Archive for 2018

When to Hire a Collection Company

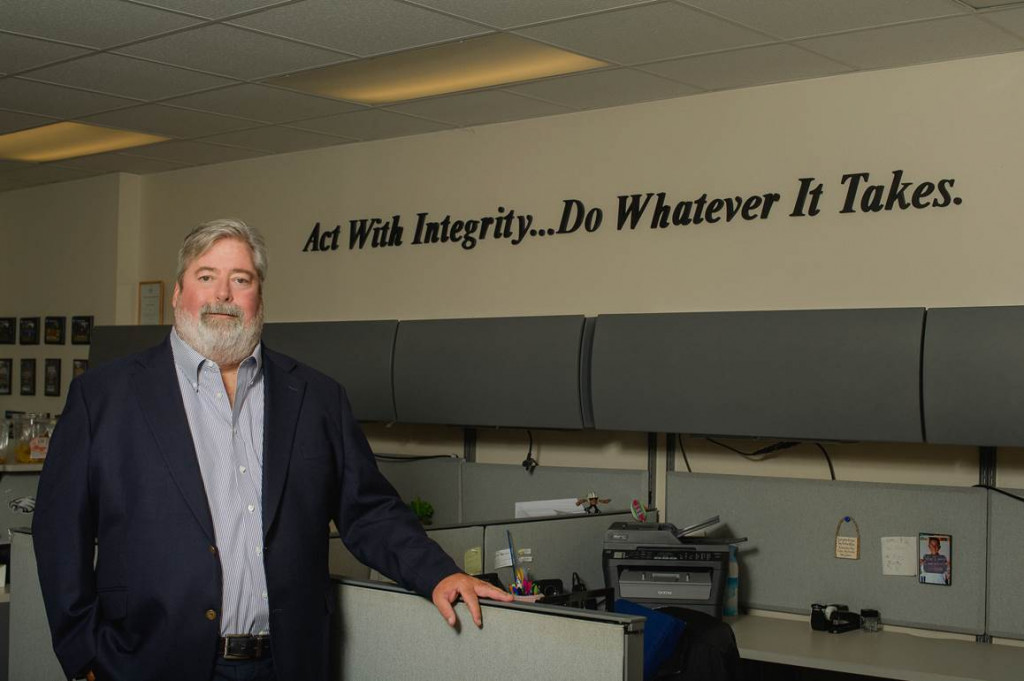

June 19, 2018

There is no rule telling a funding company at what point it should seek the help of a collection company when a client defaults on an agreement. That’s entirely up to the funding company. Some have in-house collection teams while others don’t and some go slower to approach a collection agency than others.

At 6th Avenue Capital, CEO Christine Chang said that they generally don’t use collection agencies.

“When we started 6th Avenue Capital, we had a much heavier hand,” she said. Initially, they hired an in-house collections attorney, but found that it wasn’t a very collaborative approach.

“If the first call you get is from a lawyer, you’re not going to call them back,” Chang said.

Instead, they hired an in-house Head of Collections and Chang said that has proven to be more effective.

“Now, it’s more like a call from Amanda who says ‘Mr. Smith, I see you missed a payment or two….tell us your situation and how can we help,” Chang said.

The company will occasionally hire a third party for collections, but after they have exhausted all efforts internally.

But collection agencies in the industry say that they work with some of the biggest funding companies, and at all stages of the process.

Mark LeFevre, CEO of collections firm Kearns, Brinen and Monaghan (KBM), said that his clients are not only among the top players but he also works with ISOs who have just started funding companies.

“The ones that recognize the problem early, have a better return,” he said. “The ones that kick the can down the road get a lesser return on the dollar.”

As for when LeFevre’s clients send their defaulted merchants to KBM, it varies, he said. He has one client that will send him accounts after 15 days while others will wait 90 to 120 days. He generally won’t take on defaulted accounts after 120 days, or at least will sit down with clients like these to discuss strategy.

Anh Regent, CEO of the MCA collection company, AMA Recovery Group, spoke about the value of having a merchant hear from a third party.

“There’s only so much you can do in house,” Regent said. “You need another voice. [And] when you send it to collections, the price of poker has just gone up,” meaning that the merchant feels a lot more pressure to pay.

Like KBM, Regent said that his MCA clients vary in size, from companies financing $500,000 a month to those financing $25 million a month.

Woman Arrested in Connection With Finance Company Data Theft

June 19, 2018 A woman was arrested in the Bronx this morning and charged with felony computer-related theft. The individual, whose name deBanked is not releasing until more information is known, was reportedly stealing customer data from Yellowstone Capital despite not being employed there. The photo shows police officers escorting her out from her home.

A woman was arrested in the Bronx this morning and charged with felony computer-related theft. The individual, whose name deBanked is not releasing until more information is known, was reportedly stealing customer data from Yellowstone Capital despite not being employed there. The photo shows police officers escorting her out from her home.

She is the third person to be arrested for stealing data from Yellowstone Capital in the last nine months but she’s the first that was not actually working there at the time.

Yellowstone Capital is arguably the largest merchant cash advance company in the country, according to deBanked’s leaderboard. The companies ranked ahead of them are lending companies, not MCA.

Collector Says “No” to Debt Settlement Companies That Want His Data

June 19, 2018

Debt settlement companies often find their leads by scouring through UCC filings, or publicly available forms that a creditor files to give notice that it may have rights to the property of a debtor. In the case of a small business, perhaps the refrigerators in a restaurant.

“[Looking through UCC filings] is a way of getting access to businesses that obviously owe somebody some money for their business,” said Shawn Smith, founder and CEO of Dedicated Commercial Recovery, a commercial collections company in Roseville, Minnesota.

But Smith told deBanked about another approach that debt settlement companies have taken to obtain leads of struggling businesses. He said they come to him.

“Who has a ton of accounts of struggling business owners?” Smith said. “Debt collection agencies that are working on behalf of funding sources. So [we] have like a list of all lists.”

Smith said that he gets approached by debt settlement companies looking for the contact information of struggling companies.

He always says “no.”

“They’re coming to me and saying ‘Hey, you know, for any merchant you send us that’s struggling, if we start working with them to help settle their debts, we will give you a large portion of the fee we make on settling that debt,’” Smith said. “And we of course would never do that.”

Dedicated works in two areas of collections: merchant cash advance and equipment leasing. In both cases, its goal is to recoup money for its clients, either merchant cash advance companies or equipment leasing companies.

Unlike this arrangement, a debt settlement company is not hired by a funding company. Instead, according to Smith, the debt settlement company searches for a struggling company, instructs the merchant to stop paying the funder and then approaches the funder with a settlement deal for often a fraction of what the funder is entitled to under the agreed upon deal. Smith said that settlement companies almost always propose to the funder: 20 percent of the value of the deal over five years.

Smith said he does work with debt settlement companies if they approach him representing a small business that can’t pay its bills, as long as what’s offered is within the range of what the funding company client would accept. Otherwise it’s a no-go. While Smith doesn’t share the names of struggling small businesses in exchange for kickbacks in the event of repayment, he’s convinced that this happens as he continues to be approached.

Founded by Smith in 2015, Dedicated has a staff of 18.

Agency Finds Some SBA Loan Lenders in Violation of Regulation

June 18, 2018

The Small Business Administration (SBA) has a regulation for SBA loan lenders, called the “Credit Not Available Elsewhere” requirement, that requires lenders to ensure that their borrower clients are unable to obtain reasonable credit elsewhere.

According to a report published this month by the Government Accountability Office (GAO), over 40 percent of the SBA loan lender reviews in 2016 showed noncompliance with this requirement.

“SBA provides business loan assistance only to applicants for whom the desired credit is not otherwise available on reasonable terms from non-Federal sources,” the regulation reads.

According to a blog post published last year by Janet M. Dery, a partner at Starfield & Smith who specializes in commercial lending, the SBA’s credit elsewhere test is a very significant part of the SBA 7(a) loan program.

“Failure to comply with the SBA’s credit elsewhere requirements may subject a lender to a denial of the SBA guaranty as well as a possible enforcement action by the Office of Credit Risk Management,” Dery wrote.

Furthermore, she writes that in order to comply with the SBA’s credit elsewhere requirements, which appear on pages 83-84 of SOP 50 10 5(I), “[t]he lender must determine that: (a) The Small Business Applicant is unable to obtain the loan on reasonable terms without a Federal government guaranty, and (b) Some or the entire loan is not available from any of the following sources: i. Non-Federal sources; or ii. The resources of the applicant business.”

It’s Back to Business For Alternative Funding in Puerto Rico

June 15, 2018

Last year, alternative funding in Puerto Rico ground to a halt after the island was ravaged by two devastating hurricanes in close proximity. Now, however, the alternative funding business in Puerto Rico is getting its second wind, after a several-month hiatus.

Puerto Rico got lashed by high winds and rain from Hurricane Irma in early September 2017, causing large-scale power outages and damage. Then, about two weeks later, Hurricane Maria hit the island square on, causing even more catastrophic destruction. Millions were without power for months (thousands still are), homes were destroyed, multiple lives were lost, businesses were decimated and the island’s already shaky economy teetered on the brink of disaster.

More than half a year later, residents are still trying to pick up the pieces of the epic humanitarian crisis. Hurricane Maria caused an estimated $90 billion in damage, according to the National Hurricane Center, making it the costliest hurricane on record to strike Puerto Rico and the U.S. Virgin Islands. The hurricane knocked out 80 percent of Puerto Rico’s power lines and destroyed its generators. Even months later, the lives of many residents are still in disarray as they wait desperately for insurance payments to materialize and get back to a semblance of their former lives. The island faces additional challenge—and uncertainty— with another hurricane season just around the corner.

In the midst of this turmoil, however, there’s a glimmer of hope for the budding alternative funding sector. Some businesses are once again seeking funds to rebuild or expand, and alternative funders are once again dipping their toes into the Puerto Rican market—albeit somewhat slowly. While some funders have exited the Puerto Rican alternative lending market, other new entrants are starting to stake a claim, citing an expected uptick in economic development that tends to follow natural disasters. Some funders also see Puerto Rico as a sweet spot because the market isn’t as mature as the U.S. and competition from other alternative funders is scant. Banks on the island aren’t always willing to provide businesses there with much- needed funds, so opportunities for non-bank funders are considered plentiful.

Businesses struggling to rebuild from the storms need more help than ever before, says Sonia Alvelo, president of Latin Financial LLC, an ISO that has been arranging funding for business owners in Puerto Rico for three years. “There is no doubt that Puerto Rico has a long, hard road ahead,” she says. But “I can assure you the entrepreneurial spirit is alive and well,” she says.

Latin Financial and other ISOs and funders are back to business—courting merchants and trying to help them get back on their feet. In December, Latin Financial processed its first renewal since Maria; in January it funded its first new client since September. Latin Financial continues to arrange funding of between $500k and $1 million per month on average in Puerto Rico, after some hurricane-related downtime.

“The storm destroyed a lot, but it didn’t set the small business drive back. They’re still pushing hard and really trying to maintain and grow business,” says Brendan P. Lynch, business partner and fiancé to Latin Financial’s Alvelo.

Greenbox Capital in Miami Gardens, Fla., an early entrant to the Puerto Rican alternative funding market, has also returned to funding small businesses on the island after a few-month hiatus. The company put off new deals right before Maria hit, and as a goodwill measure suspended the payments of existing customers for 90 days. Given the extension, almost all customers were able to stay on track and the firm suffered very few losses, says Jordan Fein, the company’s chief executive. Greenbox began funding again in January, he says.

Greenbox Capital in Miami Gardens, Fla., an early entrant to the Puerto Rican alternative funding market, has also returned to funding small businesses on the island after a few-month hiatus. The company put off new deals right before Maria hit, and as a goodwill measure suspended the payments of existing customers for 90 days. Given the extension, almost all customers were able to stay on track and the firm suffered very few losses, says Jordan Fein, the company’s chief executive. Greenbox began funding again in January, he says.

To be sure, it’s not exactly business as usual, since many businesses in Puerto Rico are still struggling, Fein says. While the situation should continue to improve, it will take time for the economy and businesses to fully recover, he says.

“They’ve come a long way since September, but they still aren’t fully back. We’re not seeing the same type of submissions that we saw before,” Fein says. Nonetheless, Fein remains positive about the market’s long-term prospects. “I think they are going to come back stronger, I really do,” he says.

To be sure, not all funders are interested the Puerto Rican market. Ripe with political uncertainty and economic instability, Puerto Rico already posed challenges that made many funders hesitant to do business there. The devastation wrought by Irma and Maria complicated matters further, and some funders pulled out of the market completely.

For others, however, the market’s still an opportune one, albeit not as stable as the U.S. market. Certainly, there are reasons for alternative funders to be optimistic. Despite its recent troubles, Puerto Rico is still considered a growth market. What’s more, with new businesses popping up in the wake of the storms, new infrastructure being instituted and businesses anxious to bounce back even bigger and better than before, some funders are striking while the iron is hot.

“This is the right time, as the island is growing,” says Paul Boxer, chief marketing officer and vice president of business development at Quicksilver Capital, a New York-based small business funder. Quicksilver funded its first deal in Puerto Rico in late April.

The company had been mulling over the possibility of doing business in Puerto Rico when an actual funding prospect arose. The company decided to give it a shot, sensing a potentially viable business opportunity. Existing businesses are rebuilding after the hurricane, there’s plenty of new business development and there’s a pressing need for new infrastructure as Puerto Rico continues to recover from the devastation, Boxer says.

Accordingly, Boxer says his company is in the process of vetting additional funding opportunities in Puerto Rico and hopes to continue growing this business in what he says is a largely untapped market. “I see it as a positive addition to what we offer, and I see a lot more opportunity in the future,” Boxer predicts.

Triumph Business Capital Completes Acquisition of Factoring Assets

June 14, 2018Triumph Bancorp, Inc. (NASDAQ:TBK) recently announced the closing of the acquisition of the transportation factoring assets of Interstate Capital Corporation by Advance Business Capital, also known as Triumph Business Capital.

Triumph Business Capital is a wholly owned subsidiary of TBK Bank, SSB, which is a wholly owned subsidiary of Triumph Bancorp. The assets acquired include all of the accounts receivable and transportation factoring assets and operations of Interstate Capital Corporation (ICC) and certain of its affiliates. Following the closing [of ICC], the acquired operations will continue to be conducted under the ICC brand name.

Triumph initially announced its agreement to acquire the transportation factoring assets of ICC on April 9, 2018, but the acquisition was made final at the beginning of the month. Triumph Bancorp, Inc. is a financial holding company headquartered in Dallas, Texas, with a diversified line of community banking and commercial finance activities.

Reliant Funding is a Sponsor of deBanked CONNECT – San Diego

June 14, 2018Reliant Funding is a sponsor of deBanked CONNECT San Diego. The half-day event for funders, lenders, brokers and industry professionals is being held at the Andaz on October 4th!

Check out photos from deBanked’s past CONNECT event in Miami

National Funding is the Title Sponsor of deBanked CONNECT – San Diego

June 14, 2018National Funding has signed on as the title sponsor of deBanked CONNECT San Diego. The half-day event for funders, lenders, brokers and industry professionals is being held at the Andaz on October 4th!

Check out photos from deBanked’s past CONNECT event in Miami