £130 million.

Speaking at LendIt USA recently, the company’s US co-founder and managing director Sam Hodges envisioned the golden age for marketplace lending where it takes “seconds to issue credit,” from a broad network of global investors. “A loan should get funded by a network of investors all over the world — be it a pensioner in London, a hedge fund manager in Sydney or a family office in New York simultaneously putting money to work through a global platform,” he said.

He elaborated further to note that the industry will have to work on four key tenets to get there: Stable lending capital, taking controlled risks, maintaining operational discipline to make sure that unit economics favor scaling and lastly, maintaining integrity around infrastructure and transparency.

The company has noted its intention to move in this direction at least with hiring the right talent, whether through the former Executive Board Member of the European Central Bank (ECB), Jörg Asmussen Mullane to lead business development or beefing up its risk compliance and product engineering teams in San Francisco.

AmEx to Launch Small Business Loans on Lendio

April 20, 2016American Express is getting knee deep in small business lending and has chosen to go online.

The bank is partnering with small business loan marketplace Lendio to bring its merchant financing products to small businesses. This marks a step forward for American Express as it wants to look beyond its customer base and turn new merchants into borrowers.

Lendio CEO Brock Blake called the product a hybrid between a merchant cash advance and a bank loan ranging from $5,000 up to $2 million for two years. Merchants with a minimum revenue of $50,000 and two years of operating history can apply for this loan based on cash flow and credit card sales.

“This was a relationship that has been a long time coming,” said Blake. “We are fortunate to have won this deal and this opens the door for many similar relationships.”

In February this year, American Express ended a 16 year relationship with retail giant Costco. That partnership constituted 20 percent of the company’s outstanding loans which it hopes to recover by growing the small business loan revenue. The bank also featured its charge cards on online marketplace, Fundera for merchants to compare its business charge cards with traditional loans. To provide some context, Amex cards for small businesses funded $190 billion in purchases, up from $122 billion in 2010.

And as for Lendio — the company has been bullish about striking big ticket deals. The Salt Lake City-based loan marketplace funded $128 million in financing over 5000 small businesses, clocking in 1175 percent annual growth from the previous year.

SoFi Hedge Fund was Not Created for Capital, says CEO Mike Cagney

April 19, 2016If you were at LendIt then you might nod at this — the echo from the alternative lending industry congregation last week had just three words: Long term capital.

Nearly 3500 industry folks gathered at San Francisco to share woes and celebrate victories.

“The nonbank lending industry is at an inflection point,” said Mike Cagney, CEO of SoFi. Cagney known for his candor warned that for the business to make a leapfrog, companies need to establish more balance sheet partnerships, preferably with banks. A failure to do so would cap the number of originations.

“What banks really like is for the alt lenders to be the infrastructure/origination framework and for them to be the balance sheets. But the problem occurs when they also want to retain the customer, this is going to dictate the direction of the industry because you will get a natural cap and you won’t be able to go more than a billion and half originations a month without having balance sheet partnerships.”

In house capital? Not really

Cagney doesn’t want to give the impression that its newly launched hedge fund came about because it couldn’t sell enough loans. It’s rather to gain more access to retail investors and this he said was a simpler vehicle than participating in equity and securitization.

“We have half a billion dollars going into the hedge fund and that’s a week’s production for us. So that’s not going to solve the funding problem.”

We’re not skirting regulation

“It’s a misconception that our industry exists because of some regulatory arbitrage,” Cagney said reasoning that the industry has to follow the same lending regulations as a bank.

“There are lot of limitations that we have because we are not a bank holding company.”

Who are we? Not Banks. What do we want? National lending licenses

Cagney championed the cause for a national lending license and said that Dodd Frank falls short by limiting the Office of the Comptroller of the Currency (OCC).

“The OCC was the mechanism to get a national lending license without the deposit insurance and the industry needs that back.”