Brendan Garrett was a Reporter at deBanked.

Articles by Brendan Garrett

Robinhood Goes Down Three Times in One Week, And The Timing Couldn’t Be Worse

March 10, 2020 The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

Robinhood’s first outage was on Monday, March 2. Lasting only a few minutes, the loss of service coincided with the biggest one-day point gain of the Dow in history. The second came the next day, lasting two hours after the Federal Reserve announced a cut of 0.5% to interest rates.

The Sarasota-based tech giant’s co-CEOs released a statement that Tuesday on the company’s blog placing blame for the outages on their overstressed infrastructure. They claimed that their servers struggled with an “unprecedented load” that led to a “‘thundering herd’ effect—triggering a failure of our DNS system.”

The company has yet to release a statement explaining the third service blackout today, which took place during a period that saw the stock exchange pause trading for 15 minutes to prevent a freefall.

In response, Robinhood customers are threatening legal action. Numerous Twitter accounts have popped up under the name ‘Robinhood Class Action,’ or as some variation of this, with the largest of these having over 7,500 followers at the time this article was published. Travis Taaffe of Florida filed a federal lawsuit on Wednesday on behalf of himself and other traders, claiming that Robinhood was negligent and in breach of contract by failing to “provide a functioning platform” for traders, rendering them unable to move stocks.

Having 10 million customers, the company could be facing a lot of claims. As of last week, Robinhood has been offering its Gold members three months of the subscription for free. The price of this would amount to $15 dollars altogether; and the second cost of the subscription, 5% yearly interest on borrowing above $1,000, will not be waived as part of this compensation. Robinhood has described this offer as a “first step.”

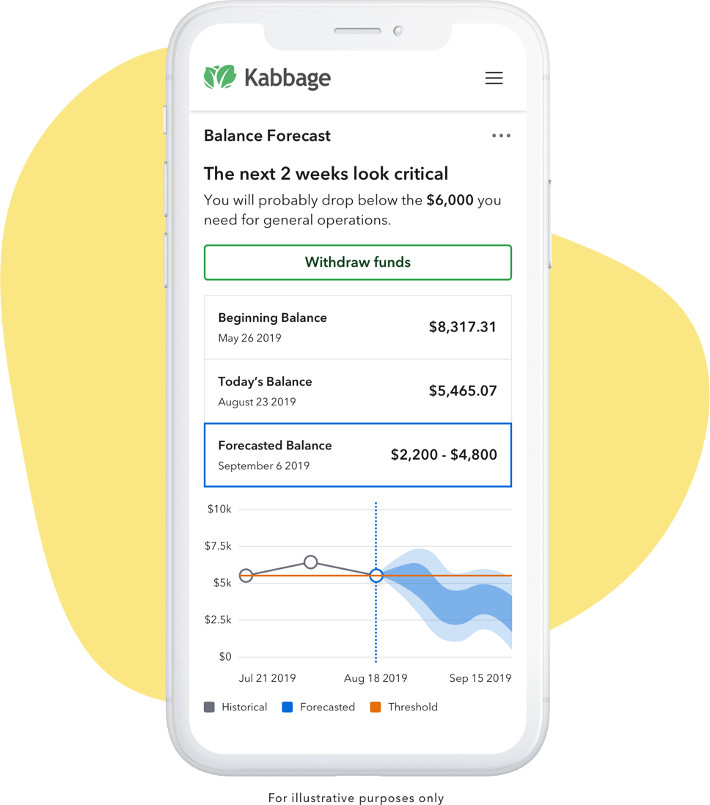

How Kabbage Insights Seeks to Level Playing Field for Small Businesses

March 5, 2020 This week, Kabbage released its latest product, Kabbage Insights, to the public. Having been available privately since February 10th, the service is now free to all Kabbage customers. Released a month after Kabbage Payments, Insights adds to Kabbage’s ecosystem of products by helping small business owners identify and prepare for cash flow deficits.

This week, Kabbage released its latest product, Kabbage Insights, to the public. Having been available privately since February 10th, the service is now free to all Kabbage customers. Released a month after Kabbage Payments, Insights adds to Kabbage’s ecosystem of products by helping small business owners identify and prepare for cash flow deficits.

Acting almost like a virtual assistant, Insights links to and analyzes a business’s financial data, serving up a report of how the company has performed historically, how it’s doing currently, and what the projections for its future are looking like. While this may sound like standard business planning and budgeting, the time and resources required to provide in-depth financial analyses are usually only in possession of larger companies. Insights, according to Kabbage’s Head of Income Products, Abraham Williams, is an attempt to bridge this gap between what larger businesses have traditionally had access to and what small business owners have been unable to claim.

“Kabbage has, for a number of years now, used data science, modeling, and machine learning to come up with financial decisions on whether to give someone a loan, and we’re right a lot of the time.” Williams told deBanked over the phone. “With this, we’re able to bring this modeling to our small business customers.”

As well as providing a breakdown of a company’s financial history and future, Insights offers a threshold alert system wherein customers can set a desired low-balance amount and receive notifications when they are nearing it. And by pairing Insights with Kabbage’s Small Business Revenue Index, users will be able to compare their company against those of a similar size/location, so long as these businesses are Kabbage customers. The data used to make these comparisons will be aggregated and anonymous.

The public launch of Kabbage is part of the company’s plan to create a fintech ecosystem that completely eliminates waiting times, and is the culmination of Kabbage’s ten years of collecting and analyzing small business financial data.

Or, as Kabbage CEO Rob Frohwein said in a statement: “As a small business owner for many years, I spent many sleepless nights trying to figure out whether I’d have the cash to pay my various expenses, including payroll at the end of the month and it’s been a mission of mine to solve this ubiquitous problem for all small business owners ever since. Kabbage is pleased to launch Insights, taking on this burden for small business owners and providing them with cash flow analyses that large enterprises have at their fingertips. We will continue to level the playing field for the small business owner.”

Democrats Call for Interest-Free Loans for Small Businesses Affected by Coronavirus

March 2, 2020 The leaders of the Democratic Party in the Senate and House, Chuck Schumer and Nancy Pelosi, respectively, have released a joint statement outlining their perspective on providing emergency funding to combat the coronavirus, otherwise known as covid-19. Among the provisions listed is a demand that “interest-free loans are made available for small businesses impacted by the outbreak.”

The leaders of the Democratic Party in the Senate and House, Chuck Schumer and Nancy Pelosi, respectively, have released a joint statement outlining their perspective on providing emergency funding to combat the coronavirus, otherwise known as covid-19. Among the provisions listed is a demand that “interest-free loans are made available for small businesses impacted by the outbreak.”

The statement comes at a point when the government has yet to confirm the amount of funds dedicated to treating and preparing against covid-19. Schumer has proposed devoting $8 billion, and House Minority Leader Kevin McCarthy has said that even $2 billion would be too little, opting instead for $4 billion. McCarthy has agreed with the Democrat leaders, saying that emergency funds should be not be stolen or transferred from other funds or emergency allotments. This position goes up against President Trump’s request for $1.25 billion from various existing funds, including $535 million from the Ebola preparedness fund.

Republican Senator Tom Cole expressed his uncertainty regarding the request, saying that “I just don’t think we should be penny-wise and pound-foolish on that.”

As well as calling for interest-free loans, the statement requests assurances that Trump will use the funds purely to fight covid-19 and other infectious diseases, that eventual vaccines will be available and affordable for all, and that state and local authorities will be reimbursed for costs incurred while assisting the federal response.

It is unsure whether or not these loans will actually come into play. While there does appear to be bipartisan cooperation within the House and Senate, the government seems to only have begun taking the virus seriously this week after it spread from China to Iran and Italy, and the first infection from an unknown source in America was diagnosed in California.

“We’re coming close to a bipartisan agreement in the Congress as to how we can go forward with a number that is a good start,” Pelosi told reporters in her weekly press conference. “We don’t know how much we will need. Hopefully, not so much more because prevention will work. But nonetheless, we have to be ready to do what we need to do.”

Lendio Plans Development and Growth With $55 Million Series E

February 27, 2020 Today Lendio announced that it raised $55 million as part of its series E funding round. This included $31 million in equity led by Mercato Partners Traverse Fund and a $24 million debt facility from Signature Bank.

Today Lendio announced that it raised $55 million as part of its series E funding round. This included $31 million in equity led by Mercato Partners Traverse Fund and a $24 million debt facility from Signature Bank.

“We think that we’re just getting started, that there’s a really large opportunity in front of us and we’re excited that this round will give us the fuel that we need to continue to grow,” Lendio CEO Brock Blake told deBanked in a call. “We have a few different reasons for pulling together the round, but primarily, it’s all around investing in organic growth through partnerships and different marketing channels.”

Asked where these funding rounds may continue in an F, G, and H, Blake was unsure, saying that “every time we raise a round we do it with the expectation that it will be the last round.”

The funds in part will be used to further develop Lendio’s integrated lenders services, which are a set of tools used to identify which loan product and lender are the best match for a business owner; as well as the expansion of Sunrise, the bookkeeping platform Lendio acquired in 2019.

Intuit Agrees to Buy Credit Karma For $7.1 Billion

February 26, 2020 This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

Under the deal, Credit Karma will continue to operate as a stand-alone business and its CEO, Kenneth Lin, will stay on and run the company. Beyond that, some believe that the merger will see Intuit rise as a go-to platform for financial services. Owning TurboTax as well as Mint, tools for filing taxes and budgeting, respectively, the addition of Credit Karma, which allows customers to view their credit score for free, would advance Intuit’s product suite as well as bolster the data it already has on users.

“There hasn’t been that much innovation in the financial services world in the past two decades,” Credit Karma Founder and CEO Kenneth Lin said. “The combination of the two companies will really be able to move consumers forward.”

Credit Karma claims to have 100 million customers, with half of all American millennials being included within that number. It also states that it has over 2,600 data points on each customer, including their social security number as well as loan history. The company makes its money by selling customer information to third parties who advertise new credit cards and loans on the Credit Karma site. Credit Karma also receives a couple of hundred dollars for each card and loan that is acquired through ads on its site. Being one of the few tech startups that actually turn a profit, Credit Karma claimed to have received $1 billion in revenue in 2019.

Speaking on the deal, Intuit’s CEO, Sasan Goodarzi, said that “This is very core to what we’ve declared around helping our customers make ends meet and make smart money decisions.”

Luxury Asset Capital Acquires and Relaunches Borro

February 26, 2020 Luxury Asset Capital, the Denver-based lender that secures financing against goods such as Ferraris and Rolexes, has announced this month that it has acquired Borro and will be relaunching borro.com. LAC did not disclose the purchase price.

Luxury Asset Capital, the Denver-based lender that secures financing against goods such as Ferraris and Rolexes, has announced this month that it has acquired Borro and will be relaunching borro.com. LAC did not disclose the purchase price.

The news comes after LAC had been in talks to acquire Borro for years, LAC CEO Dewey Burke told deBanked. The merger will see Borro’s New York office remain open for business as many of its staff will stay on. As well as this, LAC and Borro will now be offering loans on a wider range of goods, that start at lower minimum amounts, and which will make use of more flexible terms, Burke stated.

“This was a transformational acquisition for us because obviously the competitor was out of the marketplace, but it really pushed us further to the forefront of being the preeminent lender in our niche space.”

Other news to come from announcement is that LAC is now offering to store customers’ luxury assets in its company vault, allowing the users who choose to do so to access capital immediately via a phone call. LAC will also be retiring its Lux Exchange and Pawngo brands, in favor of replacing them with Borro, because, as Burke put it, “we just thought it was a brand that was stronger than the legacy brands that we had.”

Beyond the merger, LAC plans to continue forging corporate partnerships, like that of its preexisting one with WatchBox, a trading service for preowned luxury watches. The strategy here being to link with the luxury goods ecosystem, enabling convenient pathways for customers to collateralize their asset.

United Capital Source Partners with Brex to Offer Deal on Card

February 21, 2020U nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

“We really wanted to start to offer business credit cards to our clientele. We believe that as we’re helping people solve their lending or funding issues, it’s also helpful to solve any problems that they face when running their day-to-day business,” UCS Founder and CEO Jared Weitz told deBanked in a call. “The key point that we really love about Brex which we’re offering to our clients is a 60-day, no-interest float on expenses. And that’s really helpful for folks when you’re making weekly and bi-weekly payrolls, when you’re purchasing inventory, and when you have folks that pay you every 30 or 45 days.”

The news comes as companies from various backgrounds are beginning to offer debit, credit, and charge cards. Apple, BlueVine, and challenger banks such as N26 and Varo are now all offering cards of some kind to their customers.

In Weitz’s view, this is the next step for the industry. With tech becoming more and more ingrained in finance, the convergence between the two fields is inevitable and ultimately beneficial for brokers.

“They’re already doing it on the personal side. And I think that once these tech-enabled companies start to get business data on their clients’ trends in their business account, they’ll be able to offer other products to them as well. For me, as a broker, if someone says, ‘Hey, does that make you nervous?,’ honestly, I don’t believe so. Because I think it opens up the sources for me to send deals to … I’m not a lender, so I’m not competing against them. I’m someone that would send them business. So when I look at them, I say this is just a new potential partner for me, a new opportunity.”

Patreon Adds MCA-like Product With Patreon Capital

February 20, 2020 Patreon, the membership platform that provides payment and subscription services for creators, will now start funding those artists that are on its site through Patreon Capital. Said to be modeled after Shopify Capital, the service will be available to certain creators initially, with Patreon reaching out directly to them to offer merchant cash advances.

Patreon, the membership platform that provides payment and subscription services for creators, will now start funding those artists that are on its site through Patreon Capital. Said to be modeled after Shopify Capital, the service will be available to certain creators initially, with Patreon reaching out directly to them to offer merchant cash advances.

The move comes after CEO Jack Conte had been quoted in January saying that “The reality is Patreon needs to build new businesses and new services and new revenue lines in order to build a sustainable business.”

It seems like this new service is part of a trend that has overtaken tech companies recently, best exemplified by the Apple Card, wherein established players, worried about longevity, are moving further into financial services, hoping to get long-lasting hooks into their customers.

Historically, Patreon has made money by taking a 5% cut from the subscription payments made to artists on its platform, with a further 5% going towards covering transaction fees, and the remaining 90% being left for the artist, who retains complete ownership of their work. It currently has over 100,000 creators on its site and over three million active monthly users. Contributions begin at $1, with content being unlocked in exchange for payment. Thus far, Patreon has paid out over $1 billion.

It has been reported that about a dozen deals have been made between creators and Patreon Capital so far. Hot Pod News ran a story featuring one such case, in which Multitude, a Brooklyn-based podcast studio, disclosed that it took funding of $75,000 over two years in order to pay the SAG-AFTRA rates of the actors it wanted to employ for a new audio sitcom titled Next Stop.

“We were running into this problem where we have a ton of great ideas, but because we’re a small business, we constantly have to decide between putting money towards paying our people and getting more equipment versus saving it up for a bigger project,” Multitude’s CEO, Amanda McLoughlin, told Hot Pod.

The premium attached to the financing was not revealed, however Multitude did note that the revenues of one of the studio’s other shows, Join the Party, would be taken as collateral if Next Stop is not profitable enough to pay the premium after two years.

“This arrangement is directly tied to the fact that we have successful podcasts making money on Patreon, and that we’ve already invested in the Patreon system to pay this stuff back,” comment Eric Silver, Multitude’s Head of Creative, underlining how Patreon Capital is linked with the analytics of Patreon’s base service. Much like how Amazon uses sales metrics and user data to gauge which retailers to lend to on its own marketplace, Patreon appears to be making use of seven years of data on its creators to determine who is best positioned to receive funding.

“Patreon has access to all the data about a creator’s earnings history, what they offer as benefits, how much they engage with their patrons … everything needed to forecast their earnings and retention, without a creator even needing to submit an application.” Patreon VP of Finance Carlos Cabrero stated. “This would be essentially impossible for a bank to replicate.”