Archive for 2020

Trump Pledges Immediate SBA Lending Support

March 11, 2020 President Trump pledged to support SBA lending through ramped-up low interest loans to small businesses that are suffering or may suffer from a decline in business due to recent public health fears. Additionally the President says that he will make or ask Congress to impose a degree of tax relief to those affected.

President Trump pledged to support SBA lending through ramped-up low interest loans to small businesses that are suffering or may suffer from a decline in business due to recent public health fears. Additionally the President says that he will make or ask Congress to impose a degree of tax relief to those affected.

More information about the plans will be published as they become available. The President’s speech was made at 9pm EST in which he announced broad preventative and relief measures including a 30-day ban from all European travelers (excluding the UK).

OnDeck Shares Lose More Than 30% Of Their Value in a Week

March 11, 2020Shares of OnDeck have suffered in the last week as the market has seen a dramatic pullback. Shares have traded as low as $2.17 on Wednesday, down 12% from the previous day. The company’s market capitalization is at $128.2M million, down from its 2014 IPO value of $1.32 billion.

DataMerch.com to Release Updated Version 2.0 of Online Database

March 10, 2020Tampa, March 10th, 2020 /DeBanked/ — DataMerch.com, an online underwriting database for the alternative financing industry, announced they will be releasing version 2.0 in March 2020. DataMerch has designed a refreshed look of the site with improved the functionality. DataMerch took these steps to position themselves for better scalability as their database record count continues to grow past 40,000.

“We’re launching the new version of DataMerch to improve the scalability and features for our funder members,” said Co-Founder Scott Williams. “The new version will allow us to add new features and make changes quicker than before.” When asked what will be different about version 2.0, Mr. Williams responded, “We have a new updated look that I think our members will appreciate. We’ve automated the recent suspicious activity alerts that will now be viewable from the dashboard. We’ve also added an analytics tab that allows our members to see their number of searches, hits, entries, and more. This will allow our members to see in real time the business benefits of DataMerch and their contributions.”

DataMerch leadership say they will continue to invest in developing the functionality of DataMerch and add features that are relevant to their members. They plan to add billing and invoice functions, bulk automated uploads, and updated API version in 2020.

About DataMerch

DataMerch LLC was founded in 2015 to help funders in the alternative financing industry make informed underwriting decisions. DataMerch members can screen their applications using DataMerch’s specifically designed FEIN search and enter unsatisfactory businesses into the database. DataMerch currently has over 100 industry-leading subscribed members working together as a community. DataMerch can be accessed at https://www.datamerch.com and contacted for membership at support@datamerch.com

Thanks to the Virus Craze: It May Now Be Unlawful For Telemarketers Doing Business in New York To Call Large Swaths Of The Country

March 10, 2020Are you a telemarketer that does business in New York? A large and growing percentage of the country may now be off-limits to contact, thanks to a recently enacted New York State law that prohibits unsolicited telemarketing sales calls to any person in a county, city, town or village under a declared state of emergency or disaster emergency.

New York General Business Law 399-z (5-a)

It shall be unlawful for any telemarketer doing business in this state to knowingly make an unsolicited telemarketing sales call to any person in a county, city, town or village under a declared state of emergency or disaster emergency as described in sections twenty-four or twenty-eight of the executive law.

The statute, which seemingly doesn’t limit its reach to New York individuals, but rather to any place in which a state of emergency has been declared, may mean that anyone doing business in New York may need to be monitoring active states of emergency around the country. At the time of this writing, those places include the states of:

- New York

- New Jersey

- California

- Florida

- Maryland

- Washington

- Oregon

- Utah

- Kentucky

- North Carolina

As this law amends Section 399-z, it is a good idea to read the entirety of the section.

deBanked is not a law firm. For legal advice related to this law, consult with a suitable attorney.

Can Amazon and Goldman Sachs Win With SMB Lending?

March 10, 2020 B2B e-commerce dwarfs the value of retail online transactions — by some estimates, those B2B transactions top some $1 trillion per year in the U.S., which compares to about a half billion dollars of revenue for the B2C side. And B2B e-commerce keeps on growing as more companies — especially small- and medium-sized operations — look to online marketplaces and other channels for daily suppliers, and otherwise shift toward fully digital and mobile operations instead of relying on paper invoicing and other analog supply chain processes.

B2B e-commerce dwarfs the value of retail online transactions — by some estimates, those B2B transactions top some $1 trillion per year in the U.S., which compares to about a half billion dollars of revenue for the B2C side. And B2B e-commerce keeps on growing as more companies — especially small- and medium-sized operations — look to online marketplaces and other channels for daily suppliers, and otherwise shift toward fully digital and mobile operations instead of relying on paper invoicing and other analog supply chain processes.

That’s one of the important factors to keep in mind when considering the prospects of Amazon potentially working with Goldman Sachs to offer SMB lending options by adding the investment bank to the Amazon platform. The possibility of such a business offering — pairing up one of the world’s leading retail, delivery and one-button payment operations with the venerable investment bank — was floated early in 2020 and is already casting a shadow across the B2B and lending community. The backing and brand strength of Goldman Sachs could help unleash a new SMB lending force — one that is also fueled by Amazon’s treasure chest of consumer data and Goldman Sachs’ underwriting expertise. But let’s not get ahead of ourselves just yet.

Significant pitfalls come along with the anticipated opportunities. Not only that, but nothing has yet gotten off the ground, at least not officially. Here’s the idea, culled from previous reports and conversations with experts who know the lending space, along with keen observers of retail and Amazon: The e-commerce operator, eager to build a stronger ecosystem around its already robust B2B marketplace and related operations, would team on SMB lending with Goldman Sachs, itself eager to break into new product lines and add some new fat to its margins.

Amazon and Goldman Sachs aren’t saying too much about that idea and did not comment for this story. The rough outlines of the plan appeared in the financial press in February. But it’s no secret that the two companies are indeed looking for new financial products and new consumer segments.

Amazon has built its B2B business into a unit whose growth has recently outpaced its retail side and even its powerhouse Amazon Web Services. As well, Amazon was on track in 2019 to invest some $15 billion in new tools for small- and medium-sized business, according to company documents and officials.

Granted, much of that explosive growth comes about because B2B is relatively new for Amazon, but such growth demonstrates how well Amazon is gaining — and even keeping — new B2B customers. Many of them are attracted to the digital and mobile efficiency of the Amazon platform, to say nothing of the speed of Amazon deliveries as the Seattlebased company continues to pour massive investment into trucks, warehouses, fulfillment robotics and other logistical areas. Just consider this data point: SMB thirdparty sellers tend to make up more than 55 percent of sales in Amazon stores, according to company financial documents.

Loans offered by Amazon and Goldman Sachs would help those Amazon customers fund purchases of supplies without having to seek out another creditor — or leave the Amazon online and mobile ecosystem.

“If the SMB is already using Amazon to sell and distribute their product, it makes sense they would also accept a loan from them,” Julie Stitzel, the vice president, Center for Capital Markets Competitiveness, U.S. Chamber of Commerce, told deBanked. “Amazon is already a trusted partner of their business operations and integrating the financial component is convenient—it saves time because you don’t have to deal with two separate entities.”

The move also would make sense, at least on paper, for Goldman Sachs, Joe Ganzelli, Sr., a Senior Director for Cornerstone Advisors, told deBanked. “They are not in the small business space, and this is a space that, frankly, would be challenging for them to compete in without a partner,” he said. Additionally, this potential SMB lending partnership with Amazon could come as Goldman Sachs executives seek to meet their goals of diversifying their business in 2020 and beyond, according to Ganzelli, previous comments from those executives and other reports. “Small business is such a big driver of our economy,” he said.

Those are among the main opportunities. But just because Goldman Sachs and Amazon are involved doesn’t mean the SMB lending offering would succeed. For instance, both companies have had bouts of recent or high profile failure. Who, for instance, has forgotten the massive stumbles of Goldman Sachs leading up to the 2008 financial crash? And while Amazon has gained ground with fashion and apparel, the company has had a relatively hard slog selling trendy clothes to consumers. Could SMB lending become another pothole for those two companies?

Well, certain obstacles would have to be overcome. For Goldman, the learning curve to gain expertise on SMB lending would be severe, according to Ganzelli — even though all that Amazon customer data that’s already been acquired by the e-commerce giant would certainly help with that education. Still, “anytime you enter a new niche, it’s challenging,” he said. As for Amazon, the main — and perhaps only real downside visible at this point — comes from the commitment that comes with SMB lending. “Amazon will be contractually tied to this arrangement if it’s not a success or does not meet growth objectives,” he said.

All that said, this stands as an appealing time for these two heavyweights of the U.S. economy to see if they can make good money via SMB nonbank lending. “While the majority of small and medium size business lending comes from banks, alternative lending products are an increasingly popular option for SMBs,” said Stitzel. “Allowing you to work with one entity to streamline business operations and mitigate economic volatility in a cost effective way, frees a SMB owner to focus more on building their business and less on administration. Companies like Square and Intuit are already successfully doing this for SMBs using their platforms.”

That’s not the only wind behind the sales of this growing trend of alternative SMB lending, of course. Millennials still might take all kinds of scapegoating heat for various consumer, cultural or economic trends — unfairly or not — but the fact is that those younger people are growing up, and starting to take more responsibility for B2B operations, including supply chain and invoicing tasks. As that happens, millennials are playing a growing force in anchoring more B2B companies to mobile and digital platforms. In general, millennials prefer one-stop shopping with trusted outlets. That would certainly benefit Amazon and Goldman Sachs in any SMB lending offering they launch — as that is now helping such alternative lending offerings as Kabbage and some of the newer PayPal products.

“Millennials are the folks who grew up with the expectation of seamless digital experiences,” Ganzelli said. Those B2B consumers are willing to pay the often “hefty” premiums that come with such experiences, too, he said. “The delivery experience and the speed-to-close just blows banks out of the water.”

Robinhood Goes Down Three Times in One Week, And The Timing Couldn’t Be Worse

March 10, 2020 The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

Robinhood’s first outage was on Monday, March 2. Lasting only a few minutes, the loss of service coincided with the biggest one-day point gain of the Dow in history. The second came the next day, lasting two hours after the Federal Reserve announced a cut of 0.5% to interest rates.

The Sarasota-based tech giant’s co-CEOs released a statement that Tuesday on the company’s blog placing blame for the outages on their overstressed infrastructure. They claimed that their servers struggled with an “unprecedented load” that led to a “‘thundering herd’ effect—triggering a failure of our DNS system.”

The company has yet to release a statement explaining the third service blackout today, which took place during a period that saw the stock exchange pause trading for 15 minutes to prevent a freefall.

In response, Robinhood customers are threatening legal action. Numerous Twitter accounts have popped up under the name ‘Robinhood Class Action,’ or as some variation of this, with the largest of these having over 7,500 followers at the time this article was published. Travis Taaffe of Florida filed a federal lawsuit on Wednesday on behalf of himself and other traders, claiming that Robinhood was negligent and in breach of contract by failing to “provide a functioning platform” for traders, rendering them unable to move stocks.

Having 10 million customers, the company could be facing a lot of claims. As of last week, Robinhood has been offering its Gold members three months of the subscription for free. The price of this would amount to $15 dollars altogether; and the second cost of the subscription, 5% yearly interest on borrowing above $1,000, will not be waived as part of this compensation. Robinhood has described this offer as a “first step.”

OnDeck, Lending Club Shares Battered By Market Turbulence

March 9, 2020The collateral damage of market panic led to all-time low share prices for online lending companies OnDeck and LendingClub on Monday. By noon, OnDeck was down 7.5% on the day at $2.55 (the low was $2.47) and LendingClub was down 5% at $9.62 (the low was $9.26).

Online lender Elevate also hit a new all-time low of $2.50.

How Kabbage Insights Seeks to Level Playing Field for Small Businesses

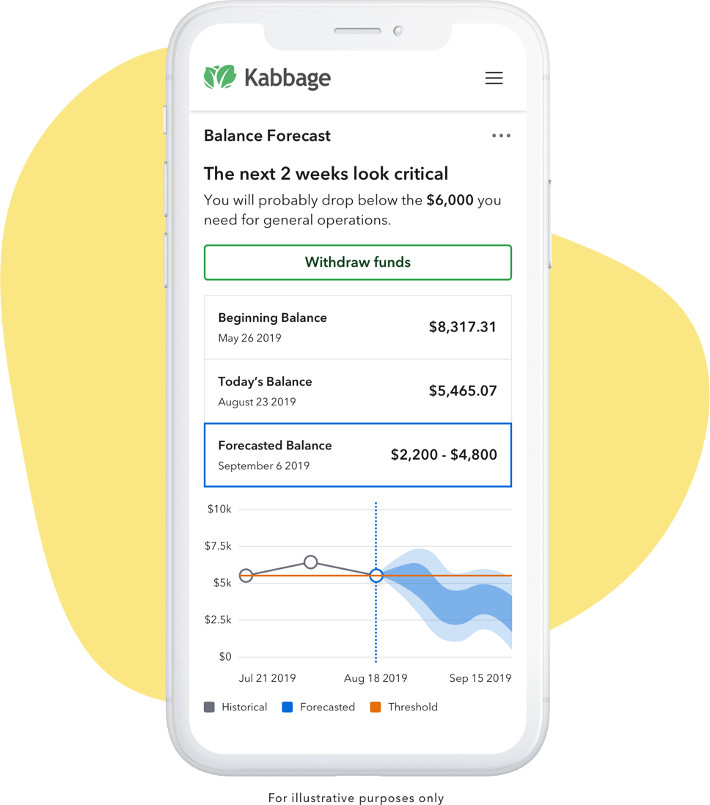

March 5, 2020 This week, Kabbage released its latest product, Kabbage Insights, to the public. Having been available privately since February 10th, the service is now free to all Kabbage customers. Released a month after Kabbage Payments, Insights adds to Kabbage’s ecosystem of products by helping small business owners identify and prepare for cash flow deficits.

This week, Kabbage released its latest product, Kabbage Insights, to the public. Having been available privately since February 10th, the service is now free to all Kabbage customers. Released a month after Kabbage Payments, Insights adds to Kabbage’s ecosystem of products by helping small business owners identify and prepare for cash flow deficits.

Acting almost like a virtual assistant, Insights links to and analyzes a business’s financial data, serving up a report of how the company has performed historically, how it’s doing currently, and what the projections for its future are looking like. While this may sound like standard business planning and budgeting, the time and resources required to provide in-depth financial analyses are usually only in possession of larger companies. Insights, according to Kabbage’s Head of Income Products, Abraham Williams, is an attempt to bridge this gap between what larger businesses have traditionally had access to and what small business owners have been unable to claim.

“Kabbage has, for a number of years now, used data science, modeling, and machine learning to come up with financial decisions on whether to give someone a loan, and we’re right a lot of the time.” Williams told deBanked over the phone. “With this, we’re able to bring this modeling to our small business customers.”

As well as providing a breakdown of a company’s financial history and future, Insights offers a threshold alert system wherein customers can set a desired low-balance amount and receive notifications when they are nearing it. And by pairing Insights with Kabbage’s Small Business Revenue Index, users will be able to compare their company against those of a similar size/location, so long as these businesses are Kabbage customers. The data used to make these comparisons will be aggregated and anonymous.

The public launch of Kabbage is part of the company’s plan to create a fintech ecosystem that completely eliminates waiting times, and is the culmination of Kabbage’s ten years of collecting and analyzing small business financial data.

Or, as Kabbage CEO Rob Frohwein said in a statement: “As a small business owner for many years, I spent many sleepless nights trying to figure out whether I’d have the cash to pay my various expenses, including payroll at the end of the month and it’s been a mission of mine to solve this ubiquitous problem for all small business owners ever since. Kabbage is pleased to launch Insights, taking on this burden for small business owners and providing them with cash flow analyses that large enterprises have at their fingertips. We will continue to level the playing field for the small business owner.”