Archive for 2020

Lendio Plans Development and Growth With $55 Million Series E

February 27, 2020 Today Lendio announced that it raised $55 million as part of its series E funding round. This included $31 million in equity led by Mercato Partners Traverse Fund and a $24 million debt facility from Signature Bank.

Today Lendio announced that it raised $55 million as part of its series E funding round. This included $31 million in equity led by Mercato Partners Traverse Fund and a $24 million debt facility from Signature Bank.

“We think that we’re just getting started, that there’s a really large opportunity in front of us and we’re excited that this round will give us the fuel that we need to continue to grow,” Lendio CEO Brock Blake told deBanked in a call. “We have a few different reasons for pulling together the round, but primarily, it’s all around investing in organic growth through partnerships and different marketing channels.”

Asked where these funding rounds may continue in an F, G, and H, Blake was unsure, saying that “every time we raise a round we do it with the expectation that it will be the last round.”

The funds in part will be used to further develop Lendio’s integrated lenders services, which are a set of tools used to identify which loan product and lender are the best match for a business owner; as well as the expansion of Sunrise, the bookkeeping platform Lendio acquired in 2019.

Intuit Agrees to Buy Credit Karma For $7.1 Billion

February 26, 2020 This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

Under the deal, Credit Karma will continue to operate as a stand-alone business and its CEO, Kenneth Lin, will stay on and run the company. Beyond that, some believe that the merger will see Intuit rise as a go-to platform for financial services. Owning TurboTax as well as Mint, tools for filing taxes and budgeting, respectively, the addition of Credit Karma, which allows customers to view their credit score for free, would advance Intuit’s product suite as well as bolster the data it already has on users.

“There hasn’t been that much innovation in the financial services world in the past two decades,” Credit Karma Founder and CEO Kenneth Lin said. “The combination of the two companies will really be able to move consumers forward.”

Credit Karma claims to have 100 million customers, with half of all American millennials being included within that number. It also states that it has over 2,600 data points on each customer, including their social security number as well as loan history. The company makes its money by selling customer information to third parties who advertise new credit cards and loans on the Credit Karma site. Credit Karma also receives a couple of hundred dollars for each card and loan that is acquired through ads on its site. Being one of the few tech startups that actually turn a profit, Credit Karma claimed to have received $1 billion in revenue in 2019.

Speaking on the deal, Intuit’s CEO, Sasan Goodarzi, said that “This is very core to what we’ve declared around helping our customers make ends meet and make smart money decisions.”

Luxury Asset Capital Acquires and Relaunches Borro

February 26, 2020 Luxury Asset Capital, the Denver-based lender that secures financing against goods such as Ferraris and Rolexes, has announced this month that it has acquired Borro and will be relaunching borro.com. LAC did not disclose the purchase price.

Luxury Asset Capital, the Denver-based lender that secures financing against goods such as Ferraris and Rolexes, has announced this month that it has acquired Borro and will be relaunching borro.com. LAC did not disclose the purchase price.

The news comes after LAC had been in talks to acquire Borro for years, LAC CEO Dewey Burke told deBanked. The merger will see Borro’s New York office remain open for business as many of its staff will stay on. As well as this, LAC and Borro will now be offering loans on a wider range of goods, that start at lower minimum amounts, and which will make use of more flexible terms, Burke stated.

“This was a transformational acquisition for us because obviously the competitor was out of the marketplace, but it really pushed us further to the forefront of being the preeminent lender in our niche space.”

Other news to come from announcement is that LAC is now offering to store customers’ luxury assets in its company vault, allowing the users who choose to do so to access capital immediately via a phone call. LAC will also be retiring its Lux Exchange and Pawngo brands, in favor of replacing them with Borro, because, as Burke put it, “we just thought it was a brand that was stronger than the legacy brands that we had.”

Beyond the merger, LAC plans to continue forging corporate partnerships, like that of its preexisting one with WatchBox, a trading service for preowned luxury watches. The strategy here being to link with the luxury goods ecosystem, enabling convenient pathways for customers to collateralize their asset.

How Hot Is The Legal Cannabis Industry?

February 24, 2020 One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

That’s some 30% more than the 1,000 vendors who packed into the Central Hall in 2018 and about double the 678 who were showing off their wares in the smaller North Hall two years ago, reports Chris Day, vice president for external relations at Denver-based Marijuana Business Daily, which follows the cannabis industry and sponsored the Las Vegas trade show.

“In December, 2019,” Day declares, “we did not have to turn people away because we expanded. We had enough room for exhibitors but we needed both halls.” Unable to resist a boast, he adds: “We’ve been the fastest-growing trade show in the country three years running.”

One face in the December crowd was seasoned financial broker Scott Jordan, the Denver-based managing director of the Alternative Finance Network. He was occupying a booth accompanied by two attractive female models in fetching T-shirts emblazoned with the message: “How much would you borrow at zero percent?”

The young ladies’ arresting appearance and the message worked to the extent that “it got people talking,” Jordan says. As for the zero-interest rate, it’s not exactly free money. “I’ve got a product that puts together a line of credit,” he explains, “and after they receive the line of credit, it charges them a fee.”

As a broker, Jordan does the spade work of poring through a cannabis business’s financial statements and business model before he tees up a deal—typically between $250,000 and $750,000—to “a cadre” of 35 lenders in 10 states. He’ll ascertain whether the best funding option should be structured as equipment leasing, a working-capital loan, a revolving line of credit, project financing, or a real estate loan.

One recent cannabis deal that Jordan midwifed involved a “post-revenue, pre-profitability” manufacturing and processing company headquartered in Colorado. The financing, which closed in April, 2019, involved a pair of four-year term loans: one for $400,000 to refinance existing machinery, and a second for an additional $500,000 to acquire new laboratory equipment. Both credits carried interest rates in the “mid-teens,” he says, and were secured by the equipment.

Once the debt financing was in place, the manufacturing operation was “fully functioning,” Jordan reports, paving the way for the company to raise $30 million in venture capital financing. Jordan argues that “even if they pay a 10-20 percent interest rate, it’s better to preserve equity and finance through a normal type of loan. If you need an extraction machine or packaging equipment,” he adds, “why give up equity if you can finance it through debt?”

Jordan’s reasoning appears to sit well with clients and funders alike. Since 2014, he has brokered 85 transactions worth $33 million. He reckons that two out of three deals that he takes to funders meet with success. “My best year was 2015 because there were only a few competitors and I was the only guy on the block,” he says.

As the country steadily decriminalizes and legalizes pot, however, early market entrants like Jordan no longer have the cannabis business all to themselves. Thirteen states have legalized recreational marijuana for adults. These include California, Colorado, Oregon, Washington and Nevada in the West; Illinois and Michigan in the Midwest; and Massachusetts, Vermont and Maine in the East. Hawaii and Alaska permit it and, if you’re over 21, you can legally grow, smoke or ingest weed in the District of Columbia, but it cannot be sold commercially.

An additional 24 states have approved medical marijuana. While research on cannabis’s medicinal properties remains thin—largely because of objections by federal law enforcement—it is being prescribed for a range of maladies, including cancer, glaucoma, epilepsy, Crohn’s Disease, multiple sclerosis, nausea, and pain. [“The marijuana plant contains more than 100 different chemicals called cannabinoids,” according to WebMD. “Each one has a different effect on the body. Delta-9- tetrahydrocannabinol (THC) and cannabidiol (CBD) are the main chemicals used in medicine. THC also produces the ‘high’ people feel when they smoke marijuana or eat foods containing it.”]

Industry data assembled by MJBizDaily reflects both the broad acceptance of legal cannabis use and its increasing commercial popularity. U.S. revenues from legal weed and its byproducts are expected to clear $16.4 billion this year, a 40% growth rate over the $11.75 billion in estimated revenues for 2019. The legal cannabis industry now employs about 200,000 persons in the U.S., about the same number as flight attendants (120,000) and veterinarians (80,00) combined.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

“We’re showing that sales were close to $3.2 million on the first day of 2020,” says MJBiz’s Day. “Illinois is the big story right now,” he adds. “Anytime a new state opens up in the market, you’re seeing enormous pent-up demand and enthusiasm.”

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

That designation has also made it hard for the cannabis industry to engage in simple financial transactions, much less obtain financing. “Despite the majority of states’ having adopted cannabis regimes of some kind, federal law prevents banks from banking cannabis businesses,” Joanne Sherwood, president and chief executive at Citywide Banks, a $2.3 billion-asset bank headquartered in Denver, testified to Congress last summer. “The Controlled Substances Act,” added Sherwood, who is chair of the Colorado Bankers Association, “classifies cannabis as an illegal drug and prohibits its use for any purpose. For banks, that means that any person or business that derives revenue from a cannabis firm is violating federal law and consequently putting their own access to banking services at risk.”

And despite the herculean efforts by the cannabis industry to soften its image, obtaining financing from traditional sources like pension funds, insurance companies and university endowments remains a daunting proposition as well, says David Traylor, senior managing director at Golden Eagle Partners. His four-person, boutique investment fund, which makes equity investments in up-and-coming cannabis companies, relies on wealthy individuals and family offices for the bulk of its funds.

“Capital is hard to come by for this industry,” Traylor says. “From day one, most venture capitalists have been staying out of it. It’s still illegal in many states and their limited partners are endowments like Harvard and Yale, which see marijuana as the antithesis of education.”

Sarah Sanger, chief financial officer at Oak Investment Funds, a real estate investment firm based in Oakland, says: “There’s a great deal of economic activity in California but it’s stymied by the lack of financing and difficulty with changing regulations. It provides an opportunity for really expensive debt from private investors willing to do due diligence.”

That absence of establishment financing has opened up a plethora of opportunities for alternative funders, and not just in agriculture and plant cultivation. While agriculture represents the bedrock of the industry there is no downstream product, of course, without the cannabis leaf— growing and harvesting cannabis is just one stage of the industry’s life cycle.

MJBiz’s Day notes, for example, that that the legal cannabis industry is regulated for safety, so growers must show that “the flower has no molds or contaminants.” That means that crops are subject to rigorous testing and decontamination, which requires both materials and expertise. To process the leaf and develop “infused products” by extracting cannabis-based oils entails the purchase and deployment of costly technology. Packaging and labeling along with tracking systems that, Day says, “are stricter than in other places” are also key components of the farm-to-market supply chain.

Meanwhile, in an ongoing effort to appeal to a fresh cohort of customers, Jordan notes, the cannabis industry continues to develop innovative uses for the plant. “There are so many applications and new products that keep appearing, like ice cream with marijuana, vaporizers, inhalers, and syrup,” he says. “Now, there are mints—something I hadn’t seen before—and different ways to ingest the product and get high and not look like a druggie.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Recent Greenbox Capital deals in 2019, Fein says, included one with merchant cash advances of $80,000 and $60,000 in growth capital to a Colorado dispensary. The operation put the money to work adding two retail outlets during the year, he says, bringing to four its total number of storefronts. In addition to cannabis flower, the dispensary sells “edibles, tinctures, lotions, and wax concentrates,” Fein reports. Both short term cash advances require regular ACH payments.

Greenbox Capital also made a $135,000 cash advance to a cannabis-testing laboratory in Southern California in August, 2019 for the purchase of sophisticated equipment. The company, he says, is doing $140,000-a-month in revenue and cashflow is strong and on the rise.

“Greenbox is always interested in higher risk deals,” Fein says, noting that banking services remain off limits to legal cannabis firms. “But we fund them for the same reason we fund lawyers and auto sales—things that most others will not do. There’s nothing wrong with risk,” he adds, “as long as you clearly assign a proper value to the deal and price to it.”

Steve Sheinbaum, a New York broker and chief executive at Circadian Funding, has unabashedly climbed aboard the cannabis bandwagon. “The market is exploding and it’s attractive to lenders because it’s a product people can put their hands on,” he says. “If I’m dealing with a grower, I can leverage real estate and usually there’s equipment. If they’re producing, there’s inventory and I can look at the income statement to see what kind of cash flow the business is generating.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

In another recent deal, Circadian arranged an unsecured merchant cash advance for $300,000 to a Pacific Northwest technology company developing specialty, point-of-sale software for the cannabis industry. The firm showed monthly revenues of $300,000.

“It’s not federally permitted for cannabis firms to take payments from Visa, Mastercard or American Express,” Sheinbaum explains. “But this technology company is using debit or credit cards to pay for cryptocurrency which is stored on a prepaid card which customers can then use to purchase cannabis.”

The tech company had been struggling to find money and Sheinbaum took satisfaction in a deal announcement that went out in an e-mail to the industry. “Funding complicated deals is what gets our blood flowing,” Sheinbaum wrote. “Anyone can get a restaurant or dentist funded. No one needs help with that.”

Manny Columbie, a Miami-based senior funding manager at H&J Capital Group, an Orlando firm, reports funding agricultural and dispensary businesses in California, Colorado and Washington State. In the Evergreen State, he says, he recently provided funding to a woman who owned a marijuana-themed café connected to a cannabis dispensary. The deal went through after examining her recent bank statements and two years of federal tax returns.

“The best thing about lending to people in this industry is their ability to repay,” Columbie says. “They’re never lacking in funds.”

He provided more detail on a deal currently in the works involving a physician in Irvine, California, with an 800-plus credit score from the rating agency Experian and personal tax returns showing $2 million in annual income. The doctor, Columbie says, has been making transdermal patches infused with THC in addition to his medical practice and needs specialized equipment to lower his manufacturing costs to 55 cents per patch. The patches sell for $40-$60 apiece, Columbie says, depending on the THC content.

If the deal goes through and is approved by H&J’s credit committee, the physician would likely be extended a $350,000 loan with a 10-year maturity secured by the Chinese-manufactured equipment. Factoring in the doctor’s excellent credit and other positives, the interest rate on the credit could be as low as 5%-7%.

While the environment for legal cannabis seems to grow more favorable by the day, market participants urge funders to remain circumspect. One remaining fly in the legal cannabis ointment has been the persistence of an illegal black market. Estimates are that as much as 60% to 80% of the marijuana market in California is illicit, says Craig Behnke, an equity analyst at MJBiz.

Law-abiding businesses must also contend with overbearing regulators and high taxation. The California Department of Fee and Tax Administration recently jacked up its excise tax on cannabis to 80%, effective on Jan. 1, 2020.

And the state’s constabulary isn’t helping matters either, notes Sanger of Oak Funds. “There are going to be a lot of operators that end up being losers because of the regulatory environment,” she says. “Law enforcement is using all of its resources to make sure legitimate businesses are following the rules instead of clamping down on black market activity. That makes it harder for legitimate retailers to make money because people are still shopping in the black market.”

The recent collapse of the shares of publicly traded Canadian cannabis companies, which some blame in part on the illicit competition from the black market, also stands as a cautionary sign. Last August, the Motley Fool listed ten “Pot Stocks”—including Canopy Growth and Aurora Cannabis, both of which are listed on the New York Stock Exchange—that together lost a stunning $20 billion in market capitalization.

The drubbing that heedless investors have taken in the Canadian stocks reminds analyst Behnke of the debacle in dotcom stocks back in 2001-2002, but with a big difference. “The dotcoms were a brand-new invention and people had no idea how big the Internet companies would be,” he told deBanked. “But cannabis has been around for a thousand years. I feel like it was a shame on investors and the companies. This shouldn’t have happened.”

Maryland State Legislators Want to Enact “Prohibition” on Merchant Cash Advances

February 21, 2020A Maryland State Senator and 4 State Delegates are calling for a prohibition on merchant cash advances through a bill introduced this month that aims to make it illegal to arrange, facilitate or consummate a merchant cash advance with a merchant in the state.

Maryland State Senator and 4 State Delegates are calling for a prohibition on merchant cash advances through a bill introduced this month that aims to make it illegal to arrange, facilitate or consummate a merchant cash advance with a merchant in the state.

Maryland State Senate Bill 913 and House Bill 1478, literally headlined as Merchant Cash Advance Prohibition, defines a merchant cash advance as:

AN ARRANGEMENT BETWEEN A BUYER AND A SELLER IN WHICH THE BUYER AGREES TO PURCHASE AN AGREED–ON PERCENTAGE OF FUTURE CREDIT CARD REVENUES OR DEBIT CARD REVENUES THAT ARE DUE TO A SELLER FOR A PREDETERMINED PURCHASE PRICE

If all went to plan, the law would go into effect as early as October 1st of this year. Support at this early stage is bipartisan, with the Senate Bill sponsored by a Democrat and the House bill sponsored by 4 republicans. Hearings on the matter are being held on March 2nd and 3rd.

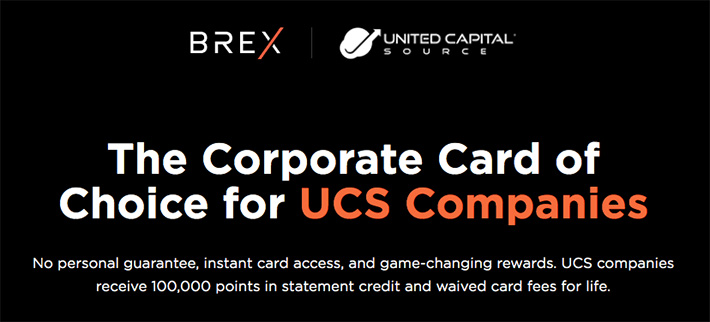

United Capital Source Partners with Brex to Offer Deal on Card

February 21, 2020U nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

“We really wanted to start to offer business credit cards to our clientele. We believe that as we’re helping people solve their lending or funding issues, it’s also helpful to solve any problems that they face when running their day-to-day business,” UCS Founder and CEO Jared Weitz told deBanked in a call. “The key point that we really love about Brex which we’re offering to our clients is a 60-day, no-interest float on expenses. And that’s really helpful for folks when you’re making weekly and bi-weekly payrolls, when you’re purchasing inventory, and when you have folks that pay you every 30 or 45 days.”

The news comes as companies from various backgrounds are beginning to offer debit, credit, and charge cards. Apple, BlueVine, and challenger banks such as N26 and Varo are now all offering cards of some kind to their customers.

In Weitz’s view, this is the next step for the industry. With tech becoming more and more ingrained in finance, the convergence between the two fields is inevitable and ultimately beneficial for brokers.

“They’re already doing it on the personal side. And I think that once these tech-enabled companies start to get business data on their clients’ trends in their business account, they’ll be able to offer other products to them as well. For me, as a broker, if someone says, ‘Hey, does that make you nervous?,’ honestly, I don’t believe so. Because I think it opens up the sources for me to send deals to … I’m not a lender, so I’m not competing against them. I’m someone that would send them business. So when I look at them, I say this is just a new potential partner for me, a new opportunity.”

Bitty Advance Has a New Major Partner

February 21, 2020Craig Hecker, who founded and sold Rapid Capital Funding, has acquired a stake in Bitty Advance. According to the press release, Hecker and Bitty Advance CEO Edward Siegel first met more than ten years ago when Siegel had just entered the merchant cash advance industry at Rapid Capital Funding.

Bitty has been on the move. The company has been a regular participant in the networking conferences that deBanked puts on each year.

Siegel says of Hecker in the announcement that “I am thrilled to bring on Craig with all of his MCA experience and his creative thinking to help scale Bitty’s growth.”

The newly-made partners told deBanked that they believe this deal will enable Bitty Advance to leap forward to the next level by adding technology to fund faster and create an industry changing awesome customer experience.

Craig Hecker Acquires Stake in Bitty Advance

February 21, 2020 Fort Lauderdale FL – February 21, 2020: Craig Hecker has acquired an equity stake in Bitty Advance.

Fort Lauderdale FL – February 21, 2020: Craig Hecker has acquired an equity stake in Bitty Advance.

Hecker is a pioneer and leader in the merchant cash advance industry who founded, grew, and sold Rapid Capital Funding.

Bitty Advance CEO Edward Siegel first crossed paths with Hecker in 2009 when Siegel was employed by Rapid Capital Funding. Siegel since then went on to launch Bitty Advance in 2017 to cater exclusively to small businesses that generate less than $100,000 in annual revenue.

Hecker will be providing valuable thought leadership and capital to help Bitty continue to grow and become the leader in the space.

“I am thrilled to bring on Craig with all of his MCA experience and his creative thinking to help scale Bitty’s growth,” Siegel says.

The start of the partnership was memorialized with a video, attached below.

About Bitty Advance

Bitty Advance was founded in 2017 and is based in Fort Lauderdale, FL. To reach the company, call 800-324-3863 or email partners@bittyadvance.com.