Brendan Garrett was a Reporter at deBanked.

Articles by Brendan Garrett

CAN Capital Brings On Edward Dietz as Chief Compliance Officer & General Counsel

February 5, 2020 CAN Capital is continuing its executive hiring spree into 2020 with the news that it has brought on Edward Dietz as its latest Chief Compliance Officer and General Counsel. After providing legal expertise to Marlin Business Services Corporation for nine years and working as an associate for two law firms in Wisconsin and Pennsylvania previous to this, Dietz will oversee CAN’s compliance with all federal and state lending, banking, and securities laws.

CAN Capital is continuing its executive hiring spree into 2020 with the news that it has brought on Edward Dietz as its latest Chief Compliance Officer and General Counsel. After providing legal expertise to Marlin Business Services Corporation for nine years and working as an associate for two law firms in Wisconsin and Pennsylvania previous to this, Dietz will oversee CAN’s compliance with all federal and state lending, banking, and securities laws.

“Having worked with Ed and knowing his skill set and the many intangibles that he brings to CAN, I feel fortunate that he’s leading our legal and compliance efforts,” noted CEO Edward Siciliano in a statement. “Ed’s just what we needed as we position CAN for growth and to lead a new era of small business lending.”

Having graduated from the University of Michigan Law School in 2004, Dietz has nearly two decades of legal experience.

Speaking on the news, Dietz said that he “could not be more excited to join a company and a team that believes so deeply that its people and its culture are the keys to harnessing the company’s growth potential.”

Kabbage Introduces Customized Short Term Loans

February 4, 2020 Today Kabbage, the Atlanta-based fintech company that has been funding businesses since 2009, announced its latest product: customized short-term loans that are a result of the combination of Kabbage Payments and Kabbage Funding.

Today Kabbage, the Atlanta-based fintech company that has been funding businesses since 2009, announced its latest product: customized short-term loans that are a result of the combination of Kabbage Payments and Kabbage Funding.

The loans, which run for the length of 3-45 days, are best suited to those businesses who need funding to cover issues in cash flow caused by the unpredictability of revenue, says Kabbage’s Head of Income Products Abraham Williams. “Rent and payroll are on set days every month, but getting paid is variable. We’ve done loans for 6, 12, and 18 months, and we’ve seen that people pay those off sooner, so we saw a need to have a short-term loan to fill gaps in cash flow.”

The terms of such loans will be decided upon by making use of the aggregate data that Kabbage has access to. With its customers providing a number of data points, such as their Amazon account, banking details, payment processes, and social media accounts, Kabbage is in “a really unique position because of the way that we make decisions on loans for small businesses,” notes Williams. “We can really see a very complete picture of a business, which can be different than how other people are essentially underwriting and assessing risk for loans.”

Two options are available for repayment: a traditional balloon payment to be paid at the end of the 45-day period, or a percentage of each sale made using Kabbage Payments going towards repayment. The latter of these provides more flexibility, with merchants being able to choose the percentage of each sale that is to go toward Kabbage and, as well as this, the fee attached to the Kabbage Payments option is smaller.

With the fee’s amount and terms being dictated by aggregated data, Kabbage is describing them as “dynamic,” providing individualized offers. Fees begin at 0.1% with the minimum amount to be borrowed being $500 and the maximum set at 10% of a merchant’s available line of credit for the short-term.

Goldman Sachs-Amazon Deal to Offer Small Business Loans in the Works

February 3, 2020

Tech giant Amazon is reportedly in talks with Goldman Sachs to offer business loans to those small and medium sized merchants operating on its marketplace, according to sources that the FT describes as “two people briefed on the discussions with the online retailer.” One of these sources said that it could launch as soon as March.

The news comes after CEO David Soloman spoke at the bank’s Investor Day recently, explaining that Goldman would be pursuing a “banking-as-a-service” model this year that would see the bank white labeling their products for third parties to use. As well as this, Solomon commented on a shareholders call last week that the bank is seeking to increase revenues from new channels such as consumer banking and wealth management.

One such channel is Goldman’s partnership with Apple last summer that saw the launch of Apple Card, a credit card solely available to Apple’s +100 million users in the US. The card’s launch was lauded by Solomon; and according to Business Insider, cardholders had $736 million in loan balances by the end of September, one month after the card was released to the public.

The Apple and Amazon deals highlight how Wall Street banks are employing and partnering with Big Tech to leverage advantage over fintechs, and ultimately gain access into markets that are historically not domains of the uber rich. Traditionally a bank that catered to elites, Goldman Sachs has been edging its way into consumer and small business banking ever since the launch of Marcus, its personal banking platform.

Amazon has been offering loans to merchants on its platform since 2011, using algorithms to determine which sellers would be best positioned to receive and repay a loan. Having previously partnered with Bank of America to finance such loans, the terms of these were for 12 months or less, with amounts funded ranging from $1,000 to $750,000. According to the FT, Amazon had $863 million in outstanding SMB loans on its balance sheet as of the end of 2019.

The digital nature of Amazon’s marketplace would accommodate Goldman Sachs’ neglect of brick-and-mortars stores, which have historically been a waypoint for small- and medium-sized businesses seeking finance.

LendIt Chairman and Co-founder Peter Renton described Goldman’s progression in the fintech space as “impressive,” noting that the speed at which it has been operating isn’t to be overlooked: “I thought something like this would happen but not in such a short space of time. Apple Card was only six months ago.”

As well as this, Renton was wary of how expansive the deal would be, admitting skepticism of it being a large project for either company. Given how both Amazon and Goldman have shown themselves to be selective in who they provide financing for, this assessment may prove correct.

Liberis Secures $42 Million in Funding, Plans American Expansion

February 3, 2020 Liberis, the London-based small business finance provider, secured £32 million ($42 million) in capital late last month following a round of equity fundraising. The firm, which has funded businesses through cash advances since 2007, has now raised a total of over £150 million ($197 million) via debt and equity.

Liberis, the London-based small business finance provider, secured £32 million ($42 million) in capital late last month following a round of equity fundraising. The firm, which has funded businesses through cash advances since 2007, has now raised a total of over £150 million ($197 million) via debt and equity.

Having already entered Nordic markets, Liberis looks to use this funding to further expand into Europe as well as make their mark in America. Speaking to deBanked, Liberis CEO Rob Straathof explained that the company would be working with its North American partner, Worldpay, to spread itself across all 50 states. Beyond Worldpay, Liberis is planning to create more partnerships with merchant acquirers, those payment platforms which serve merchants, or “SME champions,” as Straathof calls them.

Liberis will not be using brokers to provide cash advances to business owners in the States, the reason being that the company prefers to work with its affiliated partners. “We purely rely on our partners and integrating with our partners,” explained Straathof. “In the UK we still do brokers, but that’s kind of a legacy. It works very well for us and we have a great relationship with brokers. It’s a good channel for us, but we have no intention at this point to launch that in the US.”

The company will also use the funding to increase its staff by 30% in 2020, hiring around 50 people to bolster its 165-person workforce across their four offices in London, Dublin, Stockholm, and Denver.

Former Wells Fargo CEO Fined $17.5 Million

January 27, 2020 Last week the Office of the Comptroller of the Currency released a 100-page report on the Wells Fargo fake accounts scandal that came to light three years ago. Accompanying the document with a fine against the CEO who oversaw the controversy, John Stumpf, for $17.5 million.

Last week the Office of the Comptroller of the Currency released a 100-page report on the Wells Fargo fake accounts scandal that came to light three years ago. Accompanying the document with a fine against the CEO who oversaw the controversy, John Stumpf, for $17.5 million.

Stumpf, whose personal wealth was estimated to be roughly $200 million prior to the scandal, also had all of his stock options rescinded by Wells Fargo, totaling $69 million that was returned to the bank.

Being the largest ever fine to be levied against an individual by the OCC, the news contrasts regulators’ reactions to previous outrages, such as JPMorgan Chase’s London Whale fiasco as well as the ’08 financial crisis, both of which saw executives escape personal scrutiny in lieu of the institutions themselves being subject to penalties. And while Stumpf’s fine breaks records, it may not hold the top spot for long, with the OCC eyeing a follow-up charge against Carrie Tolstedt, who ran the division of Wells Fargo most involved in the scandal, for $25 million.

Stumpf was charged alongside seven others who were implicated in 2016 for opening millions of allegedly fake accounts to meet sales targets. Such goals being set by higher-ups in the 168-years-old bank were passed down to mid- and low-level employees, fostering a culture that promoted the idea of cheating or being fired, according to the OCC’s report.

Employee testimonies allege that one branch manager threatened to transfer those workers who did not meet targets to “a store where someone had been shot and killed,” whereas another employee and Gulf War veteran wrote to Stumpf noting that working for Wells Fargo proved to be more stressful than a war zone.

The filings also described an atmosphere of surveillance, mentioning that “The bank had better tools and systems to detect employees who did not meet unreasonable sales goals than it did to catch employees who engaged in sales practices misconduct.”

Reactions to the scandal have been scathing, with Congress having drilled Stumpf’s replacement, Tim Sloan, during hearings last year. Democratic presidential nominee candidate Elizabeth Warren came out during the week with guns blazing for the bank. “Giant banks like Wells Fargo only clean up their act when their executives know they’ll face handcuffs when they preside over massive fraud,” the Massachusetts Senator said in a statement on Thursday. “Tomorrow morning, former Wells Fargo CEO John Stumpf will wake up to his cushy retirement while the thousands of low-level branch employees who took the fall for him – and the hundreds of thousands of consumers who were cheated on his watch – continue to deal with the repercussions of his scams.”

Sloan ended up taking a forced retirement in March 2019, with Charles Scharf stepping in as CEO. Speaking on his first earnings call since assuming leadership of the bank, Scharf addressed the scandal, keeping the book open on investigations into wrongdoing. “I just want to be clear, I’m not suggesting here that any of these public issues will be closed this year.”

The Scoop Behind Sprout Funding’s Acquisition of Jet Capital

January 25, 2020 News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

“Sprout built a reputation as a group that funds a lot of its own internal deals, and Jet had spent a lot of time, energy, and money on their tech platforms,” Sprout’s CEO and Founder Brad Woy told deBanked. “So while we were really good on the sales and marketing side, they seemed to be a little bit more advanced in their tech and reporting, and we brought those two things together.”

Almost all of Jet’s employees will be joining Sprout, with the exception of one person who chose to go their separate way following the merger.

Jet’s COO Allan Thompson spoke kindly of the purchase, saying in a statement that “There is a great cultural alignment in addition to the obvious benefits of combining our technology, processes and people. The result will provide increased capabilities for Sprout and opportunity for all of our customers and partners.”

The financial terms of the acquisition were not disclosed.

Sun Shines on deBanked CONNECT MIAMI for Another Year

January 24, 2020 Two blocks back from where the waves were washing up on Miami Beach, attendees flocked into the halls of the Loews Miami Beach Hotel. A mix of brokers, funders, lawyers, and anyone else attracted to alternative finance made up the crowd of the 2020 outing of deBanked Connect Miami.

Two blocks back from where the waves were washing up on Miami Beach, attendees flocked into the halls of the Loews Miami Beach Hotel. A mix of brokers, funders, lawyers, and anyone else attracted to alternative finance made up the crowd of the 2020 outing of deBanked Connect Miami.

They had come for the speakers and talks, the networking opportunities, and, of course, the weather; the first of these being a mix of topics and characters from across the industry. But before the talks could properly kick off, deBanked’s President and Founder Sean Murray took to the stage to welcome attendees and announced the publication’s latest news: the utility of www.seekingfin.com and the administration of two large social media groups, Merchant Cash Advance on Facebook and Merchant Cash Advance Resource on LinkedIn.

Following on from Murray’s introduction, Brian Holloway, former Patriots Offensive Lineman, opened the show with an impassioned speech alongside his son on how to translate your passions and determination into sales maximization, citing the mantra of “Let’s move as the champions move.” A collection of industry figures including United Capital Source’s Jared Weitz, Elevate’s Heather Francis, and alternative finance veteran David Goldin discussed the challenges and changes that businesses are likely to face when making money in 2020 – including what to be aware of when considering syndication and how to build a book. And closing the show were Gunes Kulaligil from Methodical Management alongside Hans Thomas of 10X Capital, who broke down how to accurately value yourself and your company’s worth.

Following on from Murray’s introduction, Brian Holloway, former Patriots Offensive Lineman, opened the show with an impassioned speech alongside his son on how to translate your passions and determination into sales maximization, citing the mantra of “Let’s move as the champions move.” A collection of industry figures including United Capital Source’s Jared Weitz, Elevate’s Heather Francis, and alternative finance veteran David Goldin discussed the challenges and changes that businesses are likely to face when making money in 2020 – including what to be aware of when considering syndication and how to build a book. And closing the show were Gunes Kulaligil from Methodical Management alongside Hans Thomas of 10X Capital, who broke down how to accurately value yourself and your company’s worth.

Running throughout these talks, just off from the general session room, the sponsors hall was abuzz with deals and networking. With business cards exchanged, rumors swapped, and trends discussed, the hall served for the day as a focal point for the industry.

And as the sun set on South Beach, the speakers wrapped up and the sponsors wound down their tables. The audience billowed out into the courtyard, where the lasting Miami heat accompanied food, cocktails, and conversation, as deBanked Connect Miami closed for another year.

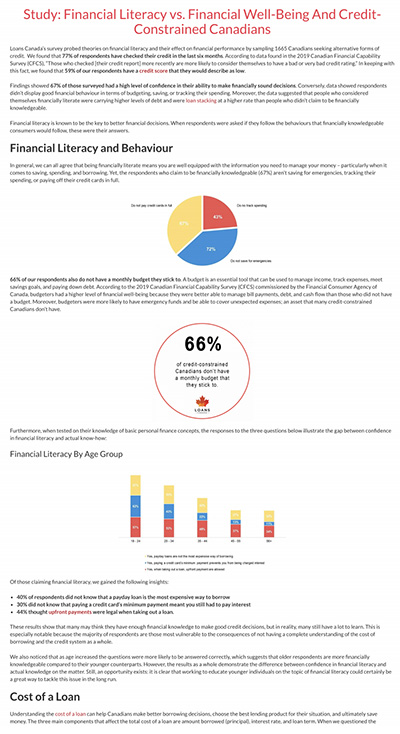

Study Claims Canadian Market Needs to Improve Financial Literacy

January 24, 2020 This week Loans Canada, a lead generation company, released a study documenting the disparities between perceived financial literacy and actual financial well-being. Surveying 1,665 Canadians, the report asserts that those individuals who claim to have a firm grasp of their financial situation may in fact be out of touch.

This week Loans Canada, a lead generation company, released a study documenting the disparities between perceived financial literacy and actual financial well-being. Surveying 1,665 Canadians, the report asserts that those individuals who claim to have a firm grasp of their financial situation may in fact be out of touch.

This being highlighted by major misunderstandings about how to budget for the future as well as a lack of education regarding loan repayments. 72% of the respondents said that they did not save for emergencies, 43% did not track their spending, and 66% do not stick to a monthly budget. Such budgetary omissions outline the potential for a large portion of the Canadian market to be in trouble should unforeseen expenses arise, and the fact that two thirds of the market aren’t even drawing up budgets is a cause for concern.

Such factors are made worse by the community’s seeming misinterpretations of loan terms. With 40% of the survey stating that they didn’t know payday loans were one of the most expensive ways to borrow money, 30% not understanding that paying the minimum amount of a credit card charge still meant you had to pay interest, and just over half of those surveyed were not able to identify the factors which affect the cost of loans, there appears to be a problem surrounding financial literacy and education of individuals regarding loans.

As well as these issues, there is the case of stacking loans, with the study indicating that the practice is not fully understood by Canadians and that the two top reasons for taking on multiple loans are for emergency costs (25%) and making ends meet (43%). Interestingly, the respondents who claimed to have the most confidence in their capacity to make financially sound decisions are more likely to be individuals who stack loans, leading them, inevitably, to have similar or more debt than those surveyed who said they were not confident in their financial decision-making ability.

Altogether, the study paints the picture of Canada as a market in need of further education. While financial literacy isn’t in crisis, the report points towards vulnerable sectors, such as such as those individuals with poor knowledge of loans and interest rates, as well as budgeting, are groups that need to develop a better understanding.