Archive for 2017

Re-Banked

April 23, 2017

Just a few years ago, the financial services community was fixing for a battle of David and Goliath proportions—with scrappy, upstart online lenders threatening to rise up and vanquish the fearful and mighty brick and mortar banks. Instead, the unexpected happened: a number of well-respected online lenders and banks set aside their battle arms and began looking for ways to collaborate with their rivals—offloading loans, making referral agreements and establishing more formal partnerships, for example.

“In the real world, sometimes David wins. Sometimes Goliath wins. Just as plausibly, sometimes both sides carve up a market and they often have different offerings that target unique customers,” says Brayden McCarthy, vice president of strategy at Fundera, a New York-based marketplace for small business lending that works with a variety of lenders, including traditional banks.

Certainly, the change didn’t happen overnight. But over time, both online lenders and banks have been forced to tailor their expectations more closely to market realities. Despite their fast growth trajectory, several online lenders have come to realize that they lack several things many banks have, namely a strong, time-tested brand, a solid customer base and ample capital. Banks, meanwhile, have realized that their slow start out of the gate with respect to technology is a severe competitive disadvantage, and that they need more nimble, savvy partners to stay in the game.

Given these shifts, more and more online lenders and banks are taking the approach that if you can’t beat ‘em, join ‘em. Although some industry leaders are actively pursuing strategies that put them in direct competition with banks, partnerships of varying degrees between traditional banks and alternative players are increasingly common. As a result, the lines separating the two are getting increasingly blurry.

“Market forces are acting as a shotgun at the wedding. Whether the two sides are entirely comfortable with the marriage is irrelevant, they need one another,” says Patricia Hewitt, chief executive of PG Research & Advisory Services LLC in Savannah, Georgia. “They’re stronger together than they are alone.”

The evolution of Square is a prime example. The San Francisco-based company really packed a punch in the merchant services world with its mobile card reader designed for small businesses. From there, the payments company sought additional ways to diversify, eventually turning to merchant cash advance as a way to help small business customers obtain funds quickly. Then, in March of last year, Square moved into online lending, teaming up with Celtic Bank of Utah to offer small business loans online. The partnership got off to a running start. In its most recent earnings report, Square said it facilitated 40,000 business loans totaling $248 million in the fourth quarter of 2016—up 68 percent year over year—while maintaining loan default rates at roughly 4 percent.

Even SoFi, the San Francisco-based online lender that has been pointedly outspoken in its anti-bank rhetoric, now has bank-like aspirations. In February, the lender acquired mobile banking startup Zenbanx, giving it the ability to offer checking accounts and credit cards in 2017. Also in February, SoFi teamed up with Promontory Interfinancial Network to enable community banks to purchase super-prime student loans originated by the online lender. Large banks have been buying SoFi loans for several years.

COLLABORATION IS THE WAVE OF THE FUTURE

Many see collaboration between banks and online lenders as a logical step in the industry’s evolution. Online disrupters have forever changed the face of lending—in the same way that online brokerage shaped the financial advisor industry, according to Bill Ullman, chief commercial officer of Orchard Platform.

“There’s a tendency to want to view things as either black or white, online lenders vs. banks. The reality is that the entire financial services industry is undergoing a transformation with technology as the core driver,” he says. “I am of the view that both traditional financial services companies and fintech players can survive and thrive,” Ullman says.

For its part, Orchard recently inked a deal with Sandler O’Neill that provides access to the Orchard platform for the investment bank and brokerage firm’s bank and specialty finance clients. The deal is expected to help small banks better evaluate their options with respect to online lending opportunities.

Partnerships between online lenders and banks take many forms. Some of them are behind the scenes, where marketplaces sell loans to banks or banks informally refer customers. Others are more public. For example, in September 2015, Prosper and Radius Bank of Boston teamed up to offer personal loans to certain customers through the bank’s website using the Prosper platform. Customers can borrow from $2,000 to $35,000 in this manner.

Then in December 2015, JPMorgan Chase and OnDeck joined forces in order to dramatically speed up the process of providing loans to some of the banking giant’s small business customers. In April 2016, Regions Bank and Avant announced a partnership to better serve customers who don’t meet Regions’ credit criteria.

Avant’s customers typically have a credit score between 600 and 700, while Regions sets the bar higher. “The benefit for banks is that they do not need to worry about a platform taking away customers that meet their own credit criteria,” according to Carolyn Blackman Gasbarra, head of public relation at Avant.

She notes that Avant expects to replicate this model with more banks in 2017. “Lately many platforms and banks have come to realize their counterparts are more friend than foe,” she says.

Given the changing tides, industry watchers expect to see more relationships develop between online lenders and banks over time. These could include referral agreements, technology licensing arrangements, formalized revenue-sharing partnerships and perhaps even outright acquisitions.

PARTNERSHIP ADVANTAGES

Certainly, working together can be mutually beneficial for both online lenders and banks. For new online lenders and other fintech players, partnering with an established bank allows them to bypass significant regulatory and compliance hurdles because the necessary requirements are already in place.

“Why jump through all the hoops when you can just have a buddy system with an existing lender?” says Kerri Moriarty, head of company development at Cinch Financial, a Boston-based company dedicated to helping people make smarter investment decisions.

Fintechs that license their technology to banks still have to meet the high standards of third-party vendors determined by bank regulators, notes Stan Orszula, co-head of the fintech team at the Chicago law firm Barack Ferrazzano Kirschbaum & Nagelberg LLP.

“But it’s still less onerous than being a direct lender,” says Orszula, who works closely with banks and fintech providers on legal, regulatory and corporate issues. “They are learning that they need banks. They really do.”

Even seasoned online lenders that have a regulatory framework in place can benefit from bank relationships by using banks’ established brands as leverage. “Everyone knows Chase, Bank of America and American Express,” says McCarthy of Fundera. “They have a solid name and a solid in-built customer base to be able to offer product to them,” he says.

Teaming up with a bank gives added credibility to an online lender, at a time when the public’s confidence has faltered due to highly publicized troubles at certain firms. “Partnering has a very important signaling effect that these online players are here to stay,” McCarthy says.

Banks, meanwhile, need the nimbleness and innovation that online lenders provide. “Banks realize they have to catch up with the fintech disrupters,” says Mark E. Curry, president and chief executive of SOL Partners, which provides strategic management and information technology consulting services to financial services companies.

DIFFERENT TYPES OF PARTNERSHIP OPPORTUNITIES ABOUND

When it comes to partnerships between banks and online players, there are numerous options. In the small business lending space, for example, McCarthy of Fundera says he expects banks to continue buying loans from online lenders, as they have been for many years. He also expects more banks will route declined applicants to online lenders or online loan brokers. “This is a partnership that will allow them to make up some incremental revenue by referring business,” he says.

In addition, McCarthy says he expects banks to make products available through online marketplaces and use an online lender’s technology for online loan applications. He also expects banks will use online lenders’ technology for underwriting and servicing loans.

Years ago, before John Donovan joined Bizfi, he recalls talking to a salesman for a large national bank. The bank didn’t offer a lending product that he could give to small businesses and the salesman was losing customers as a result. “That’s where we see a lot of those opportunities,” says Donovan, chief executive of the online marketplace for small business loans.

For instance in March 2016, Bizfi partnered with Western Independent Bankers, a trade association, for over about 600 community and regional banks, to link small business clients to financing options through Bizfi. Many banks don’t offer small business loans below $150,000, whereas the average loan Bizfi does is $40,000, Donovan says, adding that the company would like to develop additional relationships similar to its agreement with Western Independent Bankers.

In the future, he predicts fintechs will continue to be more receptive to the idea of working with banks and vice versa, as the industry digests the impact of deals that are still in their early days.

FINDING STRATEGIC GROWTH OPPORTUNITIES

As banks and online lenders become increasingly accustomed to working together, there may be more opportunities for strategic acquisitions. For instance, Sandeep Kumar, managing director of Synechron, a global consulting and technology firm, expects to see banks—especially mid-tier players that don’t have the resources to innovate like big banks buying lending-related start-ups. He says banks will likely be most interested in companies that can help them with AI and other techniques to pinpoint where they should spend more efforts on cross-selling and customer profiling, for example. “There are many start-ups in this area that have very compelling technology,” he says.

On the other hand, Chris Skinner, an independent commentator at The Finanser Ltd., a research and consulting firm in London, points out that the two cultures don’t always mesh. “Quite a few startups have young, entrepreneurial founders that would loath the idea being acquired by a bank. So it really depends on the circumstances,” he says.

Valuation differences between large banks and leading online lenders may also be a sticking point for some deals, Ullman of Orchard points out. Banks’ concern over their valuation “will place a certain amount of restraint and discipline on the tech M&A activities they pursue,” he says.

ANTICIPATING TROUBLE IN PARADISE

While increased collaboration between online lenders and banks sounds good on the surface, John Zepecki, group head of product management for lending at D+H in San Francisco, urges both sides to proceed with caution. “You have to find an arrangement where you don’t have conflict,” he says. “If your innovation partner also is a competitor, it’s a challenge. If you have an inherent conflict, it doesn’t get better over time.”

That’s one reason why companies like Chicago-based Akouba have come on the scene. In Akouba’s case, its goal is to provide banks with the technology such that they don’t have to partner with an online lender that has the potential to compete for business. “We don’t compete with the bank in any way whatsoever,” says Chris Rentner, the company’s founder and chief executive.

Akouba’s business lending platform—which the American Bankers Association endorsed in February—provides banks with leading edge technology that integrates the bank’s own unique credit policies into a convenient, online process—from application to documentation— all the way to closing and funding. The bank uses its own credit policies, originates its own loans and owns the entire brand and customer relationship.

Rentner says he started the business with the idea in mind that the online lending model wouldn’t be sustainable long-term and that working alongside banks—as opposed to competing head to head— was the direction to go. “The idea that they could somehow get all of the consumers out of the banking world and onto their platforms was never going to happen. That’s why we exist today,” he says.

FinTech Ventures Fund, LLLP Sheds More Than Half of its Shares in IOU Financial

April 22, 2017FinTech Ventures Fund, LLLP (“FinTech”), a major shareholder of IOU Financial, shed more than half of its holdings in the Canadian-listed company last week. The 7 million shares sold represented nearly 10% of IOU’s outstanding common shares.

According to a statement:

FinTech will review and monitor its options and alternatives with respect to additional acquisitions of Common Shares in light of all relevant factors from time to time, including general market conditions, prevailing market prices for the Common Shares, the business and prospects of IOU and alternative investment opportunities available to FinTech.

Catching Up With Marketplace Lending – A Timeline

April 20, 20172/17

- Prospa, an online small business lender based in Australia, was valued at $235M (AUD) in a $25M capital raise

- Square announced funding $248 million worth of business loans in Q4 2016

2/21 A Massachusetts state court vacated a merchant cash advance COJ

2/24 SoFi raised $500M in a financing round led by Silver Lake Partners that reportedly gave SoFi a $4.3B valuation

2/27 Prosper Marketplace closed a loan purchase agreement with a consortium of lenders for up to $5 billion of loans that has a provision that also enables the lenders to buy up to 35% of the company

2/28 BlueVine secured a warehouse line of up to $75M from Fortress

3/1 Lendio launched a new franchise program, allowing local offices around the country to become Lendio franchisees

3/3 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Marlette Funding for violating the state’s usury cap

3/5 Two trade associations, the Innovative Lending Platform Association (ILPA) and the Coalition for Responsible Business Finance (CRBF), joined forces. The merged company will continue to be known as ILPA

3/6 Upstart raised $32.5M

3/7

- It’s reported that former CAN Capital CFO Aman Verjee is now the COO of 500 Startups

- Kabbage priced a $525M securitization. It was oversubscribed

3/9 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Avant for violating the state’s usury cap

3/13

- Melvin Chasen, the founder of Rewards Network (originally Transmedia Network, Inc.) passed away. He was 88.

- The New York State Assembly rejected the Governor’s proposal to grant the Department of Financial Services (DFS) regulatory authority over any online lender doing business in the state

3/15

- The New York State Senate also rejected the proposal to further regulate lending

- The OCC published a manual on how it will evaluate charter applications from fintech companies

- The New York DFS published a statement rejecting the OCC’s plans

- The WSJ reported that Marlette Funding was cutting nearly 1/5th of its workforce

3/16 WebBank announced that it had a net income of $29.2M for 2016 and that it had a market valuation of $319.4M

3/20 Prosper Marketplace announced that it had originated $2.2B in loans in 2016, down from $3.7B in 2015, and had a net loss of $119M.

3/21 It’s reported that Kabbage will set up its European headquarters in Ireland

3/22 OnDeck expanded its credit facility with Deutsche Bank by $52M to a total of up to $214M

3/27 IOU Financial wins Gold Stevie Award for Best Use of Technology in Customer Service

3/30 In Advance Capital announced that they had secured access to an additional $50M

4/5

- Budget passes in New York. Proposed lending legislation was not included in it.

- Kabbage surpasses $3 billion funded to small businesses

See previous timelines:

12/16/16 – 2/16/17

9/27/16 – 12/16/16

A Tale of “Debt Restructuring”?

April 19, 2017 Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

The very next day, a merchant cash advance (MCA) company sued the merchant in New York for breach of contract, claiming that they were owed more than $300,000. And three months later, the merchant, represented by an attorney named Amos Weinberg, sued the first law firm that they hired. According to that complaint, filed on January 6, 2017, Protection Legal Group never even contacted the MCA company even though they were hired to negotiate with them specifically. Stranger yet, the merchant alleges that Protection Legal Group could not even have defended them in litigation because the MCA agreement’s jurisdiction was New York and Protection Legal Group has no lawyers that are licensed in that state. Naturally, the complaint further alleges that Protection Legal Group accepted payments anyway and has refused to return it.

The merchant’s new attorney, Amos Weinberg, is no friend to MCA companies, according to New York court records. Nevertheless, he offers harsh words for these new purported debt restructuring companies on his blog. “A growing industry that preys on people all over the country who are sued in New York is the debt resolution industry,” he wrote. “These companies promise to settle lawsuits for a portion of the sum sued by inducing the client to stop paying the creditor and instead pay sizeable weekly sums into an escrow account.” He then goes on to call out Protection Legal Group by name.

To summarize, a merchant hired a lawyer for an exorbitant fee to restructure their debts that weren’t debts, got sued and then had to hire a lawyer to sue their lawyer.

Protection Legal Group is also being sued by Forward Financing, an MCA company, for interfering with its contracts. That story has made the news in legal circles.

Court documents show that Protection Legal Group is fighting on another front as well since less than three weeks ago, a class action lawsuit (Case: 1:17-cv-02445) was filed against them for violating the TCPA. According to the complaint, they are allegedly marketing their services via pre-recorded voice messages to cell phones.

As an aside, most MCA contracts already permit merchants to have their payments lowered in the event that their revenues drop. Typically, they just need to send in their recent banking activity to demonstrate the drop and the MCA company will reimburse the merchant for anything collected above the specified percentage of sales. As this is a fundamental part of the agreement, the merchant shouldn’t require a debt negotiator or an expensive attorney to aid them with this.

MCA Case One of the Most Notable of the Year for Factoring Industry

April 17, 2017 At the 2017 Factoring Conference in Fort Worth, TX, industry attorney and talk radio show host Bob Zadek, cited Merchant Cash & Capital, LLC v G&E Asian American Enterprise., Inc. as one of the most notable legal decisions in 2016.

At the 2017 Factoring Conference in Fort Worth, TX, industry attorney and talk radio show host Bob Zadek, cited Merchant Cash & Capital, LLC v G&E Asian American Enterprise., Inc. as one of the most notable legal decisions in 2016.

The contract in question was a purchase of future receivables, i.e. a merchant cash cash advance. A summary of the decision appeared on the Usury Law Blog last year.

During Zadek’s Reports from the Courts session at the conference, he summarized the lessons as follows:

This case is interesting because it appears to confirm that a common contract structure utilized by merchant cash advance companies protects them from usury defenses. When analyzing whether a transaction is usurious, courts look to whether usurious interest is or will be charged to the Borrower from inception of the transaction. Subsequent events do not affect the analysis.

To paraphrase what Zadek also said, the New York Court correctly acknowledged that usury cannot be backwards-looking.

In that case, the MCA company was represented by New York attorney Christopher Murray of Giuliano McDonnell & Perrone, LLP

Marathon Partners Targets OnDeck Capital

April 17, 2017 Marathon Partners, which owns 1.25 million shares of OnDeck Capital, has drawn a line in sand on the shore of the online lender. The private investor is urging OnDeck, whose share price has shed approximately three-quarters of its value since its IPO, to lower its risk profile amid lofty overhead expenses, which Marathon believes are preventing the online lender from achieving real profitability. Marathon has given OnDeck until the company’s annual shareholder meeting in May to respond. Otherwise the investor has vowed to withhold its support for a trio of board members who are up for a vote.

Marathon Partners, which owns 1.25 million shares of OnDeck Capital, has drawn a line in sand on the shore of the online lender. The private investor is urging OnDeck, whose share price has shed approximately three-quarters of its value since its IPO, to lower its risk profile amid lofty overhead expenses, which Marathon believes are preventing the online lender from achieving real profitability. Marathon has given OnDeck until the company’s annual shareholder meeting in May to respond. Otherwise the investor has vowed to withhold its support for a trio of board members who are up for a vote.

“We’re talking about a stock that is down 75 percent to 80 percent from its IPO price. You’re not going to find a lot of happy campers in that situation. Shareholders are going to ask tough questions,” Mario Cibelli, Marathon Partners managing member, told deBanked.

OnDeck Capital, meanwhile, believes it is on the right path for creating greater shareholder value.

“OnDeck welcomes open communications with all stockholders and values constructive input. Members of our board and management team have met with Marathon on several occasions. We are committed to driving value for all OnDeck stockholders and will continue to take actions to achieve this important objective,” said OnDeck’s Jim Larkin.

Indeed Marathon and OnDeck executives have had their share of discussions in the past year, over which time Marathon has acquired its stake and during which time the company’s valuation has become more interesting.

While other institutional investors have been buying shares, evidenced by EJF Capital’s 13-D filing in recent weeks, Marathon — though it has the capital to increase its stake in OnDeck — would not consider doing so with the company’s current risk profile. Marathon Capital’s lack of support for the vote, however, is less a reflection on any one individual and more a protest against the actions or lack thereof of the board as a whole.

“The only way for shareholders to reflect any disappointment or criticism on the proxy is by withholding votes for directors. Instead of picking out one or two of them, we said we’re not going to vote for any of them. This is a clear protest vote for poor performance,” said Cibelli.

Chief among Marathon’s criticisms is an executive compensation structure, including that of CEO Noah Breslow, which omits detail for investors. “There is not a tremendous amount of detail on executive compensation in the proxy, so it’s hard for investors to know what the incentives are that drive the senior management team. The board needs to be very thoughtful around creating the right set of incentives to increase shareholder value,” said Cibelli.

For instance, OnDeck Capital in its quest for profitability points to adjusted EBITDA, which Cibelli said is a “terrible” metric to use to incentivize a management team of a lending business. “It excludes stock-based compensation and depreciation. It also ignores the risk level on the balance sheet. For OnDeck profitability ought to mean GAAP net income,” said Cibelli. “You don’t hear Chase, Wells Fargo or any specialty finance company talking about adjusted EBITDA. GAAP net income is the proper metric and that is what we want OnDeck Capital to achieve.”

For instance, OnDeck Capital in its quest for profitability points to adjusted EBITDA, which Cibelli said is a “terrible” metric to use to incentivize a management team of a lending business. “It excludes stock-based compensation and depreciation. It also ignores the risk level on the balance sheet. For OnDeck profitability ought to mean GAAP net income,” said Cibelli. “You don’t hear Chase, Wells Fargo or any specialty finance company talking about adjusted EBITDA. GAAP net income is the proper metric and that is what we want OnDeck Capital to achieve.”

The murkiness surrounding Breslow’s compensation incentives has been exacerbated by what Cibelli described as an “excessive” overhead structure at the company that amounts to approximately $200 million each year.

“Given the high level of overhead, they have a tremendous amount of pressure on them to maintain and grow the loan portfolio,” said Cibelli, pointing to the company’s lack of profitability. If the company were profitable, Cibelli said OnDeck would start from a very different place when making its loan decisions.

“They would focus more on the quality of loans and interest rates. If OnDeck was profitable today, they might choose to step back from certain types and durations of loans since they would be under far less pressure to grow. Instead they could let the market and their competitive positioning dictate the level of growth,” he said, adding that OnDeck Capital is very challenged to be both prudently leveraged and profitable with its current level of overhead at $200 million.

As for next steps, Marathon Partners, which also wants the online lender to consider a sale of the company, is watching and waiting to see what OnDeck Capital will do.

“The ball is in their court,” said Cibelli. “We will see what they have to say and what they tell shareholders in a couple of weeks on the first quarter call.”

Text The Merchant, Close The Deal

April 15, 2017

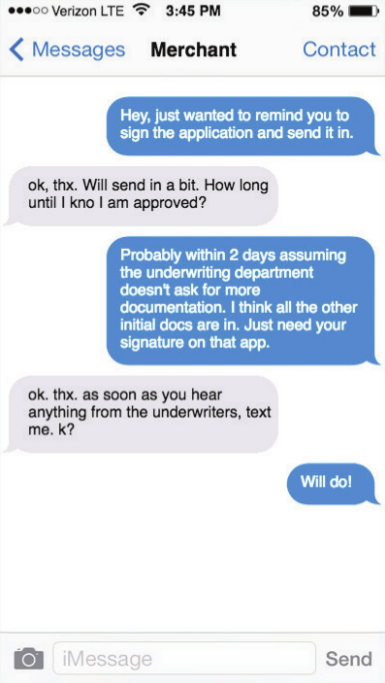

About a year ago, Cheryl Tibbs, general manager of Douglasville, Ga.-based One Stop Funding, was having trouble getting in touch with one of her clients. The merchant in question runs a lawn care service and is usually out on the job, so he isn’t quick to return phone calls or respond to email messages.

“I just got the idea to send a text,” Tibbs recalls. She typed a message expressing her regret for intruding but letting her client know that he needed to take certain steps to advance the funding process for his loan application. He texted right back.

After that initial success, the texting continued between Tibbs and the lawn care provider. He’s been a customer for us for a while, and that’s just how we communicate,” she says. “It’s easy for him to stop and shoot me a text as opposed to having a full conversation with me.”

Tibbs isn’t alone in her appreciation for text messaging as a part of the sales process. Quick responses to texts are making the medium increasingly important in the alternative small-business funding business, maintains Gil Zapata, CEO of Miami-based Lendinero. “Text messaging is more powerful than emailing nowadays,” he declares.

One reason for that shift is that texts are easy to use, according to Tibbs. “It’s a matter of convenience for the merchant,” she contends. “In this business, any way you can make it easier for the merchant to facilitate the transaction with you is the method you have to use.”

Besides the convenience, there’s the sense of urgency people feel when they receive a text, asserts Jeb Blount, a sales trainer who’s written eight sales-oriented books, including the bestselling Fanatical Prospecting. “When you send a text message you move to the top of a person’s priority list,” he says. In fact, people who are talking face-to-face often disengage from the conversation to respond to a text message, he notes. “It’s treated as something that’s urgent.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

Texting has become almost standard procedure at Florida-based Financial Advantage Group LLC, according to Scott Williams, the firm’s managing member. He prefers that sales associates make the initial contact by phone to get a sense of what the merchant is looking for in a funding deal. After gathering information and getting approval, it’s best to send the offer by email so the merchant has “all the numbers in black and white” and more details than a text message can hold, he notes. After that, text messages can deliver requests for additional documentation and provide updates on the progress of the funding process. “We can tell them, ‘Hey, everything got cleared this morning – we should be able to do the funding this afternoon,’” he says.

Texting expedites communication regarding renewals, too, Williams observes. “If a merchant is 50 percent paid back, you can check in and see if they need some additional capital right now,” he says. “It’s really good for that.”

Clients can use messaging to convey images of documents needed in the funding process, Tibbs says. “I had a merchant yesterday who sent me over her IRS tax agreement through picture message,” Tibbs says by way of example. Often, funders request color images of both sides of an applicant’s driver’s license, she notes. To fulfill such requirements, it’s generally easier to snap a photo with a phone and send it as a picture message than to scan pages of paper into a computer to create an electronic document and then send the resulting file by email. “We do a lot with picture messaging,” she observes.

But as useful as text messaging can become for contacting phone-shy clients or helping clients share an image to document a key cancelled check, companies should exercise care when using the medium for prospecting, warns Zapata. He and just about everyone else deBanked consulted emphasizes that sending unsolicited text messages can violate Federal Trade Commission regulations. “Just because our industry isn’t regulated doesn’t mean there aren’t regulations out there on the side,” he says.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

The feds heavily regulate five-digit short-code texts but tread lightly with long-code texts – the ones sent from 10-digit phone numbers, Guggenheim says. The latter would apply in alternative finance, and if a text recipient calls back on the phone number associated with a long-code text, someone will answer, he notes.

Citing guidelines from the Cellular Telecommunications Industry Association (CTIA), Guggenheim stipulates that consumers should have the ability to opt out of additional messages after receiving the first one. Members of the industry who want to send groups of text messages can post conditions on their websites that compel users to grant permission to contact them by text if they submit their contact information, he suggests.

After ensuring everything’s legal, Tucker reports 1st Capital Loans nets a good response when he uses a vendor to blast multiple identical text messages to lists of prospective clients who have already granted permission for his company to contact them by text message. The strategy has helped bring in a reasonable number of deals because the prospects were “already in the pipeline,” he notes.

Remember, though, that cell phone numbers change more often than land line numbers, Tucker cautions. That means a call to a number that’s been reassigned could inadvertently fall into the unsolicited text message category that violates federal rules, he says. “You could be texting a 14-year-old,” instead of a small business, he warns.

When mounting a mass text campaign, marketers are wise to avoid lengthy missives, according to Tibbs. “Keep it simple,” she says. A typical message from her might read: “Looking for funding? Looking for capital? Give us a call,” she notes.

In business texts, avoid acronyms like “LOL” and write in complete sentences with proper punctuation and capitalization, Blount suggests. “Begin by typing out the message somewhere other than in the text box, read it, make sure it makes sense and then send it,” he says. Put your name with the word “from” at the top of the message so the recipient knows who sent it, he emphasizes.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Users can also rely on Guggenheim’s TextUs system to schedule messages for delivery in the future to remind clients of meetings. The system detects land-line numbers and informs the user that the phone will not receive text messages, and it integrates with customer-relationship management systems to exchange information, he says.

So used properly, texting can offer benefits for everyone involved. But some unscrupulous players still insist upon using the medium to mislead prospective clients, says Zapata. His customers have shown him texts from competitors who make initial contact or early contact by sending text messages that might look like offers but are really just marketing letters, says Zapata. That approach, which might tout the availability of $50,000, can cause problems when it turns out that the merchant qualifies for only $25,000, he explains. “Trust me, you’re not going to look like the good guy,” he says of the firms that send what he considers objectionable text messages.

Sensitivity comes into play with text messaging, according to Blount. He and other sources say a great number of people regard email as business-oriented and texts as personal. That leads them to nonchalantly delete unwanted email messages but to become angry when they receive a text they didn’t want, he says. “You can’t send text messages to customers if they don’t know you,” he counsels.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Blount’s example seems to suggest the line between business and personal may be blurring when it comes to texting. People often check their email messages on phones these days – instead of on a laptop or desktop computer – which also minimizes the difference between texting and emailing, says Tibbs. “Everybody does everything with their phone these days,” she notes.

Communicating through a more personal channel such as texting has advantages, too, Williams contends. That’s because some merchants consider their financing to be personal and don’t want to broadcast the details to employees, he says. To protect their privacy, merchants often provide financial institutions with their cell phone number instead of their office number or toll-free line, he notes.

Meanwhile, the world continues to become more comfortable with texting. When Williams and his sales associates began messaging clients about four years ago, they found younger customers receptive and older ones reluctant, he remembers. In the intervening years, however, the 50 plus crowd has warmed to the medium, he observes.

An advantage that accrues with text messaging – compared with email – arises from the fact that spam filters and spam folders don’t seem to have a place in the world of texting. Several sources cite that as a big advantage with using texts. “If you send someone a text message, they’re going to see it,” notes Zapata.

Asked about a downside to the proper use of text messaging in business, most sources could not name one. However, Williams has discovered one area where the mode of communication comes up short. “I would not deliver bad news over text-messaging,” he advises. “If the merchant is upset or frustrated by the news, it would be better-handled in a phone call so you could explain the reason for the negative news. A text message leaves too many things unsaid.”

The Secret to Reviving Your Alternative Lending Business

April 14, 2017 It’s no secret times are changing for Small and Medium Enterprise (SME) lending. I think we can all agree the easy return on investment has given way to rising defaults and an origination engine that sounds like it’s barely chugging along. We all know the basic math in this business. Put lots of money on the street and hope the factor rates cover the losses while managing operating expenses to achieve a rate of return acceptable to private equity investors. So, when originations stall and defaults increase, the math becomes scary.

It’s no secret times are changing for Small and Medium Enterprise (SME) lending. I think we can all agree the easy return on investment has given way to rising defaults and an origination engine that sounds like it’s barely chugging along. We all know the basic math in this business. Put lots of money on the street and hope the factor rates cover the losses while managing operating expenses to achieve a rate of return acceptable to private equity investors. So, when originations stall and defaults increase, the math becomes scary.

As the fintech business leader for DataRobot, the leader in automated machine learning, I’ve had the opportunity to meet many SME business owners at LendIt in New York, and more recently at the Innovate Finance Global Summit in London. It’s very clear interest in machine learning (a branch of artificial intelligence used by many lenders to build risk-based pricing models) is at an all-time high. We’re grateful for the support of our customers, and we take our leadership role in predictive analytics and automated machine learning very seriously. We don’t just see ourselves as a software vendor. We’re innovators that listen intently to our customers (and potential customers), and build solutions that help them achieve their goals. So, when I see this critical juncture in the SME lending industry, I feel compelled to comment.

I believe the response in the industry to the current problem of growing defaults and dwindling originations is the wrong approach. Lenders seem to be doing one of three things (and potentially all of them): lowering underwriting standards, raising factor rates, or pushing independent sales organizations (ISOs) to bring in more applications by handing out one-time commission bumps or in-kind resources such as marketing support. I believe these actions are indicative of lenders who don’t fully realize the wealth of data they have in their companies. Let’s review what I would call a “prototypical” merchant cash advance or business loan lender. First, as Sean Murray, publisher of deBanked, recently pointed out in a LinkedIn post (see, https://www.linkedin.com/feed/update/urn:li:activity:6253411111144685568/), most of the applications lenders receive are of very low quality, and in some cases are fraudulent. This will never be an industry where 50 percent of the applications will result in an offer. From the perspective of someone who talks to lenders almost every day, a company is lucky if 25 percent of its applicant pool can justify an offer. The fact is there just aren’t enough applicants in the industry to force that percentage to go much higher while still maintaining an acceptable default rate. And in terms of default rate, I’d question any lender who says their default rate is single digits. What that leaves us with is the number of applications which are approved and result in a closed deal (i.e., the “win-rate”). And this is where lenders are missing opportunities.

If lenders want to win in this industry, they need to win the right kind of deals that work for their individual business. If all lenders pursue the same strategy of pushing originations and taking on more risks, then many lenders are going to fail because a one-size fits all response to the current funding environment doesn’t work because there is no such thing as a one-size fits all portfolio. For example, if you specialize in “C” and “D” paper in the 3rd or 4th lien position, you want to win deals that look much different than lenders who want “A” paper in the 1st or 2nd lien position. Knowing how to increase your “win-rate” for YOUR type of deals is the key to success. And the key to the lender winning more of their type of deals is being able to understand their underwriting history and immediately spot deals that fit their framework, price them accordingly, and aggressively secure them before the competition. And that only happens if lenders understand their own data and have a risk-based pricing system which is lightning fast and makes the right decisions.

I’m not going to tell every lender to pursue automated machine learning. If a lender is brand-new to the market and isn’t keeping their data for analytical purposes, then deploying advanced machine learning algorithms is an inferior solution to good old-fashioned rules-based underwriting. But for everyone else, here is something you need to know. Many private equity funds are using machine learning algorithms to allocate their investments. It doesn’t take much imagination to consider those funds may start asking themselves why they are using machine learning to allocate their investments to companies not using machine learning to manage their risk exposure. The key to achieving success in a tightening market such as SME lending is to intimately understand your business. There is no more room for one-size fits all strategies. Consider what would happen if you simply doubled your “win-rate” for the deals that fit your business without looking at more applications? You would start spending a lot less time beating the originations drum and have more time to deliver superior customer service to increase your renewal rate. Automated machine learning can make that happen.