Archive for 2018

ISO Pretending to be Funder May Be Sent to Jail

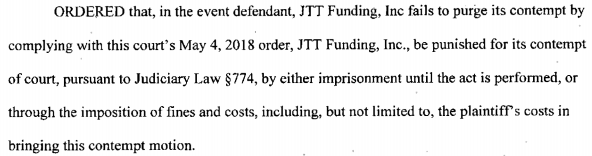

October 14, 2018A New York Supreme Court judge ordered on Thursday that Long Island-based ISO JTT Funding either be fined or sent to prison if it does not comply with a previous restraining order obtained by NYC-based funder Accel Capital.

Accel alleges that JTT funding has been impersonating it through correspondence and on contracts, a scheme that was outed when merchants claimed they had been duped into sending thousands of dollars upfront to JTT (disguised as Accel) to obtain a loan yet never received one. Accel responded by suing JTT and obtained a restraining order on default when the defendant failed to respond.

According to the Financial Times, JTT Funding is owned by Queens-born mixed martial arts fighter Jim “The Tyrant” Boudourakis. In his October 2017 interview with the publication, Boudourakis said, “There was a learning curve, going from being a fighter to a salesman. But I’m good with people.” FT also reported that his company had 18 full-time salespeople and was funding $4 – $5 million per month.

In an unrelated suit, JTT Funding is accused of forging a confession of judgment.

The Accel Capital suit can be found in the New York Supreme Court under Index Number: 153447/2018

The Broker: How Andy Savarese Changes Collars and Closes Deals

October 12, 2018 Title:

Title:

I’m the Managing Partner at JustiFi Capital, a brokerage in Farmingdale, Long Island. I started it September 2017 with my cousin, who’s the owner and my best friend. We do mostly MCA, but also some term loans.

His schedule:

I have a part-time/full-time job in the mornings. I work in sanitation for the town of Oyster Bay on Long Island. I typically wake up at around 3:37 a.m. I get into my yard at 4:15 a.m. and I go right into my route. My job is task completion. So the faster you work, the faster you get to go home. You get paid the same. I was fortunate to get on a fast truck, so I’m usually done between 7:45 a.m. and 9:30 a.m.

I go home, I take a quick shower, and I change my outfit. I go from blue collar to white collar. I get into the office around 10:30 a.m. and I start doing more of a mental hustle compared to a physical hustle.

At around 12:45 p.m., I take my lunch and I go to the gym for about 45 minutes. I get back to the office and I keep up the closing, the pitching, the selling, the prospecting. At around 5:30 p.m., I leave the office, I pick up my son from daycare, and since my wife works evenings, I take care of him at night until around 7:30 p.m., and get him ready for bed. The second he hits his crib, I hit my bed and I call it a day.

His background in the business:

About three years ago, I was driving oil trucks after sanitation, and my cousin, who is also my best friend, gave me a call. He knew I was breaking my butt all day. He had a friend that was starting his own ISO. So I did that for a year and I learned the industry. It didn’t really work out there, so I convinced my cousin to open up our own shop, which is JustiFi.

His process:

At JustiFi, we’ve been growing. We’re just grinding it out and things are going really well. We have four brokers and we keep it tight. We keep it small so that everybody is inundated with files and everybody’s making money and everybody’s happy. We don’t have any processors or chasers. We do it all on our own. We’re working the deal from beginning to end. My cousin has devised a pretty strategic marketing plan that inundates us with leads all day. I disperse them and I follow up with my guys and see how I can help. I overlook all of the closings and make sure that everything than can get worked is getting worked.

His biggest challenge as a broker:

A lot of people will say getting good leads and keeping your brokers happy. What I found is the most challenging part of being a broker in this industry is keeping a really level head and keeping your emotions out of the game. It’s a very tumultuous industry. One day, you could have 12 deals in the funding chute, the next day, your pipe could be dry. You could have a deal you think is going close and something happens on the funding call and it gets derailed. The point is that you’ve got to stay positive, you’ve got to stay confident, and you’ve got to roll with the punches. If not, you’re going to lose it and you’re going to get eaten alive. Because it’s a battlefield out there. You’ve got to keep your composure, no matter what the size of the deal. You’ve got to just keep pushing through. Because if not, you’re not going to make it.

His largest deal funded:

$250,000. And I made $38,000.

His advice for brokers:

When I go to close a good sized deal, or a tough deal, I don’t like to come off as a salesman. I’ll never do that. I’m going to come off as an advisor. I’m going to come off as a partner with you where I’m going to explain the ins and outs of the deal. I’m going to explain how it benefits you. I’ll never put on pressure or talk slang. I’m going to be a professional. You’ve got to kind of put yourself in [the merchant’s] shoes and you’ve got to see that it really makes sense for them. Because when it makes sense to you and it makes sense to them, you’re going to close the deal and you’re going to move forward.

But there are always deals that will never close, deals that you can’t sell. So you can’t be too hard on yourself. You’ve got to stay positive. You can’t beat yourself up if you don’t sell something. You’ve got to just do your best, stay neutral, and just talk to clients how you want to be talked to.

What he does to pump himself up for a deal:

If I know my day is bringing a big deal that I have to sell and I’m a little uneasy about it, I have an advantage. I’m on the back of a garbage truck all morning and I focus on what’s in store for me that day. If I have a big deal, I recite in my head [from the truck] how I’m going to report to my client. So when I get into the office, I dial up and I already know how the conversation is going to go. I have my rebuttals in my head, I have the direction, I have everything ready to go so that when I get on the call, I’m fully prepared.

Will you quit your morning job?

No. When my pension kicks in, I’ll leave. But I told myself the day I started this and the day I started seeing the return, “I’m never leaving sanitation. I won’t.” I made that promise to myself. There’s been days when I’ll have a five figure commission day and the next morning it’ll be pouring rain out, and I’ll say to myself, “Man, I just want to take the day off.” But no, I made a promise. I go in.

Why?

It keeps me grounded, it’s a stress relief. It’s what I am. It’s what I do.

Capital Stack Hit With Class Action Lawsuit

October 10, 2018A class action lawsuit brought by former employees of Capital Stack, LLC was filed in federal court on Tuesday for damages resulting from alleged labor law violations. David Rubin, Brian Stulman, eProdigy ACH, LLC, and eProdigy Operations, LLC are also among the named defendants. Capital Stack is a merchant cash advance company based in New York.

The 22-page complaint lays out seven claims including failure to pay the minimum wage required by New York Labor Law.

The suit can be downloaded here.

The case is 1:18-cv-09230 in New York Southern District Court.

Yoel Wagschal Becomes Last Chance Funding’s CFO

October 10, 2018

Yoel Wagschal, an accountant who specializes in servicing MCA funding companies, told deBanked today that he will now be the CFO for Last Chance Funding (LCF), which has been one of his clients for about five years. Wagschal said he will maintain his private accounting practice, spending half the week working for LCF and the other half running his own business, serving other clients, mostly in the MCA space.

“I always treated my clients like I was a part time CFO,” Wagschal said. “Yes, it’s a little different to be the officer of one particular company, and that’s why I feel it’s important to make this announcement so my clients or prospective clients know that I am an officer, officially, of Last Chance. You can either embrace it, or not.”

For those who might see this arrangement as a conflict of interest, he argued that this has essentially always been the case since he has two dozen MCA clients.

“If the accountant is honest and doesn’t exchange information from one client to another, his knowledge will only be better, and [the client] will gain from having an accountant with other clients in the same space.”

Wagschal said he believes that every company needs a CFO. And being a part-time, per diem CFO, largely in the MCA space, has been his niche for the past 15 to 20 years.

Already, Wagschal has eliminated some jobs in LCF’s accounting department by creating a more efficient system, he said. (No one was fired; a few employees were just moved elsewhere). Wagschal believes that many accounting departments are often too big and that great leadership actually frees up time for a company.

“If you have proper accounting procedures in your company, then the compliance and the reporting comes so easy, it’s a piece of cake,” Wagschal said.

LCF’s owner and CEO Andy Parker is very excited about Wagschal’s new role at the company.

“I have never come across a more talented accountant in the MCA space,” Parker said of Wagschal.

Parker said that since he co-founded the Long Island-based company in 2011, they have seen triple digit growth year after year.

“As we continue to grow, we really needed a serious level accountant and we’re glad Yoel accepted the position,” Parker said.

Wagschal’s introduction to the MCA industry was a dramatic one. As a forensic accountant, he had contacts with tax attorneys, one of whom introduced him to the owner of an MCA firm whose partner had made a really costly mistake. Instead of sending an agreed-upon $9,600 to a merchant, he accidentally added an extra zero to the end and $96,000 was sent to that merchant. In what Wagschal described as a “very intense” experience, Wagschal drove to the town where the merchant operated from and said he rescued the money within 48 hours of being contacted.

But beyond this initial Indiana Jones-esque introduction to the MCA industry, Wagschal said that he began to see a void.

“It was a very new industry. People were confused, and I saw an opening,” Wagschal said.

deBanked CONNECT San Diego PHOTOS

October 9, 2018

Ascentium Capital Hits Milestone

October 9, 2018Ascentium Capital announced yesterday that it had surpassed $2 billion in managed assets during the third quarter of this year. It also had a 22 percent increase in funded volume over the same period last year. Altogether, the company has provided businesses with over $4 billion.

“We had another strong quarter of growth with performance driven by the diversity of our equipment vendors and repeat business efforts,” said Ascentium Capital CEO Tom Depping. “Due to the strong demand for our offering, we continue to expand our direct sales division with recruitment efforts for our offices in Texas, California and New Hampshire as well as expansion of our vendor-specialized sales personnel in Arizona, Michigan and across the nation.”

As a direct lender, Ascentium Capital provides equipment financing, leasing and small business loans, among other products. Ascentium Capital is backed by investment firm Warburg Pincus LLC, among others, and is headquartered in Kingwood, Texas.

Fora Financial & Expansion Capital Group Partner with Ocrolus to Automate Underwriting Legwork

October 8, 2018

New York, NY — Ocrolus, the emerging leader in analyzing loan documents, today announced integrations with Fora Financial and Expansion Capital Group, two of the fastest-growing online small business lenders. Enabling quicker and more precise loan decisions, Ocrolus has seen rapid adoption since its debut in the small business lending world with flagship customer Strategic Funding Source in May 2017. Following its Series A round highlighted by QED Investors, Ocrolus is quickly growing its customer base and team with laser-focus on the lending space.

Ocrolus employs crowdsourcing and artificial intelligence to drive efficiencies in the origination process, from document collection to calculating credit model inputs. The Company’s simple API ingests and analyzes bank statements and other loan files, returning actionable data and risk analytics, with 99+% accuracy.

Fora Financial, one of the most prominent New York City-based online lenders, has partnered with Ocrolus to automate bank statement reviews, resulting in a faster, more accurate end-to-end underwriting workflow. The benefits of automation have become increasingly important as Fora Financial accelerated growth after its June 2018 acquisition of US Business Funding. Leveraging Ocrolus to parallelize underwriting tasks, Fora Financial is poised to eclipse $400 million in annual originations over the next year.

“We are excited to automate an additional step in our underwriting process that has historically been very laborious, requiring additional staffing as we grew originations,” said Dan Smith, Co-founder and President of Fora Financial. “As a tech-enabled SMB lender, we rely on our technology to achieve scale while delivering a frictionless process for small businesses to access capital.”

Expansion Capital Group (ECG), recently honored on the 2018 Inc. 5000 as one of the fastest-growing private companies in America, has also partnered with Ocrolus to enhance its underwriting process. ECG sought a loan automation partner to facilitate ambitious growth objectives while improving risk management capabilities. With Ocrolus now handling its document analysis work, ECG, who has grown 627% over the past three years, looks forward to scaling its operation to new heights, thanks to its leaner, technology-enabled infrastructure.

Herk Christie, Head of Operations at ECG says, “Using Ocrolus solutions, we have been able to create a lean, smart and tech-enabled underwriting infrastructure that focuses on quality without sacrificing speed. The level of data Ocrolus provides will continue to feed the growth of our statistical models, further benefiting our clients and partners alike.”

Growing beyond online small business lending, into online personal lending and traditional banking, Ocrolus has added a couple of prominent lending executives to its team. Matt Burton, former CEO of Orchard Platform has joined Ocrolus as a Board Advisor. Kevin Bailey, former Senior Advisor at the US Department of Treasury, has joined Ocrolus as Head of Growth.

As CEO of Orchard Platform (acquired by Kabbage), Matt Burton became a cornerstone of the online lending community. Orchard’s Online Lending Meetup events regularly brought together industry thought leaders from all over the world, helping to shape the next generation of financial services. As an Advisor to Ocrolus, Mr. Burton is continuing his mission to grow online lending into an efficient, transparent, and global financial market.

A former White House and Treasury official, Kevin Bailey brings more than fifteen years of experience as a financial services and public policy professional. Prior to joining Ocrolus, Kevin was the Director of Business Development & Capital Markets at CommonBond, a leading marketplace student lender. Mr. Bailey is a graduate of Rice University and the University of Chicago Booth School of Business. At Ocrolus, Mr. Bailey is leading growth efforts as the Company expands beyond its core online small business lending market, into online personal lending and traditional banking.

Visit www.ocrolus.com for more information.

About Ocrolus

Ocrolus is a RegTech company that automates data verification and analysis for bank statements and other loan documents. The Company analyzes e-statements, scans, and cell phone images of documents from any financial institution with over 99% accuracy, and rigorous process documentation. By replacing tedious, imperfect human audits with sharp, AI-driven analyses, Ocrolus modernizes financial review processes in lending with unprecedented speed and accuracy.

Media Inquiries:

media@ocrolus.com

Digital Mortgage Lender “Better” Goes Where No Fintechs Have Gone

October 8, 2018

One product noticeably absent from fintechs expanding into lending or banking is mortgage loans, but now a fintech startup is looking to disrupt the $13 trillion mortgage industry.

Eric Wilson is co-founder and head of operations at Better Mortgage, a New York-based digital mortgage lender. Wilson explained to deBanked:

“Our industry more than consumer lending is stuck in the pre-internet era and hasn’t been able to leverage the tools to make getting a mortgage feel as simple and as empowering as other products we’re used to consuming online. The industry was waiting for a company like ours to come along with the right skills and engineering staff.”

Better Mortgage is an end-to-end mortgage lender that matches investors interested in giving loans to a subset of consumers. “We take applications and compare with investors for the best price. Underwriting and communication with the borrower happen on the internet,” Wilson said.

The investors are large financial institutions that are in the business of buying mortgage loans.

“We are a direct lender. We originate mortgages. We don’t charge origination fees to customers. We make money when we sell those loans to the secondary market, whether it’s Fannie Mae or any one of our 28 partners,” said Paula Tuffin, Better Mortgage chief compliance officer and general counsel.

In addition to zero origination fees, Better has eliminated commissions. “For us, we believe you should be able to put your storefront online and have consumers find you. We don’t think it’s appropriate or necessary pay one individual to take $6,000 out of a $300,000 loan,” said Wilson.

Instead, Better relies on a team of loan consultants who are “full-time employees or better” who are incentivized to deliver a delightful customer experience,” said Wilson. This differs from the traditional broker model used by much of the industry. “We don’t deal with third-party mortgage brokers. This eliminates a lot of the potential for fraud and harm to investors,” he noted.

Pain Points

The “pain points,” he noted, tied to mortgage lending surpass that of personal or unsecured lending. For instance, greater amounts of data are needed for loans of this size, and there’s the complex and intensive process of risk underwriting, all of which is exacerbated by heavy regulation.

Unlike some of its fintech peers, Better Mortgage has no interest in pursuing an OCC special- purpose national bank charter, or fintech charter.

Wilson is a millennial who had a front-row seat to the mortgage crisis and all of the hardship that fell on consumers. “It was a result of irresponsible lending practices,” said Wilson, “and a failure by regulators to keep lenders in check. So to that end, we are champions of post-crisis Dodd Frank-era consumer protection regulation.”

While operating under a single regulator across all 50 states would streamline the process for Better, it would come at the high price of innovation. “It comes with some pretty hefty strings attached. That regulatory environment is often so challenging to navigate or requirements so onerous … that I would be hesitant to go head-first into a program like this,” said Wilson.

As a result, Better incurs the cost of taking a state-by-state approach, a burden that Wilson says the company is happy to bear: “If we were to pivot and get a bank charter issued by the OCC, we could transact in 50 states overnight. But our ability to innovate evaporates in the process.”

Better is licensed in 19 states and is making an expansion push in which it plans to operate in all 50 states in the first half of 2019. The minimum FICO score for a Better conforming mortgage product is 620.

“By and large, the market is shallow in the application of technology. We’re a tech company first and we acquired a mortgage company as opposed to being a mortgage company learning about tech. This gives us a fundamental advantage in the way we think about problems,” said Wilson.