Archive for 2017

New York’s Proposed Budget Slips In Sweeping Regulation of Non-bank Business Lending and Finance

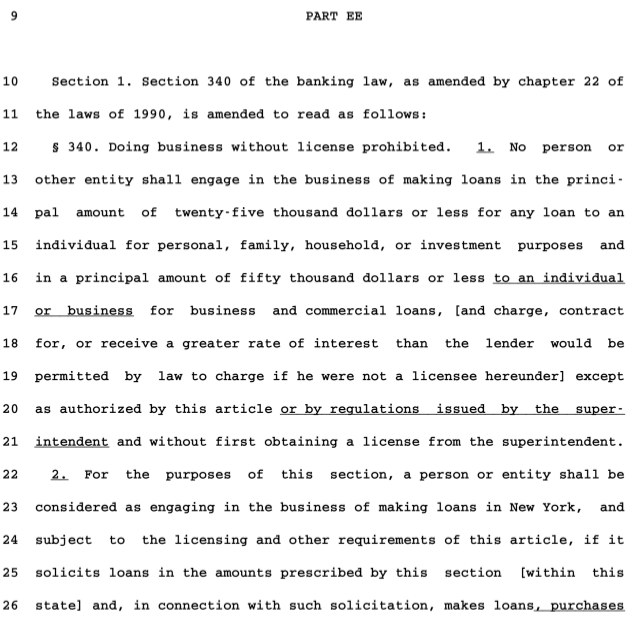

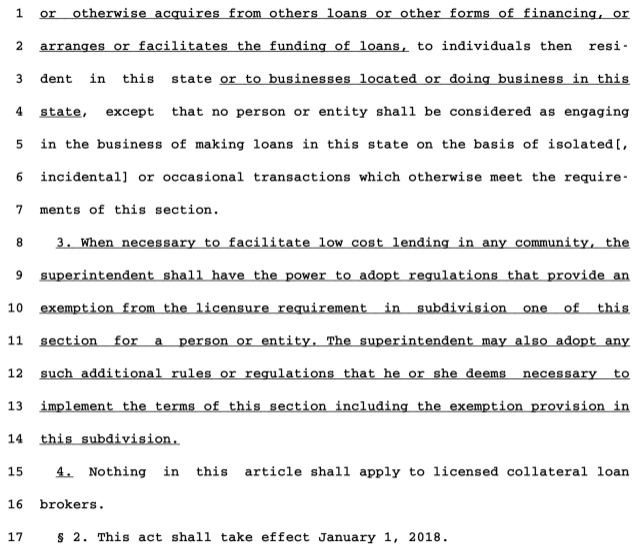

January 28, 2017In New York, Governor Cuomo’s 309-page budget proposal includes a handful of sentences tucked in towards the end (Part EE) that would revise Section 340 of the state’s banking law. And the implications are broad, given that it calls for any person or entity involved in the soliciting, arranging or facilitation of business and consumer loans or other forms of financing to be licensed in order to engage in such activity. It appears that MCA companies as well as business loan brokers and ISOs would be directly impacted.

If it passes, the regulator tasked with overseeing that would be the New York Department of Financial Services. It would be effective January, 2018.

For consumer loans, it applies to loans $25,000 and under. For business financing, $50,000 and under.

Biz2Credit – Citigroup Small Business Loan Partnership Spotted

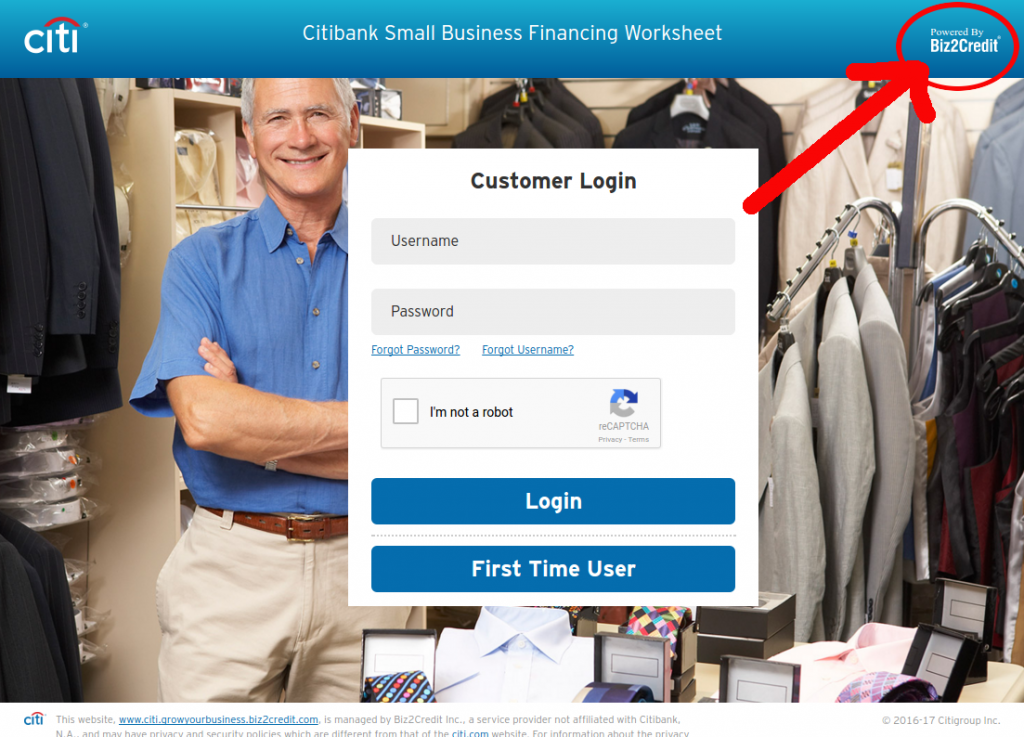

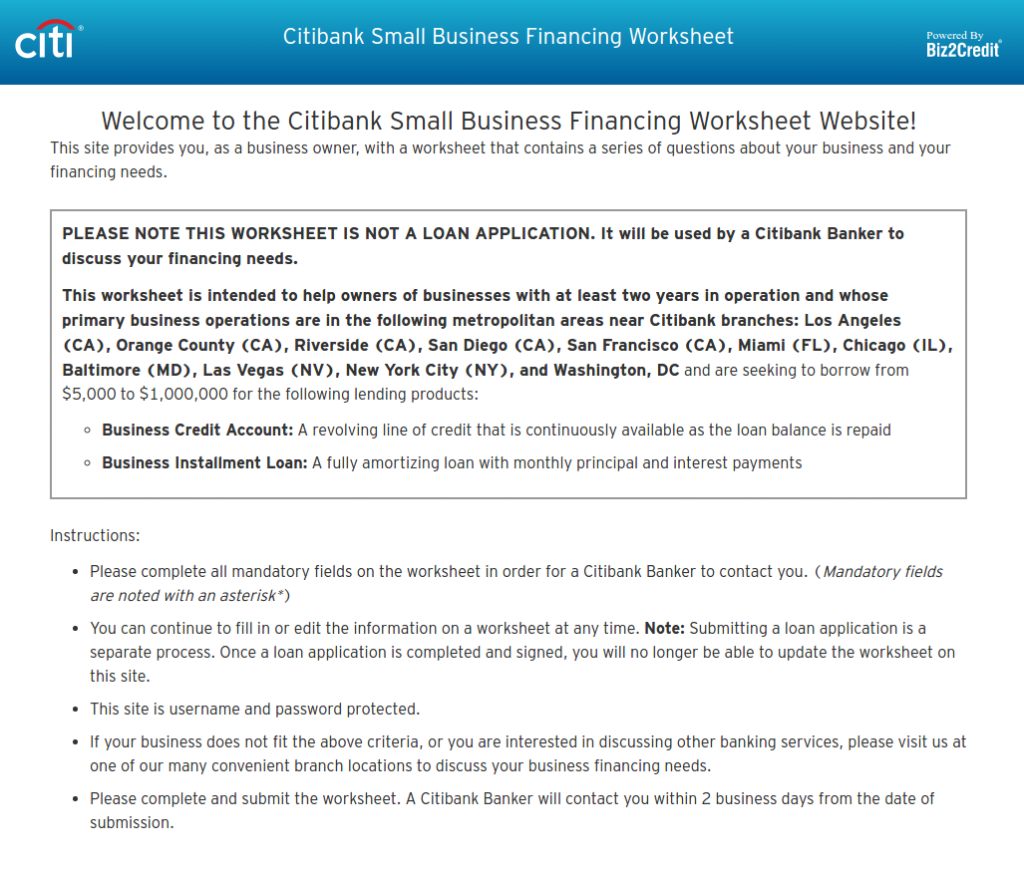

January 27, 2017Business Insider revealed that Biz2credit and Citigroup have quietly partnered up on a website to make small business loans up to $1 million. There was no actual link to it, so we’ve found it ourselves.

The link appears in several areas of Citi’s website under the small business finance category and that brings you here:

When you go to register, a page pops up insisting that this isn’t a loan application, but rather just a “worksheet” to have a banker from Citi call you within 2 days. “It will be used by a Citibank Banker to discuss your financing needs,” it reads.

The worksheet asks for very basic information such as name, business name, address, annual revenue, and financing requested.

If this doesn’t sound overly advanced, perhaps that’s why it’s being kept on the down low. According to Business Insider, Biz2credit CEO Rohit Arora said they have chosen not to publicize the effort because it’s in the very early stages.

The cat’s out of the bag now…

If a Bank Made the Loan in California, It Doesn’t Matter What Happened Next, Federal Court Holds

January 27, 2017There’s no reason to examine whether a party intended to enter into a usurious loan if there is a constitutional exemption that permitted the lender to make the loan in the first place, a federal court in California’s central district ruled. In Jamie Beechum et al. v. Navient Solutions, Inc. et al, a student loan borrower argued that loans made by Stillwater National Bank and Trust Company, are a sham because the defendants who bought the loans from Stillwater (who were not a bank) originated, underwrote, funded, and bore the risk of loss on the loans.

Beechum asked the court to examine the substance and intent of the agreements between the bank and the defendants, which they claim were designed specifically to evade state usury laws. The court did not believe it was necessary to look beyond California’s constitutional exemption since both plaintiff and defendant agreed that Stillwater Bank was the lender. The complaint was therefore dismissed.

As a secondary defense, defendants had also contended that as a national bank, Stillwater was also exempt from state usury laws under the National Bank Act, but the court did not even have to consider that to arrive at their conclusion.

A good analysis of the case (including why buying a loan from a bank differs from buying a loan from a tribe) was written in Leasing News by Tom McCurnin, a partner at Barton, Klugman & Oetting in Los Angeles, California.

Introducing LendingRobot Series: One-Stop Investing in Alternative Lending

January 26, 2017January 26, 2017 – Seattle, WA – LendingRobot, the first robo-advisor for Alternative Lending built for individual investors, announced today the launch of robo-fund LendingRobot Series. Designed as an alternative to traditional fixed income investments, LendingRobot Series is a one-stop solution that combines cloud-based investment automation, fully transparent fund secured by Blockchain technology and sophisticated machine learning algorithms to provide superior, predictable returns uncorrelated to stock market performance.

LendingRobot Series is a unique combination of a robo-advisor and an investment fund, created as one-stop solution for accredited investors looking for a way to easily invest in consumer, small business or real-estate loans diversified across multiple ‘peer lending’ origination platforms.

“Alternative lending proved to return excellent performance and with new origination platforms growing quickly comes the opportunity to diversify further. But fragmentation makes investing even more complex for individual investors” said Emmanuel Marot, CEO of LendingRobot.

Unlike a traditional fund, LendingRobot Series improves liquidity, is flexible with regards to loan selection, and 100% transparent. Investors decide what kind of risk and time horizon they want, and LendingRobot automatically manages their investments.

Hedge Funds typically charge management fees of 2% plus 20% of performance, plus obscure or unlimited fund expenses, which makes their expense ratio disproportionate to fixed income returns. In contrast with traditional investment firms, LendingRobot Series only charges 1.00% of assets under management, and caps fund expenses at 0.59%.

“Turmoil within the past twelve months among some of the largest origination platforms showed that ‘platform risk’ is real, and left many clients increasingly worried about investing only in unsecured consumer loans despite the fact that the returns have remained steady,” continued Mr. Marot. “All investors would be well served by diversifying into multiple marketplaces, but that process is tedious, complicated, and requires a high degree of domain expertise to accomplish correctly. That’s why we’ve created LendingRobot Series: to provide investors that understand the value of investing in Alternative Lending with the confidence that comes from intelligent automation, easy liquidity, and complete transparency.”

LendingRobot manages investments across four different Series, with target maturity going from 20 to 36 months, and net returns up to 9.66%. Investor’s money is converted in Units of ownership in these Series, that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases. LendingRobot publishes every week a detailed ledger of its holdings, down to the value and individual payments made by each note.

A ‘Hash code’ signature of the ledger is integrated in the subsequent versions as well as notarized in Ethereum’s Blockchain to ensure the data is tamper-proof.

To ensure maximum safety, assets are hold in a bankruptcy protection vehicle, with no other liabilities than its investors.

Investors willing to cash simply flip a switch on the LendingRobot website to start redeeming their Units on a weekly basis. Between 33% and 100% of loan payments are distributed in priority for redemption, which means that under normal circumstances investors should be able to cash out entirely in less than 3 weeks.

Investors interested in learning more about LendingRobot Series can visit www.lendingrobot.com/series.

About LendingRobot:

LendingRobot is a fully automated investment service for alternative lending platforms including Lending Club, Prosper and Funding Circle. After signing up for a LendingRobot account, investors select their risk tolerance and enable LendingRobot to instantly make investments on their behalf. Based in Seattle, Washington, LendingRobot serves 6,500 clients totaling over $120M in assets.

This So-Hot Robot Is Launching a Marketplace Lending Hedge Fund

January 26, 2017 LendingRobot has come a very long way since I first connected with them two years ago. Back then, CEO Emmanuel Marot was simplifying access to marketplace lending for individual investors by automating the decisions and executions. A year later, they were the first in the industry to introduce that technology via a mobile app. As someone who has used their service for a long time, one thing was always the same, the company helped you invest and monitor performance but they didn’t have custody of the actual money.

LendingRobot has come a very long way since I first connected with them two years ago. Back then, CEO Emmanuel Marot was simplifying access to marketplace lending for individual investors by automating the decisions and executions. A year later, they were the first in the industry to introduce that technology via a mobile app. As someone who has used their service for a long time, one thing was always the same, the company helped you invest and monitor performance but they didn’t have custody of the actual money.

That’s all changing with the announcement of their new hedge fund (“LendingRobot Series“), which will actually be separate and only open to accredited investors. The fund is managed by LendingRobot’s robo-advisor technology which scores, invests, and even manages secondary market activity without any need for human advisors. Basically the robots are doing the heavy lifting and they’re only investing in loan marketplaces such as Lending Club, Prosper and Funding Circle. Because of that, the fund only charges 1.00% of assets under management, and caps fund expenses at 0.59%.

The way Marot tells it, they’re taking the mystery out of a hedge fund. There’s no “black box,” he says. Instead, the fund uses Blockchain technology to deliver a public, unalterable ledger, so that LendingRobot Series investors see exactly which loans the fund is invested, where the defaults are, and exactly what the costs are across the fund.

![]() One of the biggest allures of investing in marketplace loans in this fashion is the liquidity offered. Investors don’t need to wait 3-5 years to wait for the loans to fully mature to take their money out. Investor money is converted to Units of ownership in these Series that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases.

One of the biggest allures of investing in marketplace loans in this fashion is the liquidity offered. Investors don’t need to wait 3-5 years to wait for the loans to fully mature to take their money out. Investor money is converted to Units of ownership in these Series that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases.

Marot said that the company only has 7 employees, yet they’ve managed to rack up more than 6,500 clients (myself among them) for their original service and have helped those clients deploy more than $120 million in assets along the way. They claim that they’ve been able to improve returns in alternative lending by more than 2.5%.

Founded in 2012, the company raised $700K in seed funding and $3M series A from Runa Capital.

As mentioned, LendingRobot Series is available to accredited investors only, and they’ll initially only allow 99 investors to participate in the fund with a minimum investment amount of $100,000.

Why Funding Circle Exited Spain

January 24, 2017

Funding Circle operates in the US, UK, Germany, and the Netherlands. Up until recently, they also counted Spain among its active European markets, but no longer. The timing is curious, right after the company raised $100 million through a round led by Accel, but upon a closer look, Spain was never really their thing to begin with.

“We inherited Spain following our acquisition of Zencap in 2015,” Funding Circle Samir Desai said. “We decided to pause new lending in June last year and we have now taken the formal decision to stop all new loans for the foreseeable future. We continue to invest in Europe in Germany and the Netherlands where we are growing fast, and expect to enter more countries in the future.”

Zencap was once said to be the fastest growing online lending marketplace in Continental Europe. In August 2015, Victory Park Capital had agreed to invest up to €230 million in loans originated by Zencap over a three year period. Funding Circle acquired them a mere two months after that, inheriting their operations in Germany, Spain and the Netherlands.

“Funding Circle will continue working on behalf of all investors to service the existing loan book,” the company said. “In total €16 million of loans have been completed in Spain, which is approximately 0.1% of cumulative global originations. Alternative roles in the company have been offered to the team and the company will retain part of the team to service the existing loans.”

“Funding Circle will continue working on behalf of all investors to service the existing loan book,” the company said. “In total €16 million of loans have been completed in Spain, which is approximately 0.1% of cumulative global originations. Alternative roles in the company have been offered to the team and the company will retain part of the team to service the existing loans.”

Ryan Weeks of AltFi, wrote of the decision to exit Spain, that it was a combination of limited awareness around P2P lending there and low quality loan applicants.

With more resources at their disposal now to focus on Germany and the Netherlands, the company also announced two new senior appointments. Thorsten Seeger has joined as Managing Director for Germany and Belkacem Krimi has joined as Chief Risk Officer for Continental Europe. Thorsten Seeger joins from Lloyds Banking Group, where he was Head of Financial Markets for SMEs and was responsible for driving and delivering access to financial markets for small businesses. Belkacem joins from GE Capital and brings extensive experience in credit risk and operational risk management, developed over 17 years across multiple countries in Europe and Asia. In his last role, he was the CRO for GE Capital France, based out of Paris – managing risk for over $10Bn consumer and commercial assets.

Desai, of Funding Circle, said, “We’re delighted to welcome Thorsten and Belkacem to the team. Both are hugely talented and have extensive experience and understanding of small business lending across Europe.”

But for now, it’s Adios to Spain.

The New Normal

January 24, 2017 In March 2014, I wrote the following for DailyFunder.com: I think we are either currently in, or are fast approaching a “market bubble” in MCA. Bubbles never end well…When I see some of the business practices, offers, terms and other aspects of our business today, I am worried…assets are being overpaid for through higher than economically justified commissions …and [funders are] stretch[ing] the repayment term of the MCA or loan even further. I went on to say that this felt to me an awful lot like the subprime mortgage meltdown of 2008.

In March 2014, I wrote the following for DailyFunder.com: I think we are either currently in, or are fast approaching a “market bubble” in MCA. Bubbles never end well…When I see some of the business practices, offers, terms and other aspects of our business today, I am worried…assets are being overpaid for through higher than economically justified commissions …and [funders are] stretch[ing] the repayment term of the MCA or loan even further. I went on to say that this felt to me an awful lot like the subprime mortgage meltdown of 2008.

Like all good bear market prognosticators, I was a touch early in my forecast. 2014 and 2015 were continued boom years for small business alternative lenders (or “small business Alt Lender.” I don’t agree with applying the moniker “online lender” for our industry. It might be sexy, but it’s not accurate.) Loan and MCA terms got longer, loan pricing to the client dropped further, companies grew 100% year over year. And then 2016 happened.

The most shocking event for me in 2016 was the disruption at CAN Capital. They had the most data, the most experience, market dominance, and the most in-depth institutional knowledge. The granddaddy of all of us. Not far behind is the fiasco that is On Deck, the only publicly traded small business Alt Lender. In the past 12 months alone, the stock price has declined by over 40%. And that is after a roughly 50% drop in stock price in 2015. The first 9 months of 2016, driven in part because of market required changes to their business model when they could no longer profitably sell a sufficient volume of loan originations, they have a GAAP net loss of almost $50 million. There have also been a number of other lesser but still high profile failures, shutdowns, and exits from the industry in the past several months alone.

So what is driving this abnormally high rate of failure in the Alt Lending industry? Is it the “New Normal?” And what do I think lies ahead in 2017 and beyond? Before revealing my personal crystal ball again, I will share an anecdote from earlier in my business career.

I was the CFO (and eventually CEO) of a profitable, long-tenured family owned construction company. We had a working capital credit line from a major bank secured by a first position lien on our accounts receivable. The credit line was also personally guaranteed. We borrowed from the credit line for three reasons. For cash flow, when our receivables paid more slowly than expected; we had tax payments due; or we purchased a large piece of equipment. We always paid back the draw on the credit line as quickly as we could, to keep interests costs low, to impose cash management discipline, and to create future availability on the line once repaid.

The credit line was for one year. It was always renewed. But I was frustrated to have to go through an annual underwrite process with our bank, despite the personal guarantee, consistent profitability, and that we always paid back our draw on the credit line. Our banker (patiently) explained to me that economic cycles changed, and medium sized businesses – we had about 200 employees – suffered ups and downs and sometimes became financially distressed and even went out of business. The bank wanted to protect their position and not overextend the term of the credit line.

The credit line was for one year. It was always renewed. But I was frustrated to have to go through an annual underwrite process with our bank, despite the personal guarantee, consistent profitability, and that we always paid back our draw on the credit line. Our banker (patiently) explained to me that economic cycles changed, and medium sized businesses – we had about 200 employees – suffered ups and downs and sometimes became financially distressed and even went out of business. The bank wanted to protect their position and not overextend the term of the credit line.

When I started RapidAdvance in 2005, I drew on my personal knowledge and previous experience as a borrower. The products we offered made sense based on our customer profile which was main street small business. We needed to protect against economic cycles and the high rate of small business failure. The maximum term offered by any company in 2005 was 8 months, at that time only for an advance product (future purchase and sale of credit card receivables), not a loan. Payment was received daily through a credit card split, thus allowing for a future capital advance (renewal) within about five or six months as the open advance was paid down. Cash advances could be used for taxes, equipment purchases, or business expansion. The price of the product reflected the risk of the credit offered.

What many in the small business Alt Lending industry seem to have forgotten, or never learned, is that our business is fundamentally a subprime credit industry. We are either lending to subprime borrowers, because of either the personal credit of the owner or the balance sheet of the borrower, or if the credit is strong and the business is more substantial, the loan itself is a subprime risk because we are at the bottom of the capital stack – behind the bank loan, the business property mortgage loan, the other personal guarantees of the owner, the factoring company, etc. We are taking the most risk. To offer two and three year terms and to try to pretend to get to “bank like” rates is, in my opinion, committing lending suicide.

At Rapid, we were dragged kicking and screaming into slightly longer term and lower cost products in order to stay competitive with certain customers. But we have kept that pool of customers as a very small percentage of our overall receivables.

Going into 2017 and beyond, I see five major trends. First, terms will get shorter, prices will increase, and offers will become more rational. That is already happening. Second, capital to this industry will become less available. The best companies with proven data driven models, consistent underwriting, a strong balance sheet and predictable loss rates will get financed. The days of easy money chasing this space are over. Equity will be particularly hard to come by.

Third, there will be continued disruption of funding companies. Companies will consolidate and some will disappear. On Deck may be in for a big challenge. They had a tremendous cash burn converting their business model to more balance sheet financed instead of originating and selling loans. Their market cap today is approximately book value, i.e. if you could buy up all the shares of the company at today’s trading price that would be roughly equal to their cash on the balance sheet and the value of their net receivables. The next two quarters are crucial for them to show the market they have turned the corner to become a self-sustaining lender. I am not optimistic, but I am rooting for them to succeed as it is in the best interests of the industry.

Fourth, stacking will continue to be an issue. I believe that the legal system over the next few years will bring some semblance of order to this industry scourge. At Rapid we have taken an aggressive legal stance against stacking, with some success in the courts. The challenge is that each situation is fact specific, and to prevail in a claim of tortious interference, the first position lender has to prove damages. I think that an unrelated decision at the end of 2016, Merchant Funding Services, LLC vs. Volunteer Pharmacy in New York State, could be a game changer. Because of the form of contract and the business practices in Volunteer, the judge ruled that the transaction constituted criminal usury. Knowing the business practices of the stackers, specifically the practice of writing an agreement that pretends to be a sale and purchase of future receivables but is in fact a loan, which is the basis for the judge’s ruling in Volunteer, I can see lawyers seizing on this precedent to help overstressed small business owners attempt to void their stacked loan agreements. The small business would first block the stacker’s ACH, claim the contract is void because of criminal usury, and then sue the stacking company. There could also be class action lawsuits like we saw a few years ago in California – bundle together a number of these claimants and go after the deep pocketed investors and banks that finance the stacking companies. The State’s Attorney General in New York may take a public policy interest in these types of loans. Once the dominoes start to fall, the costs of stacking – litigation and unpaid loans, in addition to proactive claims for damages – could be enormous for both the stacking companies and their owners and investors.

Fourth, stacking will continue to be an issue. I believe that the legal system over the next few years will bring some semblance of order to this industry scourge. At Rapid we have taken an aggressive legal stance against stacking, with some success in the courts. The challenge is that each situation is fact specific, and to prevail in a claim of tortious interference, the first position lender has to prove damages. I think that an unrelated decision at the end of 2016, Merchant Funding Services, LLC vs. Volunteer Pharmacy in New York State, could be a game changer. Because of the form of contract and the business practices in Volunteer, the judge ruled that the transaction constituted criminal usury. Knowing the business practices of the stackers, specifically the practice of writing an agreement that pretends to be a sale and purchase of future receivables but is in fact a loan, which is the basis for the judge’s ruling in Volunteer, I can see lawyers seizing on this precedent to help overstressed small business owners attempt to void their stacked loan agreements. The small business would first block the stacker’s ACH, claim the contract is void because of criminal usury, and then sue the stacking company. There could also be class action lawsuits like we saw a few years ago in California – bundle together a number of these claimants and go after the deep pocketed investors and banks that finance the stacking companies. The State’s Attorney General in New York may take a public policy interest in these types of loans. Once the dominoes start to fall, the costs of stacking – litigation and unpaid loans, in addition to proactive claims for damages – could be enormous for both the stacking companies and their owners and investors.

Lastly, and to my great pleasure, I think we will stop hearing small business Alt Lenders calling themselves “Fintech.” I think we will see the beginning of the demise of fully automated, no manual touch funding. At Rapid we have data and risk and pricing algorithms but we have always had an underwriter at a minimum review every file. At conferences when I have presented or participated in Fintech panels I always referred to Rapid as a technology enabled, non-bank small business lender. Now even On Deck describes themselves in similar terms.

Lastly, and to my great pleasure, I think we will stop hearing small business Alt Lenders calling themselves “Fintech.” I think we will see the beginning of the demise of fully automated, no manual touch funding. At Rapid we have data and risk and pricing algorithms but we have always had an underwriter at a minimum review every file. At conferences when I have presented or participated in Fintech panels I always referred to Rapid as a technology enabled, non-bank small business lender. Now even On Deck describes themselves in similar terms.

I titled this post “The New Normal.” In the classic Mel Brooks movie Young Frankenstein, Dr. Frankenstein sends his assistant Igor to steal a brain from a cadaver to implant into his monster. But Igor accidentally drops the genius brain he was supposed to steal, and brings the doctor a different brain without telling him. When the monster awakes and has the personality of a psychotic five year old, Igor tells him he brought him a brain that was labeled “normal” instead of the one he was supposed to steal. It was, as Igor read it, “Abby Normal.” Abnormal, I believe, is the “New Normal” we will be dealing with in 2017.

Ford Credit and AutoFi Debut Platform for Faster, Smoother, Simpler Digital Vehicle Buying and Financing

January 24, 2017- New platform allows customers to purchase and finance a new vehicle via the dealer website; platform introduced at Ohio dealership and will roll out over time to more U.S. Ford and Lincoln dealerships

- Platform makes it fast and convenient to finance a new Ford or Lincoln at a time when many U.S. adults say they want to spend less time at dealerships, while still going to their dealer to “sign and drive”

- Ford Credit makes equity investment in AutoFi as Ford Credit continues pursuing technology to make the financing experience better

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

In addition, Ford Credit has made an investment in AutoFi as Ford Credit continues pursuing technological advances to make the financing experience better.

“By combining our fast and efficient credit-decision process with AutoFi’s online capability, we are making the customer experience faster, smoother and simpler,” said Lee Jelenic, Ford Credit director of mobility. “With its experience in used-vehicle online financing and well-developed platform, AutoFi makes it easier for us to adopt new technology quickly to meet evolving consumer expectations.”

The AutoFi platform can be used now at Ricart Ford in Groveport, Ohio, and will roll out over time to more Ford and Lincoln dealerships across the United States. The introduction comes as 83 percent of Americans say they would like to spend as little time at the dealership as possible when shopping for or buying a car, according to a new survey of more than 1,000 U.S. adults conducted online by Harris Poll on behalf of Ford Motor Company. Many of those same people, however, still want to touch and feel their new vehicle before signing on the dotted line. The new platform provides the best of both worlds.

Through the dealer website, customers have a transparent and seamless purchase and finance experience from anywhere on their mobile phone, tablet or computer. Once the online part of the transaction is complete, all customers need to do is sign the paperwork when they collect their new Ford.

Consumers may shop for a new Ford in the showroom or from anywhere via the Ricart Ford website. After selecting a vehicle, they can apply for credit and receive a decision, choose the financing terms that make sense for them, and then review and select optional vehicle protection products – completely online on their own time. Customers then can review a final summary of the financing terms and schedule time to complete the transaction and pick up the vehicle.

“AutoFi’s platform will help cut the time people spend arranging financing and improve the experience dealerships can deliver for their customers, no matter where they are in the car-buying journey,” said Kevin Singerman, CEO of San Francisco-based AutoFi. “We think this will be a game changer for both consumers and dealers, and we are thrilled to work with Ford Credit to make this happen.”

“Technology is transforming just about every type of financed consumer purchase, and this new digital capability will help make that change for automotive purchases and deliver great experiences,” said Rick Ricart, Sales and Marketing vice president at Ricart Ford. “We are excited to be the first Ford dealership in the pilot.”

# # #

About Ford Motor Credit Company

Ford Motor Credit Company is a leading automotive financial services company. It provides dealer and customer financing to support the sale of Ford Motor Company products around the world, including through Lincoln Automotive Financial Services in the United States, Canada and China. Ford Credit is a subsidiary of Ford established in 1959. For more information, visit www.fordcredit.com or www.lincolnafs.com.

About AutoFi

AutoFi is a technology company transforming the way cars are bought and sold. The company’s platform allows auto dealers to sell vehicles completely online by connecting buyers with lenders in a fast, easy and transparent process. AutoFi’s team includes industry leaders from enterprise software, finance, automobile and consumer sectors who previously worked at companies including Lending Club, PayPal, and SunGard. AutoFi’s investors include Ford Motor Credit Company, Crosslink Capital, Lerer Hippeau Ventures, Laconia Capital Group, Basset Investment Group, Eniac Ventures, 500 Startups and Silicon Valley Bank. For more information, visit www.autofi.com.

About the Survey

This study was conducted online within the United States by Harris Poll on behalf of Ford Motor Company between November 28 and December 5, 2016, among a nationally representative sample of 1,217 adults ages 18 years and older. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated.

Contacts

Ford Credit

Margaret Mellott

313.322.5393

mmellott@ford.com

or

AutoFi

Justin Hamilton

202.630.5426

Media@autofi.com