Articles by deBanked Staff

Affirm Partners with Walmart for Payments

February 28, 2019 Walmart customers can now pay for items using credit from Affirm, the online consumer lender announced yesterday. Walmart customers can find out how much they qualify for online and then make online or in-store purchases with in three, six or twelve monthly installments. A credit decision is made in real time and does not affect the customer’s credit score, according to Affirm.

Walmart customers can now pay for items using credit from Affirm, the online consumer lender announced yesterday. Walmart customers can find out how much they qualify for online and then make online or in-store purchases with in three, six or twelve monthly installments. A credit decision is made in real time and does not affect the customer’s credit score, according to Affirm.

“Walmart serves millions and has become a leader in the retail landscape with its commitment to help shoppers ‘save money and live better,’ which closely mirrors our own mission to ‘improve lives’ with our products,” said Max Levchin, founder and CEO at Affirm, as well as a founder of PayPal. “I’m looking forward to introducing Walmart customers to a modern and innovative way to buy the things they need.”

Affirm is now available as a payment option on Walmart purchases ranging from $150 to $2,000. This is not Walmart’s first foray into financing. In fact, in July of last year, Walmart entered into an exclusive partnership with Capital One to issue a Walmart credit card. But Elizabeth Allin, Vice President of Communications at Affirm, said that this partnership is the first point-of-sale loan product partnership for Walmart.

“They’ve really embraced e-commerce and the evolution of digital and mobile,” Allin said of Walmart, which has been the biggest retailer in the world for years.

Now 57 years old, the retail giant is pursuing partnerships with financial organizations to facilitate access to customer credit. But back in 2006, Walmart set its sights on bringing these lending operations in house, by becoming bank. Using a controversial statute, it attempted to get a charter to become an ILC bank. Met with strong opposition from banks and other opponents, Walmart backed down.

Square Capital On Pace to Overtake OnDeck in Small Business Lending

February 28, 2019 OnDeck’s annual loan origination volume has more than doubled since 2014, from $1.2 billion to $2.5 billion, allowing them to retain the top spot in deBanked’s small business funder rankings. But Square Capital, the small business lending division of Square, has grown by 16x since 2014. In the course of 5 years, they’ve gone from being a footnote compared to OnDeck to a fierce rival that is rapidly closing the gap in loan volume.

OnDeck’s annual loan origination volume has more than doubled since 2014, from $1.2 billion to $2.5 billion, allowing them to retain the top spot in deBanked’s small business funder rankings. But Square Capital, the small business lending division of Square, has grown by 16x since 2014. In the course of 5 years, they’ve gone from being a footnote compared to OnDeck to a fierce rival that is rapidly closing the gap in loan volume.

Square’s secret is the ability to generate loan volume at virtually no cost because the product is merely an add-on to their payments-first business. And that’s a problem for OnDeck, because Square has a lot of money to spend on marketing its payments business. More than $400 million a year to be precise. OnDeck, meanwhile, only spent $44 million last year on sales and marketing.

With OnDeck being outspent by a factor of 10, there is a likelihood that Square will overtake OnDeck in the business loan market within the next two years.

And Square’s strength is the ecosystem it’s building. On the Q4 earnings call, company CEO Jack Dorsey said, “I believe the ecosystem is extremely sticky, because it builds durable relationships. If we’re just focused on providing payments in the Register, certainly, there are so many other competitors out there. But when people come in for payments in the Register and then they use [our] payroll for their restaurant and they use Caviar and are really getting offers from Square Capital, it’s really hard to find that mix anywhere else and that builds durability.”

New York Legislators Introduce Small Business Usury Bill

February 20, 2019Two members of the New York State legislature have introduced a bill to apply consumer usury protections to small businesses. Bill A03638, introduced by New York Assemblymembers Yuh-Line Niou and Crystal Peoples-Stokes define a small business as “one which is resident in this state, independently owned and operated, not dominant in its field and employs one hundred or less persons.”

The bill is separate from the one introduced to outlaw Confessions of Judgment in financial contracts.

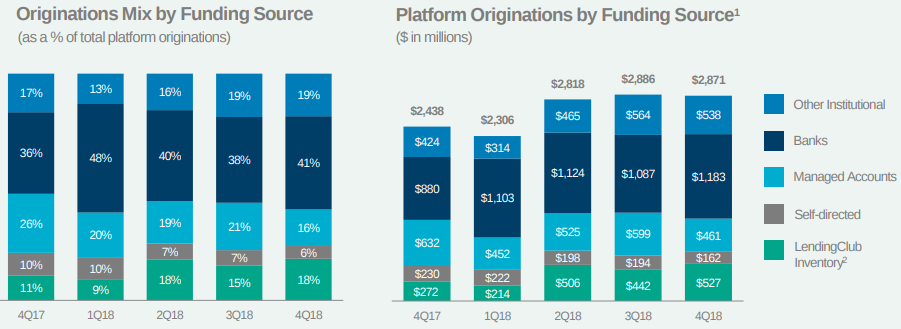

‘Peers’ Are Almost Gone From Lending Club’s Funding Mix

February 20, 2019 Long gone are the days of peer-to-peer lending.

Long gone are the days of peer-to-peer lending.

On Tuesday, Lending Club, a pioneer in the peer-to-peer lending space, reported that only 6% of its Q4 originations came from individual self-managed accounts. Accounts professionally managed for individuals made up 16%, with the rest of the loans being funded by a combination of banks, institutions, and Lending Club itself.

Nearly 4 years ago, the ratio was flipped. Self-managed accounts made up 24% of originations in early 2015 and accounts professionally managed for individuals made up 51%.

Despite the changes, Lending Club still identified itself as a “marketplace connecting borrowers and investors” in its Q4 2018 earnings report. A review of the site revealed that it is still possible for individual investors to manually review unfunded loans on the platform and invest in them, though it prods investors to rely on Lending Club’s automated investing strategy instead. The implication for manual investors is obvious, that banks, institutions, automated investment algorithms, and Lending Club itself are more likely to fully fund the best borrowers before the individual has a chance to even see them on the platform.

According to the blog of LendItFintech co-founder Peter Renton, Lending Club is producing among the lowest returns of any platform in the field, with his own accounts generating from 1.57% a year to 4.35% a year.

1 Global Capital Issued Securities, Court Rules

February 17, 2019 1 Global Capital founder Carl Ruderman suffered a major setback in his case with the SEC earlier this month, when the Court ruled that his company’s Syndication Partner Agreements and Memorandums of Indebtedness were in fact, securities. Ruderman had filed a motion to dismiss the SEC’s claims against him personally but the Court struck it down.

1 Global Capital founder Carl Ruderman suffered a major setback in his case with the SEC earlier this month, when the Court ruled that his company’s Syndication Partner Agreements and Memorandums of Indebtedness were in fact, securities. Ruderman had filed a motion to dismiss the SEC’s claims against him personally but the Court struck it down.

1 Global sold its notes to more than 3,400 investors in at least 25 states, who collectively invested at least $287 million. The company declared bankruptcy last year amid parallel criminal and civil investigations that hampered its ability to raise capital. The SEC filed suit soon after but no criminal charges have been brought to date.

In the ensuing legal discovery, it was revealed that the company funded the largest merchant cash advance in history, a collective $40 million funded over several transactions to an auto dealership group in California. Those dealerships closed not longer after 1 Global Capital’s bankruptcy. Those closures have sparked a lawsuit of its own and with it the revelation that several of 1 Global Capital’s competitors had also funneled millions into the dealerships.

The Court’s ruling in the motion to dismiss whereby the investments were deemed securities can be downloaded here.

Commonbond Receives Financing From Major Banks

February 14, 2019 Commonbond announced today that it has signed $750 million in lending capacity from Goldman Sachs, Citibank, Barclays, BMO, and ING.

Commonbond announced today that it has signed $750 million in lending capacity from Goldman Sachs, Citibank, Barclays, BMO, and ING.

“From the start, we have set out to build the highest levels of trust with our customers and our capital partners,” said CommonBond CEO and co-founder David Klein. “Access to this level of capital, and at a lower cost, is a testament to the platform we’ve built, the quality of our members, and the success of our capital markets program. We’re thrilled to have some of the world’s top banks recognize [this], and work with us in a way that ultimately benefits the consumer.”

This new financing will support growth for Commonbond, which provides student loans and student loan refinancing. According to a company statement today, in addition to growth, the new lending capacity reflects significantly lower cost of capital for CommonBond, improving the company’s borrowing spreads and advance rates.

This financing comes a little less than a month after Reuters reported that Commonbond laid off 18% of its staff, which affected 22 people. Based in New York and founded in 2013, Commonbond has originated over $2.5 billion in loans.

Shopify is Quickly Climbing the Ranks of the Largest Small Business Funders

February 12, 2019Shopify originated $277 million in merchant cash advances in 2018, according to their quarterly earnings reports. That figure already places them among the largest small business funding providers nationwide.

Below is a look of how they stack up thus far:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate

With Interest Rates Up, OnDeck’s Cost of Funds Comes Way Down

February 12, 2019 OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

During the earnings call, OnDeck CEO Noah Breslow said, “We improved the terms and structures of our credit facilities and increased the number and quality of our funding providers, adding new banks and life insurance companies.”

That’s all before OnDeck even closed on an $85 million revolving credit facility with a lender group consisting of four banks earlier this month. The rate on that came in at 1 month LIBOR (currently around 2.5%) + 3.00%.

OnDeck’s loan yield in Q4 was the highest its been in the last 2 years at 36.6%.

The company enjoyed record earnings for Q4 2018 ($14 million) and full year 2018 ($27.7 million). They also had record origination volume of $658 million, a 2% increase from Q3 and a 21% increase from Q4 2017. Their sales and marketing expense for acquiring new customers remained flat compared to last quarter.