Archive for 2017

Reaction to Lending Club’s New Credit Model

September 13, 2017The few retail investors discussing the recent change Lending Club made to their credit model weren’t exactly optimistic, according to comments on the Lend Academy forum. Of particular concern is grade inflation wherein borrowers who previously scored a C or lower may now find themselves in the A or B category.

“We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model,” Lending Club stated in an email last week.

Retail investor sentiment may not be all that important, however, as capital from self-managed accounts on the platform has waned after peaking in the first quarter of 2016. In Q2 of 2017, self-managed accounts only accounted for 13% of the capital used to fund loans. The majority came from banks and institutions.

LeaseQ and ARF Financial Partner to Automate Hospitality Equipment Financing

September 12, 2017BOSTON (Sept. 12, 2017) – LeaseQ, an online marketplace connecting business owners, equipment sellers, and lenders to make selling and financing equipment fast and easy, today announced a national partnership with ARF Financial, the only FDIC-compliant financial lender that provides short-term, unsecured business loans and lines of credit for restaurant/hospitality business owners and retailers nationwide.

“We are unique in having our own sales organization, and LeaseQ gives our loan consultants around the country a lease product with instant quotes,” ARF Financial CEO Steve Glenn said. “Now we are a one stop lender offering additional products to satisfy our customers funding needs for their businesses.”

Innovations in the equipment finance industry will continue to increase flexibility and convenience for customers, according to the Equipment Leasing and Finance Association’s (ELFA) Top 10 Equipment Acquisition Trends for 2017. Automation fuels advances in instant quotes, soft credit pulls, same-day approvals, one-day funding and blockchain for secure, multi-party transactions – many of which are available today through LeaseQ and ARF Financial.

“You can finance a car in an hour, but not a walk-in freezer to start or expand a restaurant,” said Vernon Tirey, co-founder and CEO of LeaseQ. “One-day funding is a trendy thing to say in equipment financing, but when the restauranteur or hotel manager presses the button to get financing, it has to work. We’re advancing our technology and partnering with lenders like ARF Financial who understand the value of automation to make it happen.”

LeaseQ and ARF Financial offer automated, flexible equipment financing for hospitality merchants who are frustrated with the time it takes to get a bank loan, or who cannot get a bank loan at all, including those:

- Expanding a facility

- Upgrading equipment

- Adding a location and renovating the property

- Managing working capital, and more

There are currently 150 lenders on the LeaseQ platform serving 28 vertical markets. Learn more at www.leaseq.com.

About LeaseQ

LeaseQ is an online marketplace connecting businesses, equipment sellers, and equipment finance companies to make selling and financing equipment fast and easy. The LeaseQ platform is a free, cloud-based SaaS solution with a suite of on-demand software and data solutions for the equipment leasing industry. LeaseQ provides business process optimization (BPO) and information services that streamline the purchase and financing of business equipment across a broad array of vertical industry segments. Learn more at www.leaseq.com.

About ARF Financial

ARF Financial LLC is a California licensed lender that sources short-term business loans and lines of credit for restaurant/hospitality and retail merchants nationwide. Since 2001, ARF has filled the void between traditional bank financing and less attractive venues of obtaining capital, giving merchants the ability to maintain control of their business, be more profitable and meet their financial goals. The company is managed and staffed by industry veterans with extensive experience in restaurant finance and small to medium retail industries.

For more information on their services, visit their website at www.arffinancial.com. You may fill out their contact form at www.arffinancial.com/contact, call 1-866-702-4430, or send an email to funding@arffinancial.com for inquiries.

Senate Banking Committee to Hold Hearing on Fintech

September 12, 2017The US Senate Committee on Banking, Housing, & Urban Affairs held a hearing entitled “Examining the Fintech Landscape” on Tuesday morning at 10 AM.

You can watch it below

The witnesses include:

Mr. Lawrance Evans

Director, Financial Markets

U.S. Government Accountability Office

Mr. Eric Turner

Research Analysis

S&P Global Market Intelligence

Mr. Frank Pasquale

Professor of Law

University of Maryland Francis King Carey School of Law

Lending Club Launches Its Most Advanced Credit Model Ever

September 11, 2017Lending Club is feeling pretty good about its newest credit model, according to an email that circulated to retail investors this morning. A copy of it is below:

We have launched the most advanced and predictive credit model ever used on the LendingClub platform. It’s the latest in LendingClub’s long history of innovation on behalf of borrowers and investors.

The new model leverages machine learning and 10 years of LendingClub data to better assess and price credit risk. LendingClub has helped 1.5+ million borrowers since 2007; each borrower provides unique insight that we can use in our next decision.

What investors need to know about the new credit model:

• It’s 24% better at differentiating the likelihood of a borrower charging off than the fourth-generation model, and is more predictive than a borrower’s FICO score alone.

• It’s built on a wealth of proprietary data, incorporates more data points for each borrower, uses best-in-class modeling techniques, and uses dozens of new custom attributes that are predictive in assessing risk.

• We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model, and other higher-risk borrowers, who may have received an offer previously, will be screened out.

• We continue to see lower delinquency rates across grades and terms in the existing loan portfolio than in the second and third quarters of 2016.

We see this credit model as the latest innovation in our continuous enhancement cycle, and one that helps us continue to provide investors with solid risk-adjusted returns. See here for more on what makes the model unique.

Alternative Finance Bar Association Event is Wednesday

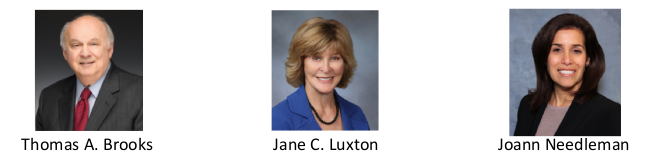

September 10, 2017If you’re interested in going, the Alternative Finance Bar Association event on Wednesday is open to both funding company executives and industry attorneys. The New Regulatory Challenges Facing Small Business Lending: Navigating the New Frontier will feature Joann Needleman, Esq., Jane Luxton, Esq. & Tommy Brooks, Esq. from Clark Hill PLC in the NYC Bar Association Offices on 42 West 44th Street in New York City.

To register or for more information, contact Tiffany Diaz at Tiffany@LRohanlaw.com.

The original announcement can be accessed here.

SOS Capital Offers Super Bowl Tickets As Part of Charity-Driven Football Contest

September 10, 2017 Think you’re good at NFL predictions? SOS Capital is offering anyone the chance to win Super Bowl tickets in their football eliminator contest. The entry fee is a $100 donation to the JJ Watt Foundation to support Hurricane Harvey flood relief in Houston, TX.

Think you’re good at NFL predictions? SOS Capital is offering anyone the chance to win Super Bowl tickets in their football eliminator contest. The entry fee is a $100 donation to the JJ Watt Foundation to support Hurricane Harvey flood relief in Houston, TX.

Pool Details:

- $100 Donation Entry Fee

- Winner Receives 2 Super Bowl Tickets- Courtesy of SOS Capital

- 100% of proceeds will be donated to JJ Watts Charity

- Unlimited Entries Allowed

- Kicks Off Week 2 of the NFL Season

- Deadline to enter is Thursday Sept 14th 2pm

Contact SOS Capital for details on how to join and donate. Call 212-235-5455 or email Charity@soscapital.com

I have already made my donation to the JJ Watt Foundation and joined. I hope to see many others of you in the contest!

ShopKeep Joins the MCA Crowd. Are Loans Next?

September 8, 2017

ShopKeep, an iPad-based cloud-connected technology company designed around POS and payments for small businesses, is expanding into MCAs with the launch of ShopKeep Capital in recent days. With its move into funding ShopKeep joins an area that competitor Square already operates in. But while both companies have unlocked the secret of customer acquisition they are not targeting the same small businesses.

Meanwhile this latest move into MCAs is just a step in what ShopKeep CEO Michael DeSimone describes as an evolution, one that could potentially lead to small business lending sooner than later.

“We had a lot of interest from our customers,” said DeSimone, referring to the nearly 25,000 small businesses that are on ShopKeep’s payment and software platform. ShopKeep Capital extends funding offers to eligible small businesses on the ShopKeep platform, and funding is approved within a couple of days.

Playing Field

ShopKeep is entering a space – MCAs — that is only getting more crowded, with the recent addition of iPayment, for instance. And while ShopKeep and Square operate in a similar market segment, they’re targeting different SMBs.

“Our customers tend to be larger than Square and more complex in their business models,” said DeSimone, pointing to the example of a restaurant with numerous employees and multiple locations. On average, customers on the ShopKeep platform generate sales of $350,000 per year.

As a payments company, ShopKeep’s customer acquisition strategy is tied directly to its software and payments businesses.

“This leverages our ability to understand the small business data flowing through our POS platform and manage it the way we do payments based on the premise of greater visibility into their business by the virtue of our payments platform,” said DeSimone.

He is quick to point out that ShopKeep is built on technology, and he said like every other part of the economy tech is disintermediating some parties and bringing others closer to the outcome they desire.

“The closer you are to the actual customer, the more your opportunity is to be able to be top of mind when they need something,” he said. “They have huge amounts of interaction with us. This level of interaction predicated on technology is really what creates the ability to have a relationship with the merchant to then be able to offer them a range of different products and services.”

DeSimone describes ShopKeep more as a technology play than a funder.

DeSimone describes ShopKeep more as a technology play than a funder.

“We have a lot of information most other providers of capital aren’t going to have unless they ask merchants to do a lot of work,” said DeSimone, pointing to an underwriting model that is almost 100% automated.

“We’ve built it to be largely pre-underwritten We only offer advances based on running the merchant through our underwriting model to see who comes up as a good candidate for ShopKeep Capital and making it available to them. We continually tweak the algorithm to make sure we are not being too tight or too loose,” he added.

Funding is the third revenue stream for ShopKeep, with software and payments representing the other two legs of the revenue stool. Meanwhile ShopKeep Capital is turning to its balance sheet to fund MCAs, but that is not the long-term plan.

“Currently it’s coming off our balance sheet, but it won’t be for very long. We have had several discussions with funding partners. And we expect over time we will migrate to more of a loan product and away from MCAs. We will explore the features and benefits of both to understand both our perspective and that of our customers,” said DeSimone, adding that there could be more clarity about the direction of this evolution in the next six months.

If ShopKeep does move into loans, the company could open up the platform to investors. “They are debt funds looking for returns and specific underwriting criteria. They will buy an advance or a loan eventually from what we originate. That’s the model we think we’ll go toward,” he said.

Something DeSimone and other lenders might want to keep in mind is a credit gap that exists among small businesses today, as described by Karen Mills, a senior fellow at Harvard Business School and former administrator of the U.S. SBA.

“There is no doubt that online lenders have identified an important segment that is not getting enough access to credit, but data also shows that borrowers are less satisfied with the interest rates and repayment terms from online lenders than from traditional banks. So even if small businesses are getting the loan, if it is not at an appropriate price, we should still consider this a credit gap,” Mills said.

Future Plans

While loans could be the next growth phase for ShopKeep Capital, this could be one of many new directions that the payments company takes. For instance, with key competitor Square, which boasts a market cap of approximately $10 billion, in pursuit of obtaining a bank charter, they could have company someday.

“It’s an interesting idea. It’s still very early for us but we’re not ruling anything out at this point,” DeSimone said.

For the near term, however, he is focused on ShopKeep Capital, for which he expects to make a couple of key hires for soon. “In my mind, this helps us to be more competitive with Square. I think it’s a really good service for our customers and it fits very well into the other pieces of our business,” said DeSimone.

Amos Weinberg and Creditors Relief Are Battling it Out

September 8, 2017A lawsuit filed by a small business against Creditors Relief in April has gone off the rails, according to court documents. Creditors Relief has sought to dismiss the case that attorney Amos Weinberg brought on behalf of a Deli in New York that alleged among other things, that Creditors Relief practiced law without a license and reneged on a contract to settle its debts.

While both sides were disputing the facts, Weinberg suddenly withdrew the complaint on September 1st, a move which did not actually bring the matter to a resolution. Instead, Creditors Relief has still asked the court to dismiss the case with prejudice and to sanction Amos Weinberg for the frivolous pleading in the first place. In its papers, Creditors Relief argues that the lawsuit was brought primarily to harass Creditors Relief and its owner Michael Lupolover and that the complaint asserted material factual statements that were false.

Across the docket, Weinberg attached documents that exposed Lupolover’s previous snafu with a federal regulator while Creditors Relief later filed an exhibit showing that Weinberg had been sanctioned in another lawsuit.

The case is still active with the motion to dismiss and sanction still pending in the New York Supreme Court under index number: 56406/2017 Natures Market Corp v. Creditors Relief LLC