Archive for 2019

With Interest Rates Up, OnDeck’s Cost of Funds Comes Way Down

February 12, 2019 OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

During the earnings call, OnDeck CEO Noah Breslow said, “We improved the terms and structures of our credit facilities and increased the number and quality of our funding providers, adding new banks and life insurance companies.”

That’s all before OnDeck even closed on an $85 million revolving credit facility with a lender group consisting of four banks earlier this month. The rate on that came in at 1 month LIBOR (currently around 2.5%) + 3.00%.

OnDeck’s loan yield in Q4 was the highest its been in the last 2 years at 36.6%.

The company enjoyed record earnings for Q4 2018 ($14 million) and full year 2018 ($27.7 million). They also had record origination volume of $658 million, a 2% increase from Q3 and a 21% increase from Q4 2017. Their sales and marketing expense for acquiring new customers remained flat compared to last quarter.

Fintech Inevitable, But Petrou Says Risks Abound

February 12, 2019 At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

If large bank mergers are a trend, Managing Director of Federal Financial Analytics Karen Petrou told MarketWatch that this is in part because banks realize that they can combine resources to develop mobile banking capabilities to compete with online banks.

“If banks don’t come up with ways to innovate, they die,” Petrou told MarketWatch yesterday. “Then consumers are left to do their banking with nonbanks.”

Federal Financial Analytics, where Petrou is the managing director, is a Washington, D.C.-based consulting firm and Petrou is a highly regarded voice in the financial regulation space.

While Petrou acknowledges that online banking is the only alternative if traditional banks don’t innovate, she sees serious problems in fintech which she outlined in a paper published earlier this month, according to American Banker.

For instance, she wrote about the danger of a company like Amazon getting into banking and being able to charge individuals different amounts for the same item based on its knowledge of how much money the customer has. Or, the implementation of better banking policies for people who exercise and eat healthier. Petrou says this favors wealthier people with more time for exercise and greater access to more expensive, healthier food.

“I am all for technology,” Petrou said. “But I spent a lot of time when I was a student at MIT studying tech policy, and there is one after another example of seemingly promising technologies with terrible, unintended consequences.”

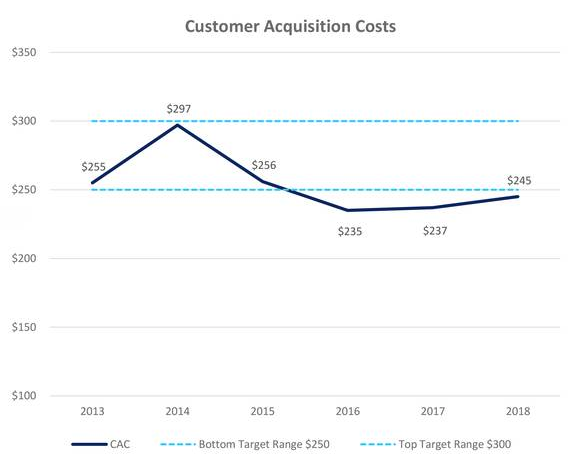

How Much Elevate Spends to Acquire Customers

February 11, 2019How much does a non-prime consumer lender spend to acquire a borrower? According to Elevate’s Q4 earnings report, the company spent less than $150 per borrower to originate $31 million in loans towards their partnership with FinWise Bank. Overall, however, their cost of acquisition has hovered below $245.

Elevate’s direct mail channels made up 42% of acquisitions in 2018. That’s down from 54% in 2017. In the company’s earnings call, Elevate CEO Ken Rees said of the decreasing reliance on direct mail, “we believe this sets us up for strong future growth through these expanded channels.”

Elevate offers three products to non-prime customers: RISE, a state-licensed online lender that offers up to $5,000 in unsecured installment loans and lines of credit, Elastic, a bank-issued line of credit, and Sunny, a short-term loan product for customers in the UK. RISE and Elastic serve the US market.

Separately, Elevate reported $787 million in revenue for 2018, an increase of $113 million, or 17%, compared to 2017’s full-year revenue of $673 million.

Liquid FSI to Augment Healthcare Lending Platform with Blockchain Technology

February 11, 2019Liquid FSI announced today that it has entered into an agreement with TVS Next, an IT company, to build a blockchain platform to enhance its healthcare lending capabilities.

“Our Blockchain solution solves a myriad of issues including the privacy of provider [typically medical office], biller, payer, patient and bank data,” said Liquid FSI President and CEO, Frank Capozza. “Blockchain will also support our on-demand payment offering Convert2Pay…and we believe that TVS Next has the depth of resources we need to serve the $3.6 trillion healthcare market.”

The is an improvement of Liquid FSI’s Convert2Pay offering which can provide cash in as little as 24 hours to medical offices with insurance claims.

“Instead of waiting 45 days or 60 days to get paid, [the doctor] can get paid in 24 hours because we’ve done all the analytics, and we’re scored [the medical practice] on a scale from 1 to 10,” Capozza said. “If he’s a solid performer and he’s using our platform to level out his peaks and valleys in cash flow, we see all of that in the system.”

The new use of blockchain, a decentralized system that logs information anonymously into a ledger, should give increased confidence to Liquid FSI’s medical office clients, Capozza said.

Capozza said he has excellent relationships with a number of brokers who send him clients. But as evidence of the privacy problem, he said that he will occasionally get applications from some brokers that include patient names, addresses, and social security numbers. This information isn’t stolen, but can be released by a medical practice if it needs money urgently. Capozza said he would rather see less of this and is confident that the new blockchain technology will significantly reduce any privacy lapses.

“It’s the same product, but it’s improving the privacy for everyone involved,” he said.

He also said that they are in talks with three banks that will be able fund on the Convert2Pay platform and will be comforted by the increased privacy afforded by the blockchain technology to be used by Liquid FSI. Capozza said Liquid FSI has plans to offer credit to doctors and sees itself as a VISA for the healthcare industry.

Aside from working with broker partners, Liquid FSI also works with medical billing companies to obtain clients, like pediatrician or dentist offices. Founded in 2014, the company has made some key recruitments to its overall team over the past year, including the addition of Barry Blecherman, professor of Finance and Risk Engineering at the NYU Tandon School, to its Board of Advisors.

Why the Human Connection is Still Important in Debt Recovery

February 10, 2019 The CEOs and lawyers for debt recovery companies, particularly those in the commercial space, say that speaking to merchants over the phone is the best way to collect money for their clients. At New York-based Empire Recovery, Managing Attorney Steven Zakharyayev told deBanked that they call this “soft collection.”

The CEOs and lawyers for debt recovery companies, particularly those in the commercial space, say that speaking to merchants over the phone is the best way to collect money for their clients. At New York-based Empire Recovery, Managing Attorney Steven Zakharyayev told deBanked that they call this “soft collection.”

“Soft collection is probably the most effective way of collecting,” Zakharyayev said. “You can tie up [the merchant’s] business and freeze their accounts. That’ll bring them to the table. But the human interaction – negotiating with them – that’s where the deals are made and that’s how these accounts are ultimately repaid.”

Most of of the debt collection companies we spoke to have an in-house lawyer that can file a lawsuit against the merchant while also using “soft collection” to get to a settlement. But Dedicated Commercial Recovery, a Minnesota-based recovery firm led by Shawn Smith, who is not an attorney, sees itself as the step before attorneys get involved.

“We use a rapport-based collections approach,” Smith said. “We try to get to the real reasons why the customers are ignoring our client and come up with a viable solution for repayment.”

Merchants in default are usually not doing very well if they’re on a collections list.

“These [merchants] get pretty beat up by the time they get to us, so the more you can connect with [them] on a personal level, the better.”

Doug Robinson, the attorney at New York-based RTR Recovery, echoed this.

“There’s a story behind every default,” Robinson said. “Most of the merchants want to pay, so they appreciate someone reaching out and saying ‘What’s the matter?’”

Robinson said that he personally calls and emails every merchant and that they have a pretty high response rate with this simple technique. He said that the voicemails of the merchants are often full, but that they will usually respond to his email, where he explains that ignoring him will only escalate the problem.

If the merchant responds and engages with him, Robinson said he can create a payment plan with them, together with his client, that can reduce the merchant’s payments, stop payments temporarily, or change payments from daily to weekly.

Meanwhile, Houston, Texas-based AMA Recovery is often brought on after a collections agency has already unsuccessfully tried to get a merchant to pay. AMA Recovery’s Vice President of Legal Operations Kimberly Raphaeli said that a demand letter is always sent to the merchant, in addition to the use of secret shoppers or contacting neighboring stores to determine if a store is really out of business if the merchant says it is.

Even with these more aggressive tactics, Raphaeli said that calling is still critical. She said that they will move files around the office, noting that merchants respond differently to different personality types. Raphaeli said that by the time a file gets to AMA Recovery, the majority of the merchants have simply decided to stop paying and about 30% are legitimately no longer in business.

Having a merchant go out of business is never a good outcome for a collector.

“You want to keep them in business,” Zakharyayev said. “[…] You want to make a relationship with them where you leave them enough to stay in business but you collect enough that your client is satisfied and they get paid in full.”

While these collection companies all agreed that communicating – one human being to another – is the best way to approach recovery, that doesn’t mean that technology is thrown out the window. None of the companies deBanked spoke to said they use autodialing, but Smith said he uses texting and email technology to make contacting merchants more efficient.

Mark LeFevre, CEO of Kearns, Brinen & Monaghan, a collections firm with offices in Delaware and South Carolina, agreed that technology makes the collections process more efficient.

“It’s important that you combine technology with the [human touch] to be most effective,” LeFevre said. “The technology will allow us to get the client to show what we can do, how we do it and so forth. But once that relationship is gained…we must talk with their customers.”

Why RapidAdvance Is Now Rapid Finance

February 7, 2019 RapidAdvance has officially changed its name to Rapid Finance.

RapidAdvance has officially changed its name to Rapid Finance.

“The term ‘advance’ is out of favor these days,” said founder and Chairman of Rapid Finance Jeremy Brown. “It also doesn’t reflect who we are as a company or what our brand is. We put our clients in a variety of different financing solutions including factoring, term loans and equipment leasing. ‘Advance’ is very narrow and old school. ‘Finance’ represents where the company has evolved to and where we’re going.”

The company’s logo is also new, but Brown said that they purposely retained the same color scheme to make the change as seamless as possible.

“Before we had an arrow through the word ‘rapid,’” Brown said. “I think the three squares [in the new logo] represent an arrow head so that there’s continuity with the old logo.”

Consistent with the rationale for the company’s name change, Brown said that their business is about 85% term loans and only 15% merchant cash advance, healthcare cash advance and bridge loans. Through partners, Rapid Finance also provides their customers with access to SBA loans, factoring, asset based loans, commercial real estate and lines of credit. By the second quarter of this year, Brown expects that they will offer their own line of credit product.

Rapid Finance is broadly diversified by business type, according to Brown. He said that no business category accounts for more than 25% of their business. As for acquiring new business, Brown said that 60% comes from partners/brokers and 40% comes from their internal direct marketing efforts.

Brown said that Rapid Finance, which employs about 200 people, has hired about 25 over the last six months. Most of the hires were in the technology and sales departments, both internal sales and sales reps who work with ISO partners. He also said they expect to fund between $550 and $600 million this year.

Founded in 2005, the company’s employees are divided between its headquarters in Bethesda, MD and another office in Detroit, MI, which houses Rapid Finance’s direct sales and marketing teams.

New Jersey MCA & Business Loan Disclosure Bill Update (S2262)

February 6, 2019 Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

- the total dollar costs to be charged to a small business concern, assuming the small business concern delivers all purchased receivables to providers at the time they are generated or at a mutually agreed upon time, and all required fees and charges that are paid by the small business concern and that cannot be avoided by the small business concern;

- the amount financed, which shall mean the advance amount less any prepaid finance charges; and

- for a cash advance that calculates repayment costs dependent on the small business concern’s future receivables, the estimated annual percentage rate, provided as a range, with at least three different repayment times provided and a narrative explanation of how each rate was derived. Any estimated annual percentage rate is to be calculated using a projected sales volume that is based on the small business concern’s average historical sales or the sales projections relied on by the provider in underwriting the cash advance; or

- for a cash advance that calculates repayment costs as a fixed payment, the annual percentage rate, expressed as a nominal yearly rate, inclusive of any fees and finance charges.

Brokers would also be required to provide uniform fee disclosures to both the small business owner and lender or MCA funding provider in a document separate from the funding contract before a small business consummates a loan or MCA transaction.

Previously, the bill defined merchant cash advances as loans. The latest draft updated the definition to mean a financing option that allows a small business concern to sell all or a portion of its future sales collections or other future revenues in exchange for an immediate payment. It refers to this as an asset-based transaction.

You can follow the bill’s updates and read the latest drafts here.

S2262 was originally introduced 11 months ago in March 2018.

Home Improvement Loans on the Rise

February 6, 2019 A story this week in American Banker suggested that popular home improvement TV shows like HGTV’s “Fixer Upper,” “Love It or List It” and “Property Brothers” are creating a growing demand for home renovation, and hence, home renovation loans.

A story this week in American Banker suggested that popular home improvement TV shows like HGTV’s “Fixer Upper,” “Love It or List It” and “Property Brothers” are creating a growing demand for home renovation, and hence, home renovation loans.

Nielsen rating data shows that the combined viewership of the three aforementioned shows on the HGTV (Home and Garden Television) channel rose from 5.4 million viewers in 2014 to 8.6 million viewers in 2018.

deBanked spoke to Michael Funderburk, Director of Personal Loans at LendingTree, which encompasses home improvement loans, and he said that he has seen an increase in home improvement loan volume at LendingTree. But he doesn’t necessarily think there is a correlation to the popularity of the HGTV shows.

Funderburk said people are likely to renovate their home as opposed to buy a new one for a few reasons. One is that new home supply hasn’t quite caught up with demand yet, which is causing home prices to increase. Secondly, mortgage rates are higher than they have been for the last several years.

“Despite the fact that the economy is doing well, people are in better financial positions, have better income, people are thinking ‘What do I do with this [money]? I don’t necessarily [have enough] to move homes, but maybe I can renovate my current home?”

Spending on home remodelling has steadily increased over the last two years from approximately $295 billion at the start of 2017 to nearly $340 billion at the end 2018, according to a study from the Joint Center for Housing Studies of Harvard University.

According to the American Banker story, Doug Duncan, Chief Economist at Fannie Mae, said that there are two reasons why home remodelling spending (and resulting borrowing) is increasing.

“Baby boomers [have] said they intend to age in place,” Duncan said. “As you get older, it requires some accommodations, things like door handles, potential wheelchair ramps, bars in the shower, that type of thing.”

The other reason for increased home improvement, he said, is that Generation X (those born between 1965 and 1979) will also be remodelling their homes.

“Gen Xers maybe have kids in junior high or high school and would like to move up,” Duncan said. “But there simply isn’t inventory, and it’s expensive if they’re in an urban center and in a school district they like.”

Whether it’s because someone saw a beautiful new den built on the “Property Brothers,” or they’re just too settled in to move, the market for the home improvement loans seems to be growing and is likely to continue. And it’s possible that small businesses may seek similar loans to freshen up their stores rather than find a new space.