Story Series: Section 1071

Greenbox Capital on Official Panel to Aid Section 1071’s Rollout

October 21, 2020 This week, Greenbox Capital, the Miami-based alternative finance company known for its MCA and SMB financing, announced they are serving as a Small Entity Representative (SER) to the Consumer Financial Protection Bureau (CFPB) as the organization proceeds with the rollout of Section 1071 of the Dodd-Frank Act.

This week, Greenbox Capital, the Miami-based alternative finance company known for its MCA and SMB financing, announced they are serving as a Small Entity Representative (SER) to the Consumer Financial Protection Bureau (CFPB) as the organization proceeds with the rollout of Section 1071 of the Dodd-Frank Act.

“I am representing, and Greenbox Capital is essentially representing, the industry,” CEO Jordan Fein said. “There are some banks, there’s Funding Circle, but other than that, it’s Greenbox Capital serving in the industry.”

Fein, who founded Greenbox in 2012 and has since facilitated MCAs and business loans across America, Puerto Rico, and Canada, wrote in a press release that it was an honor to be selected to provide feedback on Section 1071.

“Over 2 million businesses across the U.S. are either women or minority-owned,” Fein wrote. “It is vital they can secure funding as easily as non-minority-owned businesses.”

Congress passed the Dodd-Frank Act in 2010 in response to the Great Recession. To further protect consumers, the CFPB was born. Section 1071, an amendment to the 1974 Equal Credit Opportunity Act, mandates financial institutions report demographic information to the CFPB. But much was left undefined about how to go about doing that and who would technically be subject to it.

Ultimately, the intent behind the law was to measure potential disparities among factors like the race and gender of applicants. Ten years later, the rollout is finally moving along.

As part of this, the CFPB created a board of firms representing the affected industry, on which Greenbox sits, to ensure the law works with the industry, not against it. The first panel was on October 15, in compliance with the 1996 Small Business Regulatory Enforcement Fairness Act (SBREFA.)

“They’re going through the SBREFA process, which is a structured process where they have a panel of industry representatives, and they share what they’re planning to do,” Fein said. “They run it by companies like us and we give our opinion and talk about how we think companies will be impacted.”

According to an invitation letter the firms received, they will have until November 9 to respond.

Fein said Greenbox would ensure any suggestions it made would positively impact the industry. Especially during a pandemic, Fein said it is essential to create regulation with firms in mind.

Section 1071 is Back and The CFPB Wants to Know How Much It Will Cost You to Comply

August 25, 2020 At some point in this century, small business finance companies will be expected to comply with Section 1071 of the Wall Street Reform and Consumer Protection Act that was passed in 2010.

At some point in this century, small business finance companies will be expected to comply with Section 1071 of the Wall Street Reform and Consumer Protection Act that was passed in 2010.

In the wake of the ’08-’09 financial crisis (remember that?!), lawmakers passed the above act that has become colloquially known as Dodd-Frank. Section 1071 gave the Consumer Financial Protection Bureau the authority and the mandate to collect data from small business lenders (and similar companies).

The costs, risks, and challenges with rolling out this law have been discussed on deBanked for 5 years, yet little progress has been made to finally implement it. But it’s starting to move along and the CFPB would now like to know how expensive it will be for businesses to comply.

If you are engaged in small business finance, you should seriously consider submitting a response to their survey. The CFPB is specifically cataloging responses from merchant cash advance companies, fintech lenders, and equipment financiers.

Dodd-Frank’s Small Business Lending Data Collection Rule Could Still Take Years to Implement

January 12, 2020Small business lenders: Are you ready to regularly submit loan application data to the Consumer Financial Protection Bureau? No? Good, because almost ten years after Dodd-Frank passed, the provision that requires the CFPB to collect small business lending data still hasn’t been implemented.

And apparently we’re still years away.

Section 1071, as it’s known, modified the Equal Credit Opportunity Act and defined a small business lender as any company that engages in any financial activity. So if you’re wondering if this thing even applies to whatever you do in your corner of small business finance, it probably does.

The rule has taken so long to implement that consumer advocacy groups have actually sued the CFPB over the delay. The CFPB took note followed by initiative and hosted a symposium late last year to discuss how it might go forward. The next steps from here are to convene a panel of small business lenders, have that panel issue a report, propose what the rules on collection will be, collect feedback on the proposal, formulate a final rule, issue a rule, and then set a time for when it will go into effect. That process could mean that the earliest that data collection takes place is in 2023, possibly even longer as the entire financial services industry may need time to develop the infrastructure and human resources to comply.

Beyond that, advocates and critics of Section 1071 do not even entirely agree on what purpose data collection will even serve. Some believe the intent is merely for the government to have access to data it otherwise might not have while others believe that the CFPB could use statistics it deems discriminatory to bring enforcement actions against financial institutions. Sounds like we could use a few more years to get on the same page…

A recording of the 2019 Symposium is below:

CFPB’s Small Business Lending RFI is Now Closed

September 18, 2017The window to share your two cents on the CFPB’s quest to collect data on small business lending has closed. The extended deadline to respond to the RFI was September 14th.

The agency received 2,668 comments, 650 of which you can read online. Most responses that deBanked reviewed asked the CFPB to exempt certain businesses such as community banks from the law. Others denounced the CFPB’s objective as misguided or poorly thought-out from the get-go.

Nevertheless, Section 1071 of the 2009 Wall Street Reform and Consumer Protection Act directed the CFPB to collect data on small business lending presumably to determine if women and minorities are treated differently.

Some observers expected this initiative to be derailed when Richard Cordray, the Director of the CFPB, resigned to campaign for Governor of Ohio. However, the governor’s race is now in full swing and he has yet to resign, and could now possibly remain in his position until it expires next year.

The implementation of any resulting rule from the RFI would likely not take place until some time in the 2020s, sources contend.

Was Section 1071 of Dodd-Frank a Massive Mistake?

August 23, 2017Did Congress make a huge mistake by thinking small business loans were easily commoditized?

Pursuant to Section 1071 of Dodd-Frank, the CFPB is planning to collect data from companies engaged in small business finance in order to potentially screen for discrimination against women and minorities. Before deciding how exactly they’re going to do that, they’ve asked the public for comment, and the public… isn’t showing the law much love. Below are some excerpts of the nearly 300 responses already submitted.

We can tell all the stories we want, and hold all the hearings imaginable, and there is still no way to disguise the fact that implementing a HMDA-like reporting requirement will add cost, complexity, and rigidity to our amazingly customized lending

– Alan Gay

A loan priced properly for the risk may be acceptable for one institution and not acceptable to another. For example a client requests funds to open their second doughnut shop in town. One bank declines the loan because they do not specialize in food service business per lending policy and the banks appetite for risk. Another bank would consider the loan, however after reviewing the current competition decides that the market is saturated and the loan is too risky based on the three competitors within five miles. The third bank is willing to loan the money based on the cash flow of the owner and her husband, but will not take into account the expected cash flow from the business, and will require the collateral to include the primary residence of the client. The fourth bank is an SBA lender and proposes the client use the SBA program to mitigate the risk for the bank. The fifth bank declines the loan due to cash flows. They will not consider the revenues from the new location, because it is considered a start-up business. As I understand it the CFPB will collect the data from all five banks to determine “Fair Lending” similar to the consumer lending program. I find this problematic on many levels: I believe in the scenario presented all the lenders were fair. The data is redundant and will not show the result of credit search on the commercial loan request or accurate results.

– Doug Mitchell

Creating additional documentation and regulation only makes those in Congress and the CFPB feel better without truly adding benefit to our community and it’s businesses.

– Joseph Williams

COLLECTING AND AGGREGATING THIS INFORMATION WOULD BE A BURDEN THAT WOULD REQUIRE ADDITIONAL STAFF AND NOT CHANGE OUR HISTORY AND BUSINESS MANDATE OF SERVING OUR SMALL TOWN BUSINESSES.

– Dee Baertsch

As a community banker in rural Ohio I strongly urge the repeal of Section 1071 of the Dodd-Frank Act. The addition of another report will be counterproductive to lending to small businesses.

– Chuck Dixon

Commercial lending is a completely different animal from consumer lending, and has so many different aspects to consider. While a consumer loan is typically viewed from and ability and intent to pay by reviewing a consumer credit score and debt to income calculation, a commercial loan is viewed from not only current earnings but also projected earnings, the economic conditions surrounding the specific business/industry, competitiveness in the market, and the speed of obsolescence of the business’ products and services. It is so much more than pulling a credit report and getting the last two pay stubs.

– Brian Smith

The Race and Sex questions should be eliminated from all loans.

– David Ludwig

Our bank in particular will be unduly burdened by small business lending data collection.

– Casey D. Lewis, CRCM, First Bank & Trust

This new requirement will place a large burden on our small bank and staff as more time will be spent on data collection and reporting rather than giving the value added service to our actual customers. It also may increase the cost of credit to our borrowers in order to offset the increased compliance cost to comply.

– Anita Drentlaw

These regulation proposed by the CFPB will only act to hamper and restrict our ability to continue meet the credit need of our communities and will not provide any meaningful benefit to anyone.

– Jim Goetz

Adding new requirements to collect and report data related to these loans much like HMDA diverts time of our limited staff away from serving our customer needs and expends resources that do not help our community.

– James Milroy

The last thing I need is to spend even more of my time collecting data similar to the HMDA data we collect on other loans. It is a timely, costly and inefficient use of our resources which could be better utilized for spending more time with potential and current customers and lowering their interest rates. Very few businesses are the same which would lead to misrepresentation and baseless fair lending complaints.

– Daniel Mueller

By making our jobs harder, you are making it harder for small businesses to thrive.

– Joy Blum

I have seen first hand the negative effects of the HMDA collection and reporting to our bank. The increased work for our small bank has driven up our costs and is making it harder for us to compete. In addition to the negative impact on our bank mortgage customers pay a cost and as more and more community banks decide they can no longer provide these services the community will be left with fewer options.

– Jeff Southcott

Stop all the paper work to get a commercial loan. Enough is Enough!

– Jeff Spitzack

We are a small $65 Million dollar bank with limited personnel now being asked to police another segment of our customer base. We do not have the resources to carry out more regulatory burden.

– Girard J. Hoel, Chairman, The Miners National Bank of Eveleth

Commercial lending cannot be “commoditized” in the way that consumer lending can, nor can it be subject to simplified, rigid analysis which may generate baseless fair lending complaints.

– Steve Worrell

We are so heavily burdened with keeping up with all the changing regulations and requirements, it would be very burdensome for not only our bank, but many other community banks. There has to be a way to ensure the end results that you are looking to achieve without making it so hard on Community Banks. We feel that we have to really analyze if it is cost prohibitive to actually make the loan – and how does that help the small businesses?

– Margi Fleming

We would never decline a profit making loan because of the race or sex of the applicant. You would be appalled to know how little attention borrowers pay to the dozens of pages of disclosures required by regulation. Over disclosure is no disclosure.

– Douglas Krogh

Community banks simply do not have numbers on our side, either in manpower or funding, to seamlessly and efficiently absorb the vast and sweeping regulatory changes.

– Cheryl Hiller, 1st National Bank of Scotia

The new data collection will add additional staff at our institution. This salary will be passed on in the form of origination fees or increased rates to our small business customers. This is not fair to them, but with the increased regulatory demands by the CFPB on small business lending if this is adopted will increase their borrowing cost.

– Russell Laffitte

The burden of data collection and reporting would in effect end up costing our customers more to get a loan.

– Shannon Fuller

This tracking will be onerous on a small bank that stays competitive by maintaining a small staff like ours

– Jim Legare

Section 1071 will have a chilling effect on lenders’ ability to price for risk. This, in addition to the expense of data collection and reporting, may impact community banks’ ability to provide affordable commercial lending products and curb access to small business credit, an engine of local economic growth and job creation.

– Freeman Park

Please make every effort to prevent the added burden to small business lending and community bank processes by repealing Section 1071 of the Dodd Frank Act.

– Julie Goll

Puerto Rico Bankers Association Calls Section 1071 Absurd and Unreasonable

June 28, 2017Section 1071, the law that grants the CFPB authority to collect loan application data on minority and women-owned businesses, is under fire, again. This time it’s the Puerto Rico Bankers Association in response to the CFPB’s RFI on the matter. In a letter, the PRBA points out the sheer irony of conducting costly disparate impact studies on minorities in minority-only communities.

An excerpt from their statement:

According to the 2010 US Census Bureau, 99% of the population of Puerto Rico is Hispanic.

[…]

The direct and evident effect of Section 704B of ECOA for the financial institutions in Puerto Rico will inevitably be the collection, recordkeeping and reporting of virtually all commercial loan applications received within the Puerto Rico marketplace, since most of such applicants would be regarded as “Minority Owned Business”, in accordance with Section 704B.

The PRBA believes that this absurd and unreasonable result must not have been intended by Congress when it enacted Section 1071 of the Dodd-Frank Act. The data so collected, maintained and reported will not serve the purposes for with Section 1071 was enacted since, for the reasons set forth above, it will be completely inaccurate and unreliable. The potential complexity and cost of compliance with the minority-owned businesses data collection and reporting requirements of Section 704(B), will impose on our banks an unintended and unreasonable burden.

Other responses to the CFPB’s RFI have so far called Section 1071, “literally impossible to comply with” and a duplicated effort.

US Treasury Calls for Section 1071 to Be Repealed

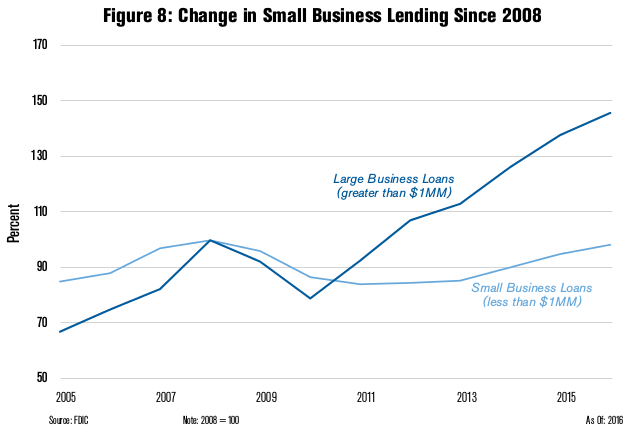

June 19, 2017In a 149-page report prepared for President Trump, the US Treasury has called for the repeal of Section 1071 of Dodd-Frank. Section 1071 is the governing law behind the CFPB’s jump into small business lending data collection. Citing the cost of data collection and anemic small business loan growth since 2008, the Treasury says, “Although financial institutions are not currently required to gather such information [required by the law], many lenders have expressed concern that this requirement will be costly to implement, will directly contribute to higher small business borrowing costs, and reduce access to small business loans.”

“THE PROVISIONS IN THIS SECTION OF DODD-FRANK PERTAINING TO SMALL BUSINESSES SHOULD BE REPEALED TO ENSURE THAT THE INTENDED BENEFITS DO NOT INADVERTENTLY REDUCE THE ABILITY OF SMALL BUSINESSES TO ACCESS CREDIT AT A REASONABLE COST” – US Treasury

The current deadline to reply to the CFPB’s Request For Information is July 14th though industry sources expect the deadline will be pushed back. Of course, if Section 1071 were successfully repealed, the RFI would be moot.

The Choice Act, a bill that just passed the House of Representatives, does indeed repeal Section 1071, but industry sources following the legislation believe the bill will die in the Senate.

Even if a repeal never happens, it is possible that regulations pursuant to Section 1071 may not even go into effect until the early 2020s if similar rulemaking trajectories are to be used as a guide. With payday lending, for example, the CFPB RFI on the matter ended in early 2012 but to-date there still has been no final rule.

What You Need to Know About The CFPB and Small Business Lending

May 10, 2017

On Wednesday, the Consumer Financial Protection Bureau (CFPB) held a hearing on small business lending. Here’s why it mattered and what you need to know:

Why: The 2010 Wall Street Reform and Consumer Protection Act, aka Dodd-Frank, empowered the CFPB to collect data on small business lending. The CFPB is just now getting around to rolling this out. The purpose is to facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority-owned, and small businesses. In short, to determine if women and minority-owned businesses are operating on a level-playing field when it comes to accessing credit.

Who: “I’m an MCA funder, factor, equipment lessor or other, and this only applies to lenders right”?

Maybe, maybe not. Although Section 1071 makes several references to loans and credit, it doesn’t refer to the companies subject to data collection as small business lenders. Instead it says financial institutions which it defines as “any partnership, company, corporation, association (incorporated or unincorporated), trust, estate, cooperative organization, or other entity that engages in any financial activity.” That sounds incredibly broad.

What: What are they trying to collect?

- the number of the application and the date on which the application was received;

- the type and purpose of the loan or other credit being applied for;

- the amount of the credit or credit limit applied for, and the amount of the credit transaction or the credit limit approved for such applicant;

- the type of action taken with respect to such application, and the date of such action;

- the census tract in which is located the principal place of business of the women-owned, minority-owned, or small business loan applicant;

- the gross annual revenue of the business in the last fiscal year of the women-owned, minority-owned, or small business loan applicant preceding the date of the application;

- the race, sex, and ethnicity of the principal owners of the business; and

- any additional data that the Bureau determines would aid in fulfilling the purposes of this section.

How: Great question. The law says that where feasible the underwriter or analyst isn’t allowed to know if the business is woman-owned or minority-owned and that this information must be captured separately and kept secret from the underwriter. The section is actually called the “NO ACCESS BY UNDERWRITERS” section. Oddly, as this applies to all small business lending, not just faceless transactions, one wonders how an underwriter is supposed to avoid discovering the gender or ethnicity of the applicant. It is possible that in 2009 when this section was drafted, the architects could not imagine a business lending universe that looked beyond FICO scores and balance sheets.

When: It’s still early days. Right now the CFPB just wants to know everything about what these “financial institutions” do and how they do it before they start requiring the data be collected. To that end, they’ve published a Request For Information, seeking voluntary responses so that they can start formulating the data collection framework in a way they believe best.

Where: Where can you read and watch more about this? We’ve got some information on this page here, including a video of the hearing.

What should I do? Should I do anything?

Join an industry trade association. When it came to the proposed regulation in New York, they did most of the heavy lifting. There are many to choose from depending on your business model. In New York though, the regulations were purely proposed. Under Dodd-Frank, the CFPB already has the power to collect data. They’re just finally getting around to using it.