cryptocurrency

Need Capital for Your Funding or Lending Company? 3Jane Does it On Blockchain

July 27, 2026“I’m a big believer in agentic capital markets. I think we’re going to see a Cambrian explosion of novel primitives, driven largely by two pieces. Today, it’s just very easy to construct arbitrary financial building blocks using smart contracts,” said Jacob Chudnovsky, Founder of 3Jane, to deBanked.

3Jane provides credit facilities and forward flow arrangements across a range of products, including consumer loans, small business loans, and even merchant cash advances. The company previously provided a $10 million senior warehouse facility to consumer lender LendSwift, for example, and followed that with an inaugural $8.5 million purchase of small business loans from Slope, an embedded credit infrastructure provider that powers business lending programs for major players across the US, including Amazon. According to Chudnovsky, 3Jane would like to do even more deals in the small business lending and MCA space.

But with a twist.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

Chudnovsky is a software engineer by trade and entered the DeFi space in 2020.

“…around 2024, I basically came to the realization that credit is still an extremely underdeveloped vertical in crypto and particularly both the capital aggregation and the capital distribution side of it,” he said. “My initial focus was ‘can we get the best of crypto to distribute capital in a better way?’ and so I founded 3Jane, and we started off by doing unsecured lines of credit for crypto users in the United States who had a bunch of these different assets and could not really borrow against it in a streamlined way.”

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

“I just think we’re going to enter this complete renaissance of new different financial primitives and I think it’s going to drive a lot of adoption, new ways of thinking about our financial system and that sort of really resonated with me with the book,” Chudnovsky said.

And that new way of thinking is starting to take root. The capital markets utilizing blockchain to create efficiencies is already cropping up around the industry. Since 3Jane last spoke with deBanked, its purchase of embedded finance products from Slope has increased to a total of $60 million.

3Jane’s customers do not need to be crypto experts. The company handles that side of the transaction while underwriting the risk and executing what is otherwise a conventional capital markets deal, but one in which the infrastructure is robust enough that this can be a lender’s first and last facility. On 3Jane’s part, doing this requires a strong understanding of the various financial products it evaluates, including MCA.

“…there are a number of MCA operators in the United States that are doing things right, they’re growing significantly and they need leverage to scale their business,” Chudnovsky said. “and so warehouse facilities and to a lesser extent forward-flows for MCAs sort of equally make sense for them as long as you are cognizant of the risks.”

It’s Live, You Can Now Invest in a Credibly Warehouse Line Through Figure

July 21, 2026 IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

Specifically, Credibly boarded a business loan portfolio on July 21 and can already borrow against it using Figure’s Democratized Prime. Investors can now effectively participate in the earnings of that line by lending their own money into the pool. The amount of capital contributed to the pool and the utilization rate of it play a big role in the yield generated from that. Investors can pull out of the pool at any time assuming there is liquidity available to do so.

Unlike most investing platforms, investors can only participate in this one using blockchain rails (as was explained in deBanked’s May 23 story). Investors fund their accounts using dollars, crypto, or stablecoins, convert them into Figure YLDS tokens, and then lend those tokens into any number of available pools. As of the time of this writing investors can participate in HELOCs, auto loans, crypto loans, and now “small and medium business loans” which at present is sourced from Credibly. This all takes place on the Provenance blockchain and can all be easily conducted through the Figure Markets mobile app. deBanked was able to execute this process with no issues while using the investor side of the platform.

The investing opportunities on Figure’s Democratized Prime are warehouse lines for institutional-grade portfolios so investors are likely to see returns that resemble warehouse line rates (versus what one might expect if they do direct syndication with mom & pop lenders/funders). Credibly stands to benefit in the long run by the likelihood of lower borrowing rates and costs versus other capital market options and then being able to pass those savings onto their customers.

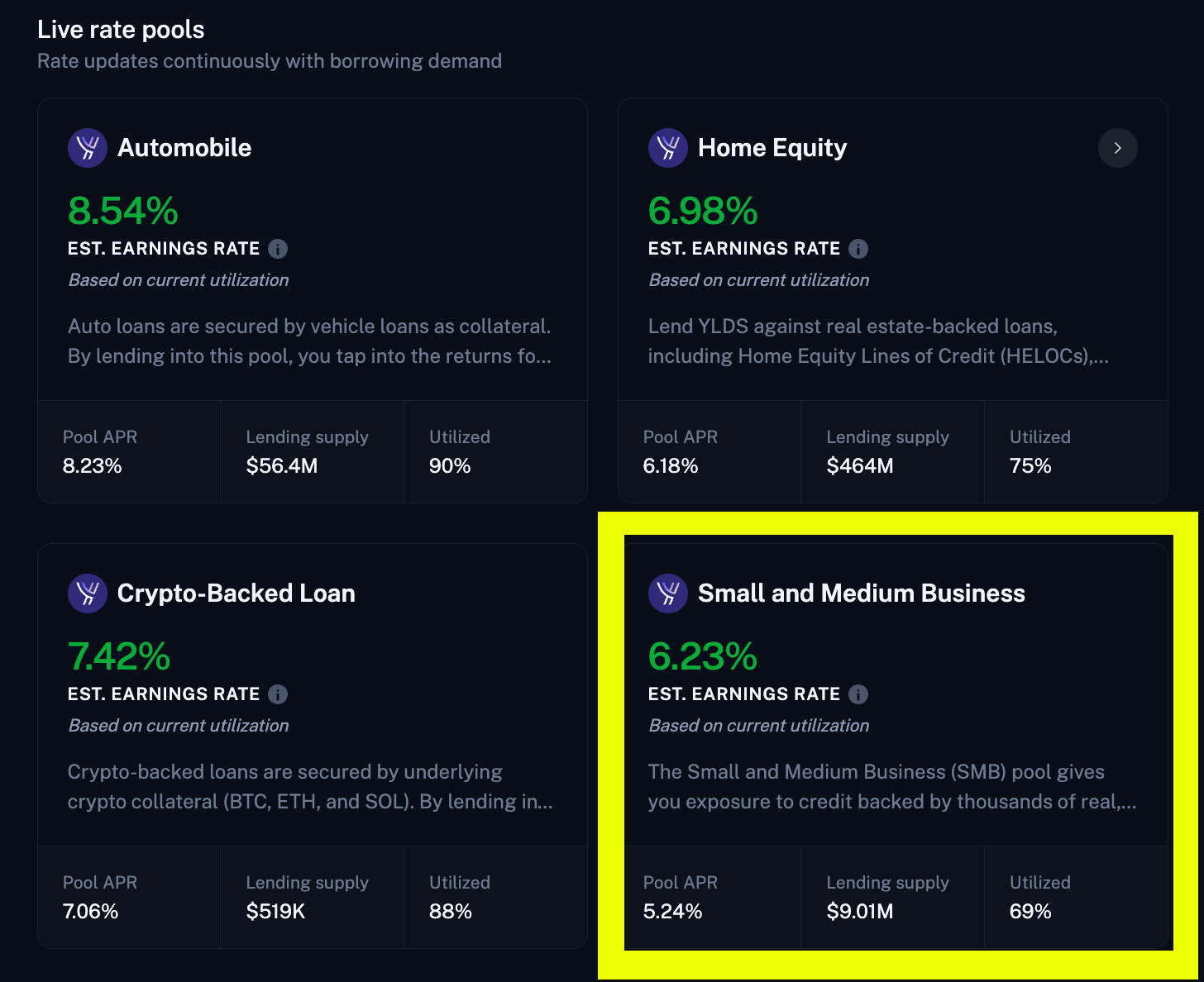

Investors will see some stats for the inaugural small and medium business loan pool which looked like this at the time of this writing:

The page also offers this information:

The Small and Medium Business (SMB) pool gives you exposure to credit backed by thousands of real, vetted American small businesses. The receivables represent payments owed by operating U.S. businesses. By lending into the pool, you earn from the cash flows those businesses generate as they repay their financing obligations. Backed by institutional-grade small-business credit, the SMB pool provides yield generated by a tangible, collateralized asset class, and a new way to diversify your portfolio.

Risk parameters

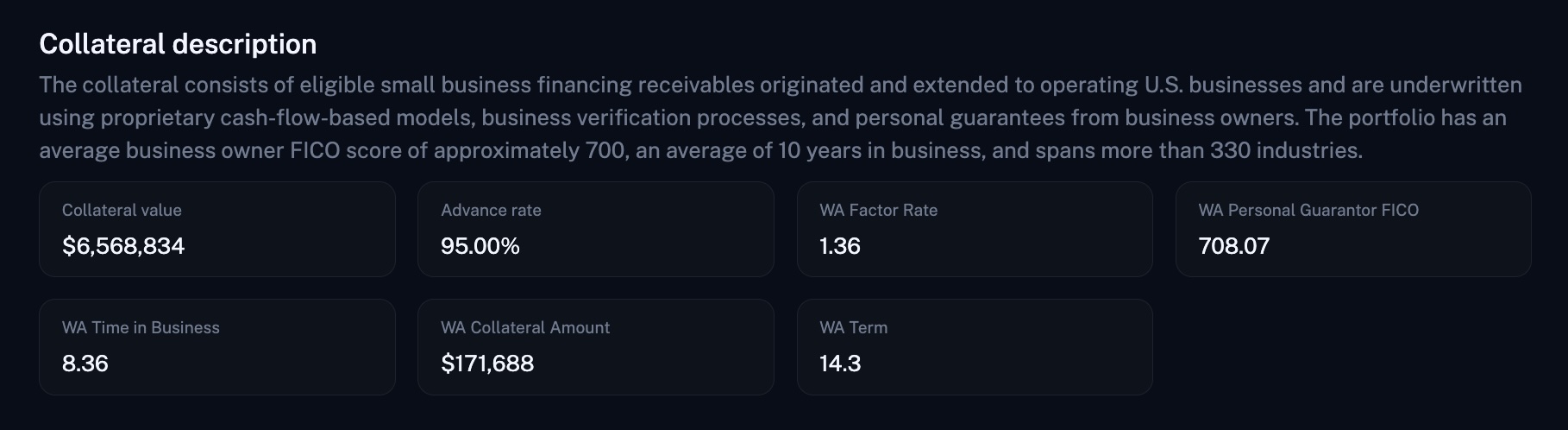

Democratized Prime manages risk through a structured financing facility backed by a diversified pool of prime small business financing receivables. The facility benefits from multiple layers of credit enhancement ensuring the pool can absorb a variety of adverse conditions before depositor yield is affected. This is enabled by a variety of mechanisms, including a 95% advance rate cap, reserve account funding, overcollateralization, originator repurchase obligations, and full recourse provisions. All receivables included in Democratized Prime must satisfy established eligibility requirements and be performing at the time of inclusion.Collateral description

The collateral consists of eligible small business financing receivables originated and extended to operating U.S. businesses and are underwritten using proprietary cash-flow-based models, business verification processes, and personal guarantees from business owners. The portfolio has an average business owner FICO score of approximately 700, an average of 10 years in business, and spans more than 330 industries.

The author contributed $5,000 in YLDS tokens into the Small and Medium Business loan pool on his own volition prior to the publication of this article for test purposes.

Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

May 23, 2026For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

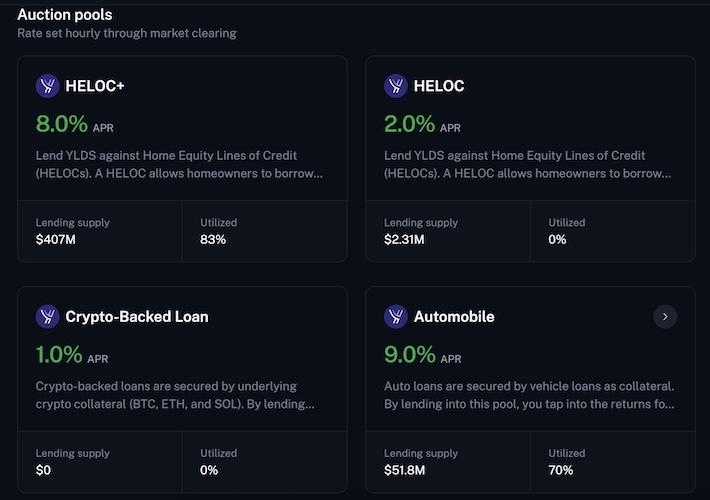

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

RadioShack Owners Accused of Running a Ponzi Scheme

September 25, 2025When the RadioShack brand was acquired in 2020 by Retail Ecommerce Ventures, LLC, the company shifted gears into a new direction, cryptocurrency. Using Twitter, now X, as its main base of messaging, the RadioShack account rapidly became outwardly controversial and hostile in order to generate eyeballs and attention. It was quite successful and piqued my curiosity to the point that it ended up on deBanked in 2021.

At the time the company said “RadioShack DeFi is focused on the early majority. It will become the first to market with a 100 year old brand name that’s recognized in virtually all 190+ countries in the world.”

When I actually inquired about information on its new DeFi platform, all I received was a digital coupon for a boombox…

I signed up to learn more about @RadioShack ‘s DeFi project and instead got offered a discount on a new boombox. pic.twitter.com/0O3i8llgyL

— Seán Murray (@financeguy74) December 30, 2021

But the party seemed to come to an end and the account stopped tweeting on November 17, 2022.

Why'd @RadioShack go dark after Nov 17, 2022? They were one of the most epic crypto troll accounts on twitter.

— Seán Murray (@financeguy74) February 15, 2023

Now, according to the SEC, it has been revealed that the owners of RadioShack and other defunct brand names had been conducting a ponzi scheme precisely through November 2022.

Taino Adrian Lopez, Alexander Farhang Mehr, and Maya Rose Burkenroad, were charged this week for running a $112M ponzi scheme. Apparently, none of the household brand names they acquired were generating any profits, but they claimed to investors that they were in order to raise capital. “Consequently, in order to pay interest, dividends and maturing note payments, Defendants resorted to using a combination of loans from outside lenders, merchant cash advances, money raised from new and existing investors, and transfers from other portfolio companies to cover obligations,” the SEC claims.

In addition to RadioShack, the accused operated Brahms, Linens ‘N Things, Modell’s, Stein Mart, and Pier 1 Imports.

Merchant Loses Whole EIDL After Attempting to Earn High Yield On It

July 25, 2022 It’s a tale of Covid EIDL relief gone wrong. A small business owner in Colorado Springs, CO is begging for his funds back after taking the entire lump sum of his EIDL funds ($525,000) and depositing them with a high-yield non-FDIC insured cryptocurrency tech company. The tech company, Celsius, declared bankruptcy less than two months later, yanking the merchant’s EIDL funds with it. Celsius was not a bank, the arrangement not a true deposit account, and the funds not FDIC-insured.

It’s a tale of Covid EIDL relief gone wrong. A small business owner in Colorado Springs, CO is begging for his funds back after taking the entire lump sum of his EIDL funds ($525,000) and depositing them with a high-yield non-FDIC insured cryptocurrency tech company. The tech company, Celsius, declared bankruptcy less than two months later, yanking the merchant’s EIDL funds with it. Celsius was not a bank, the arrangement not a true deposit account, and the funds not FDIC-insured.

In a letter submitted by the merchant to the bankruptcy court, he says that he deposited the funds there to “earn an APY to help pay back the 3.9% on the loan…” He further added that he believed his account to be safe because of the site’s Terms of Use.

“The funds in my Celsius Custodial account are not mine, they are the US Governments and I my entire business is secured and backed by these funds,” he wrote. “If they are not returned, my business would go bankrupt, my 15 employees would be let go, and 14 years of my life’s work lost and at the age of 49 years old, I would have to start over with nothing.”

Prior to the bankruptcy, Alex Mashinsky, Celsius’ CEO, oft touted the phrase: “banks are not your friend.”

Be Careful When “Financial Consultants” on LinkedIn Offer Crypto Advice

June 28, 2022 According to CNBC, fraudsters are disguising themselves on LinkedIn to trick users into financial schemes. What may seem like a simple networking conversation could be a tactic to develop trust until the mark is presented with a fraudulent crypto investment opportunity. These fake accounts on LinkedIn often pose as financial consultants. In an interview with CNBC, a group of victims that came forward revealed they had individually lost $100,000 to as much as $1.6 million from such scams.

According to CNBC, fraudsters are disguising themselves on LinkedIn to trick users into financial schemes. What may seem like a simple networking conversation could be a tactic to develop trust until the mark is presented with a fraudulent crypto investment opportunity. These fake accounts on LinkedIn often pose as financial consultants. In an interview with CNBC, a group of victims that came forward revealed they had individually lost $100,000 to as much as $1.6 million from such scams.

LinkedIn claims they removed 32 million fake accounts just in 2021 alone. There are several warning signs listed on the site that give examples of a scam message including grammar mistakes, messages that ask for personal information, offers that seem too good to be true and if they are not addressed to you personally.

Sean Ragan, the FBI’s special agent in charge of the San Francisco and Sacramento field offices, said “It’s a significant threat. This type of fraudulent activity is significant, and there are many potential victims, and there are many past and current victims.”

New Owner of Loan.eth Says its Worth Millions

June 8, 2022 Less than two months after spotlighting a new domain name market linked to the Ethereum blockchain, the name loan.eth was sold on a secondary market for the equivalent of $45,000. It’s not a website domain like one would expect with a .com or a .net, but rather a crypto wallet address shortener that can double as a screen name and authentication service on web 3.0. That’s just the tip of the iceberg of the utility that a .eth domain can offer.

Less than two months after spotlighting a new domain name market linked to the Ethereum blockchain, the name loan.eth was sold on a secondary market for the equivalent of $45,000. It’s not a website domain like one would expect with a .com or a .net, but rather a crypto wallet address shortener that can double as a screen name and authentication service on web 3.0. That’s just the tip of the iceberg of the utility that a .eth domain can offer.

Although most people may not be familiar with .eth domain names, the new owner of loan.eth, who goes by @BloomCapital_ on twitter, is so confident that such names will be adopted in the future, that he believes the value of this one will be many times what he paid for it.

“Just so it has to be said, Loan.eth won’t be sold for less than $10M,” Bloom wrote. Bloom said he considers loan to be the top .eth name that he has.

Senior Business Lending Exec of Square Has Moved to Coinbase

May 16, 2022 Ronak Daya, who spearheaded several of Square Capital’s lending divisions, including “head of product for business lending” and “head of product for external lending and partnerships,” announced on twitter that he had moved on from the company. He had been involved in SMB lending for 7 straight years. His new role? Head of Financing Products at Coinbase.

Ronak Daya, who spearheaded several of Square Capital’s lending divisions, including “head of product for business lending” and “head of product for external lending and partnerships,” announced on twitter that he had moved on from the company. He had been involved in SMB lending for 7 straight years. His new role? Head of Financing Products at Coinbase.

If you thought Coinbase was just about buying Bitcoin, you’re wrong. Daya announced that he’ll be leading a team “to build lending and financing products both for consumers and institutional clients.”

“As I explored what came after Square, my primary focus was on challenging myself to go in a fundamentally new domain/area, and build for a new customer,” Daya wrote. “The priority was learning. Learning by building in domains that I am passionate about, but know little about.”

Convinced that the world is moving towards becoming a crypto-native economy, Daya added that he wants to “play a part in using trust, ease and education to onboard the next billion customers to a new financial system.”

Currently, Coinbase already offers a lending product, loans up to $1 million at 8% APR with monthly payments and no credit check. Though Bitcoin is used as collateral, payments are made by monthly ACH debit or through a linked USD wallet.