Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

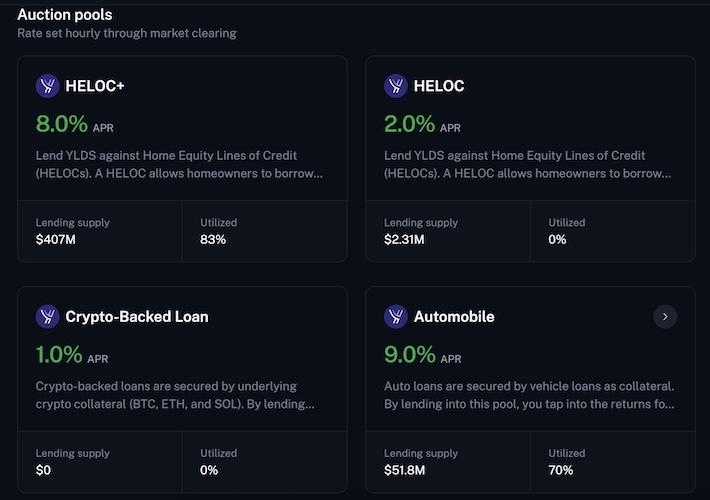

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

Last modified: May 24, 2026Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.